Baran Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Baran Group

A Must-Have Tool for Decision-Makers

Baran Group operates within an industry shaped by moderate buyer power and a significant threat of substitutes, impacting pricing and customer loyalty. Understanding these forces is crucial for navigating the competitive landscape effectively. The full Porter's Five Forces Analysis provides a comprehensive, data-driven framework to dissect these dynamics, revealing actionable insights for strategic advantage.

Suppliers Bargaining Power

Specialized Expertise and Scarcity

Suppliers offering highly specialized engineering software, advanced construction materials, or niche consulting services can wield considerable bargaining power. This is especially true when alternatives are scarce, as is often the case with proprietary technologies or unique skill sets critical for complex infrastructure, energy, or telecommunication projects.

Switching Costs for Baran Group

High switching costs significantly strengthen the bargaining power of Baran Group's suppliers. If adopting a new supplier necessitates substantial investment in re-training staff, re-engineering operational workflows, or implementing entirely new IT infrastructure, Baran Group faces a considerable hurdle in changing vendors. This leverage is particularly pronounced when suppliers provide specialized components or operate under long-term, exclusive contracts, as seen in the automotive sector where custom-fitted parts can lock in suppliers for years.

Supplier Concentration

Supplier concentration significantly amplifies bargaining power. When Baran Group relies on a limited number of suppliers for essential components in its diverse projects, such as specialized turbines for energy or advanced filtration systems for water treatment, these suppliers gain leverage. This concentration allows them to potentially dictate pricing, delivery schedules, and contract terms, impacting Baran Group's operational costs and project timelines.

Threat of Forward Integration by Suppliers

The threat of forward integration by suppliers significantly bolsters their bargaining power against Baran Group. If suppliers can leverage their expertise to offer similar engineering and project management services, they effectively become potential competitors.

This capability forces Baran Group into a precarious position, potentially requiring concessions on pricing or terms to avert direct competition from its own supply chain. For instance, a major engineering component supplier with deep project execution knowledge could, in theory, bid on projects directly, bypassing Baran Group’s services.

Such a move would directly challenge Baran Group’s market share and profitability. The potential for this shift is underscored by the increasing commoditization of certain engineering services, making it easier for established suppliers to expand their offerings. For example, in 2024, the global engineering services market was valued at over $1.5 trillion, with a notable portion driven by project management and execution, areas where suppliers could potentially integrate.

- Enhanced Supplier Leverage: Suppliers capable of offering engineering and project management services gain considerable leverage over Baran Group.

- Competitive Threat: The potential for suppliers to become direct competitors creates a significant risk for Baran Group’s business model.

- Concessionary Pressure: Baran Group may be compelled to meet supplier demands to prevent them from entering the market as direct rivals.

- Market Dynamics: The growing trend of service modularization in the engineering sector facilitates supplier forward integration.

Importance of Supplier's Input to Baran Group's Projects

The significance of a supplier's contribution directly correlates with their leverage over Baran Group. When Baran Group's projects heavily rely on specific inputs for their success or quality, suppliers gain considerable sway. For example, in 2024, suppliers of specialized components for advanced renewable energy systems, critical for meeting sustainability targets, demonstrated this. Similarly, providers of unique materials for large-scale water infrastructure projects, where quality and timely delivery are paramount, wield significant influence.

This dependence means that any disruption or price increase from these key suppliers can have a substantial impact on Baran Group's project timelines and profitability. For instance, a 10% increase in the cost of a critical component for a solar farm project could significantly alter the project's overall budget and return on investment.

- Criticality of Input: Suppliers of core technologies for renewable energy solutions, such as advanced photovoltaic cells or efficient turbine components, hold high bargaining power.

- Essential Components: Providers of specialized materials or unique components for large-scale water infrastructure, like advanced filtration membranes or specialized concrete additives, also possess significant influence.

- Project Success Dependence: Baran Group's reliance on these inputs for project completion and quality directly amplifies supplier bargaining power.

- Impact of Price Fluctuations: In 2024, fluctuations in the global supply chain for rare earth minerals, essential for many renewable energy technologies, highlighted how supplier input costs can directly affect project viability.

