China National Nuclear Power Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

China National Nuclear Power

Don't Miss the Bigger Picture

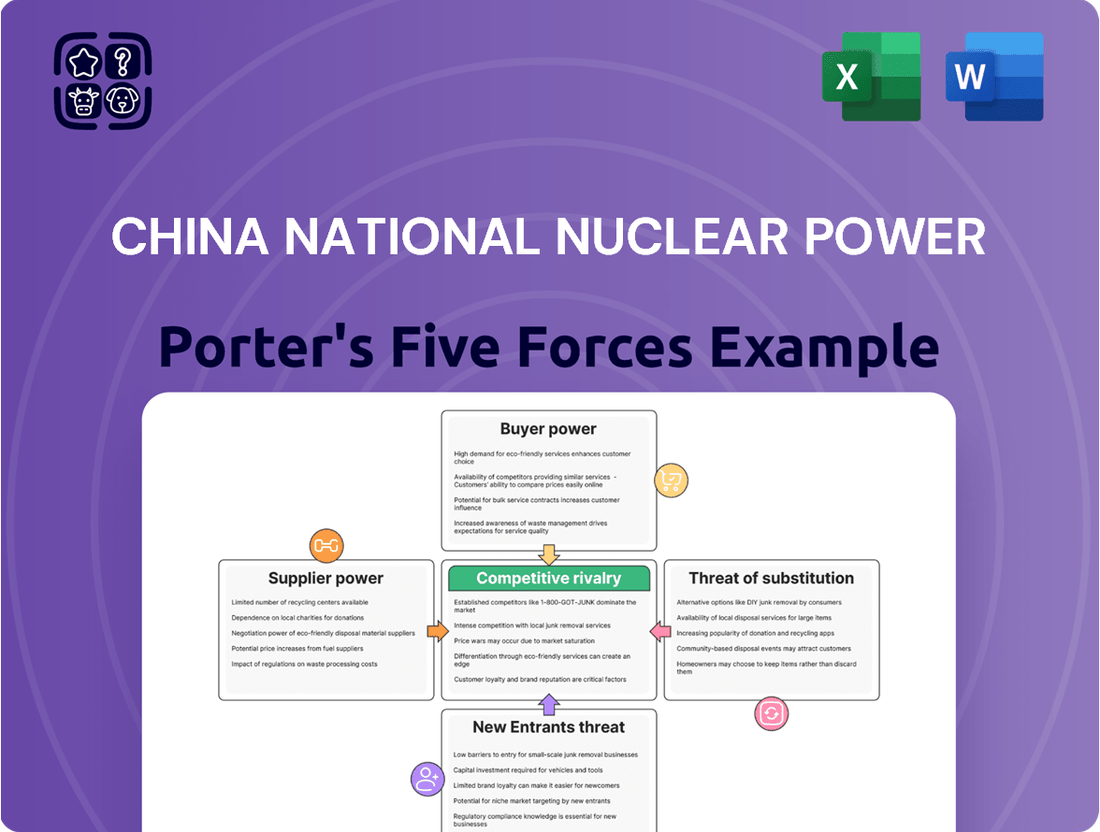

China National Nuclear Power faces significant barriers to entry due to high capital requirements and stringent regulatory oversight, limiting the threat of new competitors. However, the industry is characterized by intense rivalry among existing players and considerable buyer power from government entities and large energy consumers. Understanding these dynamics is crucial for strategic planning.

The complete report reveals the real forces shaping China National Nuclear Power’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentrated and Specialized Supply Chain

The nuclear power sector, including companies like China National Nuclear Power (CNNP), faces a concentrated supply chain for essential components. This means a limited number of qualified manufacturers produce critical items such as nuclear fuel assemblies, reactor pressure vessels, and sophisticated control systems. This scarcity of specialized suppliers inherently grants them substantial bargaining power.

