Bank Of Shanghai Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Bank Of Shanghai

Go Beyond the Preview—Access the Full Strategic Report

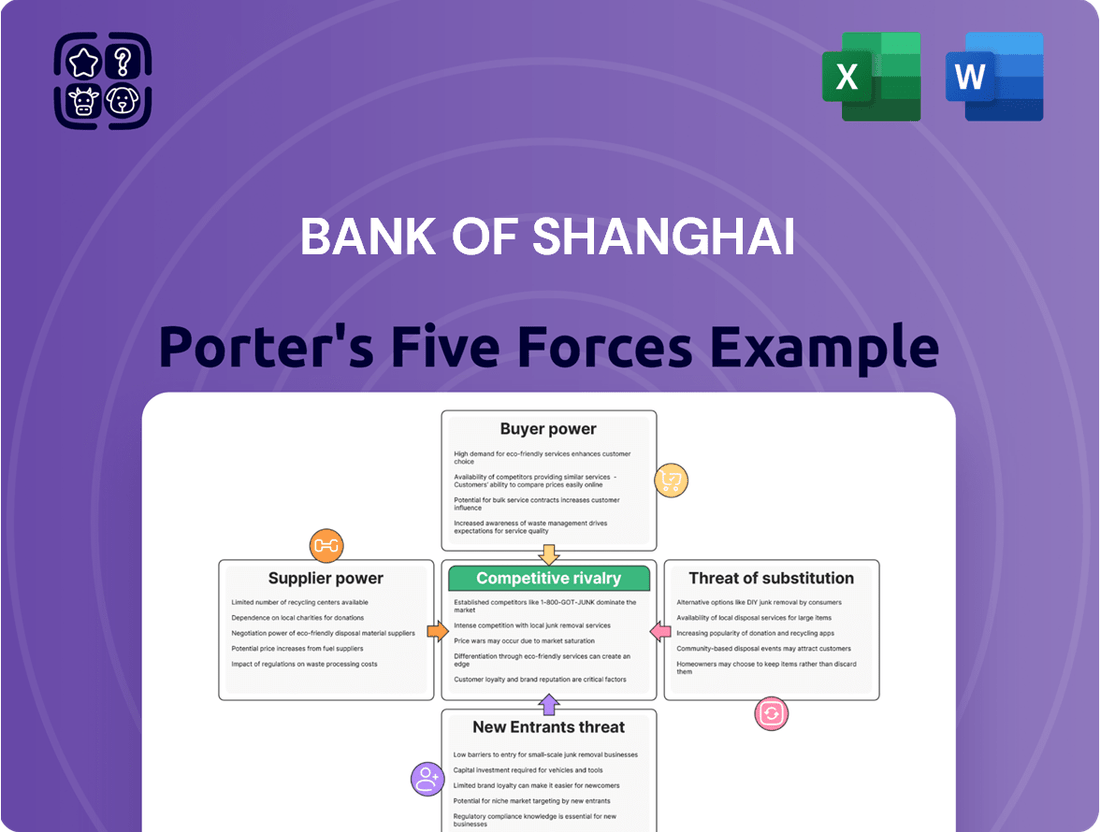

Understanding the Bank of Shanghai's competitive landscape through Porter's Five Forces reveals a dynamic interplay of forces, from the intense rivalry among existing banks to the ever-present threat of new entrants and substitutes. Bargaining power of both buyers and suppliers also plays a crucial role in shaping its strategic options.

The complete report reveals the real forces shaping Bank Of Shanghai’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Fragmented depositor base

The fragmented depositor base in China significantly limits the bargaining power of individual depositors with the Bank of Shanghai. With millions of retail and small business accounts, no single depositor can exert substantial influence. For instance, in 2024, the Bank of Shanghai reported a substantial increase in its retail customer base, further atomizing individual deposit power.

Regulatory caps on deposit rates

Regulatory caps on deposit rates, often set by bodies like the People's Bank of China (PBOC) and the National Financial Regulatory Administration (NFRA), directly curb the bargaining power of depositors. These limits prevent depositors from demanding substantially higher returns on their funds, thereby reducing their leverage as a collective supplier of capital to banks.