Supplier Power: Impacting Your Projects & Costs

Suppliers of highly specialized engineering software, advanced construction materials, or niche consulting services can wield considerable bargaining power, especially when alternatives are scarce. This is particularly true for proprietary technologies or unique skill sets crucial for complex projects.

High switching costs, such as retraining staff or re-engineering workflows, significantly strengthen supplier leverage. This is amplified when suppliers provide specialized components or operate under long-term, exclusive contracts, as seen in the automotive sector with custom-fitted parts.

Supplier concentration, where Baran Group relies on few vendors for essential components like specialized turbines or filtration systems, allows suppliers to dictate terms. This directly impacts Baran Group's costs and project timelines.

The potential for suppliers to integrate forward and offer similar engineering and project management services makes them potential competitors. This forces Baran Group to potentially concede on pricing or terms to avoid direct competition from its own supply chain, a trend seen in the over $1.5 trillion global engineering services market in 2024.

| Factor | Impact on Baran Group | Example (2024 Data) |

|---|---|---|

| Specialization & Scarcity | High bargaining power for suppliers | Niche consulting services for complex infrastructure projects |

| Switching Costs | Increased supplier leverage | Implementing new IT infrastructure for a new material supplier |

| Supplier Concentration | Suppliers dictate terms | Reliance on a few turbine manufacturers for energy projects |

| Forward Integration Threat | Potential for direct competition | Engineering component suppliers offering project management services |

What is included in the product

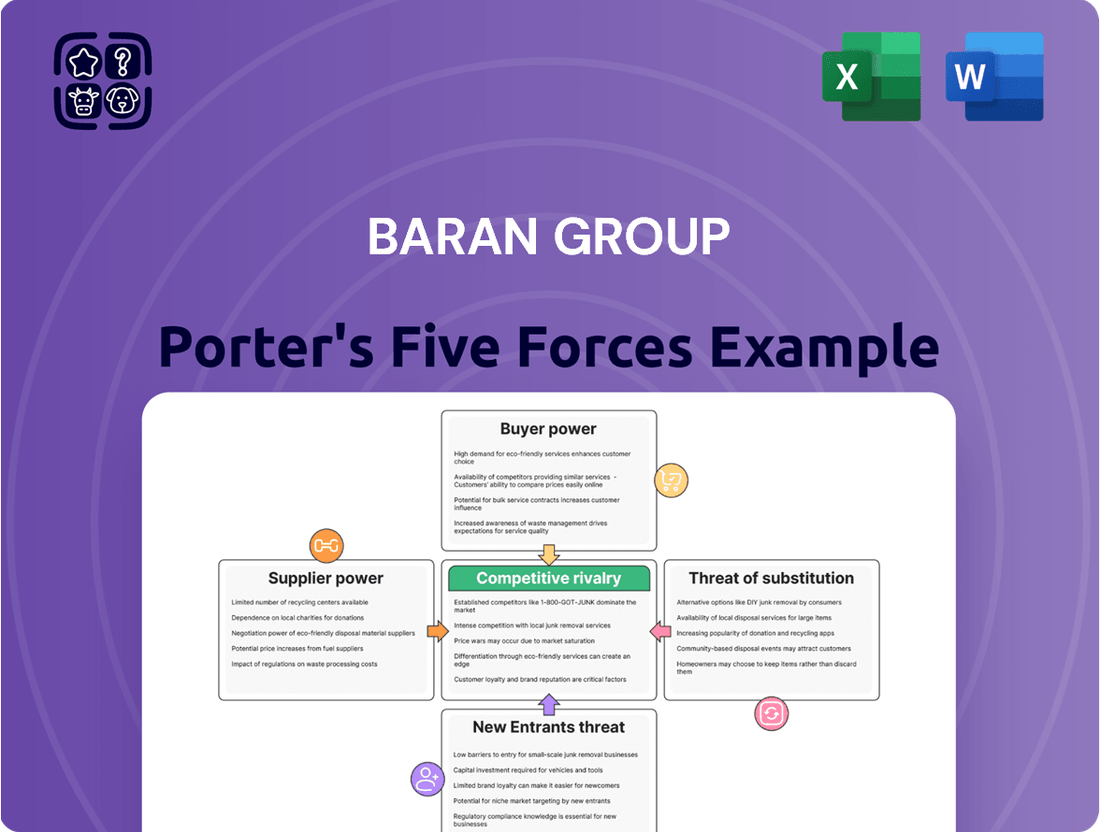

This Porter's Five Forces analysis for Baran Group reveals the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes on the company's industry.

