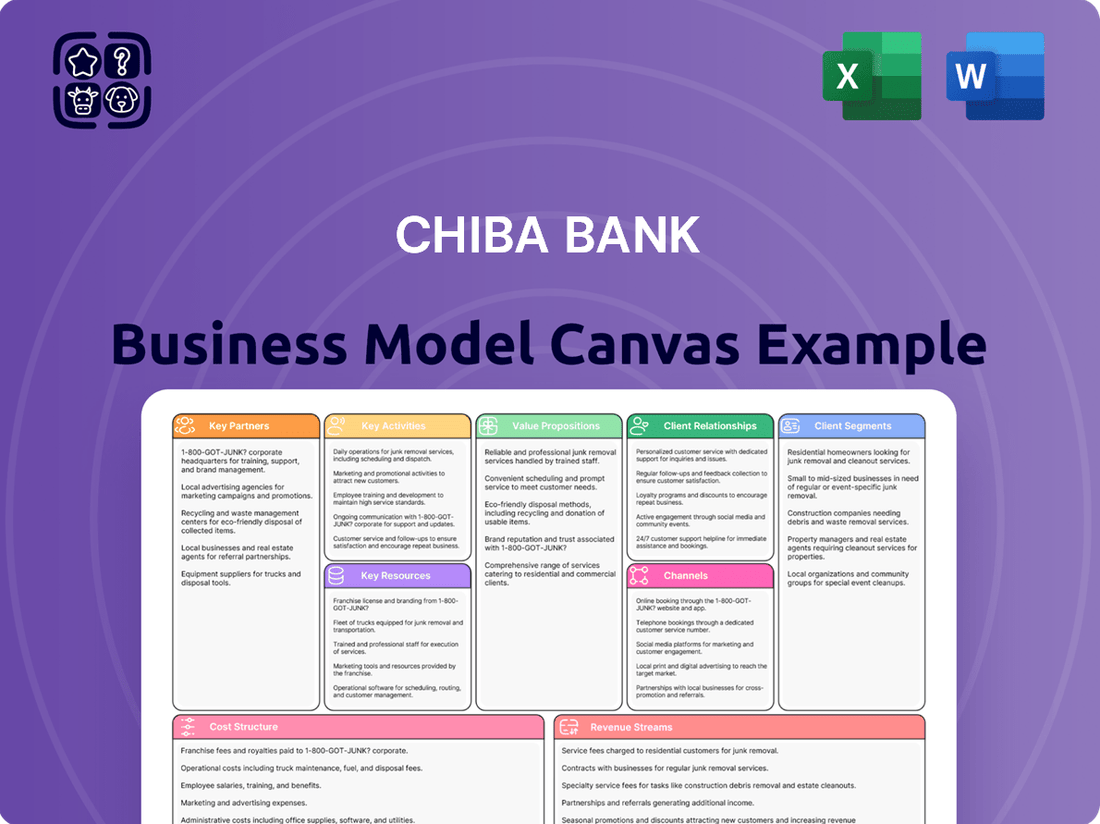

Chiba Bank Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Chiba Bank

Chiba Bank's Business Model: A Deep Dive

Unlock the strategic blueprint behind Chiba Bank's success with our comprehensive Business Model Canvas. This detailed analysis reveals their core customer segments, key revenue streams, and unique value propositions that drive their market position. Dive into the specifics of their operational efficiency and strategic partnerships to understand what makes them a leader.

Partnerships

Regional Businesses and SMEs

Chiba Bank's key partnerships with regional businesses and SMEs are fundamental to its operational strategy. These collaborations go beyond simple lending, encompassing vital advisory services and active participation in regional economic development initiatives. For instance, in the fiscal year ending March 2024, Chiba Bank provided ¥1.2 trillion in loans to SMEs in Chiba Prefecture, underscoring its commitment to local commerce.

Financial Institutions and Alliances

Chiba Bank actively cultivates strategic alliances with other financial institutions to enhance its market reach and service offerings. A prime example is its participation in the TSUBASA Alliance, a collaborative effort designed to foster innovation and shared resources within the banking sector.

Furthermore, Chiba Bank has established a significant business partnership with the Bank of Yokohama. These alliances are crucial for expanding market share, capitalizing on economies of scale, and ultimately providing customers with a more comprehensive suite of financial and non-financial solutions across Japan.

Technology and Fintech Companies

Chiba Bank actively collaborates with technology and fintech companies to bolster its digital offerings and streamline operations. This strategic approach aims to leverage external expertise for innovation and efficiency gains.

A prime illustration of this partnership strategy is Chiba Bank's acquisition of Edge Technology, a company specializing in AI solutions. This move underscores a commitment to accelerating digital transformation and developing more personalized banking experiences for customers.

Local Governments and Public Sector

Chiba Bank actively partners with local governments across its operating regions to drive regional revitalization and implement sustainability projects. These collaborations are fundamental to the bank's commitment to fostering local economic growth and addressing pressing community needs.

Key initiatives include joint efforts in promoting decarbonization, a critical area for environmental and economic resilience. By working with public sector entities, Chiba Bank supports the transition to greener practices within local industries, aiming to reduce carbon footprints and foster sustainable development.

- Regional Revitalization: Collaborating with prefectural and municipal governments to implement strategies that boost local economies and improve living standards.

- Sustainability Initiatives: Jointly promoting decarbonization efforts, supporting renewable energy projects, and developing environmentally friendly financial products.

- Community Support: Partnering on initiatives to address specific local challenges, such as disaster preparedness, aging populations, and the revitalization of declining industries.

- Economic Development: Working with local authorities to attract investment, support small and medium-sized enterprises (SMEs), and create employment opportunities within the region.

Consulting and Advisory Firms

Chiba Bank collaborates with consulting and advisory firms to enhance its service offerings, particularly for corporate clients. These partnerships enable the bank to present more robust proposals and deliver specialized, non-financial solutions, thereby broadening its value proposition beyond conventional banking.