Availability of alternative investment products

The increasing variety of investment products available to customers, such as wealth management solutions and money market funds, means that Bank of Shanghai depositors have more options than ever. This diversification of financial products gives depositors greater leverage, as they can easily shift their funds to institutions offering more attractive rates or higher returns if the bank's deposit offerings become less competitive.

Technology and IT service providers

Technology and IT service providers hold some bargaining power as banks like Bank of Shanghai accelerate digital transformation and AI adoption. The demand for specialized, cutting-edge solutions in areas like cloud computing and cybersecurity is high. For instance, in 2024, the global IT services market was projected to reach over $1.3 trillion, with significant growth in areas crucial for financial institutions.

However, this power is somewhat tempered by the competitive landscape within China's IT services sector. Bank of Shanghai, like other major banks, can often leverage this competition to negotiate favorable terms. The availability of multiple vendors offering similar advanced solutions limits the ability of any single provider to dictate terms.

- High demand for specialized AI and digital transformation services increases supplier leverage.

- China's IT services market is competitive, offering banks multiple vendor choices.

- Banks can negotiate better terms due to the availability of comparable solutions from various providers.

Skilled labor and talent

The banking industry, especially with the rapid rise of fintech, demands highly specialized talent. Professionals skilled in areas like artificial intelligence, cybersecurity, and blockchain technology are in particularly high demand. This scarcity of expertise means these individuals can negotiate for better compensation and working conditions, effectively increasing their bargaining power as suppliers of crucial labor.

In 2024, the competition for top tech talent in finance intensified. For instance, the average salary for a senior data scientist in a major financial hub could easily exceed $150,000 annually, with bonuses and stock options further enhancing their leverage. This trend highlights how specialized skills directly translate into supplier power within the banking sector.

- High demand for fintech expertise: Banks increasingly need professionals in AI, machine learning, and cybersecurity.

- Talent scarcity drives up costs: Specialized skills lead to higher salary expectations and benefit demands.

- Negotiating power of skilled professionals: Top talent can command better terms, impacting labor costs for banks.

- Impact on operational expenses: Increased labor costs for specialized roles can affect a bank's profitability.

Supplier Power: Navigating IT & Talent Demands for Bank of Shanghai

The bargaining power of suppliers to Bank of Shanghai is moderately high, particularly for providers of specialized technology and IT services crucial for digital transformation. The intense demand for AI, cloud computing, and cybersecurity solutions means these suppliers can command premium pricing and favorable contract terms. For example, the global market for IT services in finance was expected to see robust growth through 2024, driven by the need for advanced digital capabilities.

However, the competitive nature of China's IT sector offers some counterbalance. Bank of Shanghai can leverage the availability of multiple vendors offering similar advanced solutions to negotiate better terms, thus mitigating the absolute power of any single supplier. This competitive dynamic ensures that while specialized skills are valuable, banks retain a degree of leverage in procurement.

Skilled professionals, especially in areas like AI and cybersecurity, represent another significant supplier group. The scarcity of top-tier talent in these fields allows individuals to negotiate higher salaries and better benefits, directly impacting the bank's operational costs. For instance, in 2024, the demand for data scientists in financial services outstripped supply, leading to significant compensation increases.

| Supplier Group | Bargaining Power Factors | Impact on Bank of Shanghai |

|---|---|---|

| Technology & IT Service Providers | High demand for specialized digital transformation services (AI, cloud, cybersecurity) | Increased negotiation leverage for suppliers, potentially higher costs for the bank. |

| Competitive IT services market in China | Bank can leverage vendor competition to negotiate favorable terms. | |

| Highly Skilled Professionals (Fintech, AI, Cybersecurity) | Scarcity of specialized talent | Suppliers (professionals) can demand higher compensation and benefits, increasing labor costs. |

| Intensified competition for top tech talent in finance (2024) | Further drives up salary expectations and impacts operational expenses. |

What is included in the product

This analysis of Bank of Shanghai's competitive landscape reveals the intensity of rivalry, the bargaining power of customers and suppliers, and the threat of new entrants and substitutes.

