Boeing Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Boeing Bundle

Don't Miss the Bigger Picture

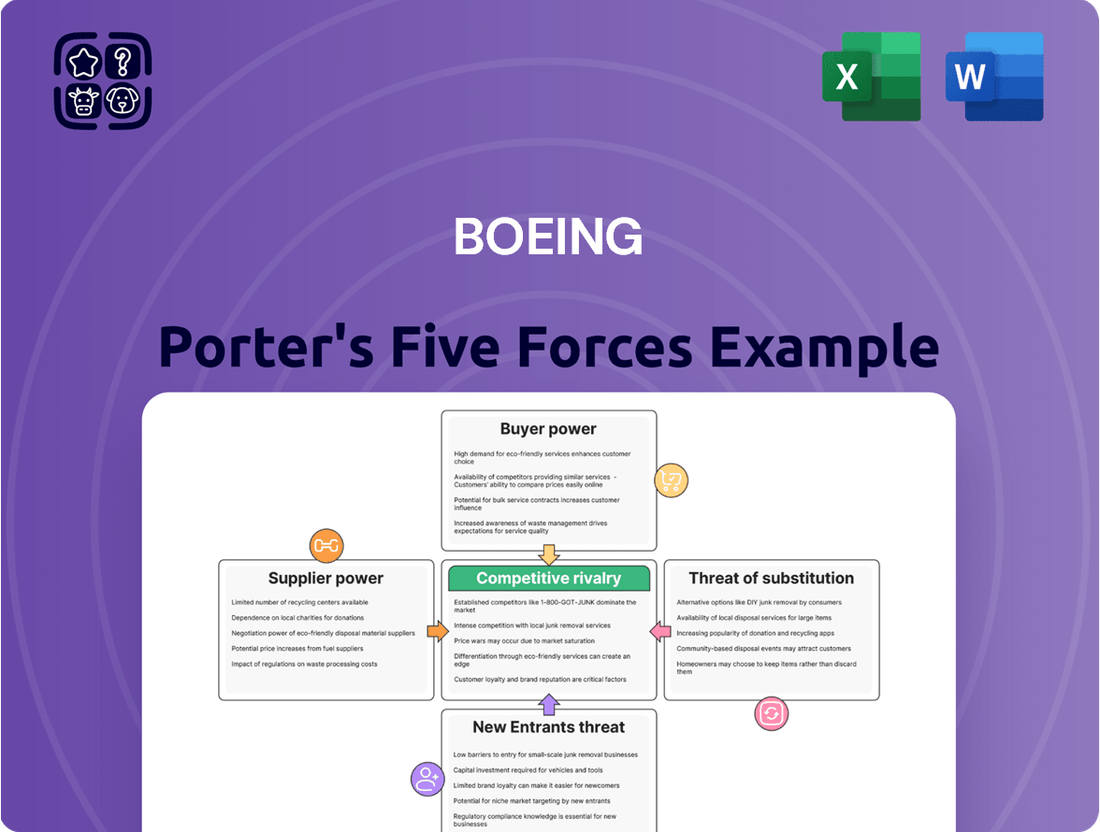

Boeing operates in an industry heavily influenced by intense rivalry and the significant bargaining power of its major customers. The threat of new entrants, while present, is somewhat mitigated by high capital requirements and established brand loyalty. However, the power of suppliers, particularly for specialized components, can exert considerable pressure on Boeing’s margins.

The threat of substitute products, while not immediate in the commercial airline sector, exists in the long term with advancements in transportation. Understanding these forces is crucial for any stakeholder in the aerospace industry. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Boeing’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Dependency

Boeing's reliance on a select group of suppliers for highly specialized components, like advanced engines and sophisticated avionics, significantly amplifies supplier bargaining power. These suppliers often hold patents or unique manufacturing processes, making it challenging and costly for Boeing to find alternatives. For instance, the long lead times and intricate integration required for new engine models mean Boeing is often locked into specific suppliers for extended periods, as was seen with the development of the 787 Dreamliner's engines.

High Switching Costs

The aerospace industry demands rigorous qualification and integration processes for new suppliers, a significant hurdle that translates into high switching costs for aircraft manufacturers like Boeing.

