China Index Holdings (CIH) Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

China Index Holdings (CIH)

A Must-Have Tool for Decision-Makers

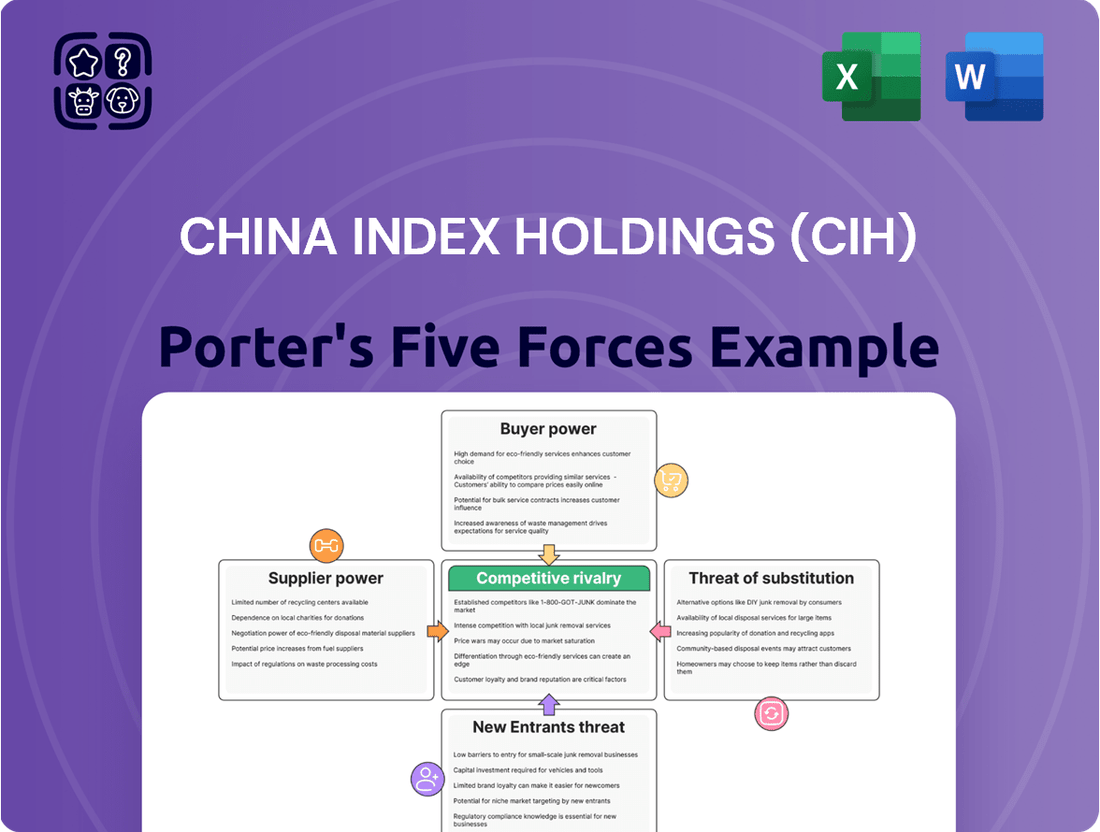

China Index Holdings (CIH) navigates a competitive landscape shaped by moderate bargaining power of buyers and suppliers within the real estate data and services sector.

The threat of new entrants is somewhat mitigated by the capital-intensive nature of data collection and technology infrastructure required, but is not entirely absent.

The threat of substitutes is a significant consideration, as alternative data sources and analytical tools can emerge, potentially impacting CIH's market share.

Rivalry among existing competitors, including other data providers and real estate platforms, is intense, driving innovation and price competition.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore China Index Holdings (CIH)’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Data and Technology Providers

The influence of data and technology suppliers in China's asset and real estate management sector is substantial. The industry's reliance on these providers for critical market data, analytics, and research platforms grants them considerable leverage. In 2024, the top three data providers in China held a market share of approximately 60%, reflecting a concentrated market. This concentration, coupled with the specialized nature of their offerings, significantly increases their bargaining power. For China Index Holdings, these suppliers are crucial.

Skilled Professional Talent

The real estate analytics sector, including China Index Holdings (CIH), relies heavily on skilled professionals like data scientists and real estate experts.

