Indian Railway Finance Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Indian Railway Finance

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

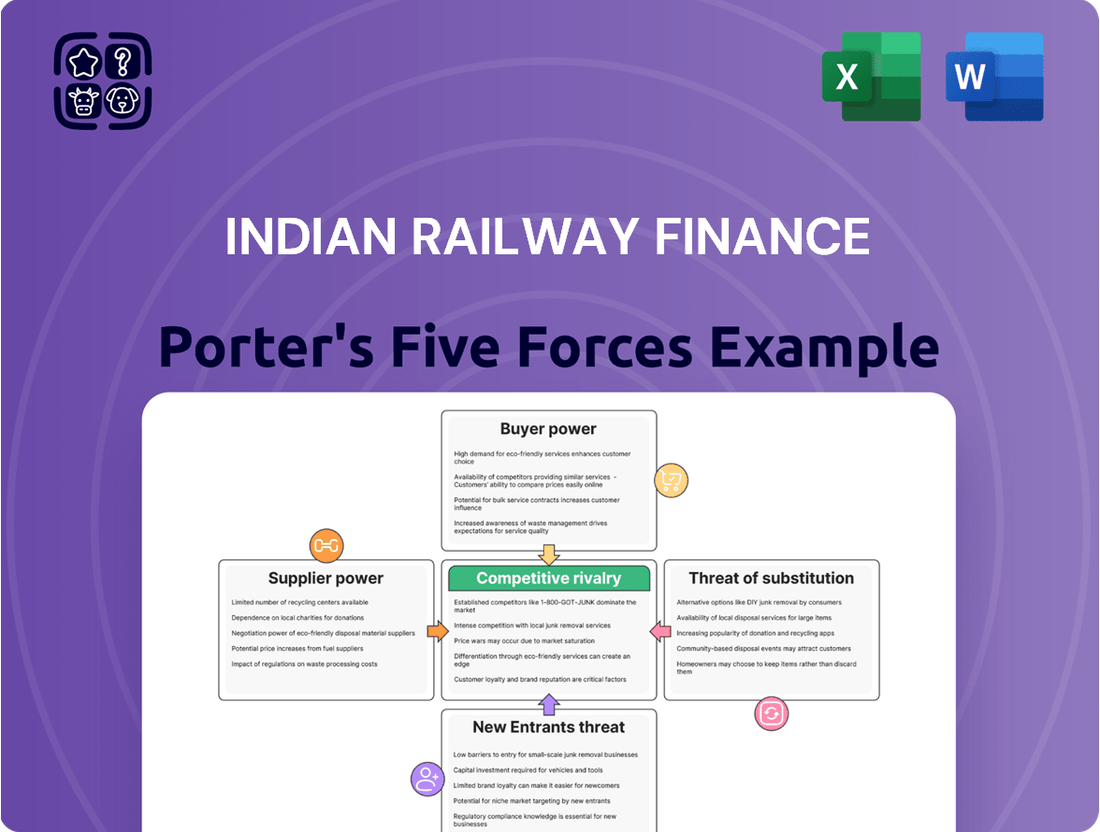

The Indian Railway Finance Corporation (IRFC) operates within a dynamic environment shaped by several powerful forces. Understanding these forces is crucial for any stakeholder seeking to grasp IRFC's strategic position and future prospects.

The bargaining power of buyers, primarily government entities and large institutional investors, can significantly influence IRFC's financing terms. Similarly, the threat of substitute financial instruments or alternative infrastructure funding models warrants careful consideration.

The intensity of rivalry among financial institutions vying for infrastructure project financing presents another key challenge. Meanwhile, the ability of suppliers, such as credit rating agencies and financial advisors, to exert influence over IRFC's operations is also a factor.

The threat of new entrants, while potentially moderate due to high capital requirements, could still emerge with innovative financing solutions. This brief snapshot only scratches the surface.

Unlock the full Porter's Five Forces Analysis to explore Indian Railway Finance’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Limited Number of Lenders

IRFC primarily sources funds from domestic and international capital markets, with a finite number of large institutional lenders and bond subscribers acting as key suppliers.

While this limited pool could theoretically give lenders leverage, IRFC's strong credit profile significantly mitigates this power.

Its sovereign guarantee from the Government of India ensures high creditworthiness, reaffirmed by ratings like ICRA's AAA (Stable) for its long-term debt in 2024.

This strong backing ensures IRFC maintains access to competitive borrowing rates, even with a concentrated supplier base.