These complexities are driven by stringent safety regulations and the intricate nature of integrating new components with existing aircraft designs, making it a lengthy and costly endeavor.

For example, in 2024, the average time to certify a new aerospace supplier could extend to several years, involving extensive testing and validation.

This lengthy process solidifies the bargaining power of existing, pre-qualified suppliers, as Boeing faces substantial financial and operational risks in switching to unproven alternatives.

Supplier Concentration and Consolidation

The aerospace sector has experienced considerable consolidation, resulting in a reduced number of dominant suppliers for crucial aircraft components. This concentration inherently limits Boeing's sourcing alternatives.

For instance, the market for certain complex engine components or specialized avionics systems is often dominated by a handful of large, established players. This situation can grant these suppliers significant bargaining power, enabling them to dictate terms and pricing more effectively to buyers like Boeing.

In 2023, the aerospace and defense industry saw continued M&A activity, with major players acquiring smaller, specialized firms to bolster their capabilities. This trend further consolidates the supply base, intensifying the leverage of these larger entities.

When a supplier holds a near-monopoly on a critical part, Boeing's ability to negotiate favorable pricing or contract terms is substantially diminished, directly impacting its cost structure and operational flexibility.

Proprietary Technology and Patents

Many aerospace suppliers invest significantly in research and development, leading to patents for crucial technologies. This proprietary intellectual property means Boeing relies on these suppliers for advancements in materials, manufacturing techniques, and critical aircraft systems. For example, companies like Spirit AeroSystems, a key supplier for Boeing, hold patents on advanced composite structures that are vital for aircraft efficiency and performance.

This dependence on patented technology grants suppliers considerable bargaining power. Boeing's ability to negotiate pricing or find alternative suppliers is constrained when a competitor holds exclusive rights to essential components or processes. In 2023, Boeing's significant reliance on a few key suppliers for advanced materials, often protected by patents, underscored this dynamic.

- Patented Innovations: Suppliers possess patents for unique materials and manufacturing methods, creating a barrier to entry for competitors.

- R&D Investment: Substantial investments in research and development by suppliers result in advanced, often patent-protected, technologies.

- Dependency Creation: Boeing's need for these specialized, proprietary technologies makes it reliant on specific suppliers, diminishing its negotiation leverage.

- Limited Alternatives: The existence of patents restricts Boeing's ability to source critical components from multiple vendors, concentrating power with the patent holder.

Quality and Reliability Requirements

The aerospace industry, and by extension Boeing, places an extremely high premium on quality and reliability. Suppliers who consistently deliver components meeting stringent aerospace specifications, backed by a robust history of performance, wield considerable sway. This is because any deviation can have catastrophic consequences for safety, regulatory compliance, and brand reputation, making these suppliers indispensable.

For instance, in 2024, the aerospace sector continued to grapple with supply chain challenges, particularly for critical components. Suppliers of highly specialized materials or advanced manufacturing processes, who have demonstrated unwavering quality and on-time delivery, are less susceptible to price pressure. Their ability to meet Boeing's exacting demands, which often involve extensive testing and certification, solidifies their bargaining position.

- Safety is paramount: Boeing cannot afford to compromise on the quality of parts, directly impacting passenger safety.

- Proven track record: Suppliers with a consistent history of meeting stringent aerospace standards gain leverage.

- Specialized capabilities: Providers of unique or advanced manufacturing processes and materials hold stronger bargaining power.

- Regulatory compliance: Suppliers adept at navigating complex aerospace regulations are highly valued and thus possess more power.

Supplier Strength: The Grip on Aerospace Production

Boeing's suppliers, particularly those providing specialized components like engines and avionics, possess significant bargaining power. This is due to the high switching costs associated with rigorous industry regulations and lengthy qualification processes, which can take years to complete, as exemplified by the 2024 certification timelines for new aerospace suppliers.

Consolidation within the supplier base further concentrates power, leaving Boeing with fewer alternatives for critical parts. Many suppliers also hold crucial patents, protecting their proprietary technologies and limiting Boeing's negotiation leverage, a situation highlighted by Boeing's 2023 reliance on patent-protected advanced materials.