Instantly identify and mitigate competitive threats by visualizing the Bank of Shanghai's Porter's Five Forces, allowing for proactive strategic adjustments.

Customers Bargaining Power

Diverse customer segments

The Bank of Shanghai caters to a wide array of customers, from individual savers to large corporations and institutional investors. This diversity means their bargaining power isn't uniform across the board.

Major corporate clients and institutional entities, by virtue of their substantial transaction volumes and deep understanding of financial products, often wield significant leverage. They can frequently negotiate for better rates, preferential services, and bespoke financial solutions, directly impacting the bank's pricing power.

Increased financial literacy and digital access

Customers today are significantly more informed, thanks to widespread financial literacy initiatives and readily available digital tools. This enhanced knowledge allows them to easily compare banking products and services across various institutions, putting them in a stronger position to negotiate.

The ability to swiftly compare rates for deposits and loans online empowers customers to demand better terms. For instance, in 2024, online comparison sites for banking products saw a substantial increase in user engagement, with many reporting over a million unique visitors monthly, highlighting the ease with which consumers can now find competitive offers.

Competition among banks for loans and deposits

In China's highly competitive banking landscape, institutions are actively vying for both loans and deposits, especially with interest rates remaining relatively low. This intense rivalry naturally shifts power toward customers, who can leverage the situation to negotiate more favorable terms. For instance, they can push for reduced interest rates on loans or seek out more attractive deposit yields from different institutions.

The pressure to attract and retain customers means banks are more accommodating to demands for lower borrowing costs. In 2023, China's benchmark lending rate, the Loan Prime Rate (LPR), saw reductions, reflecting this competitive environment and benefiting borrowers. This dynamic empowers customers to shop around for the best deals, increasing their bargaining power.

Emergence of digital banking and fintech platforms

The emergence of digital banking and fintech platforms significantly amplifies customer bargaining power for Bank of Shanghai. These platforms offer specialized, often more convenient, financial services such as digital payments, online lending, and wealth management, presenting customers with a wider array of alternatives to traditional banking. This increased choice empowers customers to switch providers more readily if they are dissatisfied with a bank's offerings or pricing. By 2024, the global fintech market was valued at over $1.1 trillion, demonstrating the substantial competitive landscape banks like Bank of Shanghai must navigate.

This competitive pressure compels traditional banks to innovate and improve their own services to retain customers. For instance, the proliferation of user-friendly mobile banking apps and competitive interest rates on digital savings accounts by fintechs forces established institutions to enhance their digital capabilities and customer experience. In 2023, Chinese fintech companies processed trillions of dollars in digital payments, highlighting the scale of this shift and the customer expectation for seamless digital transactions.

- Increased Competition: Fintechs offer specialized services, fragmenting the market and giving customers more options.

- Customer Mobility: Digital platforms make it easier for customers to switch banks, increasing their leverage.

- Demand for Innovation: Banks are pressured to improve digital offerings and customer service to compete.

- Price Sensitivity: Fintechs often compete on price, pushing traditional banks to offer more competitive rates and fees.

Regulatory focus on consumer protection

The Chinese regulatory landscape, with its increasing emphasis on consumer protection, significantly bolsters the bargaining power of Bank of Shanghai's customers. This focus translates into a more level playing field, where customers are better equipped to demand fair treatment and transparent dealings.

For instance, regulations aimed at preventing predatory lending or ensuring clear fee structures directly empower individuals and businesses interacting with the bank. This heightened awareness and legal recourse mean customers can more effectively negotiate terms or switch providers if their expectations aren't met, directly impacting the bank's pricing and service strategies.

- Enhanced Consumer Rights: Regulations mandate clearer disclosure of fees and interest rates, reducing information asymmetry.

- Promoting Financial Inclusion: Initiatives to make banking services more accessible to underserved populations can increase customer choice and bargaining leverage.

- Fair Practice Enforcement: Regulatory bodies actively monitor and penalize unfair or deceptive practices, giving customers more confidence to assert their rights.

