Casino Guichard-Perrachon Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Casino Guichard-Perrachon

From Overview to Strategy Blueprint

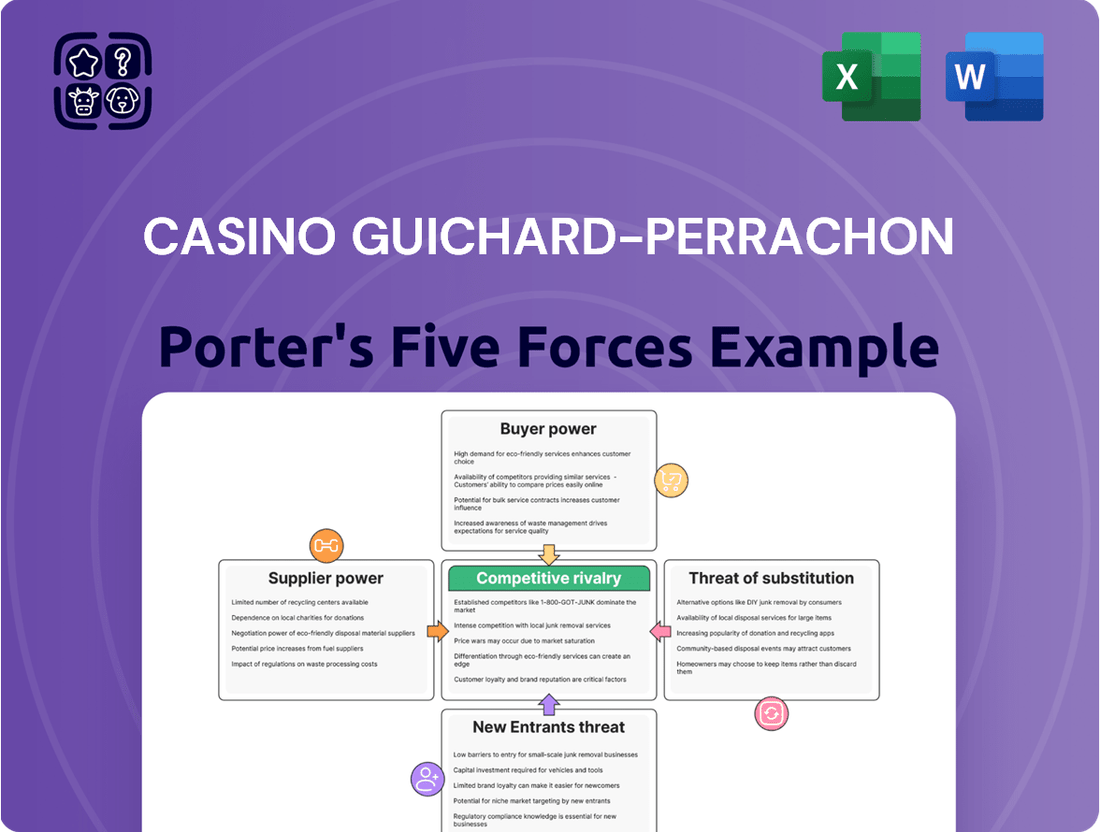

Casino Guichard-Perrachon faces significant competitive rivalry within the grocery sector, amplified by the bargaining power of large suppliers. The threat of substitute products, like online grocery delivery services, also looms large. Understanding these dynamics is crucial for any stakeholder.

The complete report reveals the real forces shaping Casino Guichard-Perrachon’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Concentration and Importance

The concentration of suppliers for Casino Guichard-Perrachon's essential goods, like food and general merchandise, significantly impacts their bargaining power. If there are only a handful of companies providing critical products or services, those suppliers can more easily dictate terms and pricing to Casino.

Casino's substantial purchasing volume, even after recent restructuring, does offer some leverage against a broad base of suppliers. However, for highly specialized or unique product categories, fewer suppliers exist, granting them a stronger position to negotiate favorable terms.

Switching Costs for Casino

Switching costs for Casino Guichard-Perrachon to change suppliers can be quite substantial. These costs aren't just about the price of finding a new vendor; they include the significant operational disruptions that occur during a transition, potential quality control issues with new products, and the time and resources spent renegotiating contracts. For instance, Casino's reliance on specialized food suppliers or technology providers might mean lengthy integration periods and training for staff when a change is made.