For CNNP, this concentration translates into higher costs and less flexibility. Suppliers of advanced materials and proprietary technologies, often holding patents or unique manufacturing processes, can dictate terms due to the difficulty and time involved in finding or developing alternative sources. For instance, the lead time for a custom-fabricated reactor component can easily extend to several years, reinforcing the supplier's leverage.

Government Control and State-Owned Suppliers

In China's nuclear power sector, state-owned enterprises like China National Nuclear Power (CNNP) often deal with suppliers that are also government-controlled entities. This means that national strategic goals and industrial policies can influence supplier behavior, potentially reducing CNNP's leverage in negotiations. For instance, during 2024, China's continued emphasis on energy security and self-sufficiency in critical materials for nuclear power generation means that the government's coordination of these state-owned suppliers is a key factor.

High Switching Costs

High switching costs significantly bolster the bargaining power of suppliers to China National Nuclear Power (CNNP). The nuclear industry's stringent safety regulations and the specialized nature of components mean that changing suppliers is not a simple matter of finding a new vendor. This complexity translates into substantial financial and operational hurdles for CNNP, making it difficult to change suppliers even when facing less favorable pricing or terms.

The process of switching suppliers in nuclear power generation involves considerable investment and potential disruption. For instance, re-certifying new equipment and conducting extensive safety testing can add years to project timelines and millions to costs. In 2024, the average cost of a nuclear power plant project delay due to regulatory or supply chain issues was estimated to be upwards of $50 million per year, a figure that underscores the financial risk associated with supplier changes.

Furthermore, the highly regulated environment governing nuclear safety necessitates rigorous approval processes for any new supplier or component. This regulatory oversight acts as a significant barrier to entry for new suppliers and simultaneously locks in existing ones. Consequently, CNNP finds itself in a position where the cost and complexity of switching suppliers heavily favor the incumbent providers, granting them considerable leverage in negotiations.

Proprietary Technology and Intellectual Property

Suppliers possessing proprietary technology and intellectual property, such as advanced reactor designs like China's Hualong One or specialized fuel fabrication techniques, wield significant bargaining power over China National Nuclear Power (CNNP). This technological exclusivity means CNNP faces limited alternatives, forcing reliance on these key suppliers for critical components and expertise. For instance, the development and deployment of indigenous reactor technologies reduce reliance on foreign suppliers, but the initial dependency on those with established intellectual property can be substantial.

The dependency on these specialized suppliers is amplified because developing comparable technologies internally would necessitate considerable research and development investment and time. This creates a situation where CNNP must negotiate terms with suppliers who control essential, hard-to-replicate capabilities. In 2024, the global nuclear industry continued to see significant investment in advanced reactor designs, further solidifying the value of intellectual property in this sector.

The bargaining power of these suppliers is further underscored by the high switching costs associated with changing technology providers in the nuclear industry. Any shift would involve extensive requalification, regulatory approvals, and potential project delays, making CNNP hesitant to seek alternatives. This inherent stickiness in supplier relationships allows those with unique technological offerings to command premium pricing and favorable contract terms.

- Proprietary Reactor Designs: Suppliers of advanced nuclear reactor designs like Hualong One and CAP1000 hold significant leverage.

- Specialized Fuel Fabrication: Expertise in nuclear fuel processing and manufacturing represents another area of supplier strength.

- High R&D Barriers: The substantial investment required to replicate proprietary technologies limits CNNP's alternatives.

- Limited Substitutes: The scarcity of suppliers with equivalent technological capabilities enhances their negotiating position.

Global Supply Chain Dynamics

While China is actively building its domestic nuclear supply chain, the reality for China National Nuclear Power (CNNP) is that certain critical inputs, such as uranium and highly specialized components, may still require international sourcing. This reliance on external markets means that global supply chain dynamics significantly influence the bargaining power of suppliers. For instance, in 2024, the global uranium market experienced price volatility due to geopolitical tensions and production disruptions in key mining regions, directly affecting procurement costs for nuclear fuel.