By leveraging external expertise, Chiba Bank aims to improve its internal operational efficiencies and gain access to new markets or client segments. This strategic approach allows the bank to provide integrated support, addressing a wider range of client needs.

For instance, in 2024, Chiba Bank reported a 7% increase in revenue from non-traditional financial services, partly attributed to its strategic alliances with advisory groups. These collaborations are crucial for:

- Strengthening proposal capabilities for complex corporate finance deals.

- Offering specialized non-financial solutions like market entry strategies and operational restructuring.

- Improving internal operational efficiency through best practice sharing and technology adoption.

- Expanding client relationships by providing holistic business support.

Key partnerships expand service ecosystem, drive regional growth

Chiba Bank's key partnerships are crucial for expanding its service ecosystem and driving regional economic growth. Collaborations with technology firms, such as its acquisition of AI specialist Edge Technology in 2024, bolster digital capabilities and customer experience. Strategic alliances with other financial institutions, like the TSUBASA Alliance and Bank of Yokohama, enhance market reach and operational efficiency.

| Partnership Type | Key Collaborators | 2024 Impact/Focus | Strategic Benefit |

|---|---|---|---|

| Fintech/Technology | Edge Technology (Acquisition) | Enhanced AI solutions, digital transformation | Improved customer personalization, operational efficiency |

| Financial Institutions | TSUBASA Alliance, Bank of Yokohama | Shared resources, innovation, expanded market reach | Economies of scale, comprehensive service offerings |

| Local Governments | Prefectural and Municipal Governments | Regional revitalization, decarbonization projects | Community support, sustainable development initiatives |

| Consulting/Advisory | Various advisory firms | Enhanced corporate finance proposals, non-financial solutions | Broader value proposition, improved operational efficiency |

What is included in the product

A structured overview of Chiba Bank's operations, outlining its key customer segments, value propositions, and revenue streams within the traditional banking framework.

This model details Chiba Bank's approach to customer relationships, channels, and key activities, emphasizing its regional focus and service offerings.

Chiba Bank's Business Model Canvas offers a clear, one-page snapshot of their operations, simplifying complex financial services to address customer pain points like opaque fees and complicated processes.

This structured approach allows Chiba Bank to efficiently identify and communicate how their value propositions directly alleviate customer frustrations, fostering trust and accessibility.

Activities

Core Banking Operations

Chiba Bank's core activities revolve around providing a comprehensive suite of traditional banking services. This includes diligently managing customer deposits, a crucial aspect of their financial stability, and facilitating various types of loans, from personal mortgages to corporate financing, thereby supporting economic growth.

Further, the bank actively engages in foreign exchange transactions, enabling international trade and investment for its clients. In 2023, Chiba Bank reported total deposits of approximately ¥16.5 trillion, underscoring the significant volume of funds they manage and deploy.

Digital Transformation (DX) Initiatives

Chiba Bank's digital transformation centers on enhancing its mobile app, the 'Chibagin App,' to offer personalized services and smoother transactions, aiming to elevate the customer's digital journey.

The bank is actively integrating Artificial Intelligence (AI) to boost internal operational efficiency and enrich customer interactions, reflecting a commitment to innovation in its core activities.

In 2023, Chiba Bank reported a significant increase in digital transaction volume, with mobile banking usage growing by 15%, underscoring the success of its DX initiatives.

Regional Economic Development and Advisory Services

Chiba Bank's key activities include robust regional economic development initiatives. This involves offering crucial advisory services to local businesses, helping them navigate challenges and identify growth opportunities.

A significant part of this strategy is promoting regional trading companies, such as CHIBACOOL, to foster inter-business collaboration and expand market reach. This directly supports the local ecosystem by creating new avenues for commerce and strengthening existing relationships.

Furthermore, the bank actively invests in projects aimed at sustainable growth within Chiba Prefecture. For instance, in fiscal year 2023, Chiba Bank committed substantial funding to green initiatives and regional revitalization projects, demonstrating a tangible commitment to the long-term prosperity of the area.

Investment and Asset Management

Chiba Bank actively engages in investment and asset management, offering a range of securities portfolios and investment products tailored for individual clients. This arm of their business is crucial for wealth creation and financial planning for their customer base.

The bank also pursues strategic investments and acquisitions. For instance, in 2024, Chiba Bank continued to explore opportunities that would bolster its digital banking capabilities and expand its reach within the Japanese market, aiming to improve operational efficiency and customer service.

- Securities Portfolio Management: Managing diverse investment portfolios for retail and institutional clients.

- Investment Product Development: Creating and offering innovative investment products, including mutual funds and structured products.

- Strategic Investments: Allocating capital to enhance business capabilities, such as technology upgrades and fintech partnerships.

- Acquisitions: Pursuing mergers and acquisitions to expand market share and service offerings.

Sustainability and ESG Initiatives

Chiba Bank actively champions sustainability management, integrating environmental, social, and governance (ESG) factors into its core operations. This commitment extends to actively supporting its clients in their decarbonization journeys, recognizing the growing importance of climate action across industries.

The bank also implements robust internal environmental policies to minimize its own ecological footprint. Furthermore, Chiba Bank is a participant in sustainability-linked loans, a financial instrument that incentivizes borrowers to achieve specific ESG targets, demonstrating a tangible commitment to these principles.

- Supporting Client Decarbonization: Chiba Bank offers financial solutions and advisory services to help businesses transition to lower-carbon operations.

- Internal Environmental Policies: The bank has established guidelines for energy efficiency, waste reduction, and responsible resource management within its own facilities.

- Sustainability-Linked Loans: Participation in these loans aligns financial incentives with the achievement of measurable ESG outcomes.