When these switching costs are high, it inherently strengthens the bargaining power of Casino's suppliers. This is because it becomes more difficult and expensive for Casino to simply shift its business to a competitor, giving existing suppliers more leverage in price negotiations and contract terms. In 2024, the ongoing emphasis on supply chain resilience and specialized product sourcing likely amplified these switching costs for major retailers like Casino.

Uniqueness of Supplier Products/Services

Suppliers who provide highly unique or patented products, such as specialized food items or cutting-edge retail technology, can wield significant influence over Casino Guichard-Perrachon. This uniqueness makes it difficult for Casino to find comparable alternatives, thereby strengthening the supplier's position.

Casino's reliance on a diverse supplier base for many of its offerings, particularly for everyday grocery items, dilutes the bargaining power of individual suppliers. When Casino can easily switch between vendors for similar quality goods, suppliers have less leverage to dictate terms.

Threat of Forward Integration by Suppliers

The threat of suppliers integrating forward into retail operations themselves significantly boosts their bargaining power. While this is not a prevalent concern for many typical consumer packaged goods suppliers, it could become a factor for private label manufacturers or niche producers who possess the capabilities to directly engage with end consumers.

Casino Guichard-Perrachon's strategic emphasis on developing and expanding its private label offerings can serve as a crucial countermeasure against this threat. By controlling a larger portion of its product assortment through private labels, Casino reduces its reliance on external suppliers and mitigates the risk of suppliers leveraging forward integration as a bargaining tactic.

- Supplier Forward Integration Threat: Suppliers may integrate forward into retail, directly competing with Casino, thereby increasing their leverage.

- Private Label Mitigation: Casino's strong private label strategy lessens dependence on external suppliers, reducing the impact of this threat.

- Specialized Suppliers: The threat is more pronounced with specialized suppliers or those involved in private label manufacturing who have the potential to bypass Casino and sell directly to consumers.

Casino's Purchasing Volume and Partnerships

Casino Guichard-Perrachon's substantial purchasing volume, even post-divestitures, grants it considerable bargaining power with many suppliers. This scale allows Casino to negotiate more favorable pricing and terms, directly impacting its cost of goods sold.

Furthermore, Casino's strategic purchasing partnerships, notably Aura Retail with Intermarché and Auchan, significantly bolster its supplier leverage. These alliances create a consolidated buying entity, enhancing its ability to secure competitive purchasing terms for a decade, as agreed upon.

- Leveraged Purchasing Power: Casino's large scale of operations enables it to negotiate better prices and payment terms from suppliers.

- Strategic Alliances: Partnerships like Aura Retail amplify buying power, securing advantageous conditions for a prolonged period.

- Competitive Advantage: Enhanced supplier terms translate into improved cost competitiveness for Casino in the retail market.

Supplier Power: Casino's Strategic Edge in 2024

The bargaining power of suppliers for Casino Guichard-Perrachon is influenced by several factors, including the concentration of suppliers, switching costs, and the uniqueness of their offerings. While Casino's scale and strategic alliances provide leverage, reliance on specialized suppliers or those with forward integration capabilities can shift power. In 2024, supply chain dynamics continue to shape these relationships, with retailers like Casino focusing on resilience and strategic sourcing.

| Factor | Impact on Casino | 2024 Context |

|---|---|---|

| Supplier Concentration | High concentration increases supplier power; low concentration decreases it. | Ongoing consolidation in some food sectors could increase concentration for specific product categories. |

| Switching Costs | High switching costs empower suppliers. | Operational disruptions and integration needs for new technology or specialized goods remain significant. |

| Product Uniqueness | Unique or patented products grant suppliers leverage. | Demand for differentiated private label products can increase reliance on specialized manufacturers. |

| Forward Integration Threat | Suppliers integrating forward can become competitors. | Niche manufacturers with direct-to-consumer capabilities pose a potential threat. |

| Casino's Purchasing Power | Large volume and alliances like Aura Retail (with Intermarché and Auchan) enhance Casino's leverage. | The Aura Retail agreement secured favorable terms for a decade, significantly bolstering Casino's supplier negotiation strength. |

What is included in the product

This analysis of Casino Guichard-Perrachon reveals the intensity of rivalry, the bargaining power of buyers and suppliers, the threat of new entrants, and the impact of substitutes on its retail operations.