Geopolitical factors and evolving trade policies are paramount in shaping supplier leverage over CNNP. Changes in international relations or the imposition of tariffs can restrict access to essential materials or components, thereby increasing their cost and potentially impacting project timelines. For example, shifts in international energy policies in 2024 have led some nations to re-evaluate their uranium export strategies, potentially strengthening the hand of suppliers in those jurisdictions.

- International Sourcing Dependence: Despite domestic advancements, CNNP still relies on global markets for uranium and specialized nuclear components.

- Geopolitical Impact: International relations and trade policies directly influence supplier bargaining power and CNNP's procurement costs.

- Market Fluctuations: Global market volatility for raw materials like uranium, as seen in 2024, can significantly impact CNNP's operational expenses and supply stability.

Supplier Power Dominates China's Nuclear Procurement

The bargaining power of suppliers to China National Nuclear Power (CNNP) is considerable due to the concentrated nature of the nuclear supply chain and high switching costs. Suppliers of specialized components and proprietary technologies, such as advanced reactor designs and fuel fabrication, hold significant leverage. This is further amplified by the lengthy regulatory approval processes and the substantial investment required to qualify new vendors, making it difficult and costly for CNNP to change suppliers.

In 2024, China's emphasis on energy security and domestic production meant that state-owned suppliers often operated under national strategic priorities, influencing negotiations. The global market for nuclear materials, like uranium, also saw price volatility in 2024, impacting CNNP's procurement costs and reinforcing supplier leverage, especially for those with exclusive technological capabilities or international supply chain access.

| Factor | Impact on CNNP | Supplier Leverage |

|---|---|---|

| Supply Chain Concentration | Limited qualified suppliers for critical components | High |

| Switching Costs | Significant financial and operational hurdles for supplier changes | High |

| Proprietary Technology/IP | Dependency on unique designs and manufacturing processes | High |

| Regulatory Environment | Rigorous approval processes create barriers for new suppliers | High |

| International Sourcing | Exposure to global market volatility and geopolitical factors | Moderate to High |

What is included in the product

This Porter's Five Forces analysis for China National Nuclear Power dissects the competitive intensity, buyer and supplier power, threat of new entrants, and the impact of substitutes within the nuclear energy sector.

Navigate the complex competitive landscape of China's nuclear power sector by instantly assessing the impact of each of Porter's Five Forces, providing clarity on strategic vulnerabilities and opportunities.

Customers Bargaining Power

Government as the Primary Customer

China National Nuclear Power's (CNNP) primary customer is the national power grid, which is largely controlled and regulated by the Chinese government. This centralized structure significantly shapes CNNP's customer bargaining power. In 2023, China's electricity consumption reached 9.5 trillion kilowatt-hours, with the state-owned grid companies being the dominant purchasers.

The government's influence means that electricity pricing and grid integration are heavily dictated by state policies and national energy strategies. This reduces the direct market-driven demand leverage that typical customers would possess. For instance, the government sets feed-in tariffs and grid access rules, directly impacting CNNP's revenue streams and operational flexibility.

Regulated Electricity Tariffs

Regulated electricity tariffs in China significantly curb the bargaining power of customers by limiting China National Nuclear Power's (CNNP) ability to independently adjust prices. The government's oversight ensures price stability and affordability for end-users, meaning customers do not have the power to negotiate lower rates directly with CNNP. This regulatory framework effectively centralizes pricing decisions, shifting bargaining power away from individual consumers and towards the state.

High Barriers to Entry for Electricity Generation

For end-consumers, the ability to switch electricity providers is typically very limited, if available at all, which significantly curtails their bargaining power. Similarly, for industrial users, the prospect of generating their own power, especially the substantial baseload required from nuclear facilities, is largely impractical. The immense capital outlay and specialized knowledge needed for nuclear power generation make it an unfeasible alternative for most businesses, thereby diminishing customer leverage.