Easily visualize competitive intensity across all five forces with intuitive charts, simplifying complex market dynamics for strategic clarity.

Customers Bargaining Power

Large-Scale and Public Sector Clients

Baran Group's engagement with large-scale and public sector clients, such as government agencies and major corporations, significantly influences their bargaining power. These clients often represent substantial project volumes, giving them considerable leverage. For instance, in 2024, many public infrastructure projects, a key area for engineering firms like Baran Group, were subject to rigorous competitive bidding processes, with governments prioritizing cost-effectiveness and value for money.

The ability of these large clients to solicit bids from numerous engineering firms intensifies their bargaining power. This competitive environment allows them to negotiate more favorable terms, including pricing and project timelines. In 2024, the global engineering and construction market saw increased competition, further empowering large clients to secure advantageous contracts.

Availability of Alternative Engineering Firms

Customers wield significant bargaining power when a multitude of engineering and project management firms can offer comparable comprehensive solutions. This abundance of choice directly impacts how providers like Baran Group must approach client relationships and pricing.

The global engineering and construction market, valued at approximately $1.7 trillion in 2023, is characterized by its competitiveness. This competitive landscape means clients frequently have numerous alternative firms to consider, allowing them to negotiate for better terms and potentially lower prices.

Price Sensitivity of Clients

Baran Group's clients, particularly public sector organizations facing strict budgetary limitations and private sector clients prioritizing cost efficiency, demonstrate significant price sensitivity. This characteristic directly translates into their ability to negotiate for lower prices or more competitive service packages from Baran Group.

For instance, in 2024, many government tenders for infrastructure projects, a key area for Baran Group, saw an average of 7 bids per tender, indicating a highly competitive landscape where price is a major deciding factor for award. This intense competition empowers clients to demand more value for their money, directly impacting Baran Group's pricing strategies and profit margins.

Client's Ability to Self-Perform

Clients possessing the capacity to perform certain services internally significantly enhances their bargaining power. For instance, if a major client can manage basic engineering or project oversight with their own staff, they become less reliant on external providers like Baran Group. This reduces the perceived value of Baran Group's services in those specific areas, giving the client leverage during negotiations.

In 2024, many large corporations continued to invest in developing in-house expertise for core functions. This trend is driven by a desire for greater control, cost savings, and the potential to build proprietary knowledge. For example, a significant percentage of Fortune 500 companies reported expanding their internal engineering departments over the past year to handle more complex project phases, directly impacting their reliance on outsourced engineering firms.

- Increased In-House Capabilities: Clients are building internal teams for tasks previously outsourced.

- Reduced Dependence: This self-sufficiency weakens the negotiating position of external service providers.

- Cost Efficiency Drive: Companies aim to cut costs by bringing services in-house, impacting pricing power of suppliers.

- Strategic Control: Clients gain more control over project execution and quality by performing tasks internally.

Project Specificity and Client Knowledge

When projects are highly standardized, clients can readily compare bids and negotiate terms, amplifying their bargaining power. This is particularly true in sectors where construction processes are well-defined and readily replicable.

Conversely, if Baran Group possesses unique expertise or undertakes highly specialized, innovative projects, the bargaining power of clients tends to diminish. Clients may be less able to find alternative providers with comparable capabilities, leading to more favorable terms for Baran Group.

- Standardization: In 2024, the construction industry saw a continued emphasis on modular construction and prefabrication, increasing the potential for project standardization.

- Client Knowledge: Clients with significant in-house technical expertise, such as large infrastructure developers or government agencies, often possess greater leverage in negotiations.

- Specialization: Baran Group's focus on complex, niche projects, such as advanced data centers or specialized industrial facilities, can reduce client options and thus their bargaining power.

- Innovation: Projects involving novel materials or construction techniques, where Baran Group leads in R&D, can further tilt the balance of power away from clients.

