China Resources Beer (Holdings) Boston Consulting Group Matrix

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

China Resources Beer (Holdings) Bundle

Unlock Strategic Clarity

China Resources Beer (Holdings) operates in a dynamic beverage market, and understanding its product portfolio through the BCG Matrix is crucial for strategic decision-making. This analysis helps identify which brands are driving growth and which may require a strategic re-evaluation.

Uncover the full potential of China Resources Beer's product lineup with our comprehensive BCG Matrix. Gain clarity on your "Stars," optimize your "Cash Cows," and make informed decisions about your "Dogs" and "Question Marks." Purchase the complete report for actionable insights and a strategic roadmap to navigate this competitive landscape.

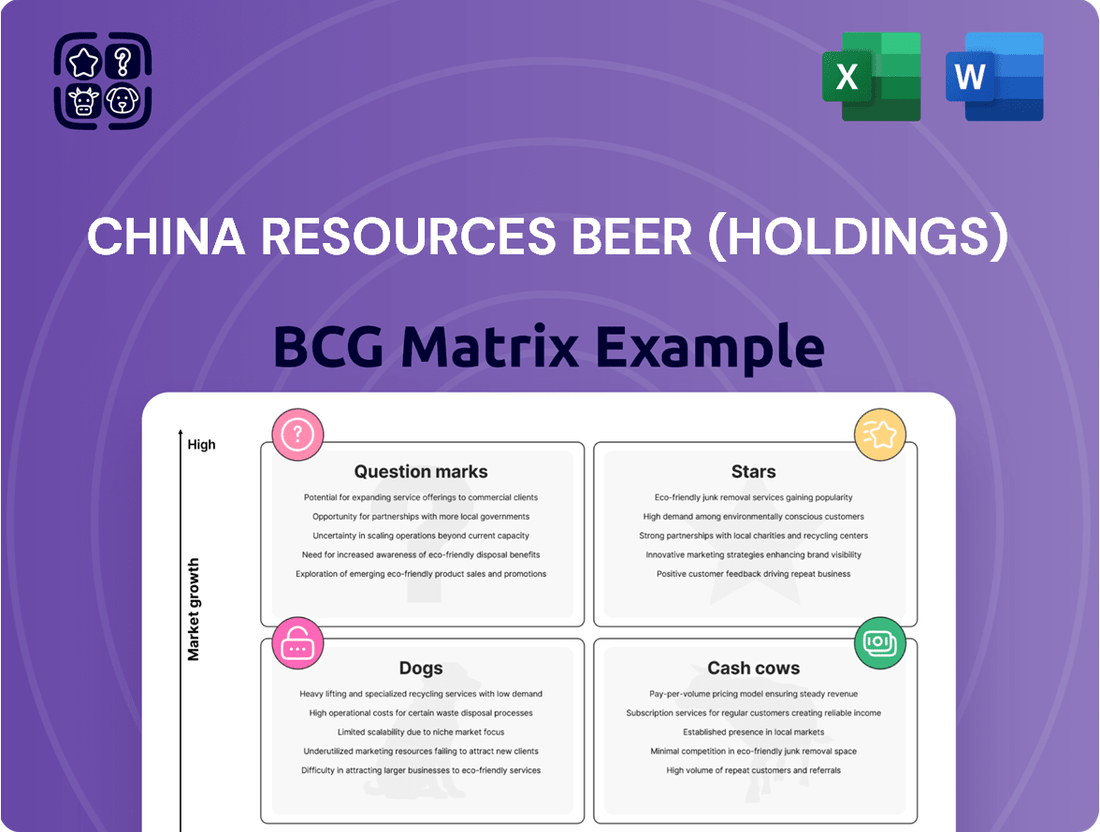

Stars

Heineken Partnership Brands

Heineken's presence within China Resources Beer's portfolio represents a significant "Star" in the BCG matrix. The Heineken brand itself has experienced robust growth, with sales increasing by nearly 20% in 2024. This strong performance is projected to continue with double-digit growth anticipated in early 2025, indicating its high market share in a rapidly expanding premium beer segment within China.

