Hanwha Solutions Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Hanwha Solutions Bundle

A Must-Have Tool for Decision-Makers

Hanwha Solutions faces a dynamic competitive landscape, with significant pressure from rivals in the solar and chemical sectors. The threat of new entrants is moderate, as high capital requirements can be a barrier, but technological advancements can lower these. Buyer power is substantial, particularly for large industrial clients who can negotiate favorable terms.

The bargaining power of suppliers varies, with some raw materials being more commoditized than others, impacting Hanwha's cost structure. The threat of substitutes is a growing concern, especially as alternative energy sources and materials evolve. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hanwha Solutions’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Dependency

Hanwha Solutions, particularly its chemical segment, has a significant reliance on basic petrochemicals and other essential raw materials. This dependence makes the company vulnerable to price volatility and potential supply chain interruptions. For instance, abnormal climate events in regions where these raw materials are sourced pose a tangible risk, as noted in their sustainability reporting, directly impacting operational stability and cost structures.

Vertical Integration in Solar

Hanwha Qcells is making significant strides in vertical integration within the solar supply chain, a move that directly impacts the bargaining power of suppliers. By becoming the sole North American entity capable of producing all essential solar components, from ingots and wafers to fully assembled modules, Hanwha Qcells is effectively insulating itself from external supply pressures.

This comprehensive in-house manufacturing capability dramatically reduces Hanwha Qcells' dependence on third-party suppliers for critical materials. For instance, in 2023, the global solar wafer market experienced price volatility due to supply chain disruptions, highlighting the strategic advantage of Hanwha's integrated model. By controlling these upstream processes, the company can better manage costs and ensure a consistent supply of raw materials.

The ability to produce ingots and wafers internally means Hanwha Qcells is not subject to the pricing dictates of external wafer manufacturers. This is particularly important as the cost of polysilicon, the primary raw material for wafers, can fluctuate significantly. By internalizing production, Hanwha Qcells mitigates the risk of being held hostage by supplier price increases, thereby strengthening its competitive position.

Furthermore, this deep integration allows for greater quality control and customization throughout the production process. Hanwha Qcells can fine-tune its wafer production to optimize performance in its modules, a benefit not readily available when relying on external suppliers who may have different specifications or quality standards. This internal control diminishes the bargaining power that suppliers of raw silicon or processed wafers would otherwise wield.

Geopolitical and Trade Policies

Geopolitical shifts and evolving trade policies significantly impact supplier bargaining power. For instance, tariffs imposed on key raw materials, like those seen in recent global trade disputes, directly increase production costs for chemical manufacturers. This means suppliers can leverage these external pressures to demand higher prices from companies such as Hanwha Solutions.

In 2024, the specter of trade protectionism continued to loom, with various nations exploring or implementing tariffs on critical inputs. For example, increased tariffs on petrochemical feedstocks could force chemical producers to absorb these costs or pass them on, directly affecting Hanwha Solutions' profitability and potentially strengthening the hand of their raw material suppliers.

Supplier Diversity and Relationship Management

Hanwha Solutions actively seeks to broaden its supplier network for crucial inputs like raw materials, equipment, and packaging across its chemical and solar energy sectors. This proactive diversification directly counters the leverage individual suppliers might hold. By engaging with a wider range of vendors, Hanwha Solutions can foster competition and secure more favorable terms.

This strategy is particularly vital in industries prone to supply chain disruptions. For instance, in 2023, the global polysilicon market, a key component for solar panels, experienced price volatility due to production constraints in certain regions. Hanwha Solutions' emphasis on supplier diversity helps buffer against such market shocks.

- Diversified Sourcing: Hanwha Solutions encourages proposals from new companies to supply chemicals, components, and packaging, thereby reducing reliance on any single entity.

- Mitigating Supplier Power: A broader supplier base limits the ability of any one supplier to dictate terms or prices, enhancing Hanwha’s negotiating position.

- Supply Chain Resilience: This approach bolsters the company's ability to navigate potential supply shortages or price hikes, as seen in volatile raw material markets.

- Competitive Advantage: By fostering competition among suppliers, Hanwha Solutions can achieve cost efficiencies and ensure consistent availability of essential materials.

ESG in Supply Chain

Hanwha Solutions prioritizes Environmental, Social, and Governance (ESG) principles within its supply chain. This commitment involves meticulous monitoring of raw material supply and implementing responsible sourcing practices to mitigate potential disruptions. For instance, in 2024, Hanwha Solutions reported a significant portion of its key suppliers undergoing ESG assessments, aiming to build more resilient and sustainable partnerships.