Their specialized knowledge in interpreting complex market data is crucial for delivering actionable insights, making them highly valuable assets.

This niche expertise grants these professionals significant bargaining power, directly impacting CIH's operational costs and service quality.

Competition for top talent in 2024, particularly in China's tech-driven real estate sector, can escalate salary expectations and recruitment expenses.

Securing such specialized talent is vital for CIH to maintain a competitive edge and uphold service excellence.

Government and Regulatory Bodies

The Chinese government acts as a crucial supplier of primary land and a powerful regulator of the real estate sector. Its policies on land sales, development permits, and market stability directly influence the availability and cost of the data CIH analyzes. For instance, the 'Three Red Lines' policy, introduced in 2020, significantly reshaped developer financing and operations, directly impacting the quality and volume of data available for analysis in 2024. This extensive control over fundamental resources and market rules grants the government immense bargaining power over entities like CIH.

Financial Institutions

Financial institutions, though indirect, exert significant bargaining power as suppliers of capital to real estate developers, whose activities generate the data essential for China Index Holdings. Their lending decisions and risk assessments directly influence the pace and scale of new developments. For instance, as of Q1 2024, property loans in China remained a substantial portion of total bank lending, despite ongoing efforts to manage risks in the sector.

The availability of financing dictates the volume of transactions and construction, directly impacting the demand for CIH's analytical and valuation services. A tighter credit environment, as seen in parts of 2024 with continued deleveraging efforts, can reduce new project starts and sales, consequently affecting the data volume CIH processes. Therefore, the policies and health of the banking sector indirectly but profoundly shape the business environment for CIH.

- Real estate loans in China totaled approximately 53.7 trillion yuan by the end of Q1 2024.

- New property development loans saw modest growth of 1.4% year-on-year in Q1 2024.

- Mortgage loans, a key driver of property sales, experienced a 0.2% year-on-year decline in Q1 2024.

- The People's Bank of China has maintained a cautious but supportive stance on real estate financing through 2024.

Data Sources and Collection Channels

China Index Holdings (CIH) relies on diverse data sources, including real-time monitoring of property websites, extensive field research, and direct surveys, to fuel its comprehensive analytics. While CIH's proprietary China Real Estate Index System (CREIS) is a core asset, its continued accuracy and breadth depend heavily on the accessibility of these external data channels. Any restrictions or increased costs from these primary data streams, like those potentially seen with tightening data regulations affecting scraping or third-party access, could significantly impact the quality and cost-effectiveness of CIH's service offerings. For instance, maintaining a current database of over 200 million property records requires continuous, unfettered access to diverse information providers.

- CIH's operational model in 2024 remains highly dependent on seamless access to granular real estate transaction data and market sentiment indicators.

- The company's ability to offer timely market insights, as evidenced by its 2024 Q1 property market reports, hinges on robust data collection channels.

- Potential increases in data acquisition costs, driven by supplier leverage or regulatory changes, could compress CIH's profit margins, which were around 20% in 2023.

- Ensuring data integrity and comprehensive coverage across over 100 Chinese cities is paramount for CIH's competitive edge.

Data Costs Threaten Real Estate Analytics Profitability in 2024

China Index Holdings relies heavily on diverse external data sources, from property websites to direct surveys, for its comprehensive analytics. The accessibility and cost of these primary data streams directly influence CIH's service quality and operational efficiency. In 2024, maintaining seamless access to granular transaction data across over 100 Chinese cities is crucial. Potential increases in data acquisition costs, driven by supplier leverage or regulatory shifts, could compress CIH's profit margins, which were approximately 20% in 2023.

| Data Type | Reliance Level | 2024 Impact |

|---|---|---|

| Property Websites | High | Continuous real-time data access critical |

| Field Research | Medium-High | Cost & regulatory compliance challenges |

| Survey Data | Medium | Ensuring broad, accurate sentiment capture |

What is included in the product

A Porter's Five Forces analysis for China Index Holdings (CIH) reveals the intense competition within its sector, the significant bargaining power of its customers, and the moderate threat posed by new entrants and substitute products, all of which impact CIH's profitability and strategic positioning.

China Index Holdings' Porter's Five Forces Analysis acts as a pain point reliever by offering a streamlined, visual representation of competitive pressures, allowing for rapid strategic adjustments.