The paramount importance of quality and reliability in aerospace means suppliers with a proven track record and specialized capabilities are indispensable. This, coupled with their ability to navigate complex regulations, strengthens their position, making them less susceptible to price pressures, especially given ongoing supply chain challenges observed in 2024.

| Factor | Impact on Boeing | Example/Data Point |

|---|---|---|

| Supplier Specialization | High reliance on few suppliers for critical, advanced components. | Engines, avionics, advanced composite structures. |

| Switching Costs | Extensive and costly to qualify new suppliers due to stringent regulations. | 2024: Average new supplier certification can take years. |

| Industry Consolidation | Reduced number of dominant suppliers limits sourcing options. | 2023: Continued M&A activity further concentrates the supply base. |

| Intellectual Property | Patented technologies create dependency and reduce negotiation flexibility. | Spirit AeroSystems patents on advanced composite structures. |

| Quality & Reliability | Suppliers with proven performance are indispensable, strengthening their power. | 2024: Suppliers meeting exacting demands are less susceptible to price pressure. |

What is included in the product

This analysis dissects Boeing's competitive environment, examining the intensity of rivalry, the bargaining power of buyers and suppliers, the threat of new entrants, and the impact of substitute products.

Quickly identify critical competitive pressures—bargaining power of buyers and suppliers, threat of new entrants and substitutes, and industry rivalry—to inform strategic responses and mitigate risks.

Customers Bargaining Power

Consolidated Customer Base

Boeing's customer base is notably concentrated, with a significant portion of its commercial business coming from a limited number of major global airlines and aircraft leasing firms. This consolidation means that large buyers, by placing substantial, multi-aircraft orders, wield considerable bargaining power. For instance, major carriers like American Airlines or Emirates can leverage their order volume to negotiate better prices, tailored configurations, and enhanced after-sales service agreements. This concentrated demand directly translates into increased customer leverage.

High Purchase Value and Infrequent Buys

Airlines, as Boeing's customers, face immense capital expenditures when purchasing commercial aircraft. These significant investments, often amounting to hundreds of millions of dollars per aircraft, are not made lightly and are typically spaced out over many years, sometimes decades, as fleets are renewed. For instance, a single wide-body aircraft can cost upwards of $300 million, and an airline might order dozens.

This substantial financial commitment grants customers considerable bargaining power. Because the purchase decision has such a profound and long-lasting impact on an airline's operational costs and its overall competitive standing, customers undertake rigorous due diligence. They are highly motivated to negotiate the most favorable terms possible, including pricing, delivery schedules, and after-sales support, to maximize their return on this critical investment.

Long-Term Relationships and Fleet Commonality

Airlines often favor fleet commonality, sticking with a single manufacturer like Boeing or Airbus. This simplifies maintenance, pilot training, and spare parts logistics, ultimately lowering operational expenses. For example, a major airline might operate a predominantly Boeing fleet, making a switch to a competitor a costly endeavor due to retraining and infrastructure changes.

This preference for consistency, while creating customer loyalty, also significantly amplifies their bargaining power. When airlines are in the market for new aircraft, they can leverage their existing fleet commonality to negotiate more favorable pricing and terms. This is particularly true for large orders that solidify a manufacturer's market share with that customer for years to come.

Availability of Competing Products (Airbus)

The bargaining power of customers in the commercial aircraft market is significantly amplified by the near-duopoly structure, primarily between Boeing and Airbus. This intense rivalry allows major airlines, the key customers, to leverage competitive offers, directly impacting pricing and terms. For instance, airlines can effectively pit Boeing against Airbus, threatening to shift substantial order volumes if their demands for price concessions or favorable delivery schedules are not met.

This dynamic is particularly potent given the high value of each aircraft order. A single airline order can represent billions of dollars in revenue. In 2023, for example, major carriers like United Airlines placed significant orders, with United ordering 200 737 MAX jets and 50 787 Dreamliners from Boeing, alongside 60 A321neo aircraft from Airbus, demonstrating the strategic maneuvering possible.

- Duopoly Dominance: The market is largely controlled by Boeing and Airbus, giving customers significant leverage.

- Order Shifting Threat: Airlines can threaten to move large orders between manufacturers to secure better deals.

- High Order Value: The substantial financial commitment of each aircraft purchase empowers customer negotiation.

- Competitive Pricing: The direct competition forces both manufacturers to offer competitive pricing and terms to win business.