This ESG focus directly impacts the bargaining power of suppliers. By emphasizing sustainability and ethical sourcing, Hanwha Solutions can exert influence over its supplier base, potentially shifting the balance of power. Suppliers who align with these ESG standards are more likely to secure long-term contracts and preferred status. Conversely, suppliers failing to meet these criteria may face reduced business opportunities.

- ESG Integration: Hanwha Solutions' active integration of ESG criteria into supplier selection and management strengthens its position.

- Supplier Compliance: Suppliers demonstrating strong ESG performance, such as reduced carbon emissions or fair labor practices, gain leverage.

- Risk Mitigation: Proactive monitoring of supply chain ESG factors in 2024 allowed Hanwha to identify and address potential risks early.

- Sustainable Partnerships: The emphasis on long-term, sustainable relationships empowers Hanwha to negotiate more favorable terms with compliant suppliers.

Supplier Power: Chemical Dependence vs. Solar Integration

The bargaining power of suppliers for Hanwha Solutions is a critical factor, particularly for its chemical division which relies heavily on basic petrochemicals. Fluctuations in raw material prices, exacerbated by events like abnormal climate patterns in sourcing regions, directly impact Hanwha's operational stability and cost structure. For example, in 2024, global trade disputes and protectionist policies led to increased tariffs on key petrochemical feedstocks, potentially strengthening suppliers' ability to demand higher prices.

Hanwha Qcells' vertical integration in the solar supply chain significantly mitigates supplier power. By producing essential components like ingots and wafers internally, the company reduces its dependence on external manufacturers. This strategy proved beneficial in 2023 when the solar wafer market experienced price volatility due to supply chain disruptions, allowing Hanwha to better manage costs and ensure material availability. Their commitment to ESG principles also influences supplier relationships, with compliant suppliers gaining preferred status.

| Factor | Impact on Hanwha Solutions | 2023-2024 Trend/Example |

|---|---|---|

| Raw Material Dependence (Chemicals) | Vulnerability to price volatility and supply disruptions | Increased tariffs on petrochemical feedstocks in 2024 due to trade policies |

| Vertical Integration (Solar) | Reduced reliance on external suppliers for critical components | Internal wafer production insulated Qcells from 2023 market volatility |

| Supplier Diversification | Fosters competition and secures favorable terms | Broadening vendor network to buffer against polysilicon market shocks |

| ESG Compliance | Strengthens negotiation leverage with compliant suppliers | Key suppliers undergoing ESG assessments in 2024 for resilient partnerships |

What is included in the product

This analysis details the competitive forces impacting Hanwha Solutions, including the threat of new entrants, bargaining power of buyers and suppliers, and the threat of substitutes, all within the context of the global chemical and renewable energy industries.

Quickly identify and mitigate threats from new entrants and substitutes with a clear, actionable overview of competitive pressures.