National Energy Security and Clean Energy Goals

China's unwavering commitment to energy security and its ambitious target of achieving carbon neutrality by 2060 significantly elevates the bargaining power of customers in the nuclear energy sector. This national directive positions nuclear power as a critical component of the country's energy strategy, ensuring sustained demand for nuclear power generation. China National Nuclear Power (CNNP) is thus a vital player in meeting these strategic objectives.

The robust governmental push for cleaner energy sources translates into a stable and predictable demand for nuclear power. This consistent demand, driven by national policy, inherently limits the ability of individual customers or even large industrial consumers to exert significant downward pressure on prices or demand unfavorable terms from CNNP. The strategic importance of nuclear energy to the nation's future energy mix is paramount.

- National Energy Security: China aims to reduce its reliance on imported fossil fuels, making domestic nuclear power a cornerstone of its energy independence strategy.

- Carbon Neutrality Goals: The commitment to achieving carbon neutrality by 2060 necessitates a substantial increase in low-carbon energy sources, with nuclear power playing a crucial role.

- Consistent Demand: Government policies and long-term energy planning ensure a steady and growing demand for nuclear power generation capacity, benefiting major players like CNNP.

Competition from Other Power Sources within the Grid

China National Nuclear Power (CNNP) faces competition from diverse power sources within the national grid. While nuclear offers reliable baseload power, it contends with established and emerging alternatives. In 2023, China's total installed power generation capacity reached approximately 2,920 GW, with coal still dominating at over 50%.

The rapid expansion of renewable energy sources, particularly wind and solar, presents a significant competitive force. By the end of 2023, China's installed wind power capacity exceeded 400 GW, and solar power capacity surpassed 600 GW. This growing renewable capacity, often with lower marginal costs, can influence electricity pricing and demand for nuclear power, especially during periods of high renewable output.

Market reforms in China's electricity sector are also intensifying competition. These reforms aim to liberalize power trading and pricing, allowing greater flexibility for different generation types to compete. This dynamic environment means CNNP must continuously adapt to evolving market conditions and the cost-competitiveness of alternative energy supplies.

- Dominant Coal Power: Coal-fired power plants still represent the largest share of China's electricity generation, exerting significant competitive pressure.

- Rapid Renewable Growth: The substantial and ongoing increases in wind and solar capacity directly challenge nuclear power's market share and pricing power.

- Market Liberalization Impact: Electricity market reforms create a more competitive landscape, potentially impacting the demand and profitability of nuclear energy.

China's Nuclear Power: Customers Hold Little Bargaining Power

The bargaining power of customers for China National Nuclear Power (CNNP) is notably low due to the centralized nature of China's electricity market and strong government regulation. Customers, primarily the state-controlled power grid, have limited ability to negotiate prices or terms, as these are largely set by national energy policies and strategic objectives.

The government's focus on energy security and carbon neutrality by 2060 ensures a stable demand for nuclear power, further diminishing customer leverage. For instance, China's commitment to increasing its nuclear power capacity as part of its clean energy transition solidifies CNNP's role and reduces the scope for customer-driven price reductions.

The impracticality for most end-users, including industrial entities, to generate their own nuclear power due to immense capital and technical requirements also limits their bargaining power. This scenario is underscored by China's vast electricity consumption, with state-owned entities being the principal buyers, as evidenced by the 9.5 trillion kilowatt-hours consumed in 2023.

Preview Before You Purchase

China National Nuclear Power Porter's Five Forces Analysis

This preview displays the comprehensive Porter's Five Forces analysis for China National Nuclear Power, detailing the competitive landscape and strategic implications. You're looking at the actual document; once your purchase is complete, you'll gain instant access to this exact, fully formatted file, ready for immediate use.

Rivalry Among Competitors

Limited Number of Major Domestic Competitors

The competitive rivalry within China's nuclear power sector is notably subdued due to an oligopolistic market structure. Dominated by a handful of major state-owned enterprises, including China National Nuclear Power (CNNP) and China General Nuclear Power Group (CGN), the landscape features limited direct competition for new projects. In 2023, these two giants accounted for the vast majority of operational nuclear capacity in China, with CNNP operating 27,309 MW and CGN operating 27,014 MW, underscoring their entrenched positions.