Customization and After-Sales Support Needs

Airlines often need highly customized aircraft configurations, and this need gives them significant bargaining power. Boeing's ability to meet these specific demands, from cabin layouts to specialized avionics, becomes a key negotiation point. Furthermore, the continuous requirement for after-sales support, including maintenance, repair, and pilot training, creates a long-term dependency that customers can leverage.

These ongoing service needs allow airlines to negotiate more favorable terms on support contracts. For example, airlines might secure lower rates for spare parts or preferential scheduling for maintenance, directly impacting their operational costs. Boeing's responsiveness to these service demands is crucial for airline profitability, reinforcing the customers' leverage in securing better deals.

- Customization Demands: Airlines frequently require bespoke aircraft modifications, increasing their influence.

- After-Sales Support: The necessity for ongoing maintenance, repair, and training creates a crucial leverage point for customers.

- Service Contract Negotiations: Customers use their ongoing needs to negotiate favorable terms and ensure responsive service.

- Operational Efficiency: Airlines' reliance on timely support for their own profitability strengthens their bargaining position.

Customer Power: Shaping Boeing's Deals and Terms

The bargaining power of Boeing's customers is substantial due to the market's oligopolistic nature, primarily dominated by Boeing and Airbus. This intense competition allows major airlines to negotiate aggressively on price, delivery schedules, and customization options. For instance, in 2023, United Airlines' significant orders for both Boeing and Airbus aircraft highlighted the leverage airlines possess in securing favorable terms by playing manufacturers against each other.

| Customer Type | Key Bargaining Tactics | Impact on Boeing |

|---|---|---|

| Major Global Airlines | Large order volumes, fleet commonality preference, threat to switch suppliers | Price concessions, favorable delivery slots, customized configurations |

| Aircraft Leasing Firms | Bulk orders, demand for standardization, financial flexibility | Negotiation on pricing, extended payment terms, fleet mix optimization |

What You See Is What You Get

Boeing Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces analysis for Boeing, detailing the competitive landscape of the aerospace industry. The document you see here is precisely the same professionally written and formatted analysis you will receive immediately after purchase, offering actionable insights into Boeing's strategic positioning. You're looking at the actual document; once your purchase is complete, you'll gain instant access to this exact file. This means no mockups, no samples, just the full, ready-to-use analysis for your business needs.

Rivalry Among Competitors

Global Duopoly with Airbus

The commercial aerospace sector is essentially a global duopoly, with Boeing and Airbus locked in a constant battle for dominance. This intense rivalry means that for every significant aircraft contract, these two giants are directly competing, pushing each other to innovate and offer competitive pricing.

This head-to-head competition forces both companies to focus heavily on operational efficiency and technological advancements to secure market share. For instance, in 2023, the order backlog for Boeing stood at over 5,600 aircraft, while Airbus reported a backlog of approximately 8,000 aircraft, highlighting the scale of their ongoing competition for new business.

High Fixed Costs and Exit Barriers

Boeing operates within an industry where massive upfront investments in research, development, and manufacturing facilities are the norm. These high fixed costs, estimated in the billions for new aircraft programs, create a significant financial hurdle for any potential new entrants. For instance, the development of the 787 Dreamliner reportedly cost Boeing tens of billions of dollars before its first delivery. This intense capital requirement inherently limits the number of players capable of competing at this scale.

The aerospace sector also presents substantial exit barriers, largely due to these same high fixed costs and specialized assets. Once invested, these resources are difficult to redeploy or sell off, effectively trapping companies like Boeing in the market. Consequently, even when facing challenging economic conditions or reduced demand, as seen during the COVID-19 pandemic which saw a sharp drop in air travel, companies are compelled to maintain operations to avoid catastrophic losses on their sunk investments, thereby fueling persistent competitive rivalry among the established few.

Product Differentiation through Technology and Efficiency

Competitive rivalry in the commercial aircraft sector is intense, driven by technological innovation. Boeing and Airbus, the primary players, vie for market share by focusing on cutting-edge advancements in fuel efficiency, flight range, passenger capacity, and overall operational reliability. These features are critical differentiators that attract airline customers and secure lucrative orders.