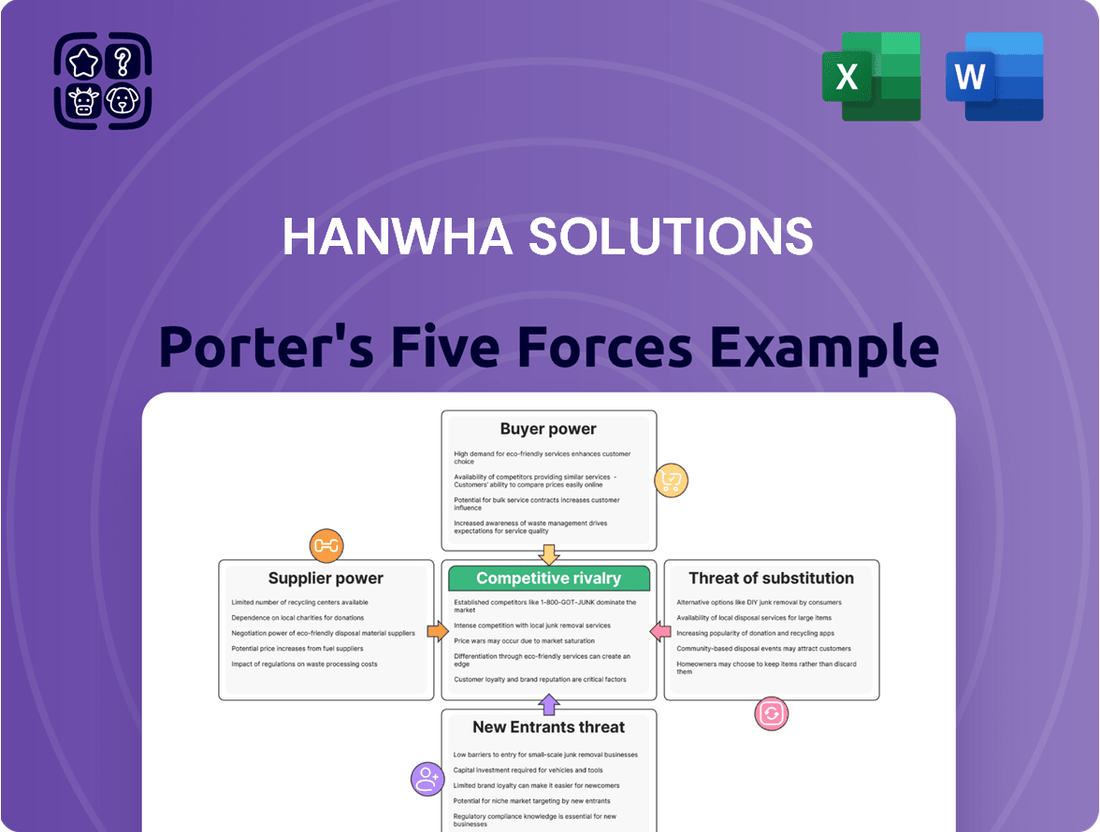

Customers Bargaining Power

Diverse Customer Base

Hanwha Solutions' diverse customer base significantly tempers the bargaining power of its clients. By supplying essential chemical, advanced materials, and renewable energy products to a broad spectrum of industries, including construction, automotive, and electronics, the company mitigates reliance on any single sector.

Price Sensitivity in Commodity Markets

In the competitive landscape of basic petrochemicals and high-performance plastics, Hanwha Solutions encounters significant customer price sensitivity. Many customers operate in markets where they too face intense competition, making them highly attuned to price fluctuations. This forces Hanwha Solutions to carefully manage its pricing strategies to remain competitive while protecting its market share. For instance, the global polyethylene market, a key area for petrochemical producers, saw average prices fluctuate significantly in 2024 due to supply-demand dynamics and feedstock costs, directly impacting customer purchasing decisions.

Demand for Sustainable Solutions

Customers are increasingly vocal about their desire for eco-friendly products. This growing demand for sustainability gives them significant leverage, pushing companies like Hanwha Solutions to innovate with greener materials and processes. For instance, a 2024 survey indicated that over 60% of consumers are willing to pay a premium for products with a lower environmental footprint.

This shift in consumer preference directly impacts Hanwha Solutions' product development and sales strategies. When customers prioritize environmental impact, they gain bargaining power by choosing suppliers who align with their values. This trend is particularly strong in sectors where Hanwha Solutions operates, such as solar energy and advanced materials.

Residential Solar Market Dynamics

Customers in the residential solar market are showing a growing preference for comprehensive energy solutions. This includes not just solar panels but also integrated systems like home batteries and electric vehicle (EV) charging stations. This shift signifies a demand for more than just electricity generation; it’s about holistic home energy management.

Hanwha's strategic alliance with LG exemplifies this trend. By partnering, they are developing bundled solar energy packages designed to directly address these evolving customer needs. This collaboration is crucial for staying competitive in a market where customers expect seamless integration of various energy technologies.

- Demand for Integrated Solutions: Residential customers are increasingly seeking combined offerings of solar panels, energy storage (batteries), and EV charging infrastructure.

- Hanwha-LG Partnership: Hanwha Solutions has partnered with LG to provide these bundled solar energy packages, directly responding to customer desire for integrated systems.

- Market Responsiveness: This partnership demonstrates Hanwha's strategy to enhance its competitive position by aligning its product offerings with the evolving preferences of the residential solar market.

Utility and Commercial Scale Buyers

Utility and commercial-scale buyers, particularly those in the solar energy sector and industrial chemical markets, wield considerable bargaining power. This is primarily driven by the sheer volume of their purchases, which can significantly impact a supplier's revenue. For instance, Hanwha Qcells' strategic emphasis on utility-scale solar projects means that securing contracts with large utility companies is crucial for their growth. These major buyers can often negotiate favorable pricing and terms due to their substantial order sizes.