Customer Bargaining Power: A Force in Modern Banking

The bargaining power of customers for Bank of Shanghai is considerable, driven by increased competition, digital accessibility, and evolving regulatory frameworks. Customers, particularly larger corporate entities and informed individuals, can leverage these factors to negotiate better terms.

| Factor | Impact on Bargaining Power | Supporting Data (2023-2024) |

|---|---|---|

| Increased Competition (Fintechs) | Provides customers with more choices and alternatives to traditional banking. | Global fintech market valued over $1.1 trillion in 2024; Chinese fintechs processed trillions in digital payments in 2023. |

| Customer Information & Digital Tools | Enables easy comparison of banking products, leading to demands for better rates. | Online banking comparison sites saw over 1 million unique visitors monthly in 2024. |

| Regulatory Environment | Strengthens consumer rights and promotes fair practices, empowering customers. | Increased regulatory focus on transparency in fees and lending practices. |

| Price Sensitivity & Rate Environment | Customers can push for lower borrowing costs and higher deposit yields. | China's benchmark lending rate (LPR) saw reductions in 2023, benefiting borrowers. |

Same Document Delivered

Bank Of Shanghai Porter's Five Forces Analysis

This preview showcases the entirety of the Bank of Shanghai Porter's Five Forces analysis, detailing the competitive landscape and strategic implications for the institution. You are viewing the exact document you will receive immediately after purchase, ensuring complete transparency and no hidden content or placeholder information. This comprehensive analysis is ready for your immediate use, providing actionable insights into the Bank of Shanghai's market position.

Rivalry Among Competitors

Large number of established players

The competitive rivalry within China's banking sector is fierce, characterized by a multitude of established players. While large state-owned banks hold significant market share, Bank of Shanghai also contends with a substantial number of joint-stock commercial banks, city commercial banks, and foreign-funded institutions. This crowded landscape means intense competition for customers and market share.

Narrowing net interest margins (NIM)

Chinese banks, including Bank of Shanghai, grapple with narrowing net interest margins (NIMs) as lending rates fall and the competition for deposits heats up. This squeeze on profitability directly fuels intense rivalry among institutions vying to hold onto their market share and revenue streams.

For instance, in 2023, the average NIM for listed Chinese banks hovered around 1.7%, a noticeable dip from previous years, reflecting the persistent downward pressure on margins. This environment forces banks to innovate in fee-based income and operational efficiency to offset the declining profitability from traditional lending activities.

Homogeneous core products

Many of Bank of Shanghai's core banking products, such as basic savings accounts and standard corporate loans, are highly commoditized. This similarity in offerings intensifies competition, often forcing banks to compete primarily on price. For instance, in 2023, the average interest rate on savings accounts across major Chinese banks hovered around 0.3%, with minimal differentiation.

While banks strive to differentiate through superior customer service, innovative digital platforms, and niche financial products, the fundamental nature of these core offerings remains largely the same. This homogeneity means that customers can easily switch between providers based on minor rate differences or perceived convenience, putting pressure on Bank of Shanghai to maintain competitive pricing and service levels.

Focus on digital transformation and innovation

Bank of Shanghai faces intense rivalry driven by a significant push towards digital transformation and innovation. Banks are pouring resources into areas like artificial intelligence and fintech, aiming to sharpen their competitive edge, elevate customer experiences, and boost operational efficiency. This technological arms race intensifies competition as institutions battle for dominance in the digital banking landscape.

The pursuit of digital leadership is a key battleground. For instance, in 2024, the global fintech market was projected to reach over $300 billion, highlighting the scale of investment and the potential for disruption. Banks like Bank of Shanghai are not just adopting technology; they are fundamentally rethinking their business models to stay relevant.

- Digital Investment: Banks are allocating substantial capital to AI and cloud computing to enhance services and reduce costs.

- Fintech Integration: Collaboration or competition with fintech startups is a major factor in staying ahead.

- Customer Experience: Superior digital platforms and personalized services are crucial differentiators.

- Operational Efficiency: Automation and AI are being used to streamline back-office functions, reducing overhead and improving speed.