Both giants continuously pour billions into research and development to maintain their technological edge. For instance, Boeing's 737 MAX program and Airbus's A320neo family represent significant R&D investments aimed at improving fuel burn by up to 20% compared to previous generations. This technological race is paramount for gaining a competitive advantage.

In 2024, the market continues to see airlines prioritizing aircraft that offer lower operating costs through enhanced fuel efficiency and reduced maintenance. Boeing's focus on advanced aerodynamics and engine technology for its upcoming aircraft, like the 777X, directly addresses these airline demands, showcasing the pivotal role of technology in this rivalry.

Cyclical Demand and Order Backlogs

The commercial aerospace sector is inherently cyclical, heavily swayed by the health of the global economy and the financial performance of airlines. This cyclicality means that demand for new aircraft fluctuates, impacting production schedules and the need for new orders. For instance, during economic downturns, airlines may defer or cancel orders, putting pressure on manufacturers like Boeing.

Despite significant order backlogs offering some insulation, competition remains fierce. Boeing and its primary rival, Airbus, are constantly vying for new orders, especially during periods of market expansion. This intense rivalry often translates into aggressive sales strategies, including attractive financing packages and price concessions, to secure market share and maintain consistent production rates.

- Market Volatility: Boeing's commercial aviation business is directly tied to global economic cycles, impacting airline capital expenditure.

- Order Backlog Dynamics: As of late 2024, Boeing's order backlog remained substantial, providing a degree of revenue visibility, but the competition to fill future production slots is ongoing.

- Competitive Tactics: Rivalry intensifies during growth phases, leading to price competition and preferential financing to win contracts.

- Production Stability: Maintaining stable production levels is crucial, especially when navigating periods of lower demand, which fuels the competitive drive for new orders.

Government Contracts and Defense Market

Boeing's competitive rivalry extends significantly into the defense, space, and security sectors, where it contends with major global defense contractors. This arena is characterized by intense competition for government contracts, often involving protracted and intricate bidding procedures. Geopolitical factors and extended development timelines further complicate this landscape, demanding strategic agility and robust capabilities from participants.

The competition for lucrative government contracts is a central theme. For instance, in 2024, the U.S. Department of Defense continued to award substantial contracts, with major players like Lockheed Martin, Northrop Grumman, and Raytheon Technologies vying alongside Boeing. These contracts often span decades and require substantial investment in research, development, and manufacturing, making them highly sought after.

- Intense Bidding: Major defense firms engage in fierce competition for government contracts, often requiring extensive proposals and cost analyses.

- Long Development Cycles: Projects in this sector, such as fighter jets or satellite systems, can take over a decade from conception to deployment.

- Geopolitical Influence: International relations and national security priorities heavily shape contract awards and market dynamics.

- Key Competitors: Boeing faces direct rivalry from companies like Lockheed Martin, Northrop Grumman, and BAE Systems in various defense segments.

Commercial Aerospace: A High-Stakes Global Duopoly

The competitive rivalry in commercial aerospace is a high-stakes, global duopoly primarily between Boeing and Airbus. This intense competition drives continuous innovation in aircraft technology, focusing on fuel efficiency and passenger comfort to capture airline orders. For example, in 2024, airlines are keenly evaluating aircraft like Boeing's 777X and Airbus's A350 family, which represent significant advancements in these areas.

The market's cyclical nature and the massive capital required for new aircraft development create high barriers to entry, concentrating competition among a few established players. This dynamic means that even with substantial order backlogs, as seen with both Boeing and Airbus exceeding 5,000 and 8,000 aircraft respectively in late 2024, the drive to secure future production slots remains a key competitive battleground.

| Metric | Boeing (Approx. Late 2024) | Airbus (Approx. Late 2024) | Significance |

|---|---|---|---|

| Order Backlog | > 5,600 Aircraft | ~ 8,000 Aircraft | Indicates future production demand and market share competition. |

| R&D Investment (Annual Estimate) | Billions USD | Billions USD | Crucial for technological differentiation and fuel efficiency gains. |

| New Aircraft Program Cost | Tens of Billions USD | Tens of Billions USD | High barrier to entry for new competitors. |

SSubstitutes Threaten

Limited Direct Substitutes for Long-Haul Air Travel

For long-haul international travel and time-sensitive cargo, commercial aircraft remain virtually unmatched in terms of speed and efficiency. The absence of practical direct substitutes significantly reduces the threat of substitution for Boeing's core commercial jetliner business, underpinning sustained demand for air transport. For instance, in 2024, air cargo continued to be a vital component of global trade, with the International Air Transport Association (IATA) reporting a robust demand for air freight services.