Government Allocation of Projects

Competitive rivalry within China's nuclear power sector is significantly shaped by government allocation of projects. Instead of open market bidding, major new nuclear power plant projects are typically approved and assigned by the State Council, China's chief administrative authority. This top-down approach means China National Nuclear Power (CNNP) and its domestic rivals, like China General Nuclear Power Group (CGN), don't directly compete for project acquisition in the same way companies do in more liberalized markets. For instance, in 2023, China approved several new nuclear projects, with allocations determined through national strategic planning rather than competitive tenders.

Technological Specialization and Collaboration

While direct competition exists, China's state-owned nuclear power entities often differentiate through technological specialization. For instance, some focus on developing and deploying advanced reactor designs like the Hualong One, while others might concentrate on smaller modular reactors (SMRs) or specific aspects of the nuclear fuel cycle. This specialization reduces head-to-head rivalry.

Furthermore, collaboration on major national nuclear projects is a key feature, mitigating intense direct competition. This cooperative approach allows for shared expertise and resources, fostering a more unified and efficient national nuclear energy development strategy. For example, joint ventures on large-scale power plant construction are common.

Focus on Domestic and International Expansion

China National Nuclear Power (CNNP) faces intense rivalry, with competition extending beyond domestic projects to a global arena. This rivalry is fueled by the race to develop cutting-edge nuclear technologies, including Generation IV reactors and Small Modular Reactors (SMRs). Companies are also vying for lucrative international export deals, often facilitated by geopolitical initiatives like the Belt and Road. This dynamic shifts the competitive landscape from solely domestic market share to achieving technological supremacy and exerting global influence.

- Technological Advancement: Competition is fierce in developing next-generation reactors, with significant R&D investment from global players.

- Export Markets: Securing international contracts is a key battleground, with countries actively seeking nuclear energy partnerships.

- Geopolitical Influence: Initiatives like the Belt and Road can shape which companies gain preferential access to emerging markets.

Underlying Drive for National Energy Goals

The competitive rivalry within China's nuclear power sector, primarily between giants like China National Nuclear Corporation (CNNC) and China General Nuclear Power Group (CGN), is less about cutthroat market share grabs and more about aligning with national strategic objectives. Both entities are driven to advance China's energy security and its ambitious carbon neutrality targets.

This dynamic means that while they are competitors, their efforts are largely channeled towards a common goal: expanding China's nuclear power capacity and technological prowess. For instance, by the end of 2023, China had 55 operational nuclear reactors, with CNNC and CGN being the primary developers and operators of these facilities.

- National Alignment: Rivalry is secondary to achieving China's energy security and carbon neutrality goals.

- Collective Advancement: Focus is on increasing overall nuclear capacity and technological sophistication.

- Operational Scale: CNNC and CGN manage the majority of China's 55 operational nuclear reactors as of end-2023.

- Technological Development: Competition spurs innovation in areas like Generation IV reactors and small modular reactors (SMRs).

China's Nuclear Power: State-Driven Oligopoly

Competitive rivalry in China's nuclear power sector is characterized by an oligopolistic structure dominated by state-owned enterprises like China National Nuclear Power (CNNP) and China General Nuclear Power Group (CGN). Project allocation is government-driven, not market-based, with the State Council assigning new plants. This governmental control significantly moderates direct competition among domestic players, as seen in the strategic approval of projects in 2023.

| China National Nuclear Power (CNNP) | China General Nuclear Power Group (CGN) | Total Operational Reactors (End 2023) | |

| Operational Capacity (MW) | 27,309 | 27,014 | N/A |

| Market Share | Dominant | Dominant | 55 |

SSubstitutes Threaten

Renewable Energy Sources (Solar, Wind, Hydro)

The most significant substitutes for nuclear power in China are renewable energy sources such as solar, wind, and hydropower. China's commitment to these alternatives is substantial, evidenced by its rapid expansion of renewable energy capacity. For instance, in 2023, China added a record 216.9 GW of renewable power capacity, exceeding previous years and demonstrating a clear strategic shift.