CR Beer’s Premium-and-Above Beer Segment

CR Beer’s premium-and-above beer segment, featuring brands like Lao Xue and Amstel, is a significant engine for the company's growth. Amstel, in particular, saw its sales volumes double, showcasing the strength of this strategic focus.

This segment experienced a volume increase of over 9% in 2024, and projections indicate it will surpass 10% growth in 2025. This robust performance underscores CR Beer's successful capture of market share within China's rapidly expanding premium beer category.

The company's investment in this higher-value segment directly addresses and capitalizes on the prevailing market trend of premiumization observed across China's consumer landscape.

SuperX (Revamped)

SuperX, following a significant revamp, achieved full-year growth in 2024, with expectations of high-single to double-digit growth continuing into 2025. This strategic repositioning in the sub-premium-and-above segment capitalizes on a clear consumer trend favoring higher-quality beer, even within a fiercely competitive market landscape. The brand's resurgence highlights its potential in a growing niche.

Snow Draft

Snow Draft is positioned as a Star in China Resources Beer's BCG Matrix, reflecting its strong market growth and significant market share. This premium lager is expected to achieve high-single digit growth in 2025, aligning with the broader trend of premiumization in the Chinese beer market.

Consumers are increasingly looking for more diverse and higher-quality beer options, and Snow Draft is well-suited to meet this demand. Its success indicates China Resources Beer's ability to innovate and capture value in the evolving beverage landscape.

- Market Position: Star

- Growth Expectation: High-single digit growth in 2025

- Consumer Trend Alignment: Capitalizes on premiumization and demand for quality

- Strategic Importance: Key premium offering driving market share

'Zhaiyao' (Premium Baijiu)

'Zhaiyao' stands out as China Resources Beer's premium baijiu offering. In 2024, this brand experienced an impressive 35% surge in sales volume.

This growth is particularly noteworthy as 'Zhaiyao' accounted for more than 70% of the total revenue generated by CR Beer's baijiu division. Despite broader challenges within the baijiu market, 'Zhaiyao' exhibits robust growth and high profitability, solidifying its status as a star performer within a segment CR Beer is actively developing.

- Brand: Zhaiyao (Premium Baijiu)

- 2024 Volume Growth: 35%

- Contribution to Baijiu Turnover: Over 70%

- Market Position: Star product with strong growth and high profitability

CR Beer's Stars: Heineken, Snow Draft, and Zhaiyao Shine!

Heineken and Snow Draft are prime examples of Stars within China Resources Beer's portfolio. Heineken saw nearly 20% sales growth in 2024 and is projected for continued double-digit growth, dominating the premium segment. Snow Draft, a premium lager, is expected to achieve high-single digit growth in 2025, aligning with consumer demand for quality.

Zhaiyao, CR Beer's premium baijiu, is another standout Star, achieving a remarkable 35% sales volume increase in 2024 and contributing over 70% to the baijiu division's revenue. This demonstrates CR Beer's successful expansion into the premium baijiu market.

| Brand | Category | 2024 Volume Growth | 2025 Growth Projection | Market Position |

| Heineken | Premium Beer | ~20% | Double-digit | Star |

| Snow Draft | Premium Beer | N/A | High-single digit | Star |

| Zhaiyao | Premium Baijiu | 35% | N/A | Star |

What is included in the product

This BCG Matrix overview highlights China Resources Beer's product portfolio, identifying Stars for growth, Cash Cows for funding, Question Marks for potential, and Dogs for divestment.

The China Resources Beer BCG Matrix offers a clear, one-page overview, simplifying complex portfolio decisions for executives.

Cash Cows

Snow Beer (Mass-Market Volume)

Snow Beer, a cornerstone of China Resources Beer (Holdings), exemplifies a classic cash cow within the Boston Consulting Group (BCG) matrix. As the world's top-selling beer by volume, its dominance in the vast Chinese market, where it holds a significant share, ensures consistent and robust cash generation.

Despite a general trend of declining or stagnant mass-market beer volumes in China, Snow Beer's immense scale and deeply entrenched brand loyalty allow it to continue producing substantial cash flow. This brand's widespread recognition and extensive distribution network solidify its position as a reliable revenue engine in a mature segment.