High-Speed Rail for Short to Medium Distances

In regions with extensive and efficient rail networks, high-speed rail presents a viable substitute for short to medium-haul domestic flights. This is particularly true for business travelers who prioritize speed and convenience between city pairs. For instance, in Europe, routes like Paris to Brussels or Frankfurt to Munich see significant passenger traffic via high-speed rail, directly competing with airlines on these segments.

This substitution threat can impact Boeing's smaller commercial aircraft, such as the 737 family, by diverting a portion of the passenger market, especially for routes under 500 miles. While air travel remains dominant for longer distances, the increasing investment and development of high-speed rail infrastructure in key markets like China and parts of the US could exacerbate this competitive pressure. For example, China's high-speed rail network, which exceeded 45,000 kilometers by the end of 2023, offers a compelling alternative to domestic flights for many travelers.

Virtual Communication Technologies

Virtual communication technologies, significantly boosted by the pandemic, present a threat by reducing the necessity for certain business travel. While not a direct replacement for aircraft, this shift can dampen demand for business class seats on specific routes. This impacts airline revenue streams and potentially their fleet expansion plans. For example, a 2024 survey indicated that 60% of companies plan to continue with hybrid work models, suggesting a sustained reduction in travel compared to pre-pandemic levels.

Alternative Transportation for Cargo

For non-time-sensitive cargo, sea shipping and overland freight transportation, including trucks and trains, present more cost-effective alternatives to air cargo. These modes are particularly attractive when delivery speed is not the primary concern. For instance, in 2024, the global maritime shipping industry continued to handle the vast majority of international trade volume, demonstrating its cost-efficiency for bulk goods and non-perishable items. This significant market share highlights the substantial threat posed by sea freight to air cargo, especially for shipments where cost savings outweigh rapid transit times.

While air freight remains indispensable for high-value, time-critical, or perishable goods, the broader logistics landscape offers viable substitutes that can cap the growth potential of specific air cargo segments. The cost differential can be substantial; for example, shipping by sea can be as much as 10 times cheaper per kilogram than by air. This economic reality forces airlines and cargo operators to compete not just with other air carriers but with entirely different modes of transport.

- Sea Freight Dominance: Maritime shipping accounts for approximately 80% of global trade volume, underscoring its cost-effectiveness as a substitute for air cargo for many goods.

- Overland Efficiency: Rail and truck transport provide competitive alternatives for regional and domestic shipments, offering flexibility and lower costs than air freight for non-urgent deliveries.

- Cost Sensitivity: The significant cost savings offered by sea and overland transport limit the ability of air cargo to capture a larger share of the general freight market, particularly for price-sensitive customers.

Military and Defense Alternatives

While direct substitutes for Boeing's advanced military aircraft are scarce, the threat of substitutes in the defense sector arises from alternative strategic choices governments might make. Instead of procuring new fighter jets or bombers, nations could invest more heavily in unmanned aerial vehicles (UAVs) or advanced drone swarms, which can perform similar reconnaissance and strike missions at a lower cost and with reduced risk to personnel. For instance, the U.S. Department of Defense's fiscal year 2024 budget request included significant funding for autonomous systems and artificial intelligence, signaling a growing emphasis on these alternatives. This strategic pivot away from traditional manned platforms can indirectly substitute for demand for Boeing's legacy aircraft programs.

Furthermore, the expansion of sophisticated ground-based missile systems and enhanced naval capabilities presents another layer of substitution. Countries might prioritize long-range precision strike capabilities delivered via missiles or focus on bolstering their naval fleets, which can project power and conduct operations in ways that previously required air superiority. By 2024, global military spending reached an estimated $2.44 trillion, with a notable portion allocated to modernizing non-air-centric defense assets. This reallocation of defense budgets can diminish the market share for manned military aircraft, impacting Boeing's order books.

- The rise of drone technology: Governments are increasingly investing in autonomous systems for reconnaissance and combat, potentially reducing the need for manned aircraft.