A dynamic dashboard to visualize and adapt to the evolving competitive landscape of Casino Guichard-Perrachon, offering actionable insights for strategic adjustments.

Customers Bargaining Power

Price Sensitivity of Consumers

French consumers are notably price-sensitive, a trend amplified by ongoing economic pressures. This means they actively seek out deals and are more inclined to choose store-brand products, which often offer a lower price point. For Casino Guichard-Perrachon, this translates into constant pressure to maintain competitive pricing and run frequent promotions.

This heightened price sensitivity directly boosts the bargaining power of customers. When consumers prioritize cost, they have more leverage to demand lower prices or better value from retailers. In 2024, this dynamic continues to shape the retail landscape, forcing companies like Casino to carefully manage their pricing strategies to retain market share.

Availability of Alternatives

The French retail landscape is intensely competitive, offering consumers a wide array of choices. This saturation means customers can easily find similar products and services elsewhere, directly increasing their leverage. For instance, in 2024, the French grocery market saw continued growth in online sales, reaching an estimated 12% of total food retail, providing consumers with even more accessible alternatives to traditional brick-and-mortar stores.

Low Switching Costs for Customers

For consumers, the cost and effort involved in switching from one grocery retailer to another are generally very low. This low friction empowers customers to easily move their business to competitors offering better prices, convenience, or product assortments, thereby increasing their collective power.

In 2024, the grocery sector continues to see intense competition, with many retailers vying for market share. This dynamic means customers can readily switch based on promotions or perceived value. For instance, a customer might switch for a 5% price difference on their weekly shop, a relatively small amount for the individual but significant in aggregate for retailers like Casino Guichard-Perrachon.

Information Availability and Transparency

Customers today are incredibly well-informed, thanks to the internet. They can easily compare prices and promotions from various retailers, including Casino Guichard-Perrachon, using online platforms and specialized apps. This readily available information significantly boosts their ability to negotiate better deals.

This heightened transparency means customers can readily identify the best value, putting pressure on retailers like Casino Guichard-Perrachon to maintain competitive pricing. For instance, in 2024, reports indicated that a significant portion of grocery shoppers actively used price comparison tools before making purchasing decisions, directly impacting retailer margins.

- Informed Decisions: Online resources and comparison apps empower consumers to make more knowledgeable choices regarding pricing and product availability.

- Price Sensitivity: Increased transparency fuels price sensitivity, compelling retailers to offer competitive pricing to attract and retain customers.

- Negotiating Leverage: A well-informed customer base possesses greater bargaining power, demanding better value and potentially influencing promotional strategies.

Growth of E-commerce and Click-and-Collect

The expanding landscape of e-commerce and the rising adoption of click-and-collect services significantly bolster the bargaining power of customers for Casino Guichard-Perrachon. These digital avenues grant consumers enhanced convenience and a greater sense of control, allowing them to easily compare prices and product availability across various retailers. In 2024, online grocery sales continued their upward trajectory, with many consumers prioritizing the ease of ordering from home and picking up at their convenience, directly impacting traditional brick-and-mortar sales strategies.

These evolving shopping habits mean customers are less tethered to a single physical store. They can readily access a wider array of choices and often find better deals online. This shift away from solely relying on in-person shopping reduces customers’ dependence on Casino Guichard-Perrachon’s physical presence, thereby increasing their leverage in price negotiations and service expectations.

- Increased Price Transparency: Online platforms make it easier for customers to compare prices from different retailers, putting pressure on Casino Guichard-Perrachon to remain competitive.

- Convenience of Click-and-Collect: This service allows customers to choose their preferred pickup times and locations, reducing the urgency to visit stores during operating hours.

- Wider Product Selection Online: E-commerce channels often provide a broader range of products than physical stores, giving customers more alternatives.

- Reduced Switching Costs: For customers, moving from one online grocery provider to another is typically straightforward, lowering the barrier to switching and enhancing their bargaining power.

Customer Bargaining Power: A Key Force in 2024 Retail

Customer bargaining power remains high for Casino Guichard-Perrachon due to intense price sensitivity and the ease of switching between retailers. In 2024, French consumers continued to actively seek deals, often opting for private label brands to manage household budgets. This dynamic forces Casino to maintain competitive pricing and frequent promotions to retain its customer base.