This aggressive growth in renewables directly challenges nuclear power's market share. The declining costs of solar and wind technologies, coupled with faster deployment times, make them increasingly competitive. By the end of 2023, China's installed renewable energy capacity surpassed 1.4 billion kilowatts, a significant portion of its total power generation, signaling a robust long-term threat to nuclear's dominance.

Fossil Fuels (Coal and Natural Gas)

Despite China's strong push towards clean energy, coal continues to be a significant player in its energy landscape, acting as a traditional substitute for the baseload power that nuclear energy provides. As of 2023, coal still accounted for approximately 56% of China's total energy consumption, underscoring its persistent role, especially in meeting escalating electricity demands.

While government policies are actively working to curb coal's dominance, it remains a crucial backup power source, particularly during periods of high demand or when renewable energy output is lower. This inherent substitutability means that the cost and availability of coal directly influence the perceived value and competitiveness of nuclear power.

Natural gas also presents a viable substitute, particularly for managing peak electricity loads. In 2024, China's natural gas consumption saw continued growth, driven by its cleaner-burning profile compared to coal. This dual role of coal and natural gas as substitutes for nuclear power highlights the complex energy market dynamics China navigates.

Energy Efficiency and Demand-Side Management

Improvements in energy efficiency and the rise of demand-side management programs present a significant threat of substitution for China National Nuclear Power. These initiatives aim to reduce overall energy consumption, thereby lessening the demand for new power generation capacity, including nuclear. For instance, by 2023, China's industrial sector saw energy intensity decrease by 2.3% compared to 2022, showcasing progress in efficiency.

As China prioritizes sustainable development and carbon reduction goals, the focus on these alternative energy management strategies could diminish the perceived necessity for substantial new nuclear power plant construction. This shift in energy policy and consumer behavior directly impacts the market share and growth potential for nuclear power, acting as a substitute for its baseload electricity provision.

Energy Storage Technologies

Advancements in energy storage technologies present a significant threat of substitutes for nuclear power. Large-scale battery systems, for instance, are increasingly capable of enhancing the dispatchability and reliability of intermittent renewable energy sources like solar and wind. This makes renewables a more direct competitor to the baseload power traditionally supplied by nuclear plants.

China's commitment to developing and deploying these storage solutions underscores this threat. By 2024, the nation's investments in grid-scale battery storage are expected to reach tens of billions of dollars, aiming to integrate a higher percentage of renewable energy onto its grid. This strategic push could diminish the perceived necessity of nuclear power for grid stability.

- Battery Storage Growth: Global grid-scale battery storage capacity is projected to grow substantially, with significant contributions from China, potentially reaching hundreds of gigawatts by 2030.

- Cost Reductions: The cost of lithium-ion batteries, a primary technology for grid storage, has seen dramatic decreases, making them increasingly competitive with traditional power generation.

- Renewable Integration: Improved storage capabilities allow for greater penetration of renewables, directly challenging the market share of nuclear power in providing consistent energy supply.

Emerging Technologies (e.g., Nuclear Fusion)

While still in the nascent stages of development, advanced energy solutions like nuclear fusion represent a significant potential long-term substitute for conventional power generation methods. China is demonstrating a strong commitment to this frontier, channeling substantial investment into nuclear fusion research and development. The nation's ambitious roadmap includes the creation of industrial prototypes within the next few decades.

This technological pursuit aims to unlock a cleaner, and possibly more plentiful, energy source. By 2024, China's investment in fusion research has been substantial, with projects like the Experimental Advanced Superconducting Tokamak (EAST) achieving record-breaking plasma confinement times, signaling progress towards viable fusion power. The potential for fusion to provide baseload power without greenhouse gas emissions positions it as a disruptive force in the energy landscape.