Government policies and guidance

Government policies significantly shape the competitive landscape for banks like Bank of Shanghai. Initiatives promoting green finance, for instance, encourage banks to develop new products and services, potentially creating new competitive arenas. In 2023, China's central bank continued to emphasize support for the real economy, with targeted lending facilities and policy adjustments aimed at sectors like manufacturing and technology.

Banks that effectively align their strategies with these national priorities, such as inclusive finance or supporting small and medium-sized enterprises (SMEs), can gain a competitive edge. This alignment often involves adjusting lending practices and developing specialized financial solutions. For example, by mid-2024, many Chinese banks were actively increasing their support for technology innovation and green development projects, as guided by regulatory bodies.

- Government Initiatives: Policies promoting green finance and support for the real economy directly influence bank strategies.

- Strategic Alignment: Banks compete by aligning operations with national priorities like inclusive finance.

- Shifting Dynamics: Government guidance can create new competitive areas and alter existing market structures.

China's Banking Battle: Navigating Intense Rivalry and Digital Transformation

The competitive rivalry within China's banking sector is intense, with Bank of Shanghai facing numerous domestic and international competitors. This crowded market forces banks to compete aggressively on pricing, service, and innovation, particularly in the digital space. Narrowing net interest margins, exemplified by a 2023 average NIM around 1.7% for listed Chinese banks, further fuels this rivalry as institutions seek to maintain profitability.

The commoditized nature of core banking products means differentiation is challenging, leading to price-based competition. For instance, savings account interest rates in 2023 were around 0.3% across major banks, with minimal variation. This environment pushes Bank of Shanghai to focus on enhancing customer experience through digital platforms and specialized offerings to stand out.

The race for digital dominance is a critical battleground, with significant investments in AI and fintech. By mid-2024, global fintech investments were projected to exceed $300 billion, underscoring the strategic importance of technological advancement. Banks are leveraging these technologies to improve efficiency and customer engagement, intensifying the competitive landscape.

Government policies also play a crucial role, with initiatives like green finance and support for the real economy creating new competitive avenues. Banks that align with these priorities, such as supporting SMEs or technology innovation, as guided by regulators by mid-2024, can gain a strategic advantage.

| Key Competitive Factors | Observation | Impact on Bank of Shanghai |

| Number of Competitors | Numerous state-owned, joint-stock, city commercial, and foreign banks | High pressure on market share and pricing |

| Profitability Squeeze | Narrowing Net Interest Margins (NIMs) (Avg. ~1.7% in 2023 for listed banks) | Drives competition for revenue and operational efficiency |

| Product Commoditization | Similar core banking products (e.g., savings accounts with ~0.3% interest in 2023) | Intensifies price competition and need for differentiation |

| Digital Transformation | Significant investment in AI, fintech (Global fintech market projected >$300B in 2024) | Necessitates innovation in digital services and customer experience |

| Regulatory Influence | Policies on green finance, real economy support | Creates opportunities and competitive pressures based on strategic alignment |

SSubstitutes Threaten

Fintech companies and digital payment platforms

Fintech companies, such as Alipay and WeChat Pay, present a substantial threat by offering highly convenient digital payment and financial services that directly substitute traditional bank payment and settlement solutions. These platforms have captured a vast user base in China, with reports indicating over 1.2 billion active users across both in 2023, significantly impacting conventional banking transactions.

Online lending platforms

Online lending platforms and peer-to-peer (P2P) services present a significant threat of substitutes for Bank of Shanghai. These platforms, particularly those catering to small businesses and individuals, offer alternative avenues for financing outside traditional banking channels. For instance, by mid-2024, the global P2P lending market was projected to reach over $100 billion, indicating a substantial shift in borrowing behavior.

Wealth management products and direct investments

Customers increasingly have access to a broad spectrum of wealth management products from non-bank financial institutions, mutual funds, and direct investment platforms. This allows them to diversify their savings and investments beyond traditional bank deposit accounts, thereby diminishing their reliance on banks for wealth accumulation. For instance, in 2024, the global wealth management market was valued at approximately $79.4 trillion, showcasing the vastness of alternative options available to consumers.