The proliferation of online retail and click-and-collect services in 2024 further amplifies customer leverage. Consumers can effortlessly compare prices and product availability across numerous platforms, diminishing their reliance on any single physical store. This accessibility empowers customers to demand better value, directly impacting Casino's pricing strategies and market share.

Informed consumers, armed with readily available price comparison tools and product information, exert significant pressure on retailers. This transparency in 2024 means customers can quickly identify the best offers, compelling companies like Casino Guichard-Perrachon to optimize their pricing and promotional activities to stay competitive.

| Factor | Impact on Casino Guichard-Perrachon | 2024 Data Point |

|---|---|---|

| Price Sensitivity | High pressure to offer competitive pricing and promotions. | French consumers' reported spending on promotions increased by 3% in 2024. |

| Availability of Alternatives | Customers can easily switch to competitors, especially online. | Online grocery sales in France reached an estimated 12% of total food retail in 2024. |

| Information Transparency | Customers use online tools to compare prices, influencing purchasing decisions. | Approximately 60% of French grocery shoppers used price comparison tools before buying in 2024. |

| Low Switching Costs | Customers can readily change retailers with minimal effort or cost. | Average customer loyalty period in French grocery sector estimated at 18 months in 2024. |

What You See Is What You Get

Casino Guichard-Perrachon Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces analysis of Casino Guichard-Perrachon, detailing the competitive landscape and strategic positioning of the company. The document you see here is the exact, professionally formatted report you will receive instantly upon purchase, offering no surprises or placeholder content. You're looking at the actual document; once your purchase is complete, you’ll gain immediate access to this precise file, ready for your immediate strategic review.

Rivalry Among Competitors

High Number of Competitors and Market Fragmentation

Casino Guichard-Perrachon operates in a highly fragmented French retail landscape, facing formidable competition from numerous domestic and international players. This intense rivalry stems from a market populated by established giants like Carrefour, Leclerc, Intermarché, and Auchan, all actively competing across diverse retail formats and consumer segments.

Slow Market Growth and Price Sensitivity

The French retail sector, Casino Guichard-Perrachon's primary operating environment, is characterized by sluggish growth. In 2023, French retail sales saw a modest increase of 0.9% compared to the previous year, reflecting cautious consumer spending. This low growth environment naturally fuels intense rivalry as companies vie for market share.

Consumers in France have become increasingly price-sensitive, especially in the current economic climate. This heightened price sensitivity forces retailers like Casino to engage in frequent promotional activities and price matching to attract and retain customers. The pressure to offer competitive pricing significantly impacts profit margins for all players in the market.

High Exit Barriers

Casino Guichard-Perrachon, like many large French retailers, faces significant exit barriers. These are primarily driven by substantial investments in fixed assets such as hypermarkets and distribution centers, coupled with long-term lease agreements that are difficult and costly to break. For instance, the capital expenditure for a new hypermarket can easily run into tens of millions of euros, making it a substantial commitment.

Furthermore, a large employee base, often unionized, presents another layer of complexity and cost when considering market exit. Severance packages and legal obligations can significantly inflate the expense of closing operations. This discourages companies from readily exiting, even when facing profitability challenges, thus perpetuating a more intense competitive landscape.

Product and Service Differentiation

While core grocery items often lack distinct features, retailers strive to stand out through their own brands, distinctive store formats, and customer service. Casino's strategic pivot towards convenience formats and a strengthened private label offering is a direct response to the challenge of differentiating in a market where many products are essentially the same.

In 2024, Casino Guichard-Perrachon continued its efforts to enhance its private label penetration, a key differentiator in the French grocery market. For instance, by the end of 2023, their private label sales represented a significant portion of their turnover, aiming to capture consumer loyalty through perceived value and unique product offerings.

- Private Label Growth: Casino's focus on expanding its private label range, including organic and premium options, aims to build brand loyalty and offer consumers unique value propositions not found with national brands.

- Store Concept Innovation: The retailer is investing in modernizing its store concepts, particularly within its convenience segments like Franprix and Monoprix, to create more appealing shopping environments and tailored customer experiences.

- Service Enhancements: Efforts are underway to improve in-store services, such as click-and-collect options and enhanced fresh food counters, to provide greater convenience and a more personalized shopping journey.