- Nuclear Fusion Investment: China is a global leader in fusion research funding, with significant national programs dedicated to its advancement.

- Technological Milestones: Projects like EAST are pushing the boundaries of plasma physics, crucial for achieving sustained fusion reactions.

- Long-Term Energy Potential: Successful development of fusion power could offer a virtually limitless, low-carbon energy supply, fundamentally altering the energy market.

China's Nuclear Power: Alternatives Reshape Energy Future

Renewable energy sources like solar and wind are significant substitutes for nuclear power in China, driven by rapid capacity expansion and cost reductions. By the end of 2023, China's installed renewable energy capacity exceeded 1.4 billion kilowatts, a testament to this growing threat. Energy efficiency improvements and demand-side management also reduce the need for new power generation, including nuclear, with industrial energy intensity decreasing by 2.3% in 2023.

Advancements in energy storage, particularly grid-scale battery systems, are enhancing the integration of renewables, making them more competitive with nuclear's baseload provision. China's substantial investments in battery storage, expected to reach tens of billions of dollars by 2024, aim to bolster renewable energy's grid stability role.

While coal remains a substantial substitute, accounting for around 56% of China's energy consumption in 2023, and natural gas also serves as a backup, the long-term threat from emerging technologies like nuclear fusion is notable. China's significant investment in fusion research, exemplified by projects like EAST achieving record plasma confinement, signals a potential future disruption to the current energy landscape.

| Substitute Energy Source | 2023/2024 Data Point | Impact on Nuclear Power |

|---|---|---|

| Renewable Energy Capacity | 1.4 billion kW installed (end of 2023) | Directly competes for market share, reducing demand for new nuclear builds. |

| Energy Efficiency | 2.3% decrease in industrial energy intensity (2023) | Lowers overall energy demand, lessening the need for nuclear power. |

| Grid-Scale Battery Storage Investment | Tens of billions of dollars expected by 2024 | Enhances renewable reliability, making them a stronger substitute for baseload nuclear power. |

| Coal Consumption | ~56% of total energy consumption (2023) | Continues to provide baseload power, acting as a traditional substitute. |

Entrants Threaten

High Capital Costs and Long Lead Times

The nuclear power sector presents a significant hurdle for newcomers due to its exceptionally high capital expenditure requirements. Building a new nuclear power plant can cost tens of billions of dollars, with estimates for new builds in 2024 often exceeding $20 billion USD. This massive upfront investment, coupled with the lengthy development cycles that can stretch over a decade from initial planning to full operation, effectively deters most potential entrants.

Stringent Regulatory Requirements and Safety Standards

Stringent regulatory requirements and safety standards represent a significant barrier to entry in the nuclear power sector. Globally, nuclear energy is subject to exceptionally rigorous oversight due to inherent safety and security considerations.

New companies entering this market must navigate an incredibly complex and costly approval process, demanding substantial technical expertise and a demonstrable history of successful operations, hurdles that are challenging for emerging players to overcome.

For instance, the U.S. Nuclear Regulatory Commission (NRC) mandates a multi-year licensing process for new reactors, involving extensive environmental reviews and safety analyses, a process that can cost hundreds of millions of dollars before construction even begins. China's National Nuclear Safety Administration (NNSA) employs similarly demanding standards, ensuring that only entities with proven capabilities and robust safety protocols can operate.

Government Control and State-Owned Dominance

The threat of new entrants in China's nuclear power sector is significantly low due to stringent government control and the dominance of state-owned enterprises. Major players like China National Nuclear Corporation (CNNC) and China General Nuclear Power Group (CGN) are state-owned, meaning the government has direct influence over industry development.

This state ownership, coupled with the government's strategic oversight in project allocation and licensing, creates substantial barriers. For instance, in 2024, China continued its ambitious nuclear expansion plans, with several new reactors under construction and planned, all overseen by state entities, making it exceedingly difficult for private or foreign companies to enter and compete.