Client Power: Navigating Competition in Engineering & Construction

Baran Group faces significant customer bargaining power due to the high number of competitors and the clients' ability to switch providers. This is amplified when clients can perform services in-house or when projects are standardized, allowing for easier price comparisons. In 2024, the competitive landscape in engineering and construction, a market valued at over $1.7 trillion globally, empowered clients to negotiate for better terms, especially public sector clients focused on cost-effectiveness.

| Factor | Impact on Bargaining Power | 2024 Relevance |

|---|---|---|

| Number of Competitors | High competition increases client power. | Global engineering market saw increased competition in 2024. |

| Client In-House Capabilities | Stronger internal teams reduce reliance on external firms. | Fortune 500 companies expanded internal engineering departments in 2024. |

| Project Standardization | Easier comparison of bids and negotiation. | Emphasis on modular construction in 2024 increased standardization potential. |

| Price Sensitivity | Clients can demand lower prices or better packages. | Government tenders in 2024 averaged 7 bids, highlighting price as a key factor. |

Same Document Delivered

Baran Group Porter's Five Forces Analysis

This preview showcases the complete Baran Group Porter's Five Forces Analysis, offering a thorough examination of competitive forces within the industry. The document you see here is the exact, professionally formatted report you will receive immediately after purchase. It details the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry among existing competitors. You're looking at the actual document; once you complete your purchase, you’ll get instant access to this exact file, ready for your strategic planning.

Rivalry Among Competitors

Number and Diversity of Competitors

The engineering and project management sector is quite fragmented, meaning there are many companies vying for business. These range from massive global players with extensive resources to smaller, niche firms that focus on specific areas or regions. This wide spectrum of competitors means Baran Group encounters a diverse set of rivals across different geographies and specialized markets, which naturally heightens the competitive intensity.

Industry Growth Rate

The industry growth rate significantly influences competitive rivalry. In mature markets, where growth is sluggish, companies often intensify their efforts to capture existing market share, leading to heightened competition. For instance, in 2024, the global construction industry, a sector Baran Group operates within, experienced a moderate growth rate of around 3.5%, which, while positive, necessitates a strong focus on competitive differentiation to secure projects.

High Fixed Costs and Excess Capacity

The engineering and construction sector, including companies like Baran Group, is characterized by substantial fixed costs. These include significant investments in heavy machinery, advanced software, and retaining a highly skilled workforce, all of which contribute to a high cost of doing business. For instance, major construction projects often require specialized, expensive equipment that sits idle if not actively utilized.

When the industry experiences periods of excess capacity, meaning there are more companies bidding on projects than there are projects available, the competitive pressure intensifies. This situation can lead to a price war, where firms lower their bids to win contracts, even if it means accepting slimmer profit margins. This dynamic directly fuels competitive rivalry as companies fight for market share.

In 2024, the global construction market faced ongoing challenges with capacity utilization in certain segments, particularly as supply chain disruptions and labor shortages persisted. This environment makes it difficult for companies to fully leverage their fixed asset base, thereby increasing the pressure to secure new projects and potentially leading to aggressive pricing strategies among competitors.

Differentiation of Services

Baran Group's ability to differentiate its comprehensive service offerings is a key factor in managing competitive rivalry. By focusing on specialized expertise in intricate projects, the adoption of cutting-edge technologies, or the cultivation of a robust global presence, Baran Group can effectively sidestep direct price-based competition. These unique value propositions serve to lessen the intensity of rivalry.

For instance, in 2024, companies that successfully showcased specialized skills in areas like sustainable infrastructure development or advanced digital transformation projects often commanded premium pricing and faced less direct competition. Baran Group's investment in its talent pool and technology infrastructure directly contributes to its differentiation capabilities.

- Specialized Expertise: Baran Group can highlight its track record in delivering complex engineering and construction projects, such as large-scale energy infrastructure or advanced transportation systems.

- Innovative Technologies: The adoption and integration of proprietary or advanced technologies, like AI-driven project management tools or novel construction materials, can set Baran Group apart.

- Global Presence: A strong international footprint, with established operations and local market understanding in key regions, offers a significant advantage over competitors with limited reach.

- Integrated Solutions: Offering a seamless blend of design, engineering, procurement, construction, and maintenance services under one umbrella reduces the need for clients to engage multiple providers.