The concentration of buyers within these large-scale segments further amplifies their influence. A few key utility providers or industrial conglomerates might represent a substantial portion of a company's customer base. This situation allows them to exert pressure on pricing and product specifications. In 2023, global utility-scale solar project installations reached record levels, indicating the sustained demand from these large-scale buyers and their continued importance in the market landscape.

- Significant Volume Purchasing: Large buyers like utility companies can order megawatts of solar modules or tons of chemicals, giving them leverage.

- Concentration of Buyers: In certain industrial sectors, a limited number of large customers may account for a significant percentage of a supplier's sales.

- Price Sensitivity: For massive projects, even small price reductions per unit translate into substantial cost savings, making price a key negotiation point.

- Potential for Backward Integration: Very large customers could theoretically consider producing their own components if supplier terms become unfavorable.

Customer Power: Shaping Hanwha's Solar & Chemical Future

Hanwha Solutions faces moderate bargaining power from its customers, influenced by product differentiation, switching costs, and the availability of substitutes. While the company serves diverse markets, price sensitivity in basic chemicals and the demand for integrated solutions in solar energy are key drivers of customer leverage. For instance, in 2024, the fluctuating prices of petrochemical feedstocks directly impacted customer cost considerations, increasing their negotiation power.

In the solar sector, customers are increasingly demanding comprehensive energy solutions that combine panels, storage, and EV charging. Hanwha's partnership with LG to offer these bundled packages directly addresses this trend, aiming to lock in customers and reduce their incentive to switch. However, the broader availability of solar components means that for standalone panel purchases, customer bargaining power remains significant, particularly for large-scale buyers who can negotiate on volume.

| Customer Segment | Key Drivers of Bargaining Power | Impact on Hanwha Solutions |

|---|---|---|

| Residential Solar | Demand for integrated solutions (storage, EV charging), Growing preference for eco-friendly products | Requires product innovation and bundled offerings; Moderate price sensitivity for integrated systems. |

| Industrial Chemicals/Petrochemicals | Price sensitivity due to competitive markets, Feedstock cost fluctuations | High price sensitivity, Requires competitive pricing strategies; Significant leverage for large volume buyers. |

| Utility-Scale Solar | High purchase volume, Concentration of buyers | Significant leverage on pricing and terms; Essential for securing large contracts. |

What You See Is What You Get

Hanwha Solutions Porter's Five Forces Analysis

This preview showcases the complete Hanwha Solutions Porter's Five Forces Analysis, offering a detailed examination of competitive forces impacting the company.

The document you see here is the exact, professionally crafted analysis you'll receive immediately after purchase, providing actionable insights into Hanwha Solutions' strategic landscape.

You are previewing the final, ready-to-use document; what you see is precisely what you'll be able to download and utilize instantly after completing your purchase.

No placeholders or samples—the comprehensive Porter's Five Forces Analysis for Hanwha Solutions displayed here is the actual file you'll gain access to upon payment.

Rivalry Among Competitors

Global Competitors in Solar

Hanwha Qcells operates in a highly competitive global solar photovoltaic (PV) module manufacturing market. Companies like JinkoSolar, LONGi Green Energy, JA Solar, and Trina Solar are major players, constantly pushing for market share through innovation and aggressive pricing strategies.

In 2023, the global solar PV market saw significant growth, with China continuing to dominate module production. For instance, LONGi Green Energy reported substantial revenue increases, underscoring the intense competition. This dynamic landscape means Qcells must continually invest in research and development to maintain its edge.

The sheer volume of production by these global competitors, particularly those based in Asia, creates downward pressure on prices. This means that for Hanwha Qcells, maintaining profitability requires not only technological advancement but also efficient supply chain management and cost optimization to compete effectively against rivals with potentially lower production costs.

Chemical Industry Rivals

In the chemical sector, Hanwha Solutions faces intense rivalry from major global and regional players. Key competitors include TotalEnergies Petrochemicals & Refining, LG Chem, Lotte Chemical, and SK Innovation, all of which possess significant market share and resources.

The competitive landscape is further intensified by inherent industry characteristics. High energy costs, crucial for chemical production, and stringent regulatory burdens, often related to environmental standards, create substantial operating challenges and increase the pressure on companies like Hanwha Solutions.