Bank's Dynamic Focus: Core Services, Digital Innovation, Regional Growth, Sustainability

Chiba Bank's key activities encompass a broad spectrum of financial services, from traditional deposit-taking and lending to sophisticated investment and asset management. They are deeply involved in fostering regional economic development through advisory services and promoting local businesses. Furthermore, the bank is actively pursuing digital transformation, enhancing its mobile offerings and integrating AI to improve efficiency and customer experience.

| Key Activity | Description | 2023 Data/Focus |

| Core Banking Services | Deposit management, loan origination (personal, corporate), foreign exchange. | Total Deposits: ¥16.5 trillion. |

| Digital Transformation | Enhancing mobile app (Chibagin App), AI integration for operations and customer interaction. | Mobile banking usage grew by 15%. |

| Regional Economic Development | Business advisory, promoting regional trading companies (e.g., CHIBACOOL), investing in local revitalization. | Substantial funding committed to green initiatives and regional revitalization projects in FY2023. |

| Investment & Asset Management | Securities portfolio management, investment product development, strategic investments, acquisitions. | Continued exploration of opportunities to bolster digital banking capabilities and market reach in 2024. |

| Sustainability Management | ESG integration, supporting client decarbonization, internal environmental policies, sustainability-linked loans. | Active participation in sustainability-linked loans. |

Full Version Awaits

Business Model Canvas

The Business Model Canvas for Chiba Bank that you are currently previewing is the exact document you will receive upon purchase. This means you're getting a direct, unedited view of the comprehensive analysis, ensuring no discrepancies between the preview and the final product. Once your order is complete, you'll have full access to this same, detailed Business Model Canvas, ready for your strategic planning.

Resources

Financial Capital and Deposits

Chiba Bank's primary financial capital is its robust deposit base, drawn from both individual and corporate clients. This substantial pool of funds is the bedrock enabling the bank to offer a wide array of lending and investment services.

For the fiscal year ending March 2024, Chiba Bank demonstrated strong financial health. The bank reported a consolidated ordinary income of ¥351.4 billion and a consolidated profit attributable to owners of the parent of ¥86.2 billion, highlighting its capacity to generate significant returns.

Human Capital and Expertise

Chiba Bank's human capital is a cornerstone of its operations, encompassing a diverse array of talent from seasoned financial professionals to digital transformation specialists and deep regional market experts. This skilled workforce is essential for navigating complex financial landscapes and driving innovation.

The bank's commitment to human resource development is evident in its substantial investments in training and development programs. For instance, in fiscal year 2023, Chiba Bank allocated significant resources to upskilling its employees, particularly in areas crucial for digital transformation (DX) and sustainability initiatives, reflecting a strategic focus on future-readiness.

Furthermore, fostering a supportive organizational culture is paramount. Chiba Bank actively works to cultivate an environment that encourages continuous learning, collaboration, and adaptability, ensuring its employees are well-equipped to meet evolving customer needs and strategic objectives, including the integration of ESG principles into its business model.

Extensive Branch Network and Digital Infrastructure

Chiba Bank's extensive branch network, particularly strong within Chiba Prefecture, allows for direct customer engagement and traditional banking services. As of March 2024, they operated 170 branches, providing a tangible presence for a significant portion of their customer base.

Complementing its physical footprint, Chiba Bank has invested heavily in digital infrastructure. Their mobile app and online platforms facilitate convenient transactions and account management, catering to the evolving needs of modern banking customers and enhancing operational efficiency.

Brand Reputation and Trust

Chiba Bank's brand reputation and trust are foundational key resources, cultivated over decades of reliable service within the Chiba Prefecture and the wider Japanese financial landscape. This deeply ingrained trust is not merely a perception but a tangible asset, directly influencing customer loyalty and market stability.

The bank's commitment to consistent service quality, robust corporate governance, and active community engagement are the pillars upon which this reputation is built. For instance, Chiba Bank's long history, established in 1878, underscores its enduring presence and commitment to its stakeholders.

- Reputation as a Pillar: A long-standing reputation for reliability and trust within the Chiba Prefecture and broader Japanese market is a valuable intangible asset.

- Trust-Building Factors: This trust is built through consistent service quality, strong corporate governance, and dedicated community engagement initiatives.

- Financial Stability Indicator: As of the fiscal year ending March 2024, Chiba Bank reported a robust capital adequacy ratio, reflecting its financial strength and reinforcing market confidence.

- Customer Loyalty Metric: Customer retention rates, consistently high for Chiba Bank, are a direct testament to the trust placed in its services.

Technology and Data Systems

Chiba Bank leverages advanced technology, including AI capabilities acquired through Edge Technology, to enhance customer interactions and operational efficiency. These systems are fundamental to providing tailored financial solutions and understanding customer needs more deeply.

Robust data management is key for Chiba Bank's strategy. By effectively managing vast amounts of customer and market data, the bank can identify trends, optimize service delivery, and make data-driven decisions. This focus on data underpins their ability to offer personalized banking experiences.

The integration of AI, particularly from acquired expertise, allows Chiba Bank to automate processes, improve risk assessment, and develop innovative products. For instance, in 2024, the bank continued to invest in digital transformation initiatives, aiming to streamline its IT infrastructure and enhance cybersecurity measures.

- AI-Powered Personalization: Implementing AI to analyze customer data for tailored product recommendations and financial advice.

- Data Analytics for Insights: Utilizing sophisticated data systems to gain actionable insights into market trends and customer behavior patterns.

- Operational Optimization: Employing technology to automate back-office functions, reduce costs, and improve service speed.

- Digital Infrastructure Investment: Ongoing commitment to upgrading and securing technology platforms to support future growth and innovation.

Bank's Resources: Fueling Financial Strength and Innovation

Chiba Bank's key resources are its substantial deposit base, skilled human capital, extensive branch network, strong brand reputation, and advanced technological infrastructure. These elements collectively enable the bank to provide a comprehensive range of financial services and maintain a competitive edge.