For instance, in 2023, China Resources Beer reported that Snow Beer continued to be the leading brand in its portfolio, contributing significantly to the company's overall financial performance, even as the broader beer market faced headwinds.

Traditional Mass-Market Beer Portfolio

China Resources Beer's traditional mass-market beer portfolio, anchored by its dominant Snow brand, continues to be a powerhouse in China. Despite operating in a low-growth or even declining volume segment, these brands command an exceptionally high market share nationwide.

This strong market position translates into a reliable and substantial cash flow. The sheer volume of consumers and the deeply entrenched distribution networks ensure that these established brands, even without explosive growth, act as consistent cash cows for the company.

For example, in 2023, China Resources Beer reported revenue of approximately RMB 25.4 billion, with the mass-market segment being the primary contributor. This segment’s stability is crucial for funding investments in other, higher-growth areas of the business.

Extensive Distribution Network

China Resources Beer's extensive distribution network is a significant strength, acting as a key driver for its Cash Cow status. This robust infrastructure ensures their products reach consumers across China efficiently.

The company leverages partnerships with diverse channels, including major e-commerce players like Meituan and Sam's Club. In 2023, China Resources Beer's net profit attributable to equity shareholders reached 10.5 billion RMB, a testament to the effectiveness of its wide reach and mature operational framework.

Established Production Capacity

China Resources Beer (Holdings) leverages its established production capacity as a significant strength within its BCG Matrix, positioning it as a strong Cash Cow. This extensive manufacturing footprint is a key driver of its financial performance.

The company boasts a robust network of 62 breweries strategically located across 25 provinces in China. As of December 2024, this infrastructure supported an impressive aggregate annual production capacity of approximately 18.7 million kilolitres. This vast capacity ensures CR Beer can meet substantial market demand efficiently.

- Extensive Network: 62 breweries across 25 provinces.

- High Production Volume: 18.7 million kilolitres annual capacity (as of Dec 2024).

- Economies of Scale: Enables cost efficiencies and stable cash flow generation.

- Market Dominance: Consistent supply supports market leadership and revenue stability.

Overall Beer Business (Volume & Profitability)

China Resources Beer's core beer business, despite a slight volume dip in 2024, remains the company's powerhouse. It continues to contribute the lion's share of overall turnover, underscoring its dominant market position.

The profitability of this segment is particularly noteworthy. Even with fluctuating sales volumes, the business saw improved gross profit margins in 2024. This strength stems from successful premiumization strategies and diligent cost control measures.

- Dominant Turnover Contributor: The beer segment consistently generates the majority of China Resources Beer's consolidated turnover.

- Premiumization Driving Margins: Efforts to move consumers towards higher-priced, premium beer products have successfully boosted gross profit margins.

- Resilience in a Mature Market: Despite market maturity and some volume sensitivity, the business demonstrates strong cash-generating capabilities.

- 2024 Performance Snapshot: While specific consolidated turnover figures for the beer segment in 2024 are part of broader financial reporting, the trend of improved gross profit margins highlights operational efficiency and pricing power.

Beer Giant's Cash Cow: Dominance in China's Market

China Resources Beer's core beer operations, particularly its mass-market offerings led by Snow Beer, firmly establish it as a cash cow. These brands benefit from an exceptionally high market share in China, ensuring consistent and substantial cash generation despite operating in a mature, low-growth segment.

The company's extensive distribution network, comprising 62 breweries across 25 provinces with an aggregate annual production capacity of approximately 18.7 million kilolitres as of December 2024, underpins this cash cow status. This vast infrastructure allows for efficient market penetration and cost economies of scale.

