Enhabit Home Health & Hospice Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Enhabit Home Health & Hospice

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

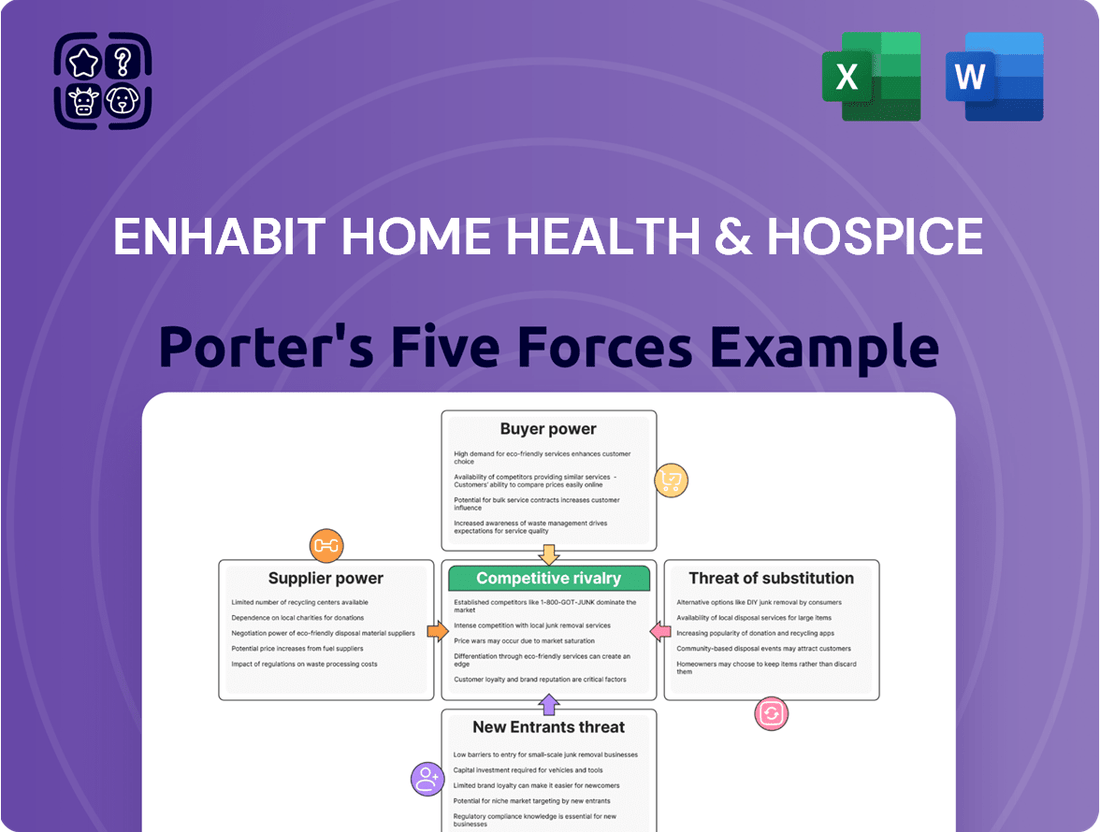

The home health and hospice industry, as faced by Enhabit, presents a complex interplay of forces. While the threat of new entrants might seem moderate due to regulatory hurdles, the bargaining power of buyers, particularly Medicare and private insurers, significantly shapes pricing and service delivery. The full analysis reveals the real forces shaping Enhabit Home Health & Hospice’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Highly Skilled Healthcare Professionals

The scarcity of highly skilled healthcare professionals, including nurses, therapists, and aides, significantly amplifies their bargaining power within the home health and hospice industry. This persistent shortage means providers like Enhabit are locked in intense competition for talent, directly driving up wages and benefits as they strive to attract and retain essential staff. For instance, in 2024, the Bureau of Labor Statistics projected a 6% growth for registered nurses between 2022 and 2032, a rate faster than the average for all occupations, underscoring the ongoing demand and competitive landscape Enhabit navigates to maintain its nationwide service delivery.

Specialized Medical Equipment and Supplies Providers

Enhabit Home Health & Hospice depends on specialized medical equipment and supplies providers for crucial items like durable medical equipment (DME), pharmaceuticals, and other medical necessities. These suppliers are critical to delivering effective in-home care.

The market for these specialized medical goods is quite concentrated, with major players like McKesson Corporation and Cardinal Health holding significant sway. Their dominance allows them considerable leverage in negotiations regarding pricing and the availability of essential supplies.

Furthermore, the growing demand for home healthcare equipment, which was anticipated to hit $63 billion in 2024, amplifies the bargaining power of these key suppliers. This robust market growth means they are less dependent on any single buyer, strengthening their position.