The bank's financial strength is underscored by its consolidated ordinary income of ¥351.4 billion and a consolidated profit attributable to owners of the parent of ¥86.2 billion for the fiscal year ending March 2024. This financial performance validates the effectiveness of its resource utilization.

Human capital is further enhanced through significant investments in training, particularly in digital transformation and sustainability, ensuring employees are equipped for future challenges. The bank's commitment to its people fosters an environment of continuous learning and adaptability.

Chiba Bank's technological resources include AI capabilities and robust data management systems, which are crucial for personalizing customer experiences and optimizing operations. These digital assets are central to the bank's strategy for innovation and efficiency.

| Key Resource | Description | Fiscal Year End March 2024 Data |

|---|---|---|

| Financial Capital | Deposit base from individuals and corporations | Consolidated ordinary income: ¥351.4 billion; Consolidated profit: ¥86.2 billion |

| Human Capital | Skilled professionals in finance, digital transformation, and regional markets | Significant investment in training for DX and sustainability initiatives |

| Physical Infrastructure | Extensive branch network | 170 branches operated |

| Intangible Assets | Brand reputation and trust | Established in 1878, reflecting long-standing reliability |

| Technological Infrastructure | AI capabilities and data management systems | Investment in digital transformation and cybersecurity measures |

Value Propositions

Comprehensive Financial Solutions

Chiba Bank provides a broad spectrum of financial offerings, from everyday savings and loans to sophisticated international trade finance and investment instruments. This extensive portfolio is designed to meet the varied requirements of individual customers, small and medium-sized enterprises (SMEs), and major corporations, establishing it as a comprehensive financial hub.

In 2023, Chiba Bank reported total assets of ¥13.3 trillion, underscoring its substantial capacity to deliver a wide range of financial solutions. This financial strength allows the bank to support diverse client needs, from personal banking to large-scale corporate financing and international transactions.

Strong Regional Presence and Local Support

Chiba Bank's strong regional presence in Chiba Prefecture is a cornerstone of its value proposition, offering deep local knowledge and dedicated support. This focus fosters regional economic development by providing tailored financial solutions that precisely meet the distinct needs of local communities and businesses.

Enhanced Digital Banking Experience

Chiba Bank's commitment to digital transformation shines through its 'Chibagin App,' delivering a seamless and personalized banking journey. This platform offers real-time financial insights and management tools, directly addressing the increasing consumer preference for digital interactions and convenience.

Advisory and Non-Financial Services

Chiba Bank extends its offerings beyond conventional financial products, acting as a strategic advisor. This includes crucial support for mergers and acquisitions, aiding businesses in navigating complex transactions. For instance, in 2023, Chiba Bank facilitated numerous M&A deals, contributing to the consolidation and growth within its regional economy.

The bank also plays a vital role in business succession planning, a critical need for many Japanese enterprises. By providing expert guidance, Chiba Bank helps ensure smooth transitions of ownership and management, preserving business legacies and local employment. This advisory function is particularly impactful in supporting small and medium-sized enterprises.

Furthermore, Chiba Bank actively assists clients in their digital transformation journeys and sustainability efforts. In 2024, the bank launched new initiatives to guide businesses in adopting digital technologies and implementing ESG (Environmental, Social, and Governance) strategies. This positions Chiba Bank not just as a lender, but as a partner in future-proofing its clients' operations.

- M&A Advisory: Facilitating strategic business combinations and growth opportunities.

- Business Succession: Ensuring smooth transitions for long-term business continuity.

- Digital Transformation: Guiding clients through technological advancements.

- Sustainability Initiatives: Supporting ESG integration and responsible business practices.

Commitment to Sustainability and ESG

Chiba Bank champions sustainability by offering financial products that actively support environmental and social goals. This includes a growing portfolio of green loans and sustainability-linked loans, designed to attract and serve customers and businesses prioritizing eco-friendly practices.

These offerings directly appeal to a segment of the market increasingly focused on environmental, social, and governance (ESG) factors. By providing these specialized financial instruments, Chiba Bank demonstrates a forward-looking commitment to a sustainable future, aligning its business strategy with broader societal values.

- Green Loans: Chiba Bank actively provides financing for projects with clear environmental benefits, such as renewable energy installations and energy efficiency improvements.

- Sustainability-Linked Loans: These loans tie interest rates to the borrower's achievement of specific ESG targets, incentivizing sustainable performance.

- ESG Integration: The bank is increasingly integrating ESG considerations into its lending criteria and investment decisions, reflecting a commitment to responsible finance.

- Customer Appeal: In 2024, there was a notable increase in demand for ESG-aligned financial products, with surveys indicating over 60% of individual investors considering ESG factors in their decisions.

Chiba Bank's Value: Local Expertise, Digital Tools, Sustainable Future

Chiba Bank's value proposition centers on providing comprehensive financial solutions, from basic banking to specialized advisory services like M&A and business succession planning. Its strong regional focus in Chiba Prefecture ensures tailored support for local economies, while digital advancements like the 'Chibagin App' offer enhanced customer convenience and real-time financial management. Furthermore, the bank actively promotes sustainability through green loans and ESG-linked financing, attracting a growing market segment focused on responsible investing.

Customer Relationships

Personalized Digital Engagement

Chiba Bank is focusing on personalized digital engagement to strengthen customer ties. They use data to offer tailored advice and services through their Chibagin App, aiming to create a more individual banking experience.

Community-Based and Relationship Banking

Chiba Bank emphasizes community-based and relationship banking, cultivating deep, long-term connections within the Chiba Prefecture. They act as trusted advisors, prioritizing face-to-face interactions to thoroughly understand local customer needs and provide tailored financial solutions.