Access to Specialized Technology and Expertise

The development and operation of nuclear power plants demand highly specialized technology, proprietary intellectual property, and a deeply skilled workforce. This includes nuclear engineers, experienced operators, and safety specialists, all of whom are critical for safe and efficient operations.

New entities face significant hurdles in acquiring or developing this proprietary knowledge and the necessary human capital. This expertise is largely concentrated within established state-owned enterprises, making it difficult for newcomers to gain a foothold.

Consider these specific barriers:

- High R&D Investment: Significant capital is required for research and development in nuclear technology, often running into billions of dollars for initial breakthroughs and ongoing advancements.

- Proprietary Technology: Existing players possess patented designs for reactors, fuel processing, and safety systems, which are not readily available to new entrants.

- Skilled Workforce Scarcity: The global pool of qualified nuclear engineers and safety personnel is limited, with many already employed by established entities. For instance, China's nuclear workforce has seen steady growth, but the specialized nature of roles means experienced individuals are highly sought after.

- Regulatory Hurdles: Obtaining licenses and approvals for nuclear technology development and plant operation is an intensely complex and lengthy process, requiring extensive demonstration of technological capability and safety protocols.

Established Infrastructure and Grid Integration

Established players like China National Nuclear Power (CNNP) possess a significant advantage due to their existing, extensive infrastructure. This includes robust supply chains for nuclear fuel and components, proven construction capabilities honed over years of operation, and critical grid integration systems that ensure reliable power delivery. For instance, as of early 2024, China's installed nuclear capacity continued its steady expansion, with existing operators like CNNP already deeply embedded within this framework.

New entrants would face immense hurdles in replicating this established ecosystem. The capital expenditure required to build new supply chains, develop specialized construction expertise, and secure grid access is substantial. Furthermore, navigating the complex regulatory landscape and achieving the necessary scale to compete effectively presents a formidable barrier. In 2023, the lead times for new nuclear plant construction remained lengthy, often exceeding a decade, highlighting the difficulty for newcomers to quickly establish a competitive presence.

- Established Infrastructure: CNNP benefits from existing nuclear fuel supply chains, construction expertise, and grid integration.

- High Entry Costs: New entrants need massive capital for infrastructure, supply chains, and grid access.

- Grid Integration Challenges: Existing operators have seamless integration, a difficult feat for new companies.

- Market Penetration: Building scale and market share against established giants is a significant threat.

China's Nuclear Power: An Impenetrable Fortress for New Entrants

The threat of new entrants for China National Nuclear Power (CNNP) is exceptionally low. This is primarily due to the immense capital investment required, estimated to be in the tens of billions of dollars for a single plant, with 2024 projections for new builds often surpassing $20 billion USD. Furthermore, the sector is heavily regulated, demanding specialized technical expertise and a proven track record, which are significant hurdles for any newcomer.

State ownership of major players like CNNC and CGN, coupled with the government's strategic control over project allocation and licensing in 2024, creates substantial barriers. The concentration of proprietary technology, R&D investment in the billions, and a scarcity of specialized nuclear engineers further consolidate the market, making it exceedingly difficult for new entities to gain a foothold or compete effectively against established infrastructure.

| Barrier Type | Description | Estimated Cost/Impact (Illustrative) |

|---|---|---|

| Capital Expenditure | Building a new nuclear plant | >$20 Billion USD (2024 estimates) |

| Regulatory & Licensing | Navigating approval processes | Hundreds of Millions USD (pre-construction) |

| Technology & Expertise | Acquiring proprietary knowledge & skilled workforce | Billions USD (R&D); Limited availability of specialists |

| Infrastructure & Supply Chain | Establishing operational ecosystem | Massive investment; Long lead times (often >10 years) |

Porter's Five Forces Analysis Data Sources

Our analysis for China National Nuclear Power is built upon data from official company filings, including annual reports and prospectuses, alongside industry-specific reports from reputable research firms and government energy agencies.

We leverage publicly available financial statements, news archives from major business publications, and data from international energy organizations to provide a comprehensive view of the competitive landscape.