For instance, in 2023, the global chemical industry saw mixed performance, with some segments experiencing demand fluctuations. Companies with integrated value chains and strong cost management, like those in Hanwha Solutions' peer group, were better positioned to navigate these market dynamics.

Price Competition and Overcapacity

The solar and battery manufacturing sectors have experienced substantial investment, particularly in China, resulting in considerable global overcapacity. This has led to a sharp decline in prices across these industries, creating a highly competitive pricing landscape. For Hanwha Solutions, this means constant pressure to maintain profitability amidst falling market prices, directly impacting its revenue streams.

Technological Innovation as a Differentiator

Hanwha Solutions leverages technological innovation as a key differentiator, notably through its advancements in solar energy. The company is pushing the boundaries with technologies like perovskite-silicon tandem cells, aiming to significantly boost solar module efficiency. This focus on cutting-edge R&D is vital for staying ahead in a rapidly evolving market.

Hanwha Solutions' commitment to innovation extends to developing eco-friendly products across its business segments. This strategic emphasis on sustainability and technological leadership helps create unique value propositions. The company's investment in research and development is a continuous effort to maintain and strengthen its competitive position.

- Perovskite-Silicon Tandem Cells: Aiming for higher energy conversion rates, potentially exceeding 30% efficiency, a significant leap from current silicon-only technologies.

- Eco-Friendly Product Development: Expanding offerings in areas like advanced materials for sustainable packaging and construction, responding to growing market demand.

- R&D Investment: Hanwha Solutions consistently allocates substantial resources to its research and development efforts, crucial for driving future growth and competitive advantage.

Regional Market Focus and Vertical Integration

Hanwha Qcells is strategically focusing on the U.S. market by building a comprehensive, locally integrated solar manufacturing operation. This move is designed to capitalize on government incentives, such as those provided by the Inflation Reduction Act (IRA), which offers significant tax credits for domestic solar production.

By controlling more of its supply chain within the U.S., Hanwha Qcells aims to mitigate the cost advantages of inexpensive solar panel imports, particularly from China. This vertical integration is a direct response to intense competitive rivalry, allowing them to offer more competitive pricing and secure market share.

- U.S. Manufacturing Expansion: Hanwha Qcells announced plans to invest billions in U.S. solar manufacturing, aiming for a complete local value chain.

- Leveraging Subsidies: The company is positioned to benefit significantly from the U.S. Inflation Reduction Act, enhancing its cost competitiveness.

- Countering Chinese Imports: This regional strategy directly addresses the challenge posed by lower-cost Chinese solar products in the U.S. market.

- Strengthened Competitive Position: By integrating its operations, Hanwha Qcells can improve efficiency and responsiveness to market demands.

Intense market rivalry shapes strategic focus

Competitive rivalry is extremely high across all of Hanwha Solutions' key business segments, including solar, chemicals, and advanced materials. In the solar market, major global players like JinkoSolar and LONGi Green Energy continually drive down prices through massive production volumes and technological innovation, creating intense pressure on Hanwha Qcells.

The chemical sector also sees fierce competition from established giants such as LG Chem and Lotte Chemical, where market share is fiercely contested. This intense rivalry necessitates continuous investment in R&D and operational efficiency to maintain profitability and market position.

Hanwha Solutions is actively mitigating this rivalry by focusing on technological differentiation, such as its perovskite-silicon tandem solar cells, and by strategically building out its U.S. manufacturing base to leverage incentives and counter lower-cost imports.

| Segment | Key Competitors | Competitive Pressure Factors |

|---|---|---|

| Solar PV | JinkoSolar, LONGi Green Energy, JA Solar, Trina Solar | Price competition, technological advancements, production capacity, import competition |

| Chemicals | LG Chem, Lotte Chemical, SK Innovation, TotalEnergies | Market share, cost of production, regulatory environment, product innovation |

| Advanced Materials | Various specialized global and regional players | Technological sophistication, customization capabilities, sustainability demands |

SSubstitutes Threaten

Alternative Energy Sources

While solar energy is a rapidly expanding sector, other renewable energy sources pose a threat of substitution for Hanwha Solutions. Wind power, for instance, is a mature renewable technology that competes directly for market share in many regions. Global wind power capacity reached approximately 1,063 GW by the end of 2023, presenting a significant alternative for electricity generation.

Furthermore, advancements in energy storage solutions, such as battery technology, can act as both substitutes and complementary technologies. Improved storage can make intermittent renewables like solar and wind more reliable, but also allows for greater integration of diverse energy sources, potentially diluting the market dominance of any single technology. The global energy storage market was valued at over $200 billion in 2023, highlighting the rapid development and adoption of these alternatives.