Government Influence on Borrowing

The Government of India, as the majority shareholder, profoundly influences IRFC's borrowing, essentially acting as a dominant supplier of borrowing terms. Policy decisions and Union Budget 2024-25 allocations directly dictate the timing and volume of funds IRFC needs to raise for railway projects, such as the record capital outlay of approximately INR 2.52 lakh crore for Indian Railways in FY2024. This dependence provides stability and sovereign backing for IRFC's debt instruments, enhancing their attractiveness to lenders. However, it also significantly limits IRFC's autonomy in sourcing funds or negotiating interest rates independently. While IRFC aims to diversify funding, sovereign control remains paramount.

Cost of Borrowing

The cost of borrowing significantly influences IRFC's financial health, as fluctuations in domestic and international interest rates directly impact its cost of funds. While IRFC operates on a cost-plus agreement with Indian Railways, substantial volatility in borrowing costs, such as changes in the RBI's repo rate, can still affect its financial planning. To mitigate this, IRFC relies on diverse funding sources, including domestic bonds, external commercial borrowings (ECBs), and loans from financial institutions. For example, in FY2024, IRFC continued to diversify its borrowing mix to optimize funding costs.

Credit Rating Agencies

Credit rating agencies significantly influence Indian Railway Finance Corporation’s (IRFC) borrowing costs by assessing its financial health. A robust credit rating, such as IRFC's 'AAA' rating from CRISIL and ICRA in 2024, is crucial for securing funds at competitive rates. These agencies, therefore, wield considerable indirect power over IRFC’s primary capital supply, impacting its ability to finance railway projects. Their assessments directly affect investor confidence and the terms of debt issuance.

- IRFC maintained a 'AAA' rating from CRISIL and ICRA as of early 2024.

- These high ratings enable IRFC to access capital markets efficiently.

- A one-notch downgrade could increase borrowing costs by basis points, impacting project viability.

- Rating agencies are key gatekeepers for IRFC's access to domestic and international debt.

Rolling Stock Manufacturers

Rolling stock manufacturers indirectly influence Indian Railway Finance Corporation's (IRFC) business volume, as their capacity and pricing determine the scale of railway assets needing financing. A concentrated market for specialized locomotives and wagons can significantly increase these suppliers' bargaining power over Indian Railways. For example, in 2024, major tenders for new Vande Bharat trainsets and freight locomotives highlight the reliance on a few key players.

- India’s capital outlay for railways in 2024-25 is approximately INR 2.52 lakh crore.

- Leading manufacturers like Chittaranjan Locomotive Works (CLW) and Diesel Locomotive Works (DLW) are key suppliers.

- Private sector participation is growing, yet specialized components often come from limited sources.

- The Indian Railways' ambitious target of 3,000 km of new tracks annually by 2024-25 drives demand for new rolling stock.

Shielded by Sovereignty: IRFC's Supplier Dynamics

The bargaining power of IRFC's suppliers, primarily large institutional lenders, is significantly mitigated by its sovereign guarantee from the Government of India, ensuring high creditworthiness and competitive borrowing rates, evidenced by its AAA ratings in 2024. While the Government of India acts as a dominant supplier of borrowing terms, dictating funds for projects like the INR 2.52 lakh crore railway capital outlay in FY2024, this also provides stability. Credit rating agencies, with IRFC's 'AAA' rating from CRISIL and ICRA as of early 2024, indirectly influence borrowing costs by affecting investor confidence. Rolling stock manufacturers also indirectly impact business volume, with major tenders for Vande Bharat trainsets in 2024 highlighting reliance on a few key players.

| Supplier Type | Bargaining Power | 2024 Context |

|---|---|---|

| Institutional Lenders | Low to Moderate | IRFC's AAA rating, sovereign guarantee |

| Government of India | High (as decision-maker) | INR 2.52 lakh crore railway outlay FY2024 |

| Credit Rating Agencies | Indirectly High | CRISIL/ICRA AAA ratings maintained |

What is included in the product

This Porter's Five Forces analysis for Indian Railway Finance (IRFC) dissects the competitive intensity within its sector, examining supplier and buyer power, the threat of new entrants and substitutes, and the overall industry rivalry.

Quickly identify and mitigate competitive threats by visualizing the intensity of each of Porter's Five Forces on the Indian Railway Finance Porter.

Gain actionable insights into the bargaining power of suppliers and buyers, allowing for strategic adjustments to improve financial leverage.