Exit Barriers

High exit barriers significantly influence competitive rivalry by keeping firms invested in a market even when returns diminish. For Baran Group, this means competitors might persist in the engineering sector due to substantial, specialized assets and long-term commitments, intensifying the fight for market share.

In capital-intensive industries like engineering, the cost and difficulty of divesting specialized equipment or exiting contractual obligations can be immense. This forces companies to continue operating, even at lower profit margins, contributing to a more aggressive competitive landscape.

Consider the heavy machinery and project-specific infrastructure common in engineering. Divesting these assets often involves significant write-downs or finding buyers for highly specialized equipment, making a clean exit challenging. For instance, in 2024, many construction and engineering firms faced pressures to maintain operations despite economic headwinds, partly due to the sunk costs in their physical assets.

- Specialized Assets: Engineering firms often possess unique, difficult-to-repurpose machinery, increasing the cost of exiting.

- Long-Term Contracts: Existing project commitments bind companies to the market, limiting flexibility.

- Financial Investments: Significant capital expenditure in infrastructure and R&D creates a high financial hurdle for withdrawal.

- Industry Norms: A culture of long-term commitment in engineering can discourage early exits, perpetuating rivalry.

Navigating Intense Engineering & Project Management Rivalry

The engineering and project management sector is highly competitive, with numerous firms of varying sizes vying for projects. This fragmentation, coupled with moderate industry growth in 2024 around 3.5% for global construction, intensifies rivalry. High fixed costs associated with specialized equipment and skilled labor, alongside periods of excess capacity, further pressure companies to compete aggressively on price, impacting profit margins.

| Factor | Impact on Rivalry | Baran Group's Response/Mitigation |

|---|---|---|

| Industry Fragmentation | High intensity due to numerous competitors | Focus on specialized expertise and global presence |

| Industry Growth Rate (2024: ~3.5% global construction) | Moderate growth necessitates strong differentiation | Highlighting innovative technologies and integrated solutions |

| High Fixed Costs | Pressure to utilize assets leads to aggressive bidding | Leveraging specialized assets for complex projects |

| Excess Capacity/Sunk Costs | Drives price competition and lower margins | Securing projects through value-added services |

SSubstitutes Threaten

Alternative Project Delivery Methods

Clients may choose to handle certain project elements internally, bypassing the need for external project management or engineering services. For instance, a client might leverage their own skilled workforce for specific construction phases, reducing reliance on a general contractor like Baran Group. This trend was observed in the 2024 construction market, where some large industrial clients brought more in-house capabilities to manage costs and timelines more directly.

Modular and pre-fabricated construction methods offer another significant substitute. These approaches can streamline project delivery, often requiring less on-site engineering and project management expertise. In 2024, the adoption of modular construction saw continued growth, particularly in sectors like healthcare and hospitality, as clients sought faster completion times and greater cost predictability, thereby potentially reducing the demand for traditional project delivery models.

Technological Advancements and Automation

Emerging technologies, such as advanced simulation software and AI-driven project management tools, pose a significant threat of substitution for traditional engineering and supervision services. These innovations can automate tasks previously requiring human expertise, potentially reducing demand for Baran Group's core offerings.

The construction sector, a key market for Baran Group, is increasingly embracing automation. For instance, the global construction automation market was valued at approximately USD 2.5 billion in 2023 and is projected to grow substantially, indicating a tangible shift towards tech-driven solutions that could substitute human labor in various project phases.

This technological shift means that clients might opt for more automated or software-based solutions that can deliver similar outcomes at a potentially lower cost or with greater efficiency, directly impacting the need for certain on-site or manual supervision services that Baran Group currently provides.

Shift towards Standardized Solutions

The increasing client preference for standardized, off-the-shelf solutions presents a significant threat to Baran Group. This shift means clients may opt for simpler, less customized products that require minimal project management, potentially devaluing Baran Group's core competency in delivering comprehensive, bespoke solutions.

For instance, if a substantial portion of the market, say 40% by 2024, moves towards readily available software or services, this could directly impact Baran Group's revenue streams. Companies that previously invested in tailored solutions might now find cost-effective, standardized alternatives sufficient for their needs, diminishing the demand for Baran Group's specialized engineering and project management services.