- Ground-based and naval alternatives: Enhanced missile systems and naval power projection offer strategic options that can substitute for air power in certain scenarios.

- Shifting defense budgets: Global military spending trends indicate a potential reallocation of funds away from traditional aircraft towards alternative defense strategies.

- Strategic defense posture: Nations may opt for different defense strategies that de-emphasize manned aviation, indirectly impacting demand for Boeing's products.

Boeing's Market Faces Diverse Substitutes: Rail, Virtual, and Autonomous Tech

The threat of substitutes for Boeing is moderate, primarily driven by alternatives in commercial aviation and defense. For commercial air travel, high-speed rail competes on shorter routes, while virtual communication reduces business travel needs. In cargo, sea and overland freight offer more cost-effective, albeit slower, alternatives.

In the defense sector, the rising capabilities of unmanned aerial vehicles (UAVs) and advanced missile systems present a growing substitute threat to traditional manned aircraft. Nations are increasingly prioritizing these technologies, which can offer similar mission profiles at a lower cost and with reduced risk. This strategic shift could impact demand for Boeing's fighter jets and bombers.

For example, by 2024, global military spending trends indicated a growing allocation towards autonomous systems and AI, signaling a potential move away from legacy manned platforms. This strategic reallocation of defense budgets directly influences the market for new military aircraft, a core segment for Boeing.

| Mode of Transport | Primary Substitute for | Key Substitute Characteristics | Relative Cost Advantage (vs. Air) | Example Data (2024) |

|---|---|---|---|---|

| High-Speed Rail | Short/Medium Haul Flights | Speed, Convenience | Potentially Lower for specific city pairs | Significant passenger traffic on key European routes |

| Virtual Communication | Business Air Travel | Cost Savings, Reduced Need for Travel | Significant | 60% of companies planning hybrid work models |

| Sea Freight | Air Cargo (Non-time Sensitive) | Cost-Effectiveness, Bulk Capacity | Up to 10x cheaper per kg | Handles ~80% of global trade volume |

| Overland Freight (Rail/Truck) | Air Cargo (Regional/Domestic) | Flexibility, Lower Cost | Lower | Competes for domestic and regional shipments |

| UAVs/Drone Swarms | Manned Military Aircraft | Lower Cost, Reduced Risk, Autonomy | Lower | Increased defense budget allocation for autonomous systems |

| Missile Systems/Naval Power | Air Power Projection | Long-Range Strike, Alternative Power Projection | Varies | Global military spending reached $2.44 trillion |

Entrants Threaten

Prohibitive Capital Requirements

The aerospace industry presents an incredibly high barrier to entry due to its staggering capital requirements. Developing a new aircraft program alone can necessitate tens of billions of dollars for research, design, advanced manufacturing facilities, and specialized tooling. For instance, Boeing's investment in the 787 Dreamliner program was estimated to be in the tens of billions.

This immense financial hurdle effectively dissuades all but the most established and financially robust companies. The sheer scale of investment needed makes it nearly impossible for new, smaller players to compete, significantly limiting the threat of new entrants to the market.

Stringent Regulatory and Certification Hurdles

The threat of new entrants for Boeing is significantly dampened by stringent regulatory and certification hurdles. Aspiring aircraft manufacturers must navigate an incredibly complex and lengthy approval process, encompassing rigorous safety testing and certification by global aviation authorities such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA).

This arduous journey can span many years, demanding proven technical expertise and substantial capital investment, thereby delaying market entry and escalating costs and risks for any potential challenger. For instance, the certification process for a new commercial aircraft model can easily cost billions of dollars and take a decade or more from initial design to final approval, presenting a formidable barrier.

Established Brand Loyalty and Trust

Established brand loyalty and trust present a significant barrier to new entrants in the commercial aircraft manufacturing industry. Boeing and Airbus have cultivated deep, long-standing relationships with airlines and governments over decades. This loyalty is built on a foundation of proven reliability, exceptional safety records, and comprehensive global support infrastructures, making it incredibly difficult for newcomers to earn the necessary confidence for substantial orders from risk-averse customers.