Customers Bargaining Power

Monopolistic Customer Base

Indian Railway Finance Corporation (IRFC) operates with a unique customer base, as its primary client is the Indian Railways, effectively the Ministry of Railways, creating a monopsonistic relationship. This high concentration means nearly all of IRFC's business, with its loan book exceeding ₹4.7 trillion by March 2024, is directed towards a single entity. Consequently, the Indian Railways possesses immense bargaining power over IRFC. All lease agreements and financing terms are negotiated directly with the Ministry, allowing it significant leverage in dictating conditions and rates.

Government Mandate and Control

As a public sector undertaking, Indian Railway Finance Corporation’s operations are intrinsically linked to the government’s agenda for the railway sector. The Union Budget 2024-25 allocated a substantial capital outlay of ₹2.55 lakh crore for railways, directly dictating the demand for IRFC’s financing. This strong governmental control means the customer, Indian Railways, wields significant power. Their expansion plans and policy changes directly determine the projects IRFC will fund, underscoring high customer bargaining power.

Cost-Plus Pricing Model

The Indian Railway Finance Corporation operates on a cost-plus pricing model, where lease rentals are determined by its cost of borrowing plus a pre-determined margin. While this structure ensures IRFC's profitability, the specific margin is subject to direct negotiation with the Ministry of Railways, its primary customer. This negotiation power gives the Ministry significant leverage over IRFC's financial outcomes. For instance, in fiscal year 2024, IRFC's net profit margin remained within a tight band, influenced by these agreements, highlighting the customer's considerable bargaining strength.

Long-Term Lease Agreements

Long-term lease agreements, often spanning 30 years, define the financial relationship between IRFC and Indian Railways. While these leases offer predictable revenue streams for IRFC, they also inherently lock the company into terms with its primary customer for an extended duration. The bargaining power of Indian Railways, as the sole major client, is significant, influencing critical clauses such as interest rate resets and other financial covenants that directly impact IRFC's profitability. For instance, in the fiscal year ending March 2024, IRFC continued to primarily finance railway projects through these long-term arrangements.

- IRFC's revenue visibility is secured by these long-term, typically 30-year, lease agreements.

- The singular customer relationship with Indian Railways grants it substantial leverage in negotiating lease terms.

- Critical clauses like interest rate resets in these agreements directly influence IRFC's financial performance.

- As of early 2024, IRFC's business model remains heavily reliant on these long-duration financing structures.

Diversification Efforts

IRFC has actively diversified its lending portfolio, extending financing beyond the Ministry of Railways to other railway ecosystem entities. This strategic move includes significant funding for Rail Vikas Nigam Limited (RVNL) and various other critical railway infrastructure projects. Such diversification aims to reduce IRFC's overwhelming dependence on its primary customer, thereby mitigating the high bargaining power traditionally held by the Ministry of Railways. By expanding its client base, IRFC enhances its financial resilience and strategic flexibility within the Indian railway sector.

- For FY2024, IRFC aimed to increase its non-Ministry of Railways loan book to over 10% of total disbursements.

- RVNL's project pipeline, valued at over INR 75,000 crores as of early 2024, represents a key area for IRFC's diversified lending.

Railways' Monopsony: Dictating Terms for India's Rail Financier

Indian Railways, as IRFC's sole major customer, holds substantial bargaining power, dictating terms and margins on long-term lease agreements. This monopsonistic relationship means the Ministry of Railways, influenced by the ₹2.55 lakh crore railway capital outlay for 2024-25, significantly impacts IRFC's profitability. While diversification efforts are underway, aiming for over 10% non-Ministry loan book by FY2024, the core dependence remains high. This ensures the customer continues to wield considerable influence over financing conditions.

| Factor | Description | 2024 Data |

|---|---|---|

| Customer Base | Primary client: Indian Railways | Loan book >₹4.7 trillion |

| Government Control | Linked to Union Budget | ₹2.55 lakh crore for Railways |

| Diversification Goal | Non-Ministry lending | Target >10% of disbursements |

What You See Is What You Get

Indian Railway Finance Porter's Five Forces Analysis

The document you see is your deliverable. It’s ready for immediate use—no customization or setup required. This comprehensive Porter's Five Forces analysis for Indian Railway Finance delves into the competitive landscape, examining the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the sector. Understanding these forces is crucial for strategic decision-making and forecasting future profitability for Indian Railway Finance.