Next-Generation Solar Technologies

Innovations within the solar industry itself, like thin-film, organic photovoltaics (OPV), and ferroelectric cells, offer alternatives to conventional silicon panels. These advancements strive for improved efficiency or reduced manufacturing costs, directly impacting the competitive landscape for Hanwha Solutions.

For instance, advancements in perovskite solar cells, a type of thin-film technology, have shown promising efficiency gains, with lab efficiencies exceeding 25% by early 2024, potentially challenging the dominance of silicon. This continuous innovation from within the sector itself creates a significant threat of substitutes.

Bio-based and Recycled Material Alternatives for Plastics

The rising availability of bio-based and recycled materials presents a significant threat of substitution for traditional plastics. Consumers and industries are increasingly prioritizing sustainability, driving demand for alternatives like plant-based packaging, mushroom mycelium, and seaweed-derived materials. For instance, the global bioplastics market was valued at approximately USD 12.0 billion in 2023 and is projected to reach USD 35.5 billion by 2030, indicating strong growth and a direct challenge to conventional plastic usage.

Energy Efficiency and Conservation

Improvements in energy efficiency and a growing emphasis on conservation can significantly reduce the demand for energy. This indirectly acts as a substitute for new energy generation sources, including solar installations, and also lessens the need for energy-intensive chemical products that Hanwha Solutions may produce. For instance, advancements in building insulation and smart grid technologies deployed in 2024 are making energy consumption more efficient, thereby dampening the growth potential for traditional energy suppliers.

The threat of substitutes from energy efficiency is elevated by consumer and corporate commitment to sustainability. Many businesses are setting ambitious energy reduction targets. For example, in 2024, major corporations across various sectors announced plans to cut their energy usage by an average of 15% by 2030, directly impacting overall energy demand.

- Reduced Demand: Energy efficiency measures can lessen the overall need for new energy infrastructure, including solar farms.

- Technological Advancements: Innovations in insulation, smart appliances, and energy management systems make existing energy go further.

- Policy Support: Government incentives and regulations promoting energy conservation further strengthen this substitute threat.

- Consumer Behavior: Increased awareness and adoption of energy-saving practices by individuals contribute to lower overall energy consumption.

Shift to Circular Economy Models

The growing global momentum towards circular economy models presents a significant threat of substitutes for Hanwha Solutions. As societies increasingly prioritize waste reduction and resource efficiency, the demand for virgin petrochemicals and plastics, core products for Hanwha Solutions, is likely to diminish.

This shift encourages the use of recycled materials and bio-based alternatives, directly impacting the market share of traditional chemical products. Hanwha Solutions is proactively addressing this by investing in eco-friendly initiatives, such as developing products derived from renewable carbon resources, aiming to align with and benefit from this evolving economic paradigm.

- Circular Economy Growth: The global circular economy market was valued at approximately $238.3 billion in 2023 and is projected to reach $820.2 billion by 2030, indicating substantial growth and a potential reduction in demand for virgin materials.

- Hanwha's Eco-Initiatives: Hanwha Solutions has announced plans to increase its investment in sustainable businesses, including the development of advanced recycled plastics and bio-plastics, signaling a strategic response to the threat of substitutes.

- Consumer Preference Shift: Surveys in 2024 show a growing consumer preference for products made from recycled or sustainable materials, which could directly impact purchasing decisions away from petrochemical-based goods.

Renewable Energy: Exploring Solar's Diverse Alternatives

Beyond solar and wind, other renewable sources like geothermal and hydropower also represent potential substitutes, especially in regions with favorable geological or hydrological conditions. While Hanwha Solutions primarily focuses on solar, these alternatives can capture market share for electricity generation, indirectly impacting the demand for solar installations.

| Energy Source | Global Capacity (approx. end of 2023) | Key Characteristic |

|---|---|---|

| Wind Power | 1,063 GW | Mature technology, direct competitor for electricity generation. |

| Geothermal Power | 17.1 GW (as of 2023) | Reliable baseload power, geographically dependent. |

| Hydropower | 1,330 GW (as of 2023) | Established renewable, significant baseload capacity. |

Entrants Threaten

High Capital Investment

Entering the chemical and solar manufacturing sectors, where Hanwha Solutions operates, demands immense capital. New players must fund the construction of advanced manufacturing facilities, invest heavily in research and development for cutting-edge technologies, and build robust, reliable supply chains. For instance, Hanwha Solutions' commitment to its U.S. solar manufacturing complex, a multi-billion dollar project, underscores this significant financial barrier to entry.