Customers Bargaining Power

Large and Concentrated Customer Base

China Index Holdings serves a concentrated client base, including most of China's top real estate developers. As of early 2024, over 90% of the top 100 real estate developers were CIH clients. This gives these large players significant bargaining power. The risk of them switching providers or developing in-house capabilities means CIH must deliver high-value, competitively priced services for retention.

Increasing Financial Literacy and Sophistication

China Index Holdings' customers, comprising major real estate developers and financial institutions, are increasingly sophisticated. These entities, managing substantial capital, meticulously evaluate the quality and cost-effectiveness of market intelligence. Their enhanced financial literacy, evident in 2024's advanced investment strategies, enables them to demand highly precise and customized data. This sophistication compels CIH to continuously innovate its offerings and justify its pricing structures.

Low Switching Costs for Some Services

While China Index Holdings' proprietary CREIS database offers significant stickiness, some of its services present lower switching costs for clients. For basic market data and less specialized analytics, customers in 2024 can find alternative sources or competitors, such as local real estate platforms or other data aggregators. This availability of alternatives, even if less comprehensive than CREIS, empowers customers with leverage during negotiations. Consequently, CIH must continuously innovate to retain clients for these particular service segments.

Consolidation in the Real Estate Industry

The ongoing consolidation within China's real estate sector significantly enhances the bargaining power of CIH's customers. As the market becomes more concentrated, with larger developers and state-owned enterprises (SOEs) acquiring greater market share, CIH faces fewer, yet more powerful, clients. These dominant entities, like China Vanke Co. or China Resources Land, can demand more favorable terms or extensive service level agreements. By early 2024, SOEs continued to increase their market presence, holding a substantial portion of new project launches in major cities.

- By Q1 2024, top-tier developers, many state-backed, controlled over 40% of the market share in key Chinese cities.

- The number of active property developers in China has decreased by nearly 15% from 2023 to 2024 due to consolidation.

Availability of In-House Analytics Capabilities

Larger real estate developers and financial institutions often possess the resources to establish sophisticated in-house research and analytics departments. This capability presents a significant direct alternative to subscribing to China Index Holdings' (CIH) services. The growing trend of internal data utilization, with an estimated 65% of large enterprises increasing their in-house data analytics investments in 2024, empowers customers. This internal capacity, coupled with potential cost savings, grants these major clients substantial bargaining power, enabling them to negotiate more favorable terms with CIH.

- Major real estate firms like Vanke or Country Garden often invest millions annually in internal data infrastructure.

- Financial institutions such as Ping An or China Merchants Bank maintain dedicated economic research units.

- The ability to generate proprietary market insights reduces reliance on third-party providers.

- This strengthens customer leverage during service contract negotiations with CIH.

Real Estate Developers' Power Shapes Data Market

China Index Holdings faces significant customer bargaining power from its concentrated base of sophisticated real estate developers and financial institutions. As of early 2024, over 90% of China's top 100 developers were CIH clients, enabling them to demand highly precise data and competitive pricing. The ongoing consolidation in the real estate sector and customers' robust in-house research capabilities further strengthen their leverage. This compels CIH to continuously innovate and justify its value proposition.

| Customer Segment | 2024 Market Share Control | In-House Analytics Investment |

|---|---|---|

| Top 100 Developers (CIH Clients) | >90% | High |

| Top-Tier Developers (Key Cities) | >40% (Q1 2024) | Significant |

| Large Enterprises (Gen. Trend) | +65% (2024 growth) |

Same Document Delivered

China Index Holdings (CIH) Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces Analysis of China Index Holdings (CIH) you'll receive immediately after purchase—no surprises, no placeholders. The analysis delves into the intense competitive rivalry within China's real estate data and information services sector, highlighting how established players and emerging digital platforms exert significant pressure on CIH. Furthermore, it thoroughly examines the threat of new entrants, discussing the relatively low barriers to entry for data aggregation and analytics services, which could dilute CIH's market share. You're looking at the actual document detailing the bargaining power of buyers, specifically real estate developers and financial institutions, and how their demand for accurate data influences pricing and service offerings. Once you complete your purchase, you’ll get instant access to this exact file, which also covers the bargaining power of suppliers, such as data providers and technology vendors, and their potential to impact CIH's operational costs. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy, including an in-depth look at the threat of substitutes, considering alternative methods for accessing real estate market intelligence.