Rivalry Among Competitors

Absence of Direct Competitors

Indian Railway Finance Corporation (IRFC) operates as the dedicated financing arm for Indian Railways, maintaining a virtual monopoly in its core business. As of 2024, no other domestic entities possess the same specific mandate and scale for financing railway assets. This unique positioning significantly limits direct competitive rivalry for IRFC. Its specialized role ensures it faces negligible competition in its primary function of funding railway infrastructure and rolling stock.

Other Public Sector Financial Institutions

While Indian Railway Finance Corporation (IRFC) operates with a distinct focus on railway financing, it faces indirect rivalry from other public sector financial institutions in India. Entities like Power Finance Corporation (PFC) and REC Limited, which also issue bonds, compete for capital in the broader debt markets. This competition for investor funds, especially for long-term borrowings, can influence IRFC's borrowing costs and its access to diverse capital sources. For instance, as of early 2024, the bond market saw various PSU issuances, creating a competitive landscape for attracting large institutional investments. Despite this, IRFC's strategic importance and specific mandate for Indian Railways maintain its unique position.

Government's Budgetary Allocations

The Union Government's direct budgetary support is a significant competitive factor for Indian Railway Finance Corporation. If the government increases its capital allocation to the Ministry of Railways, it directly reduces the reliance on extra-budgetary resources raised by IRFC. For instance, the interim Union Budget for 2024-25 allocated a capital outlay of over ₹2.52 lakh crore for Indian Railways, marking a substantial increase. This substantial direct funding acts as an internal form of competition for railway project financing, potentially impacting IRFC's business volume.

Potential for Private Sector Participation

While the Indian Railway Finance Corporation (IRFC) largely dominates railway financing, any future policy shifts allowing private sector companies to directly finance railway projects could introduce significant competition. The government has consistently explored private participation across various aspects of the railway sector, extending to financing mechanisms. For instance, the Indian Railways aims for a capital expenditure of around ₹2.60 lakh crore in 2024-25, much of which traditionally comes from IRFC and budgetary support. However, initiatives like the corporatization of railway production units and the push for private train operations indicate a broader openness to private capital. This evolving landscape suggests a potential for new private entities to emerge as direct financing rivals, especially for new infrastructure projects like the Dedicated Freight Corridors.

- Government initiatives like the National Rail Plan 2030 envision significant private investment in rail infrastructure.

- The Indian Railways' Public-Private Partnership (PPP) cell is actively exploring models for private financing of projects.

- Potential private entrants could include large infrastructure funds or specialized financial institutions.

- Policy changes in 2024-25 facilitating easier private project execution could accelerate this shift.

International Financial Institutions

International financial institutions offer an alternative funding avenue for Indian Railways, particularly for large infrastructure projects. While this is not direct competition to IRFC's core model of domestic market borrowing, it broadens the funding landscape for railway development. IRFC maintains a strong competitive edge due to its established domestic structure, sovereign backing, and efficient access to Indian debt markets. For instance, IRFC successfully raised ₹500 crore through a private placement of bonds in March 2024, demonstrating its strong domestic funding capabilities.

- IRFC's domestic market dominance is evident, securing over 80% of Indian Railways' extra-budgetary resources annually.

- International loans, like those from ADB or JICA, often target specific projects such as high-speed rail corridors.

- IRFC's cost of funds in the domestic market remains highly competitive due to its AAA credit rating.

- In FY2024, IRFC continued to be the primary financing arm for Indian Railways' capital expenditure.

IRFC's Monopoly: Indirect Challenges & Future Competitive Shifts

Indian Railway Finance Corporation (IRFC) holds a near monopoly in railway financing, limiting direct competition. Yet, it faces indirect rivalry for capital from other public sector entities in the broader debt market, impacting borrowing costs in 2024. Government budgetary allocations to Indian Railways also serve as a competitive factor, potentially reducing IRFC's financing volume. Future policy shifts towards private sector involvement could introduce significant new competitors.

| Rivalry Factor | Impact on IRFC | 2024 Context |

|---|---|---|

| Direct Competition | Minimal due to unique mandate | No new direct competitors emerged |

| Indirect (Debt Market) | Competes for capital with PSUs | Various PSU bond issuances observed |

| Government Funding | Reduces reliance on IRFC | ₹2.52 lakh crore allocated to Railways |

SSubstitutes Threaten

Direct Government Funding

The most significant substitute for IRFC's financing is direct budgetary support from the Government of India to the Ministry of Railways.

An increase in the central government's capital outlay for railways could diminish IRFC's role as the primary fundraiser.