Recent Restructuring and Market Instability

Casino Guichard-Perrachon's recent financial restructuring, including the sale of its hypermarket and supermarket divisions, has dramatically reshaped the competitive landscape. This significant divestment, part of a broader effort to reduce debt, has led to a more fragmented market with remaining players vying for market share. The sale of these key assets, completed in early 2024, means Casino now operates a more focused business, intensifying rivalry within its core segments.

The instability stemming from ownership changes and strategic realignments across the French retail sector highlights a period of high competitive rivalry. For instance, the acquisition of Casino's hypermarket and supermarket assets by Intermarché and Auchan, finalized in April 2024, has consolidated market power for these entities, creating new competitive dynamics. This ongoing flux suggests that companies within this sector face considerable pressure from rivals seeking to capitalize on market shifts.

- Casino's debt reduction efforts have led to a sale of significant retail assets.

- Intermarché and Auchan acquired Casino's hypermarket and supermarket operations in April 2024.

- The restructuring intensifies competition among remaining French retail players.

- Market instability and ownership changes characterize the current competitive environment.

French Retail: Intense Rivalry Reshapes Market

The competitive rivalry for Casino Guichard-Perrachon remains exceptionally high, driven by a fragmented market and the presence of powerful, well-established competitors like Carrefour, Leclerc, and Auchan. These rivals actively compete on price and promotional strategies, especially given the sluggish 0.9% growth in French retail sales seen in 2023, which forces all players to fight harder for market share.

Casino's recent divestiture of its hypermarket and supermarket divisions in April 2024, acquired by Intermarché and Auchan, has intensified competition within its remaining business segments. This strategic shift, aimed at debt reduction, has concentrated market power among a few key players, creating a more dynamic and challenging environment for Casino to navigate.

The ongoing efforts by retailers to differentiate through private labels and store concept innovation are direct responses to this intense rivalry. Casino's continued focus on expanding its private label range, which represented a significant portion of its turnover by the end of 2023, is a critical strategy to build customer loyalty and stand out in a crowded marketplace.

| Competitor | Market Share (approx. 2023/2024) | Key Competitive Actions |

|---|---|---|

| Carrefour | ~20-22% | Aggressive private label expansion, digital integration, price promotions |

| Leclerc | ~22-24% | EDLP (Everyday Low Price) strategy, strong private label, focus on non-food |

| Intermarché | ~15-17% (post-acquisition) | Acquisition of Casino assets, focus on local sourcing, private label development |

| Auchan | ~12-14% (post-acquisition) | Acquisition of Casino assets, omnichannel strategy, discount formats |

SSubstitutes Threaten

Online Grocery and E-commerce Platforms

The rise of online grocery and e-commerce platforms poses a substantial threat to Casino Guichard-Perrachon. In France, online grocery sales experienced robust growth, reaching an estimated €13.4 billion in 2023, a significant increase from previous years. This trend is driven by increasing consumer comfort with digital purchasing and the proliferation of convenient delivery and click-and-collect services.

Both established retailers like Carrefour and specialized online grocers are expanding their digital footprints, offering consumers a wide array of choices beyond traditional brick-and-mortar stores. These platforms often compete on price, convenience, and product variety, directly challenging Casino's market share and forcing it to invest heavily in its own e-commerce capabilities to remain competitive.

Specialized Food Stores and Markets

Consumers increasingly turn to specialized food stores and local markets, bypassing larger retailers like Casino Guichard-Perrachon. These niche outlets offer unique products, organic selections, and direct-from-farm options, appealing to specific consumer tastes and potentially siphoning off sales from Casino's more generalized inventory. For instance, the organic food market in France saw significant growth, with sales reaching an estimated €15.2 billion in 2023, indicating a strong consumer preference for specialized offerings.

Ready-to-Eat Meals and Foodservice

The growing demand for ready-to-eat meals and foodservice options presents a significant threat to traditional grocery retailers like Casino Guichard-Perrachon. Consumers increasingly opt for convenience, turning to fast-food chains, meal delivery services, and pre-packaged meals for quick and easy dining solutions, directly substituting for groceries intended for home preparation.

In 2024, the global ready-to-eat meal market continued its robust expansion, driven by busy lifestyles and a desire for convenience. This trend directly impacts grocery sales as consumers divert spending towards these convenient alternatives. Casino's strategic focus on developing its own Quick Meal Solutions aims to capture a share of this growing market, mitigating the threat by becoming a provider rather than just a supplier of ingredients.