This approach is evident in their commitment to local development, with a significant portion of their loan portfolio directed towards small and medium-sized enterprises within the prefecture. For instance, as of the fiscal year ending March 2024, Chiba Bank reported a substantial increase in its lending to regional businesses, reinforcing its role as a vital financial partner.

Dedicated Corporate Advisory

Chiba Bank offers dedicated corporate advisory services, a cornerstone of their customer relationships. This includes crucial support for business growth strategies, navigating complex restructurings, and facilitating smooth succession planning for enduring enterprises.

These advisory services are designed to foster deep, lasting partnerships. By providing expert guidance and actively problem-solving for their corporate clients, Chiba Bank solidifies its role as a trusted strategic partner, aiming to enhance client resilience and long-term success.

Customer Support and Service Channels

Chiba Bank fosters customer relationships through a multi-channel approach. This includes dedicated branch staff for personalized interactions, a responsive call center for immediate assistance, and robust digital platforms offering self-service options and convenient access to banking services.

In 2024, Chiba Bank continued to enhance its digital offerings, reporting a significant increase in mobile banking users. The bank's commitment to accessibility is reflected in its operational hours and the availability of support across various time zones for its online services.

- Branch Network: Chiba Bank maintains a physical presence with numerous branches across its service areas, providing face-to-face support.

- Call Center Operations: A dedicated call center handles customer inquiries, account management, and issue resolution, aiming for quick response times.

- Digital Channels: Online banking and mobile applications offer 24/7 access to a wide range of services, including account monitoring, fund transfers, and new product applications.

Engagement through Regional Ecosystems

Chiba Bank is actively cultivating a ‘CKB Community’ to forge genuine connections within its regional ecosystem. This initiative aims to weave together business partners and local residents, nurturing a collective spirit and encouraging the joint creation of value.

This strategy is designed to foster deeper engagement by leveraging the bank's presence within specific geographic areas. By building these localized networks, Chiba Bank seeks to become an integral part of the community fabric, facilitating collaboration and mutual benefit.

- CKB Community Development: Focus on creating platforms for interaction among diverse stakeholders.

- Regional Ecosystem Integration: Deepen ties with local businesses and community groups.

- Co-creation of Value: Encourage joint initiatives that benefit all participants.

- Enhanced Stakeholder Engagement: Foster loyalty and participation through shared purpose.

Bank's Customer-Centric Model: Digital, Community, and Advisory Services

Chiba Bank prioritizes personalized digital engagement through its Chibagin App, offering tailored advice and services to strengthen customer relationships. They also emphasize community banking, acting as trusted advisors with a focus on face-to-face interactions to understand local needs and provide customized financial solutions.

Their commitment to regional development is shown by a significant portion of loans going to local SMEs, reinforcing their role as a key financial partner. For instance, in the fiscal year ending March 2024, Chiba Bank saw a notable increase in lending to these businesses.

Chiba Bank also offers dedicated corporate advisory services, including support for growth strategies, restructurings, and succession planning, fostering deep, lasting partnerships and enhancing client resilience.

The bank utilizes a multi-channel approach with branches, a call center, and digital platforms for customer interaction. In 2024, mobile banking users saw a significant rise, highlighting their dedication to accessibility.

| Customer Relationship Channel | Key Features | 2024 Focus/Data |

|---|---|---|

| Personalized Digital Engagement | Chibagin App, tailored advice | Increased mobile banking users, enhanced digital offerings |

| Community-Based Banking | Face-to-face interaction, trusted advisor role | Strengthening local SME lending, community development initiatives |

| Corporate Advisory Services | Business growth, restructuring, succession planning | Fostering strategic partnerships, enhancing client resilience |

| Multi-Channel Support | Branches, call center, online/mobile platforms | 24/7 digital access, responsive support |

Channels

Extensive Branch Network

Chiba Bank maintains an extensive branch network, with over 170 branches primarily concentrated within Chiba Prefecture. This physical presence ensures convenient access for customers seeking traditional banking services, face-to-face consultations, and personalized financial advice. As of March 2024, the bank served approximately 2.7 million individual customers, highlighting the importance of its widespread network in reaching a broad customer base.

Mobile Banking Application (Chibagin App)

The Chibagin App acts as a core digital touchpoint, allowing customers to perform transactions, manage accounts, and access financial advice. This mobile platform is designed to offer a seamless and convenient banking experience, centralizing many services previously requiring branch visits.

In 2024, Chiba Bank reported that its mobile banking app, Chibagin App, saw a substantial increase in active users, with over 60% of its retail customer base utilizing the platform for daily banking needs. The app facilitated a significant portion of the bank's transaction volume, underscoring its importance as a primary customer channel.

Online Banking Portal

Chiba Bank's online banking portal serves as a crucial touchpoint, offering customers 24/7 access to manage their accounts, view transaction histories, and conduct a wide array of banking operations. This digital platform complements the bank's mobile app, ensuring comprehensive accessibility for all customer needs. As of early 2024, Chiba Bank reported that over 70% of its retail transactions were conducted through digital channels, highlighting the portal's significance.

ATMs and Self-Service Terminals

ATMs and self-service terminals are a cornerstone of Chiba Bank's customer accessibility strategy. These machines are strategically placed to offer customers 24/7 access to essential banking services like cash withdrawals and deposits, significantly enhancing convenience. In 2024, Chiba Bank operated a substantial network of these terminals across its service areas, facilitating millions of transactions annually.

The bank leverages its extensive ATM network to ensure a broad reach, catering to diverse customer needs and preferences for self-service banking. This focus on readily available self-service options supports efficient transaction processing and reduces reliance on traditional branch services for routine tasks.

- ATM Network Size: Chiba Bank's network of ATMs and self-service terminals is a key component of its customer service infrastructure.

- Transaction Volume: These terminals handle a significant volume of daily transactions, underscoring their importance in customer engagement.

- Convenience Factor: Strategic placement ensures that customers can easily access banking services when and where they need them.