For the fiscal year 2024-25, the Union Budget allocated a record capital outlay of ₹2.55 lakh crore for Indian Railways, showcasing this potential.

This is a key variable dependent on prevailing fiscal policy and government priorities.

Public-Private Partnerships (PPPs)

The Indian government's increasing emphasis on Public-Private Partnerships (PPPs) for infrastructure, including railways, presents a significant potential substitute. Private entities can directly invest in and finance railway projects, potentially bypassing the need for Indian Railway Finance Corporation's (IRFC) intermediation. For instance, the 2024 Union Budget continues to push for private sector participation in areas like station redevelopment and new line construction, such as the Amrit Bharat Station Scheme. This direct private funding mechanism could reduce the reliance on traditional financing channels like IRFC for specific projects, impacting its market share.

Other Debt Instruments

Indian Railways inherently possesses the capacity to raise funds directly through its own bonds or other debt instruments, although this has not traditionally been its primary funding model. Indian Railway Finance Corporation (IRFC) has largely served as the dedicated financing vehicle. However, should the Ministry of Railways decide to significantly develop its own in-house borrowing capabilities on a larger scale, perhaps leveraging sovereign guarantees more directly, it would present a clear substitute for IRFC's specialized financial services. As of 2024, IRFC continues to be the main channel for market borrowings, having raised substantial funds, for instance, through public issues and various bonds for railway projects.

Leasing from Manufacturers

Rolling stock manufacturers, both domestic and international, could potentially offer direct leasing options to Indian Railways, acting as a substitute for IRFC’s finance lease model. While this represents a theoretical threat, the immense scale of Indian Railways’ capital expenditure, projected to be over INR 2.5 trillion by 2024-25, often exceeds the direct financing capabilities of individual manufacturers. The significant financial capacity and long-term commitment required to fund such large-scale acquisitions make this a limited substitute at present.

- Indian Railways' significant capital outlay limits direct manufacturer financing.

- Manufacturers typically lack the extensive financial resources of dedicated finance institutions like IRFC.

- The long-term nature of railway asset financing favors specialized lessors.

- Direct leasing from manufacturers remains a niche rather than a systemic threat to IRFC.

Alternative Infrastructure Financing Models

The emergence of new infrastructure financing models, particularly Infrastructure Investment Trusts (InvITs), presents a long-term substitute threat to traditional railway funding sources like IRFC. While IRFC primarily raises debt for Indian Railways, the financial market evolution could see InvITs directly funding railway assets. For instance, as of early 2024, India's InvIT market continues to grow, attracting significant private capital for infrastructure projects. This shift allows private investors to directly participate in revenue-generating assets, potentially bypassing conventional financing routes.

- InvITs raised over 200 billion INR in India by early 2024, signaling growing investor appetite for direct infrastructure investment.

- The Indian government actively promotes InvITs for asset monetization, including potential railway infrastructure.

- Direct private equity and pension funds increasingly explore InvIT routes for long-term, stable returns.

- This model shifts funding from debt-centric to equity-based, offering alternative capital pools for large-scale projects.

New Funding Channels Challenge IRFC's Dominance

The primary substitutes for IRFC's financing include direct government budgetary support, significantly increased to ₹2.55 lakh crore for Indian Railways in 2024-25. Growing Public-Private Partnerships and the potential for Indian Railways to issue its own bonds also pose threats. Emerging InvITs, having raised over 200 billion INR by early 2024, offer alternative equity-based funding channels, though direct manufacturer leasing remains limited due to scale.

| Substitute Type | 2024/25 Data | Impact on IRFC |

|---|---|---|

| Government Budgetary Support | ₹2.55 lakh crore capital outlay (2024-25) | Reduces reliance on IRFC debt. |

| Public-Private Partnerships | Amrit Bharat Station Scheme (2024 focus) | Bypasses IRFC for project funding. |

| Indian Railways' Own Borrowing | IRFC remains primary channel (2024) | Potential long-term shift. |

| Infrastructure Investment Trusts (InvITs) | >200 billion INR raised (early 2024) | Alternative equity funding for assets. |

Entrants Threaten

High Barriers to Entry

The threat of new entrants in the Indian railway financing sector is exceptionally low due to formidable barriers to entry. A new entity would necessitate a specific government mandate to operate as a dedicated financing arm for Indian Railways, a role currently fulfilled by Indian Railway Finance Corporation (IRFC). This represents a significant regulatory and political hurdle, as the sector's scale, with Indian Railways' capital outlay for 2024-25 projected around INR 2.52 lakh crore, demands immense capital and sovereign backing. Such a specialized and strategically vital function is not open to new private or public competition without explicit state directive.