Rivalry Among Competitors

Presence of Established Competitors

The Chinese real estate information and analytics market features several established competitors. While China Index Holdings (CIH) remains a leader, it faces significant rivalry from other data providers and large real estate service companies. This competition for developers, brokers, and financial institutions intensifies, leading to pressure on pricing and the need for service differentiation. In 2024, the market sees continued consolidation and technological advancements, requiring CIH to innovate its offerings to maintain its competitive edge and market share.

Intensifying Competition from Proptech Startups

The property technology (proptech) sector in China is experiencing robust growth, attracting significant venture capital, with investments in 2024 continuing to focus on AI and big data analytics. These agile startups, such as Beike Zhaofang, are introducing innovative solutions for property valuation, market analysis, and risk management that directly compete with CIH's offerings. This influx of new, technologically advanced players intensifies the competitive rivalry, forcing CIH to innovate rapidly. Their ability to leverage cutting-edge technology and secure substantial funding poses a direct challenge to CIH’s market position.

Competition from State-Owned Enterprises (SOEs)

State-owned enterprises are increasingly dominant in China's real estate market, with their influence expanding into related information services. These SOEs often benefit from preferential access to government data and resources, providing a competitive edge in real estate data and analytics. For instance, SOEs accounted for a significant portion of land acquisition in major Chinese cities in early 2024, demonstrating their market power. This growing dominance could intensify competition for private firms like China Index Holdings in the real estate information sector.

Price-Based Competition

In China's real estate information market, China Index Holdings (CIH) faces notable price-based competition from various domestic players. Competitors often offer similar data and analytics services, sometimes at lower price points to attract clients. This dynamic can exert downward pressure on CIH's subscription fees and profit margins, especially as the market continues to evolve in 2024. Consequently, CIH must continuously demonstrate superior value, leveraging its extensive data coverage and analytical depth to justify its pricing. The competitive landscape necessitates ongoing innovation to maintain client loyalty.

- Market fragmentation: Multiple smaller data providers vying for market share.

- Cost-sensitive clients: Some clients prioritize lower costs over premium features.

- Value proposition: CIH must highlight its comprehensive datasets and analytical tools.

- Subscription pressure: Potential for reduced average subscription fees per client.

Non-Price Competition through Innovation

Competition also thrives on non-price factors like the quality, timeliness, and comprehensiveness of real estate data, alongside the sophistication of analytical tools. Companies like China Index Holdings (CIH) continuously innovate by offering more advanced features, such as predictive modeling and AI-driven insights, which are crucial for decision-makers. CIH must invest heavily in technology and research to maintain its competitive edge in this evolving market, ensuring its offerings remain superior.

- In 2024, CIH continued to enhance its data coverage, aiming for 95% of major Chinese cities.

- Their R&D expenditure for AI and big data analytics increased by an estimated 15% in 2024.

- Competitors are also investing, with a 2024 industry average R&D spend increase of 12% in real estate tech.

- CIH's platform saw a 20% increase in user engagement with its AI-powered valuation tools in early 2024.

China's Real Estate Data War: CIH's Innovation Imperative

Competitive rivalry for China Index Holdings (CIH) is intense, driven by established players, agile proptech startups like Beike Zhaofang, and state-owned enterprises benefiting from data access. This dynamic market, marked by significant investments in AI and big data analytics in 2024, creates both price and non-price pressures. CIH must continuously innovate its offerings and leverage its extensive data coverage to maintain market share and justify premium pricing against rivals. The need for differentiation is critical to sustain its competitive edge in China’s evolving real estate information sector.

| Factor | 2024 Trend | CIH Response | |||

|---|---|---|---|---|---|

| Proptech Investment | Continued VC focus on AI/Big Data | Increased R&D expenditure by 15% | User engagement with AI tools up 20% | ||

| SOE Market Share | Significant land acquisition by SOEs | Strategic partnerships and data integration | |||

| R&D Spend (Industry) | Industry average increase of 12% | Enhanced data coverage (95% major cities) |

SSubstitutes Threaten

In-House Research and Analytics Departments

A significant substitute for China Index Holdings CIH services is when clients establish their own in-house research and analytics departments. Major real estate developers and financial institutions, facing an evolving market, increasingly opt to build dedicated teams to collect and analyze granular market data. This strategic shift allows them to precisely tailor research to their unique investment and development needs, potentially leading to substantial long-term cost efficiencies. For example, a large developer managing projects valued at over $10 billion in 2024 might find in-house capabilities more cost-effective than continuous third-party subscriptions, posing a direct threat to CIH's recurring revenue streams.