Complex and Integrated Supply Chains

The aerospace industry's reliance on a deeply complex and globally integrated supply chain acts as a significant barrier to new entrants. This intricate network involves thousands of highly specialized suppliers, each critical for delivering specific, high-quality components on time. Establishing and managing such a sophisticated system requires immense capital, expertise, and time, making it exceptionally difficult for newcomers to replicate.

For instance, Boeing's supply chain involves over 12,500 suppliers globally, a testament to its scale and complexity. Building a comparable network that meets stringent aerospace quality and regulatory standards would be a monumental undertaking for any new competitor. The sheer logistical challenge of coordinating production and ensuring the seamless flow of thousands of unique parts, from raw materials to finished sub-assemblies, deters potential market entrants.

- Global Reach: Boeing's supply chain spans numerous countries, necessitating expertise in international logistics and regulations.

- Specialization: Suppliers are often highly specialized, producing unique components that require advanced manufacturing capabilities.

- Quality Control: The aerospace industry demands exceptionally high standards for every component, adding layers of complexity to supplier management and integration.

- Lead Times: Long lead times for specialized materials and manufacturing processes further complicate the establishment of a new supply chain.

Intellectual Property and Proprietary Technology

Existing players like Boeing have an immense library of patents, trade secrets, and unique manufacturing methods honed over more than a century in aviation. This deep well of intellectual property acts as a substantial hurdle. New competitors would need to invest heavily in creating their own groundbreaking technologies or secure licenses for existing ones, significantly extending timelines and increasing initial expenses.

For instance, Boeing's ongoing investment in research and development, which reached approximately $3.5 billion in 2023, directly contributes to this barrier. This R&D fuels the creation of new patents and proprietary processes, making it increasingly challenging for newcomers to match the technological sophistication and efficiency of established manufacturers.

- Patented Technologies: Boeing holds thousands of patents covering everything from advanced aerodynamics to novel materials and propulsion systems.

- Trade Secrets: Critical manufacturing techniques and design elements are often protected as trade secrets, offering competitive advantages without public disclosure.

- Proprietary Software: Advanced design, simulation, and production software developed in-house further differentiates established players.

- Licensing Costs: Acquiring rights to use even a fraction of this protected technology would represent a substantial upfront investment for any new entrant.

Aerospace Entry: A Minimal Threat to Incumbents

The threat of new entrants for Boeing is minimal, largely due to the astronomical capital required to enter the commercial aircraft manufacturing sector. Developing a single new aircraft model can cost tens of billions of dollars, a figure that few entities can realistically finance. This immense financial barrier, coupled with the need for extensive R&D and manufacturing infrastructure, effectively deters most potential competitors.

Regulatory and certification hurdles further solidify this low threat. Navigating the complex, multi-year approval processes mandated by aviation authorities like the FAA and EASA demands significant expertise and financial resources, adding years and billions to a new entrant's timeline and cost structure. Established brand loyalty, built over decades, also makes it difficult for newcomers to gain the trust of risk-averse airlines.

Boeing's sophisticated global supply chain, involving over 12,500 specialized suppliers, represents another formidable barrier. Replicating this intricate network, which adheres to stringent aerospace quality and regulatory standards, is a monumental task for any new player. Furthermore, Boeing's extensive portfolio of patents, trade secrets, and proprietary manufacturing processes, bolstered by annual R&D investments of billions, creates a significant technological moat.

| Barrier Type | Description | Impact on New Entrants |

|---|---|---|

| Capital Requirements | Developing a new aircraft program can cost tens of billions of dollars. | Extremely High - Deters most potential competitors. |

| Regulatory Hurdles | Complex, multi-year certification processes by aviation authorities (FAA, EASA). | Very High - Increases cost, time, and risk significantly. |

| Supply Chain Complexity | Managing a global network of thousands of specialized, high-quality suppliers. | Very High - Requires immense capital, expertise, and time to replicate. |

| Intellectual Property | Extensive patents, trade secrets, and proprietary manufacturing methods. | High - Requires significant R&D investment or costly licensing for newcomers. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Boeing is built upon a robust foundation of publicly available data, including Boeing's annual reports and SEC filings, alongside industry-specific reports from aviation consultancies and market research firms.

We also incorporate insights from financial news outlets, macroeconomic indicators, and government aviation authority publications to provide a comprehensive understanding of the competitive landscape.