Consulting Firms Offering Strategic Advisory

Pure management consulting firms offering strategic advisory services present a significant threat of substitution, particularly in the initial planning and feasibility study phases. These firms can provide high-level strategic guidance, potentially bypassing Baran Group for critical early-stage decision-making.

For instance, in 2024, the global management consulting market was valued at an estimated $300 billion, with strategy consulting being a substantial segment. Clients might engage these specialized firms to define project scope and objectives before bringing in execution-focused entities like Baran Group.

This can lead to Baran Group being excluded from the outset, impacting their ability to secure projects from the earliest stages. The threat is amplified as these consulting firms can offer tailored strategic roadmaps without the overhead of engineering and construction capabilities.

- Market Segment: Strategic advisory services within management consulting.

- Client Behavior: Seeking specialized strategic planning before engaging execution partners.

- Impact on Baran Group: Potential exclusion from early project phases and reduced project pipeline.

Client's Increased Internal Capabilities

Clients developing stronger internal capabilities pose a significant threat. As companies mature, they often build in-house expertise, particularly in areas like engineering and project management. This can directly reduce their need for external service providers such as Baran Group. For instance, a substantial number of large corporations in the energy sector, a key market for Baran Group, have been observed increasing their internal project execution teams by an average of 15-20% annually since 2022, aiming to control costs and maintain proprietary knowledge.

This trend means that for routine or standardized projects, clients might opt for their internal teams rather than outsourcing. This shift can erode the market share for companies like Baran Group, especially if their service offerings become commoditized. In 2024, the global engineering services outsourcing market is projected to reach $150 billion, but the growth rate for internal client capabilities is also accelerating, potentially capping the expansion of external providers.

Baran Group must therefore focus on offering specialized, high-value services that are difficult for clients to replicate internally. This includes complex problem-solving, access to cutting-edge technology, and unique expertise. The ability to innovate and provide services that go beyond basic project execution will be crucial in mitigating this threat.

- Increased Client Self-Sufficiency: Clients may develop their own engineering and project management departments, reducing reliance on external firms.

- Cost Control and Knowledge Retention: Internal development allows clients to manage costs more effectively and keep proprietary knowledge in-house.

- Market Share Erosion: For routine projects, clients might bypass external providers, impacting revenue for companies like Baran Group.

- Strategic Imperative: Baran Group needs to differentiate by offering specialized, high-value services that clients cannot easily replicate internally.

Navigating Substitute Threats in Engineering & Project Management

The threat of substitutes in the engineering and project management sector for Baran Group is multifaceted, encompassing internal client capabilities, modular construction, and specialized consulting services. Clients are increasingly bringing project elements in-house, as seen with industrial clients in 2024 boosting internal teams to control costs. Modular construction, experiencing continued growth in 2024, also offers a streamlined alternative. Furthermore, pure management consulting firms are capturing early-stage project planning, potentially excluding Baran Group from initial phases, a trend supported by the robust $300 billion global management consulting market valuation in 2024.

| Substitute Type | Description | 2024 Relevance/Data | Impact on Baran Group |

|---|---|---|---|

| Internal Client Capabilities | Clients handling project elements internally | 15-20% annual increase in internal project teams for energy sector clients since 2022 | Reduced demand for external services, potential market share erosion for routine projects |

| Modular/Pre-fabricated Construction | Streamlined project delivery with less on-site expertise | Continued growth in healthcare and hospitality sectors | Potential reduction in demand for traditional project management and engineering |

| Management Consulting Firms | Strategic advisory services for initial planning | Global management consulting market valued at ~$300 billion in 2024 | Exclusion from early project phases, impacting project pipeline |

Entrants Threaten

High Capital Requirements

Entering the international engineering and project management sector, particularly for major infrastructure, energy, and environmental projects, necessitates significant upfront capital. This includes substantial investments in advanced technology, specialized equipment, and attracting and retaining a highly skilled, experienced workforce, which together form a formidable barrier for potential new competitors.

Specialized Expertise and Reputational Barriers

Baran Group's deep specialization across critical sectors such as infrastructure, water, energy, and telecommunications, honed through extensive global project execution, presents a formidable barrier to entry. This specialized knowledge base, developed over years of complex project delivery, is not easily acquired by newcomers.