Technology and Software Vendors

The bargaining power of technology and software vendors for companies like Enhabit is notably increasing. The push towards digital transformation in healthcare, including home health and hospice, means providers are increasingly reliant on specialized tech. For instance, the telehealth market, a key area for home care, was projected to reach $193.2 billion by 2028, demonstrating its growing importance and the vendors' leverage.

As Enhabit integrates advanced solutions such as remote patient monitoring and AI for diagnostics or administrative tasks, its dependence on these tech providers strengthens. This dependency can translate into higher pricing or less flexibility in contract terms if only a limited number of vendors offer the specific, high-quality solutions required for competitive patient care and operational efficiency.

Physician and Hospital Referral Networks

Local healthcare providers, including hospitals and physicians, are critical sources for patient referrals, directly impacting companies like Enhabit Home Health & Hospice. Their ability to steer patients towards specific agencies grants them significant leverage, influencing patient acquisition and revenue streams. For instance, in 2024, a substantial portion of patient referrals for many home health agencies originated from hospital discharge planners and physician offices, underscoring the importance of these relationships.

- Referral Dependence: Hospitals and physicians act as gatekeepers, controlling access to a significant patient base for home health and hospice services.

- Relationship Value: Strong, established partnerships with referral sources are vital for consistent patient volumes and market share.

- Performance Impact: The quality of care and patient outcomes directly influence a provider's willingness to continue referring patients to specific agencies.

Specialized Training and Education Institutions

The bargaining power of specialized training and education institutions is a significant factor for home health and hospice providers like Enhabit. The quality and availability of these programs directly influence the competence and supply of qualified caregivers. For instance, a shortage of accredited training programs can drive up the cost for companies like Enhabit when they need to recruit or upskill their workforce. This limited supply of well-trained professionals can impact the overall consistency and quality of care delivered.

In 2024, the demand for skilled home health aides remained high, with industry reports indicating a persistent shortage in many regions. This scarcity often translates to higher recruitment and training expenses for agencies. For example, the average cost to train a new home health aide can range from $500 to $2,000, depending on the program's length and accreditation. Institutions that offer specialized, high-quality training can therefore command higher fees, increasing operational costs for providers.

- Limited supply of accredited training programs can inflate recruitment and training costs for Enhabit.

- The quality of specialized education directly impacts the competence and availability of the caregiver workforce.

- Higher training costs can potentially affect the overall pricing and profitability of home health services.

Home Health Suppliers Gain Leverage Amidst Market Growth

The bargaining power of suppliers for Enhabit Home Health & Hospice is amplified by the concentration of specialized medical equipment providers and the growing demand for these goods. Key players in the durable medical equipment (DME) market, like McKesson and Cardinal Health, leverage their market share to negotiate favorable terms. This situation is further intensified by the increasing overall market for home healthcare equipment, which was projected to reach $63 billion in 2024, making these suppliers less reliant on any single buyer.

What is included in the product

This analysis delves into the competitive landscape for Enhabit Home Health & Hospice, examining the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the industry.

Quickly identify and mitigate competitive threats by visualizing the intensity of rivalry and the impact of new entrants on Enhabit's market position.

Understand the power of buyers and suppliers to optimize pricing and service delivery, ensuring Enhabit remains a preferred choice in home health and hospice.

Customers Bargaining Power

Medicare and Medicaid Programs

Government payers, primarily Medicare and Medicaid, wield considerable bargaining power over home health and hospice providers like Enhabit. These programs represent a substantial portion of the company's revenue, meaning their reimbursement rates and policy shifts directly influence Enhabit's financial health and strategic planning.

For instance, the Centers for Medicare & Medicaid Services (CMS) regularly adjusts payment rates. In 2024, CMS proposed a net payment rate increase of 0.8% for home health agencies, a figure that, while positive, still requires providers to carefully manage costs and operations to maintain profitability amidst such incremental changes.

The sheer volume of patients covered by these government programs gives them leverage. Any significant changes in reimbursement methodologies or regulatory requirements, such as those related to quality reporting or patient eligibility, can force providers like Enhabit to adapt their service delivery models and financial projections swiftly.

Medicare Advantage Plans and Private Insurers

The increasing prevalence of Medicare Advantage plans positions private insurers as significant customers for Enhabit Home Health & Hospice. These plans, experiencing substantial enrollment growth, wield considerable influence over contract terms and reimbursement rates.

As Medicare Advantage plans expand their in-home support benefits, they naturally increase their leverage with providers like Enhabit. This growing customer power necessitates proactive engagement from Enhabit to manage evolving payment structures and secure favorable terms.

Enhabit's strategy includes pursuing payor innovation contracts, a move designed to improve reimbursement rates and effectively navigate the changing landscape of their customer base. This focus on partnership aims to mitigate the bargaining power of these influential insurers.