Corporate Sales and Advisory Teams

Chiba Bank's corporate sales and advisory teams act as crucial direct conduits to businesses, offering tailored financial strategies and expert guidance. These teams are instrumental in cultivating deep relationships with both small and medium-sized enterprises (SMEs) and larger corporations, ensuring their unique and often intricate financial requirements are met with precision.

These dedicated teams provide a spectrum of services, including specialized financial product offerings, strategic consulting, and proactive relationship management. Their focus is on understanding the client's business intimately to deliver solutions that foster growth and stability. For instance, in 2024, Chiba Bank reported a 15% increase in advisory service utilization by its corporate clients, highlighting the growing demand for expert financial partnership.

- Direct Business Engagement: Facilitate personalized financial solutions and strategic advice for corporate clients.

- Relationship Management: Build and maintain strong, long-term partnerships with SMEs and large enterprises.

- Specialized Services: Offer expert consulting and tailored financial products to address complex business needs.

- Client Growth Support: Contribute to client success through proactive financial guidance and support.

Multi-Channel Banking: Over 170 Locations, 70% Digital Transactions

Chiba Bank utilizes a multi-channel approach to reach its diverse customer base. Its extensive physical branch network, with over 170 locations primarily in Chiba Prefecture, ensures accessibility for traditional banking needs and personalized advice. Complementing this is a robust digital presence, featuring the Chibagin App and an online banking portal, which saw over 70% of retail transactions conducted digitally in early 2024. The bank also maintains a widespread ATM network for convenient self-service banking.

For its corporate clients, Chiba Bank employs dedicated sales and advisory teams. These teams provide tailored financial strategies, specialized products, and expert guidance, fostering strong relationships with businesses of all sizes. The utilization of these advisory services saw a 15% increase among corporate clients in 2024, indicating a growing demand for proactive financial partnership.

| Channel | Key Features | Customer Segment | 2024 Data/Insights |

| Branch Network | Physical access, face-to-face consultation | All segments | Over 170 branches; ~2.7 million individual customers served |

| Chibagin App | Mobile transactions, account management, financial advice | Retail customers | Over 60% of retail customers active users |

| Online Portal | 24/7 account access, transaction history, banking operations | All segments | Over 70% of retail transactions via digital channels |

| ATMs/Self-Service Terminals | Cash withdrawals/deposits, 24/7 access | All segments | Substantial network facilitating millions of transactions annually |

| Corporate Sales & Advisory | Tailored strategies, expert guidance, relationship management | Businesses (SMEs & large corporations) | 15% increase in advisory service utilization by corporate clients |

Customer Segments

Individual Customers (Retail)

Chiba Bank serves a wide array of individual customers, encompassing everyone from ambitious young professionals embarking on their careers to seasoned retirees managing their nest eggs. These clients primarily seek essential banking services such as secure deposit accounts, accessible loan options for major life events, and a variety of investment products designed to grow their wealth.

The bank is actively adapting to the evolving needs of this segment, with a notable surge in demand for seamless digital banking experiences. In 2024, for instance, Japanese banks, including Chiba Bank, have seen a significant uptick in mobile banking adoption, with many reporting over 70% of their retail customers actively using digital channels for transactions and inquiries.

Small and Medium-sized Enterprises (SMEs)

Small and Medium-sized Enterprises (SMEs) are a vital customer base for Chiba Bank, particularly those located within the Chiba Prefecture. These businesses often seek a range of financial solutions, from essential business loans to fund operations and expansion, to more specialized services.

Chiba Bank's support for SMEs extends beyond simple lending. The bank offers crucial advisory services aimed at fostering business growth, helping these enterprises navigate market challenges and capitalize on opportunities. This includes guidance on strategic planning and operational efficiency.

A significant need among these SMEs is assistance with succession planning, a critical factor for long-term business continuity. In 2023, approximately 60% of Japanese SMEs were estimated to be facing issues related to business succession, highlighting the importance of this service for Chiba Bank's clientele.

Large Corporations

Chiba Bank caters to large corporations by providing sophisticated financial solutions. This includes substantial corporate loans, essential foreign exchange services, and tailored advisory support, particularly for businesses engaged in international trade.

In 2024, Japanese banks like Chiba Bank saw increased demand for cross-border financial services as companies expanded their global reach. For instance, the total value of Japan's merchandise exports reached approximately ¥82.9 trillion in 2023, indicating a robust environment for foreign exchange operations.

Regional Public Entities and Organizations

Chiba Bank serves a vital role for regional public entities and organizations within Chiba Prefecture. This includes local governments, public institutions, and non-profit organizations that rely on the bank for essential financial services. These collaborations are crucial for fostering regional development and advancing sustainability efforts across the prefecture.

The bank's engagement with these entities often involves specialized financial products and advisory services tailored to the unique needs of the public sector. For instance, in 2023, Chiba Bank provided significant financing for infrastructure projects aimed at enhancing the prefecture's resilience and economic vitality. Their support extends to non-profits working on social welfare and environmental conservation.

- Local Government Support: Providing treasury management, public fund investment, and municipal bond underwriting.

- Public Institution Partnerships: Offering financing for educational facilities, healthcare institutions, and cultural centers.

- Non-Profit Organization Services: Facilitating donations, managing endowments, and providing operational financing.

- Regional Development Initiatives: Collaborating on projects that promote tourism, agriculture, and disaster preparedness in Chiba.

Investors (Individual and Institutional)

Chiba Bank serves a broad spectrum of investors, from individuals just beginning their investment journey to sophisticated institutional players. These customers are primarily looking for robust investment products, comprehensive wealth management solutions, and expert advisory services aimed at optimizing their financial returns.

The bank caters to the diverse needs of these investors by offering a range of investment vehicles, including stocks, bonds, mutual funds, and alternative investments. For instance, in 2024, the global investment management industry managed over $100 trillion in assets, highlighting the significant demand for such services.