Central Bank Digital Currency (e-CNY)

The emergence of China's digital yuan (e-CNY) presents a significant threat of substitutes for traditional banking services. By offering a direct digital payment channel, it bypasses commercial banks for certain transactions, potentially reducing their intermediary role and revenue streams in the payments sector. As of late 2023, the e-CNY pilot program had expanded to over 26,000 application scenarios across more than 30 cities, with transaction volumes reaching hundreds of billions of yuan, underscoring its growing adoption and competitive pressure.

This central bank digital currency (CBDC) directly competes with the payment services provided by commercial banks like Bank of Shanghai. Its increasing integration into daily life, from retail purchases to public transport, directly substitutes for services where banks have historically held a dominant position.

The threat is amplified as the e-CNY's functionality potentially expands beyond payments to include other financial services, further encroaching on the traditional offerings of commercial banks.

- Digital Yuan Adoption: Over 26,000 application scenarios for e-CNY as of late 2023.

- Transaction Value: Hundreds of billions of yuan processed through e-CNY pilots.

- Competitive Impact: Direct substitution for commercial bank payment services.

- Future Scope: Potential expansion of e-CNY to broader financial services.

Shadow banking activities

Shadow banking activities present a significant threat of substitutes for Bank of Shanghai. These entities, operating outside traditional regulatory frameworks, offer alternative avenues for both borrowing and investing. For instance, by mid-2024, the global shadow banking sector was estimated to be worth trillions of dollars, providing substantial capital that might otherwise flow through conventional banks.

This parallel financial system can siphon off business from established banks like Bank of Shanghai. Customers seeking higher yields on deposits or more flexible lending terms may be drawn to wealth management products, peer-to-peer lending platforms, or other non-bank financial intermediaries. This competition directly impacts deposit growth and loan origination volumes for traditional institutions.

- Alternative Financing: Shadow banking offers credit and investment products that bypass traditional bank intermediation.

- Deposit Outflows: Higher yields and different product structures in the shadow sector can attract customer deposits away from banks.

- Regulatory Arbitrage: Less stringent regulations in some shadow banking areas can allow for more competitive pricing and product innovation.

Digital Disruptors and Shadow Finance Reshape Banking Landscape

The threat of substitutes for Bank of Shanghai is significant, driven by a burgeoning landscape of alternative financial service providers. Fintech innovations, digital currencies, and less regulated financial entities are increasingly offering services that directly compete with traditional banking functions, potentially eroding market share and profitability.

Digital payment platforms like Alipay and WeChat Pay have already captured a massive user base in China, with over 1.2 billion combined active users in 2023, directly challenging bank payment systems. Similarly, the digital yuan (e-CNY) is expanding its reach, with over 26,000 application scenarios by late 2023, processing hundreds of billions of yuan and bypassing commercial banks in transactions.

| Substitute Type | Key Characteristics | Market Presence/Impact (2023-2024 Data) |

| Fintech Payment Platforms | Convenience, wide user adoption | >1.2 billion combined active users (Alipay/WeChat Pay, 2023) |

| Digital Yuan (e-CNY) | Direct digital payment, bypasses banks | >26,000 application scenarios (late 2023); Hundreds of billions of yuan processed |

| Online Lending/P2P | Alternative financing for individuals/SMEs | Global P2P lending market projected >$100 billion (mid-2024) |

| Shadow Banking | Unregulated credit/investment products | Global sector estimated in trillions of dollars (mid-2024) |

| Non-Bank Wealth Management | Diversified investment options | Global wealth management market ~$79.4 trillion (2024) |

Entrants Threaten

High regulatory barriers

The Chinese banking sector, overseen by entities like the National Financial Regulatory Administration (NFRA) and the People's Bank of China (PBOC), presents substantial regulatory barriers. These include rigorous licensing procedures, strict capital adequacy ratios, and ongoing prudential supervision, effectively limiting the influx of new competitors.

Significant capital requirements

Significant capital requirements are a major hurdle for new banks looking to enter the market. For instance, in 2024, regulatory bodies often mandate substantial minimum capital reserves to ensure financial stability and protect depositors. Establishing a physical presence, developing robust IT systems, and adhering to stringent compliance standards all demand considerable upfront investment, often in the billions of dollars, making it difficult for smaller or less-funded entities to compete with established players like the Bank of Shanghai.