Technological Complexity and R&D

The high technological complexity and ongoing research and development (R&D) requirements in advanced materials and renewable energy create a significant barrier for new entrants wanting to compete with established players like Hanwha Solutions. Developing cutting-edge technologies or acquiring necessary intellectual property demands substantial upfront investment and specialized knowledge.

For instance, the solar photovoltaic industry, a key area for Hanwha Solutions, requires continuous innovation in cell efficiency and material science. Companies entering this space must either invest heavily in R&D to match or surpass existing technological capabilities, or acquire firms with established patents and expertise. This steep learning curve and the need for sustained innovation deter many potential new competitors.

Regulatory Hurdles and Policy Landscape

The chemical and solar sectors face a labyrinth of intricate and ever-changing regulations. These include stringent environmental standards, lengthy permitting procedures, and trade policies such as tariffs, which can significantly deter new entrants. For instance, in 2024, many countries continued to implement or adjust carbon pricing mechanisms and renewable energy mandates, adding layers of complexity for any newcomer aiming to establish operations.

Established Supply Chains and Distribution Networks

Established supply chains and distribution networks present a significant barrier for new entrants aiming to compete with established players like Hanwha Solutions. Hanwha Solutions, for instance, has cultivated deep, long-standing relationships with its key suppliers and maintains a vast, efficient distribution infrastructure across global markets. This intricate web of connections allows for reliable sourcing of raw materials and timely delivery of finished products, contributing to cost efficiencies and market responsiveness.

For a new company to replicate this level of operational sophistication, it would require substantial upfront investment in building similar supplier partnerships and establishing a widespread distribution system. The time and capital needed to create these foundational elements are considerable, making it a daunting challenge for newcomers. For example, establishing a global logistics network can take years and involve millions in infrastructure and partnership development. This inherent advantage for incumbents significantly dampens the threat of new entrants.

- Supplier Relationships: Hanwha Solutions benefits from established, often exclusive, contracts with key raw material providers, securing supply and potentially better pricing.

- Distribution Reach: Access to established logistics, warehousing, and retail channels globally provides immediate market penetration for existing firms.

- Cost of Replication: New entrants face high capital expenditures and operational hurdles to build comparable supply chain and distribution capabilities.

- Market Access: Existing networks facilitate faster and more cost-effective product delivery, giving incumbents a competitive edge in reaching customers.

Brand Recognition and Customer Trust

Hanwha Solutions, particularly through its Hanwha Qcells brand, has cultivated significant brand recognition and deep customer trust across its various business segments. This established reputation acts as a formidable barrier. Newcomers would face the substantial challenge of matching this level of market penetration and consumer confidence.

To effectively compete, potential new entrants would need to commit substantial financial resources to marketing campaigns and reputation-building initiatives. For instance, in the solar energy sector where Qcells is a major player, brand loyalty is often tied to long-term performance and warranty assurances. In 2023, Hanwha Qcells reported significant growth, indicating the strength of its market position and brand appeal.

- Brand Equity: Hanwha Solutions benefits from strong brand equity built over years of consistent product quality and market presence.

- Customer Loyalty: Established trust translates into customer loyalty, making it harder for new brands to attract and retain customers.

- Marketing Investment: New entrants must anticipate significant marketing expenditure to even begin building brand awareness comparable to Hanwha Solutions.

- Market Penetration: Replicating Hanwha's existing market penetration would require extensive distribution networks and sales efforts.

Market Entry Hurdles Shield Hanwha Solutions

The threat of new entrants into Hanwha Solutions' chemical and solar markets is generally low due to substantial barriers. High capital requirements for advanced manufacturing facilities and R&D, coupled with complex technological needs, demand significant upfront investment. For example, Hanwha Solutions' multi-billion dollar U.S. solar manufacturing complex exemplifies the scale of investment required. Furthermore, navigating stringent, evolving regulations in 2024, including carbon pricing and renewable energy mandates, adds further complexity for potential newcomers.

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Hanwha Solutions is built upon a foundation of verified data, including the company's annual reports, investor presentations, and regulatory filings. This is further enriched by insights from reputable industry research firms and global economic databases to provide a comprehensive view of the competitive landscape.