In 2024, while overall beer volumes saw some fluctuations, the core beer business remained the primary turnover contributor. Crucially, improved gross profit margins in this segment, driven by premiumization efforts and cost control, highlight its robust cash-generating capability, essential for funding other business ventures.

| Brand Segment | BCG Classification | Key Strengths | 2024 Financial Indicator |

|---|---|---|---|

| Core Beer (Snow Beer & Mass Market) | Cash Cow | Dominant Market Share, Extensive Distribution Network, High Production Capacity | Improved Gross Profit Margins |

| 62 Breweries, 18.7 Million KL Capacity (Dec 2024) | Primary Turnover Contributor | ||

| Economies of Scale, Brand Loyalty | Stable Cash Flow Generation |

Delivered as Shown

China Resources Beer (Holdings) BCG Matrix

The preview you are currently viewing is the exact China Resources Beer (Holdings) BCG Matrix report you will receive upon purchase, offering a comprehensive strategic overview without any watermarks or demo content. This professionally designed document is ready for immediate use, providing actionable insights for your business planning and competitive analysis. You can confidently expect the full, unedited version to be delivered directly to you, allowing for seamless integration into your strategic decision-making processes. This BCG Matrix analysis is crafted to empower your understanding of China Resources Beer's product portfolio and market positioning.

Dogs

Underperforming Regional/Legacy Brands

China Resources Beer, a dominant player in the Chinese beer market, likely manages several regional or legacy brands with limited market share in stagnant or shrinking local markets. These brands, often catering to a more traditional consumer base, represent a challenge in the company's portfolio.

The company's strategic initiatives, including the closure of less efficient breweries and consolidation of operations, directly address the need to divest or revitalize these underperforming assets. For instance, in 2023, China Resources Beer announced plans to optimize its production network, which would likely involve phasing out facilities tied to these older brands.

Inefficient Production Facilities

China Resources Beer (Holdings) is addressing its inefficient production facilities, often termed 'dogs' in a BCG matrix context. In 2024, the company made a strategic move by ceasing operations at two of its older breweries. These facilities were characterized by high operating expenses and underutilized capacity, making them drains on resources rather than contributors to profit.

The decision to close these less efficient breweries is a key part of China Resources Beer's broader strategy to optimize its overall capacity and improve operational efficiency. By shedding these underperforming assets, the company aims to redirect resources towards more productive and modern facilities, ultimately enhancing its competitive position and profitability in the long run.

Undifferentiated Low-End Products

Undifferentiated low-end beer products within China Resources Beer's portfolio, especially in a market leaning towards premiumization, would likely be classified as dogs. These offerings typically face low growth and minimal profitability, struggling to gain traction against more sophisticated or value-driven competitors. For instance, while the overall Chinese beer market saw growth, the low-end segment might lag significantly.

Baijiu Brands (Pre-Investment Underperformers)

Within China Resources Beer's portfolio, certain mainstream baijiu brands might be categorized as dogs, especially if their market performance doesn't improve. For instance, if brands like Jinsha continue to underperform in 2024, they could fall into this category. This designation hinges on whether strategic investments and new product launches can significantly boost their market share and profitability.

The performance of these brands is crucial. If initiatives aimed at revitalizing them don't show substantial gains, they represent a drain on resources. This is in contrast to premium offerings like Zhaiyao, which are considered stars and contribute significantly to the company's growth.

- Market Share Concerns: Brands like Jinsha experienced weaker performance in 2024, potentially indicating a declining market share in the competitive baijiu segment.

- Profitability Challenges: If these brands are not generating sufficient profits despite sales, they could be flagged as underperformers requiring strategic review.

- Investment Impact: The success of recent or planned investments and new product rollouts will be a key determinant in whether these brands can escape the dog category.

- Strategic Re-evaluation: A continued lack of improvement could lead China Resources Beer to re-evaluate its commitment to these specific baijiu brands, possibly leading to divestment or restructuring.

Non-Core, Stagnant Non-Alcoholic Offerings

Within China Resources Beer's portfolio, any non-alcoholic brands struggling to capture market share or operating in slow-growth sectors would be classified as Dogs. These brands, despite being part of the company's operations, represent a drain on resources without generating significant profits.

For instance, if a particular non-alcoholic tea or juice brand, launched several years ago, has consistently shown minimal sales growth and a declining market share, it would fit this category. Such products often require ongoing investment in marketing and distribution, tying up capital that could be better allocated to more promising ventures.

- Stagnant Market Segments: Non-alcoholic offerings in categories like traditional carbonated soft drinks or certain juice segments might be experiencing very low single-digit or even negative growth rates in China as consumer preferences shift towards healthier or more premium options.