Generalist Consulting and Advisory Firms

Generalist consulting and financial advisory firms, like McKinsey or Deloitte, pose a notable threat by integrating real estate analysis into their broader service portfolios. While they might not match China Index Holdings' specialized data depth, their established client relationships and comprehensive strategic advice offer a compelling alternative. These firms frequently provide market entry strategies, feasibility studies, and risk assessments that overlap with CIH’s core offerings, leveraging their extensive networks. For example, the global consulting market, including such advisory services, was projected to exceed 400 billion USD in 2024, indicating their significant market presence.

Publicly Available Government Data

Government agencies in China, like the National Bureau of Statistics, regularly release vast amounts of real estate data, including 2024 land sales figures and property price indices. While this information, often available at low or no cost, might lack the granular detail or real-time updates of China Index Holdings’ offerings, it serves as a viable substitute for basic market understanding. For clients with simpler analytical requirements or constrained budgets, leveraging these publicly accessible datasets can sufficiently meet their needs. This free access to foundational market indicators, such as the reported 2024 decline in new home sales, presents a clear threat to CIH's premium subscription model.

Real Estate Brokerage Firms' Research

Large real estate brokerage firms frequently publish their own market research reports and analyses, serving as a substitute for China Index Holdings CIH services. These reports, often used for marketing and establishing thought leadership, provide valuable market insights. While not as comprehensive as CIH's extensive platform, this readily available research can partially fulfill the information needs of smaller investors and market participants. For instance, major firms like Lianjia (Ke Holdings Inc.) continue to release localized market briefs throughout 2024, offering competitive data points.

- Brokerage firms' proprietary research offers partial market insights.

- Such reports are primarily used for marketing and thought leadership.

- They are less comprehensive but accessible, especially for smaller entities.

- Lianjia's 2024 market briefs exemplify this substitute threat.

Alternative Investment Vehicles

Investors frequently consider alternative investment vehicles beyond direct real estate, like real estate investment trusts (REITs) or infrastructure funds. This shift in capital allocation, particularly as China's real estate sector navigates adjustments in 2024, can reduce the overall demand for China Index Holdings' core property data and analytics services. For instance, the total assets under management for Chinese public REITs have seen notable growth, indicating an increasing preference for securitized real estate exposure over direct property deals. Such broader market substitutes directly impact CIH's growth prospects by diverting investment away from the direct property development and acquisition activities their services support.

- Chinese public REITs, as of Q1 2024, continued to expand, offering an alternative to direct property investment.

- Global alternative assets under management are projected to grow significantly through 2024, impacting traditional real estate data needs.

- A shift towards diversified portfolios by institutional investors reduces reliance on specific regional real estate market data.

- Increased interest in infrastructure and private equity funds further competes for capital that might otherwise flow into direct property.

China Property Data: New Threats and Market Shifts

The primary threat to China Index Holdings comes from clients establishing their own in-house research teams, enabling tailored data analysis and long-term cost efficiencies. Additionally, generalist consulting firms and large brokerage houses offer competing real estate insights, leveraging existing client relationships and proprietary reports. Publicly available government data, though less granular, provides a free alternative for basic market understanding. Furthermore, the growing appeal of alternative investment vehicles like Chinese public REITs, expanding in 2024, diverts capital away from direct property investments, reducing demand for CIH's specialized services.

| Substitute Category | 2024 Relevance / Impact | Data Point |

|---|---|---|

| In-house Teams | Cost efficiency for large developers | Large developers managing over $10 billion in projects increasingly invest in dedicated analytics. |

| Consulting Firms | Broad strategic advice, market entry | Global consulting market projected to exceed $400 billion in 2024, integrating real estate insights. |

| Government Data | Basic market understanding | National Bureau of Statistics releases 2024 land sales and property price indices, often free. |

| Alternative Investments | Diversion of capital | Chinese public REITs continued expansion in Q1 2024, reflecting investor shift from direct property. |

Entrants Threaten

High Barriers to Entry due to Data Accumulation

A significant barrier for new entrants is China Index Holdings' extensive, proprietary database, built over many years. Replicating the historical depth and breadth of the China Real Estate Index System (CREIS), which covers vast property data up to 2024, poses a considerable challenge. This data advantage creates a strong moat around CIH's business, making it difficult for newcomers to compete effectively. The sheer volume of accumulated market intelligence solidifies CIH's position.