Sovereign Guarantee and Relationship with GoI

The Indian Railway Finance Corporation (IRFC) thrives on its deep-rooted relationship with the Government of India, benefiting from an implicit sovereign guarantee. This backing significantly enhances its creditworthiness, enabling access to exceptionally low-cost funds, crucial for financing large-scale railway projects. For instance, IRFC successfully raised over ₹32,500 crore through various borrowings in the fiscal year 2023-24, leveraging this trust. A new entrant would find it nearly impossible to replicate such an established level of government trust and the associated financial advantages, posing an immense barrier to entry in this specialized financing sector.

Massive Capital Requirements

The sheer scale of capital needed for Indian Railways infrastructure projects creates a formidable barrier for any new financial entrant. To illustrate, the Indian Railways' capital expenditure target for fiscal year 2024-25 is an ambitious ₹2.52 lakh crore, or approximately $30 billion, demonstrating the massive investment required. Any potential competitor would need access to similarly vast amounts of capital to fund railway expansion or rolling stock, an undertaking far exceeding typical private sector capabilities. This immense financial hurdle effectively limits competition, cementing IRFC's dominant position due to its established borrowing capacity and substantial balance sheet.

Established Low-Risk Business Model

IRFC’s established cost-plus business model presents a significant barrier to new entrants. This model, characterized by standardized lease agreements for rolling stock and infrastructure, ensures predictable revenue streams with minimal risk, a track record proven over decades. Replicating this deep understanding of the Indian railway sector’s unique financial needs and its long-standing relationship with the Ministry of Railways would be an immense challenge for any prospective competitor, especially given IRFC’s extensive asset base. This entrenched operational framework and sovereign backing make market penetration incredibly difficult for new players.

- IRFC's net profit for Q3 FY24 reached ₹1,604.22 crore, showcasing consistent profitability.

- The company's asset under management (AUM) grew by 17.76% year-on-year to ₹4,68,900 crore as of December 31, 2023.

- IRFC maintains a strong credit rating, reflecting its low-risk profile and government support.

- Their cost-plus model ensures a stable margin, making it unattractive for new entrants to compete on price.

Exemptions and Specialized Status

The Indian Railway Finance Corporation (IRFC) enjoys unique regulatory advantages, significantly deterring new entrants. Due to its specialized mandate of primarily financing the Ministry of Railways, IRFC benefits from exemptions, such as those related to credit concentration norms, not typically extended to other financial institutions.

A new entity attempting to enter this niche would face a substantial competitive disadvantage, lacking such favorable regulatory treatment. This privileged status, cemented by IRFC's long-standing role in national infrastructure financing, makes it exceptionally difficult for any challenger to replicate its operational framework or achieve similar cost efficiencies by 2024.

- IRFC's unique mandate simplifies regulatory compliance.

- Exemptions reduce capital requirements for IRFC compared to new players.

- New entrants face higher compliance costs and stricter lending limits.

- This creates a high barrier to entry for the railway financing sector.

IRFC's Unassailable Hold on Indian Railway Financing

The threat of new entrants in Indian railway financing remains extremely low. This is due to IRFC's unique government mandate, sovereign backing, and the immense capital required, exemplified by Indian Railways' 2024-25 capital outlay of ₹2.52 lakh crore. New players face insurmountable regulatory hurdles and an inability to replicate IRFC's low-cost funding, like its ₹32,500 crore borrowings in FY2023-24, or its established cost-plus model and asset base of ₹4,68,900 crore as of December 2023.

| Factor | IRFC Position (2024 Data) | Barrier to New Entrants |

|---|---|---|

| Capital Outlay | Indian Railways: ₹2.52 lakh crore (2024-25) | Immense; requires sovereign backing |

| Funding Access | ₹32,500 crore raised (FY2023-24) | Difficult to replicate low-cost, government-backed funds |

| Assets Under Management | ₹4,68,900 crore (Dec 31, 2023) | Massive scale; deep operational expertise required |

Porter's Five Forces Analysis Data Sources

Our Indian Railway Finance Porter's Five Forces analysis is built upon a foundation of official government reports, railway budget documents, financial statements of key players, and industry-specific publications. We also incorporate data from economic surveys and reports by financial institutions to provide a comprehensive view of the competitive landscape.