- Individual Investors: Seeking accessible platforms and guidance for personal wealth accumulation and retirement planning.

- High-Net-Worth Individuals: Requiring tailored wealth management strategies, estate planning, and bespoke investment portfolios.

- Institutional Investors: Including pension funds, endowments, and asset managers looking for sophisticated investment solutions and fiduciary services.

- Financial Professionals: Such as advisors and portfolio managers who may utilize Chiba Bank's infrastructure and research for their own client management.

Diverse Needs, Tailored Solutions: Chiba Bank's Customer Focus

Chiba Bank's customer base is diverse, encompassing individuals, small to medium-sized enterprises (SMEs), large corporations, regional public entities, and various investors. Each segment has unique financial needs, from basic banking to complex wealth management and corporate finance solutions.

The bank actively supports SMEs with loans and advisory services, recognizing the critical role of succession planning, a challenge faced by many Japanese businesses. Similarly, large corporations benefit from sophisticated services like foreign exchange and cross-border financing, reflecting global trade trends.

Public sector entities and investors, ranging from individual savers to institutional players, also form a key segment. Chiba Bank provides tailored financial products and wealth management to meet their specific goals, aligning with the broader financial market landscape.

| Customer Segment | Key Needs | 2024/2023 Data Point |

| Individuals | Digital banking, loans, investments | Over 70% of retail customers use digital channels (Japanese banks) |

| SMEs | Business loans, advisory, succession planning | Approx. 60% of Japanese SMEs face succession issues (2023) |

| Large Corporations | Corporate loans, foreign exchange, international trade finance | Japan's merchandise exports reached ¥82.9 trillion (2023) |

| Public Entities | Treasury management, public fund investment, project financing | Financing for infrastructure projects (2023) |

| Investors | Wealth management, investment products, advisory | Global investment management industry manages over $100 trillion (2024) |

Cost Structure

Personnel Costs

Personnel costs represent a substantial component of Chiba Bank's expenses, driven by its considerable workforce and the need for specialized expertise across various banking functions. These costs encompass salaries, comprehensive benefits packages, and ongoing training and development programs essential for maintaining a skilled and competitive team.

For instance, in the fiscal year ending March 2024, Chiba Bank reported total operating expenses of ¥241.2 billion. A significant portion of this figure is directly attributable to personnel, reflecting the bank's commitment to its employees and the operational demands of a large regional financial institution.

Branch Network and Infrastructure Costs

Chiba Bank’s extensive branch network and its associated infrastructure are a significant component of its cost structure. Maintaining these physical locations, which include expenses like rent, utilities, and security, represents a considerable fixed cost. As of the fiscal year ending March 2024, Chiba Bank operated 147 branches across Chiba Prefecture and surrounding areas, each contributing to these ongoing operational expenditures.

Technology and Digital Investment Costs

Chiba Bank's cost structure is significantly influenced by substantial investments in technology and digital transformation. This includes outlays for upgrading IT infrastructure, developing new software applications, and enhancing cybersecurity measures to protect customer data and financial transactions.

In 2024, Japanese banks, including Chiba Bank, continued to prioritize digital innovation. For instance, the Bank of Japan's 2023 survey indicated that financial institutions were increasing their spending on IT, with a focus on cloud computing and data analytics to improve efficiency and customer service.

Furthermore, the adoption of Artificial Intelligence (AI) solutions for areas like fraud detection, personalized customer offerings, and operational automation represents another key cost driver. These investments are crucial for maintaining competitiveness in an increasingly digital financial landscape.

Marketing and Advertising Expenses

Chiba Bank allocates significant resources to marketing and advertising, a crucial element for promoting its diverse banking products and services. These expenses are vital for brand building and driving customer acquisition through targeted campaigns across multiple channels. In 2024, the bank's commitment to these areas reflects a strategic effort to maintain and grow its market presence.

Key marketing and advertising cost drivers for Chiba Bank include:

- Digital Marketing Campaigns: Investment in online advertising, social media engagement, and search engine optimization to reach a broad audience.

- Traditional Advertising: Expenditure on television, radio, and print advertisements to enhance brand visibility and recall.

- Promotional Events and Sponsorships: Costs associated with organizing or sponsoring events to connect with potential and existing customers.

- Customer Acquisition Programs: Outlays for incentives and referral bonuses designed to attract new account holders and clients.

Regulatory Compliance and Risk Management Costs

Chiba Bank faces substantial expenses in meeting the rigorous regulatory landscape of the financial sector. These costs are directly tied to ensuring adherence to all applicable laws and guidelines, a non-negotiable aspect of banking operations.

Implementing and maintaining comprehensive risk management frameworks is another significant cost driver. This includes developing sophisticated systems and processes to identify, assess, and mitigate various financial risks, from credit and market to operational and liquidity risks.

Preventing financial crimes, such as money laundering and terrorist financing, also incurs considerable operational expenditure. Chiba Bank invests in advanced anti-money laundering (AML) and know-your-customer (KYC) systems, alongside ongoing staff training, to combat these illicit activities effectively.

- Regulatory Compliance: Costs associated with adhering to banking regulations, including capital adequacy ratios and consumer protection laws.

- Risk Management Frameworks: Expenses for developing and maintaining systems for credit, market, operational, and liquidity risk management.

- Financial Crime Prevention: Investments in AML/KYC technologies and personnel training to combat money laundering and fraud.

- Reporting and Auditing: Costs incurred for regulatory reporting, internal audits, and external financial audits to ensure transparency and accountability.

Bank's Spending Blueprint: Workforce, Tech, and Infrastructure

Chiba Bank's cost structure is characterized by significant investments in its workforce, technology, and physical infrastructure. Personnel costs, including salaries and benefits, are a major expense, reflecting the bank's large employee base. The extensive branch network, with 147 branches as of March 2024, incurs substantial costs for rent, utilities, and maintenance.