- Low Market Share: Brands that have failed to achieve critical mass in their respective non-alcoholic categories, perhaps holding less than a 1-2% market share, would be considered Dogs.

- Capital Tie-up: These brands consume resources for production, marketing, and distribution, yet their low revenue generation and profitability mean they offer little to no return on investment, hindering overall financial performance.

China Resources Beer's "Dogs": Strategic Pruning for Growth

Within China Resources Beer's portfolio, certain legacy or regional beer brands with limited market share in slow-growing or declining local markets are classified as Dogs. These products often cater to a shrinking consumer base and represent a drain on resources due to low profitability and minimal growth potential. For example, the company's strategic consolidation efforts in 2024, including the closure of inefficient breweries, directly target these underperforming assets.

The company's approach to these 'dog' brands involves either divestment or revitalization. In 2024, China Resources Beer ceased operations at two older breweries, a move that directly addresses the inefficiency and underutilization often associated with these brands. This strategic pruning aims to reallocate capital and resources to more promising segments of the business, such as their premium offerings.

The continued underperformance of specific baijiu brands, like Jinsha, in 2024 also places them in the 'dog' category if market share and profitability do not improve. These brands require significant strategic investment to overcome their current challenges, and failure to do so could lead to their eventual divestment.

Similarly, non-alcoholic brands failing to gain traction in stagnant market segments or holding a very low market share, perhaps less than 1-2%, are also considered Dogs. These brands consume resources without generating substantial returns, impacting the overall financial health of China Resources Beer.

| Brand Category | Market Growth | Market Share | Profitability | Strategic Implication |

| Legacy Beer Brands | Low/Negative | Low | Low | Divest or Revitalize |

| Underperforming Baijiu Brands (e.g., Jinsha) | Stagnant/Declining | Low | Low | Strategic Investment or Divestment |

| Underperforming Non-Alcoholic Brands | Low | Very Low (<2%) | Negligible | Resource Reallocation |

Question Marks

New Low-Calorie Beer Line

China Resources Beer's new low-calorie beer line, launched in 2024, targets the burgeoning health-conscious market, a segment experiencing significant growth in China. This strategic move aligns with evolving consumer preferences for healthier beverage options.

Despite the promising market trend, this new product line currently occupies a modest market share. Substantial investment in brand building and expanding distribution networks will be crucial to elevate its competitive standing and capitalize on the high-growth potential.

Non-Alcoholic Beer Offerings

The non-alcoholic beer segment in China is experiencing robust growth, fueled by a rising trend of health-conscious consumers. China Resources Beer is strategically positioning itself to capitalize on this by planning new non-alcoholic beer launches, signaling a belief in its high-growth potential.

While these new offerings are promising, they currently hold a modest market share and necessitate significant investment to compete effectively against established and emerging players in this dynamic category.

Craft Beer Variations

Chinese consumers are increasingly embracing craft beers, driving significant volume growth in this segment. China Resources Beer (CR Beer) is strategically planning to introduce its own craft beer variations, recognizing the high-growth potential of this evolving market.

While these craft offerings are still in their early stages for CR Beer, they represent a crucial investment area. Establishing a strong competitive position in the craft beer market will necessitate substantial financial commitment and marketing efforts.

'Nong Li' (Super-Premium Beer)

Nong Li, launched in 2024, is China Resources Beer's foray into the super-premium beer segment, a market showing robust expansion. This new entrant, designed to capture the high-end consumer, begins with a nascent market share.

Its classification as a 'Question Mark' in the BCG matrix stems from its high growth market potential coupled with a low current market share. Significant investment in marketing and brand development is crucial for Nong Li to capitalize on its growth prospects and establish a strong foothold.

- Nong Li's Market Position: High market growth, low market share.

- Strategic Imperative: Invest heavily in marketing and brand building.

- 2024 Context: Launched in a rapidly expanding super-premium segment.

- Objective: Convert high growth potential into significant market share.