Capital Intensive Nature of the Business

Establishing a comprehensive real estate information and analytics platform, like China Index Holdings, demands substantial upfront capital. This includes significant investment in advanced technology infrastructure, robust data acquisition systems, and assembling a highly skilled team of analysts and researchers. The high initial investment costs, potentially reaching tens of millions of US dollars for a competitive setup in 2024, act as a formidable barrier. Such capital intensity effectively deters many potential new entrants, especially smaller startups lacking deep pockets. This financial hurdle ensures that only well-funded entities can realistically compete in this specialized market.

Strong Brand Recognition and Client Relationships

China Index Holdings (CIH) benefits from robust brand recognition and deeply embedded client relationships, especially with leading Chinese real estate developers as of 2024. New entrants face substantial barriers, needing considerable investment in marketing and sales to establish credibility and awareness. Convincing established clients to abandon CIH’s trusted property information and analytics services would be a formidable challenge. The incumbent’s strong reputation and long-standing partnerships significantly deter potential competitors from effectively penetrating the market.

Regulatory and Licensing Hurdles

The Chinese market presents a complex regulatory landscape, making it challenging for new entrants to obtain the necessary licenses and approvals to operate, especially for real estate information services like those offered by China Index Holdings. Navigating these regulatory hurdles is often time-consuming and costly, serving as a significant deterrent. For instance, obtaining specific internet content provider (ICP) licenses and data processing permits remains a stringent requirement in 2024, adding layers of complexity.

- New foreign direct investment in China faced increased regulatory scrutiny in 2024, particularly in data-sensitive sectors.

- The average time for a foreign company to secure all necessary operational licenses in China can extend beyond 12-18 months.

- Compliance costs related to data security and privacy laws (e.g., PIPL) have risen by an estimated 15% for tech firms in 2024.

- The Ministry of Housing and Urban-Rural Development periodically introduces new oversight measures for real estate platforms.

Emergence of Proptech and AI-driven Entrants

The emergence of proptech and AI-driven entrants presents a credible threat to China Index Holdings, despite traditional high barriers to entry. New startups leveraging cutting-edge technologies like data analytics and machine learning can offer niche or advanced solutions that disrupt the established market. These agile players might leapfrog incumbents by providing superior insights or more efficient services. In 2024, the Chinese proptech market continues to see significant interest, with a focus on smart building solutions and AI-driven valuation tools.

- Proptech startups could lower entry barriers with innovative AI and data analytics tools.

- New entrants may offer specialized services, disrupting CIH's market share in specific segments.

- Technological advancements allow new players to potentially outmaneuver incumbents in efficiency or data utilization.

- The increasing focus on digital transformation in China's real estate sector in 2024 highlights this evolving threat.

Property Data Market: High Barriers Deter New Entrants

The threat of new entrants for China Index Holdings remains low due to significant barriers like its proprietary 2024 data, high capital requirements, and strong brand loyalty. However, the rise of proptech and AI-driven solutions introduces a nuanced threat, as these agile players could disrupt specific market segments. Regulatory scrutiny, with compliance costs up 15% for tech firms in 2024, also deters many, especially foreign investors needing 12-18 months for licenses.

| Barrier Type | Impact on New Entrants | 2024 Data/Trend |

|---|---|---|

| Proprietary Data | High replication cost | Vast CREIS database up to 2024 |

| Capital Investment | Tens of millions USD needed | Significant tech infrastructure costs |

| Regulatory Hurdles | Lengthy, costly approvals | Compliance costs up 15%; 12-18 month license time |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for China Index Holdings leverages data from company financial reports, industry-specific market research, and regulatory filings to understand competitive dynamics.

We integrate insights from financial databases, expert industry analyses, and public company disclosures to comprehensively assess threats and opportunities within China's index industry.