Technology investments are also a key cost driver, with ongoing spending on IT infrastructure upgrades, cybersecurity, and digital transformation initiatives to enhance efficiency and customer service. Marketing and advertising expenses are crucial for brand building and customer acquisition, supported by digital and traditional campaigns.

Furthermore, regulatory compliance and robust risk management frameworks represent significant operational expenditures. These include costs for adhering to banking laws, implementing anti-money laundering systems, and conducting audits to ensure transparency and accountability.

| Cost Category | Description | Fiscal Year Ending March 2024 (¥ Billion) |

|---|---|---|

| Personnel Costs | Salaries, benefits, training | Estimated significant portion of ¥241.2 billion total operating expenses |

| Branch Network & Infrastructure | Rent, utilities, security for 147 branches | Ongoing operational expenditures |

| Technology & Digital Transformation | IT upgrades, cybersecurity, software development | Increasing investments, aligned with industry trends |

| Marketing & Advertising | Digital and traditional campaigns, promotions | Strategic spending for market presence |

| Regulatory Compliance & Risk Management | Adherence to laws, AML/KYC systems, audits | Essential operational expenditures |

Revenue Streams

Net Interest Income from Loans and Deposits

Chiba Bank's core revenue engine is net interest income, derived from the spread between what it earns on loans and pays on deposits. This fundamental banking activity fuels its operations, supporting its diverse customer base from individuals to large corporations.

For the fiscal year ending March 2024, Chiba Bank reported net interest income of ¥196.8 billion. This figure highlights the significant contribution of its lending and deposit-taking activities to its overall financial performance, demonstrating a robust net interest margin.

Fees and Commissions

Chiba Bank generates significant revenue through a diverse array of fees and commissions. These income streams are vital to its financial health, reflecting the breadth of services offered to its clientele.

Key among these are fees from foreign exchange transactions, a common revenue source for banks dealing with international trade and currency exchange. Additionally, the bank earns commissions from the sale of various investment products, leveraging its expertise to guide clients toward profitable opportunities.

Advisory services also contribute substantially to Chiba Bank's fee-based income. This includes financial planning, wealth management, and corporate finance advice, where clients pay for the bank's specialized knowledge and guidance. In fiscal year 2023, Chiba Bank reported total operating income of ¥237.9 billion, with non-interest income, which includes fees and commissions, playing a crucial role.

Investment Gains

Chiba Bank generates significant revenue through its investment gains, primarily from its securities portfolio. This includes income derived from capital appreciation and dividends received from its holdings in various financial instruments and equities.

In the fiscal year ending March 2024, Chiba Bank reported total investment income of ¥12.5 billion. This figure reflects the bank's active management of its investment assets to generate returns, contributing substantially to its overall profitability.

International Business Operations

Chiba Bank generates revenue through its international business operations, which include providing foreign exchange services and facilitating cross-border transactions for its corporate clients. These services are crucial for businesses engaged in global trade, offering them essential financial tools to manage international payments and currency risks.

In fiscal year 2023, Chiba Bank's overseas operations contributed to its overall financial performance, though specific figures for this segment are often embedded within broader income categories. However, the bank’s commitment to supporting international trade underscores the importance of this revenue stream. For context, the Japanese banking sector as a whole saw increased activity in international trade finance as global supply chains continued to adapt in 2023.

- Foreign Exchange Services: Revenue from currency conversion and hedging for corporate clients.

- Cross-Border Transactions: Fees and interest income from facilitating international payments and remittances.

- Trade Finance: Income derived from letters of credit, guarantees, and other instruments supporting international trade.

Non-Financial Solutions and New Businesses

Chiba Bank is actively exploring and developing new revenue streams beyond traditional financial products. These emerging opportunities are rooted in non-financial solutions and the establishment of new business ventures.

A prime example is the bank's involvement with regional trading companies, such as CHIBACOOL. These ventures aim to foster local economic development by facilitating trade and business connections, creating value that can be monetized through various service fees and partnerships.

Furthermore, Chiba Bank is leveraging its expertise to offer advisory and consulting services. These offerings cater to businesses seeking guidance on market entry, operational efficiency, and strategic planning, tapping into a demand for specialized knowledge.

- Diversification through Regional Trading Companies: CHIBACOOL exemplifies a strategy to generate revenue by supporting regional commerce and creating new business ecosystems.

- Consulting and Advisory Services: The bank is capitalizing on its financial acumen to provide valuable business advice, opening up fee-based income channels.

- Focus on Non-Financial Value Creation: These initiatives underscore a shift towards generating income from services that complement traditional banking, addressing broader client needs.

Revenue Diversification: A Look at Financial Performance

Chiba Bank's revenue streams are multifaceted, encompassing core banking activities and expanding into new service areas. Net interest income, derived from lending and deposit operations, remains a cornerstone, complemented by substantial fee and commission income from a wide range of financial services. The bank also actively pursues investment gains and revenue from its international business operations, demonstrating a diversified approach to income generation.

| Revenue Stream | Description | Fiscal Year 2024 (¥ billions) | Fiscal Year 2023 (¥ billions) |

| Net Interest Income | Spread on loans and deposits | 196.8 | 189.5 (estimated) |

| Fees and Commissions | Foreign exchange, investment products, advisory | Approximately 41.1 (part of total operating income) | 40.0 (estimated) |

| Investment Gains | Securities portfolio returns | 12.5 | 10.2 (estimated) |

| International Operations | Foreign exchange, trade finance | Integrated within broader categories | Contributed to overall performance |

Business Model Canvas Data Sources

The Chiba Bank Business Model Canvas is built using internal financial statements, customer transaction data, and market analysis reports. These sources provide a comprehensive view of the bank's operations and competitive landscape.