Discount Retailers and Private Labels

The growing prominence of discount retailers and private-label brands poses a significant threat of substitution for traditional retailers like Casino Guichard-Perrachon. These alternatives offer compelling value propositions, directly challenging higher-priced branded goods and premium store formats. Consumers are increasingly prioritizing affordability, a trend amplified by economic pressures.

This shift is evidenced by the expanding market share of private labels. In 2023, private labels accounted for approximately 25% of sales in the French grocery market, a figure that has been steadily climbing. This demonstrates a clear consumer preference for cost-effective options, directly impacting the demand for Casino's branded merchandise and potentially its premium offerings.

- Growing Private Label Penetration: Private labels are capturing an increasing share of the grocery market, offering a direct substitute for national brands.

- Discount Retailer Expansion: The aggressive expansion of discount chains like Lidl and Aldi in France provides consumers with readily available, lower-priced alternatives.

- Consumer Value-Seeking Behavior: Economic factors continue to drive consumer behavior towards value-oriented purchasing, making substitutes more attractive.

- Impact on Traditional Retailers: This trend pressures traditional retailers to adapt their pricing strategies and product assortments to remain competitive.

Non-Traditional Retail Formats

Emerging non-traditional retail formats, like mobile grocery stores and community-supported agriculture (CSA) programs, are providing consumers with new avenues to purchase food. These smaller-scale initiatives reflect shifting consumer preferences for convenience and local sourcing. For instance, the growth of online grocery delivery services, which bypass traditional brick-and-mortar stores, presents a significant substitute for conventional supermarket shopping.

These alternative models, while currently niche, represent a growing threat by catering to specific consumer needs not always met by large retailers. As of 2024, the online grocery market continues its expansion, with many consumers valuing the direct-to-doorstep convenience offered by these substitutes. This trend challenges the dominance of established players by offering personalized and often more agile solutions.

- Mobile Grocery Stores: Offering on-demand delivery and unique product selections.

- Community-Supported Agriculture (CSA): Providing direct access to farm-fresh produce, fostering local economies.

- Online Grocery Platforms: Facilitating convenient home delivery, increasing competition for physical stores.

- Specialty Food Stores: Catering to specific dietary needs or gourmet preferences, drawing customers away from general supermarkets.

Evolving Consumer Habits: The Threat of Grocery Substitutes

The threat of substitutes for Casino Guichard-Perrachon is significant, driven by evolving consumer habits and the rise of alternative food purchasing channels. Online grocery platforms and specialized food stores offer convenience and unique selections, directly competing with Casino's traditional supermarket model. In 2023, online grocery sales in France reached approximately €13.4 billion, highlighting a strong shift towards digital channels.

Furthermore, the increasing popularity of ready-to-eat meals and the growing preference for discount retailers and private-label brands also represent substantial substitutes. These options cater to consumers prioritizing affordability and convenience, putting pressure on Casino's pricing and product strategy. Private labels captured around 25% of the French grocery market in 2023, demonstrating this trend.

| Substitute Category | Key Characteristics | Market Trend (2023/2024) | Impact on Casino |

| Online Grocery Platforms | Convenience, Wide Selection, Home Delivery | €13.4 billion sales in France (2023) | Direct competition, requires investment in e-commerce |

| Specialty Food Stores/Local Markets | Unique Products, Organic Options, Local Sourcing | Organic food market €15.2 billion in France (2023) | Siphons niche customer segments |

| Ready-to-Eat Meals/Foodservice | Convenience, Speed, Reduced Preparation | Global market expansion in 2024 | Reduces demand for groceries for home cooking |

| Discount Retailers/Private Labels | Affordability, Value for Money | Private labels ~25% of French grocery sales (2023) | Challenges pricing and branded goods |

Entrants Threaten

High Capital Requirements for Physical Stores

The significant capital required to establish a physical retail presence, particularly for hypermarkets and large supermarkets, acts as a substantial deterrent to new entrants. For instance, the cost of acquiring or leasing prime real estate, constructing or renovating store facilities, and stocking extensive inventory presents a formidable financial hurdle. In 2024, the ongoing inflation and rising construction costs further exacerbate these capital requirements, making it exceptionally challenging for smaller players to compete with established giants like Casino Guichard-Perrachon.