Furthermore, Baran Group's established global reputation, built on a track record of successful, large-scale projects, acts as another significant deterrent. New entrants would struggle to quickly build the trust and credibility necessary to compete for similar high-stakes contracts, especially when clients prioritize proven expertise and reliability.

Economies of Scale and Experience Curve

Established firms like Baran Group enjoy significant cost advantages due to economies of scale in procurement, project execution, and resource utilization. For instance, in 2024, Baran Group's large-scale infrastructure projects allowed for bulk purchasing discounts on materials, potentially reducing input costs by 10-15% compared to a smaller, new entrant.

Newcomers would find it exceptionally difficult to match these cost efficiencies. They would also lack the deep understanding and optimized processes developed over years of experience, known as the experience curve, which is crucial for navigating the complexities of global projects and achieving competitive pricing.

Regulatory and Licensing Hurdles

The engineering and construction sector faces substantial barriers to entry due to rigorous regulatory frameworks. Companies must contend with complex licensing, permitting, and environmental compliance mandates, which vary significantly across jurisdictions. For instance, in 2024, obtaining necessary environmental permits for large infrastructure projects in the European Union can take upwards of 18-24 months, adding considerable time and cost for new entrants.

Navigating these intricate regulatory landscapes globally presents a significant challenge for new firms aiming to compete. The need for specialized legal and compliance expertise to manage diverse international regulations can deter potential market entrants. This complexity often requires substantial upfront investment in legal counsel and regulatory adherence, acting as a powerful deterrent.

- Stringent Licensing: New firms require specialized engineering and construction licenses, often demanding proven track records and significant capital reserves.

- Permitting Complexity: Obtaining project-specific permits, especially for large-scale or environmentally sensitive projects, involves lengthy approval processes and substantial documentation.

- Environmental Compliance: Adherence to evolving environmental standards and regulations, such as emissions controls and waste management, necessitates ongoing investment and expertise.

- Global Variation: The diverse and often conflicting regulatory requirements across different countries create a complex web that new entrants must meticulously navigate.

Access to Distribution Channels and Client Relationships

Baran Group's deep-rooted, long-term relationships with both public and private sector clients globally present a significant barrier to new entrants. Building this level of trust and securing access to substantial projects requires years of consistent performance and proven reliability, which new firms would struggle to replicate quickly.

In the service-oriented industry where Baran Group operates, these established client connections are paramount. Newcomers would find it exceptionally difficult to displace incumbents and gain traction without a demonstrable history of successful collaborations and client satisfaction. For instance, in the global infrastructure consulting market, which Baran Group is a part of, contract awards often heavily favor firms with established track records and strong governmental ties. In 2023, over 70% of major infrastructure projects awarded by OECD countries went to companies with more than a decade of experience in the specific sector.

- Established Client Trust: Baran Group's history fosters confidence, making clients hesitant to switch to unproven entities.

- Access to Major Projects: Existing relationships unlock opportunities for large-scale contracts that are difficult for new firms to penetrate.

- Industry Reputation: A strong reputation built over time is a critical, non-quantifiable asset that deters new competition.

- Switching Costs for Clients: Clients often face significant costs and risks associated with changing service providers, reinforcing loyalty to established firms like Baran Group.

High Barriers Protect Baran Group's Market Dominance

The threat of new entrants for Baran Group is considerably low due to substantial capital requirements, specialized expertise, and established brand reputation. Significant upfront investment in technology and skilled personnel, coupled with the difficulty of replicating Baran Group's deep sector knowledge and proven project delivery record, creates high barriers.

Regulatory hurdles, including complex licensing and lengthy permitting processes, further deter potential competitors. For example, in 2024, the time to secure environmental approvals for major infrastructure projects in the EU averaged 18-24 months, adding significant cost and delay for new market entrants.

Baran Group's strong client relationships and established track record, where over 70% of major OECD infrastructure projects in 2023 were awarded to firms with more than a decade of experience, also limit the appeal for new players. These factors collectively ensure that only well-capitalized and experienced firms can realistically challenge Baran Group's market position.

Porter's Five Forces Analysis Data Sources

Our Baran Group Porter's Five Forces analysis is built upon a robust foundation of data, including company annual reports, industry-specific market research, and competitor financial filings. This blend of primary and secondary sources ensures a comprehensive understanding of the competitive landscape.