Established brand loyalty and trust

Established brand loyalty and trust act as a significant barrier to entry for new banks. Incumbent institutions like the Bank of Shanghai have cultivated deep-rooted customer relationships and a strong reputation for security and reliability, which are hard for newcomers to replicate swiftly. For instance, in 2023, the Bank of Shanghai reported a customer deposit base exceeding RMB 1.4 trillion, showcasing the scale of trust it has earned.

Economies of scale and network effects

Existing banks, like Bank of Shanghai, benefit significantly from economies of scale. This allows them to spread costs across a large operational base, covering technology investments, marketing, and extensive branch networks. For instance, by mid-2024, major Chinese banks reported substantial asset bases, enabling them to offer more competitive interest rates and a wider array of financial products than a new entrant could easily match without massive upfront capital.

Network effects further bolster the position of established players. A larger customer base often leads to more data, better insights into market trends, and a stronger ability to attract and retain talent, creating a virtuous cycle. A new bank would face considerable hurdles in building a comparable network and trust within the market, especially when competing against institutions with decades of operational history and established customer relationships.

- Economies of Scale: Established banks leverage their size to reduce per-unit costs in operations, technology, and marketing, making it difficult for new entrants to compete on price.

- Network Effects: A larger customer base for existing banks creates a more valuable service and greater market influence, a hurdle for newcomers to overcome.

- Capital Requirements: Significant initial investment is needed for new entrants to build comparable infrastructure and reach, posing a substantial barrier.

Intense competition from incumbents

Any new entrant would face intense competition from well-capitalized and established domestic banks like Industrial and Commercial Bank of China (ICBC) and China Construction Bank (CCB), which would aggressively defend their market share. These incumbents possess significant brand loyalty and extensive branch networks, making it difficult for newcomers to gain traction.

The current environment of narrowing margins, with net interest margins for Chinese banks declining from around 2.2% in 2022 to an estimated 2.0% in 2024, further intensifies this competitive response. Established players are likely to engage in aggressive pricing strategies and enhanced service offerings to retain customers, creating a formidable barrier for any new entrant.

- Incumbent Market Share: Major Chinese banks hold substantial market share, with the top five banks controlling over 50% of total banking assets as of late 2023.

- Capitalization: Leading domestic banks are well-capitalized, with Tier 1 capital ratios often exceeding regulatory requirements, allowing them to absorb potential losses and invest heavily in competitive strategies.

- Margin Pressure: The ongoing trend of declining net interest margins forces incumbents to compete more fiercely on fees, service quality, and customer retention, making market entry challenging.

China's Banking Barriers: A Fortress Against New Entrants

The threat of new entrants for Bank of Shanghai is considerably low due to stringent regulatory hurdles, high capital requirements, and the significant advantages held by established players. These factors combine to create a challenging environment for any new bank seeking to enter the Chinese market, especially when competing against the scale, brand recognition, and established networks of incumbents.

| Barrier Type | Description | Impact on New Entrants |

| Regulatory Requirements | Rigorous licensing, capital adequacy, and prudential supervision by NFRA and PBOC. | High barrier; requires extensive compliance and financial strength. |

| Capital Investment | Substantial upfront capital needed for infrastructure, technology, and compliance. | High barrier; estimated billions of dollars for a competitive setup. |

| Economies of Scale | Lower per-unit costs for established banks in operations, technology, and marketing. | High barrier; new entrants struggle to match competitive pricing. |

| Brand Loyalty & Trust | Deep-rooted customer relationships and reputation of incumbents. | High barrier; difficult for new players to build comparable trust. |

| Network Effects | Larger customer bases provide better data, insights, and talent attraction for incumbents. | High barrier; challenging to replicate established networks. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for the Bank of Shanghai is built upon a foundation of publicly available financial statements, annual reports, and regulatory filings from the bank itself and its key competitors. We also incorporate data from reputable financial news outlets and industry-specific research reports to capture market dynamics and competitive strategies.