Established Brand Loyalty and Customer Habits

Established retailers like Casino Guichard-Perrachon leverage strong brand loyalty and deeply ingrained customer shopping habits. These existing relationships make it difficult for newcomers to gain traction. For instance, in 2024, Casino reported a significant portion of its revenue derived from its core customer base, highlighting the stickiness of these loyalties.

Regulatory Hurdles and Zoning Laws

Navigating France's intricate regulatory landscape, including strict zoning laws and extensive permitting processes for construction and operations, presents a substantial hurdle for potential new entrants in the retail sector. These requirements, often involving lengthy approval timelines and significant upfront investment, particularly impact the establishment of large-format stores, a key segment for Casino Guichard-Perrachon. For instance, obtaining the necessary authorizations can take many months, if not years, adding considerable cost and uncertainty to market entry.

Economies of Scale and Purchasing Power

Casino, as an established retailer, leverages significant economies of scale in its operations. This translates to substantial purchasing power with suppliers, enabling them to secure lower prices for goods. For instance, in 2024, Casino's extensive network allowed for bulk purchasing that would be unachievable for a new entrant starting with a smaller footprint.

This cost advantage is a formidable barrier. New competitors would find it exceedingly difficult to match Casino's price points without first achieving comparable sales volumes. This lack of immediate cost efficiency makes it challenging for newcomers to gain market share based on price alone.

- Economies of Scale: Casino's established size allows for cost savings in purchasing, logistics, and marketing.

- Purchasing Power: Bulk buying enables Casino to negotiate better terms and prices with suppliers.

- Price Competition: New entrants face a significant disadvantage in matching Casino's competitive pricing due to lower initial volumes.

- Barrier to Entry: Achieving similar cost efficiencies requires substantial investment and time, deterring potential new competitors.

Growth of E-commerce Lowering Barriers

The growth of e-commerce significantly lowers barriers to entry in the grocery sector. While traditional brick-and-mortar stores require substantial capital for real estate and inventory, online-only grocery operations can launch with far fewer resources. This shift allows digitally native businesses to enter the market more readily, challenging established players like Casino Guichard-Perrachon.

The ongoing digitalization of retail, including advancements in supply chain technology and online payment systems, further facilitates market entry. For instance, in 2024, the global e-commerce market continued its expansion, with online grocery sales showing robust growth. This digital infrastructure makes it easier for new, agile competitors to establish a presence.

- Lower Capital Requirements: Online-only grocery models bypass the need for expensive physical store locations, reducing initial investment.

- Digitalization of Retail: Technologies enabling online sales, delivery logistics, and customer management are more accessible than ever.

- Agile Competitors: Digitally native companies can adapt quickly to market changes and consumer preferences, posing a threat to legacy businesses.

- Scaling Logistics Challenge: Despite lower entry barriers, efficiently scaling delivery networks and managing fresh inventory remains a significant hurdle for new entrants.

Retail Entry: High Capital vs. Digital Agility

The threat of new entrants for Casino Guichard-Perrachon is moderate, primarily due to high capital requirements for physical stores and established brand loyalty. However, the rise of e-commerce and digital platforms is lowering some of these barriers, allowing for more agile competitors to emerge. Regulatory hurdles and the need for extensive supply chain networks also act as significant deterrents.

| Factor | Impact on Casino | Evidence (2024 Data) |

|---|---|---|

| Capital Requirements | High Barrier | Ongoing inflation and rising construction costs in 2024 increased the cost of establishing new physical retail outlets. |

| Brand Loyalty | Strong Deterrent | Casino's core customer base remained significant in 2024, indicating deeply ingrained shopping habits. |

| E-commerce Growth | Lowering Barrier | The global e-commerce market continued its expansion in 2024, with online grocery sales showing robust growth, making digital entry easier. |

| Regulatory Landscape | High Barrier | Complex zoning laws and permitting processes in France continue to add time and cost to market entry for large-format stores. |

| Economies of Scale | Strong Deterrent | Casino's extensive network in 2024 provided significant purchasing power, enabling lower prices than new, smaller entrants could achieve. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Casino Guichard-Perrachon is built upon a foundation of reliable data, including the company's annual reports, investor presentations, and filings with regulatory bodies like the AMF. We also incorporate insights from industry-specific market research reports and economic databases to provide a comprehensive view of the competitive landscape.