'Ken 14' (Premium National Barley Product)

'Ken 14', launched in 2024 by China Resources Beer, is positioned as a premium national barley product under the 'Chinese Barley, Chinese Beer' initiative. This product enters a rapidly expanding premium beer segment. Significant marketing and distribution investments are crucial for 'Ken 14' to establish brand awareness and capture market share, thereby preventing it from becoming a low-growth, low-market-share 'dog' in the BCG matrix.

The premium beer market in China has seen robust growth, with reports indicating a 10% year-over-year increase in 2023. 'Ken 14' will require substantial capital expenditure to compete effectively. For instance, similar premium product launches in 2023 saw marketing budgets exceeding 50 million RMB to achieve initial brand penetration. Without this investment, 'Ken 14' risks lagging behind established premium brands.

- Product Launch: 'Ken 14' debuted in 2024.

- Market Position: Premium national barley product.

- Strategic Goal: Promote 'Chinese Barley, Chinese Beer.'

- Market Dynamics: Entering a growing premium segment requiring significant investment.

China Resources Beer's Strategic Moves in China's Booming Beverage Market

China Resources Beer's new low-calorie beer line, launched in 2024, targets the burgeoning health-conscious market, a segment experiencing significant growth in China. This strategic move aligns with evolving consumer preferences for healthier beverage options.

Despite the promising market trend, this new product line currently occupies a modest market share. Substantial investment in brand building and expanding distribution networks will be crucial to elevate its competitive standing and capitalize on the high-growth potential.

The non-alcoholic beer segment in China is experiencing robust growth, fueled by a rising trend of health-conscious consumers. China Resources Beer is strategically positioning itself to capitalize on this by planning new non-alcoholic beer launches, signaling a belief in its high-growth potential.

While these new offerings are promising, they currently hold a modest market share and necessitate significant investment to compete effectively against established and emerging players in this dynamic category.

Chinese consumers are increasingly embracing craft beers, driving significant volume growth in this segment. China Resources Beer (CR Beer) is strategically planning to introduce its own craft beer variations, recognizing the high-growth potential of this evolving market.

While these craft offerings are still in their early stages for CR Beer, they represent a crucial investment area. Establishing a strong competitive position in the craft beer market will necessitate substantial financial commitment and marketing efforts.

Nong Li, launched in 2024, is China Resources Beer's foray into the super-premium beer segment, a market showing robust expansion. This new entrant, designed to capture the high-end consumer, begins with a nascent market share.

Its classification as a 'Question Mark' in the BCG matrix stems from its high growth market potential coupled with a low current market share. Significant investment in marketing and brand development is crucial for Nong Li to capitalize on its growth prospects and establish a strong foothold.

'Ken 14', launched in 2024 by China Resources Beer, is positioned as a premium national barley product under the 'Chinese Barley, Chinese Beer' initiative. This product enters a rapidly expanding premium beer segment. Significant marketing and distribution investments are crucial for 'Ken 14' to establish brand awareness and capture market share, thereby preventing it from becoming a low-growth, low-market-share 'dog' in the BCG matrix.

The premium beer market in China has seen robust growth, with reports indicating a 10% year-over-year increase in 2023. 'Ken 14' will require substantial capital expenditure to compete effectively. For instance, similar premium product launches in 2023 saw marketing budgets exceeding 50 million RMB to achieve initial brand penetration. Without this investment, 'Ken 14' risks lagging behind established premium brands.

| Product/Segment | Market Growth | Market Share | Strategic Consideration | 2024 Status |

| Low-Calorie Beer | High | Low | Invest for growth, build brand awareness. | New launch, targeting health-conscious consumers. |

| Non-Alcoholic Beer | High | Low | Significant investment needed for market penetration. | Planned launches in a growing segment. |

| Craft Beer | High | Low | Requires substantial marketing and financial commitment. | New variations planned, early stages for CR Beer. |

| Super-Premium (Nong Li) | High | Low | Focus on marketing and brand development for market capture. | Launched in 2024, nascent market share. |

| Premium Barley ('Ken 14') | High | Low | Requires significant marketing and distribution investment. | Launched in 2024, part of a national initiative. |

BCG Matrix Data Sources

Our China Resources Beer BCG Matrix utilizes a blend of financial disclosures, market research reports, and industry growth forecasts to accurately position each business unit.