Patients and Families (Private Pay Segment)

In the private pay segment for Enhabit Home Health & Hospice, patients and their families wield considerable bargaining power. This is largely driven by their price sensitivity, especially considering the significant median annual costs of in-home care, which can range from $54,912 for home health aides to $63,386 for skilled nursing care, according to 2024 Genworth data. The presence of numerous competing providers in the market allows these consumers to readily compare services and negotiate pricing, putting pressure on Enhabit to clearly articulate its value proposition and the personalized nature of its care to secure and maintain these crucial customer relationships.

Managed Care Organizations

Managed care organizations (MCOs), beyond Medicare Advantage, wield considerable bargaining power by overseeing vast patient populations. These entities actively negotiate contracts with healthcare providers, including home health and hospice services. In 2024, the continued emphasis on value-based care and cost containment by MCOs puts pressure on providers like Enhabit to prove enhanced patient outcomes and operational efficiency. For instance, many MCOs are increasingly tying reimbursement rates to quality metrics and patient satisfaction scores, directly impacting revenue streams for home health agencies.

Enhabit's ability to secure favorable contracts with these powerful payers is crucial for market access and sustained growth. The negotiating leverage of MCOs stems from their ability to direct large volumes of patients to specific providers. This necessitates that Enhabit demonstrate a clear value proposition, showcasing not only quality care but also cost-effectiveness to maintain and expand these vital relationships. As of the first half of 2024, national MCOs continue to consolidate their market share, further amplifying their negotiating strength.

- Managed Care Organizations (MCOs) represent a significant customer segment for Enhabit.

- MCOs influence pricing and contract terms through their large patient bases and focus on value-based care.

- In 2024, MCOs are increasingly scrutinizing provider performance on quality metrics and cost efficiency.

- Successful partnerships with MCOs are essential for Enhabit's market access and revenue generation.

Hospital Systems and Post-Acute Networks

Hospitals and other post-acute care facilities are significant customers for Enhabit, influencing its bargaining power. These institutions, when selecting preferred partners for patient transitions and ongoing care, can negotiate terms based on the substantial patient volume they represent. For instance, in 2024, the demand for home health services to manage post-hospitalization care remained robust, with an estimated 1.5 million Medicare beneficiaries receiving home health services annually, highlighting the leverage these referral sources possess.

Enhabit's strategic advantage lies in its capacity to integrate smoothly into these established healthcare networks. This seamless integration not only facilitates patient flow but also secures a consistent stream of referrals, thereby strengthening Enhabit's position in these negotiations. The ability to demonstrate efficient care coordination and positive patient outcomes is crucial for maintaining these relationships and mitigating the bargaining power of these large customer groups.

- Hospitals as Key Customers: Healthcare systems and post-acute care providers are crucial referral sources for Enhabit.

- Negotiating Power: Their significant patient volume allows them to negotiate favorable terms and service level agreements.

- Integration Advantage: Enhabit's ability to integrate seamlessly into hospital discharge processes enhances its appeal and referral stability.

- Referral Volume Impact: In 2024, the continued reliance on home health for post-acute care underscored the importance of these hospital relationships for consistent business.

Decoding Customer Bargaining Power in Home Care

The bargaining power of customers for Enhabit Home Health & Hospice is significant, particularly from government payers like Medicare and Medicaid, and increasingly from Medicare Advantage plans. These entities represent a substantial portion of Enhabit's revenue, granting them considerable leverage over reimbursement rates and policy changes. Private pay customers also exert influence due to price sensitivity, with the high cost of care, around $54,912 to $63,386 annually in 2024 for different care levels, prompting comparisons and negotiations among numerous providers.

Managed care organizations (MCOs) wield substantial power due to their large patient populations and focus on value-based care, with reimbursement increasingly tied to quality metrics and patient outcomes in 2024. Hospitals and post-acute care facilities, as major referral sources, also negotiate terms based on the patient volume they represent, with home health remaining critical for post-hospitalization care in 2024, evidenced by approximately 1.5 million Medicare beneficiaries annually receiving such services.

| Customer Segment | Influence Factor | 2024 Relevance |

|---|---|---|

| Government Payers (Medicare/Medicaid) | Significant revenue share, reimbursement rate control | CMS proposed 0.8% net payment increase for home health in 2024, requiring cost management. |

| Medicare Advantage Plans | Growing enrollment, expanding in-home benefits | Increased leverage with providers as benefits expand, necessitating proactive engagement. |

| Private Pay Customers | Price sensitivity, availability of competing providers | Median annual costs range from $54,912 (home health aide) to $63,386 (skilled nursing). |

| Managed Care Organizations (MCOs) | Large patient bases, value-based care focus | Reimbursement tied to quality metrics and cost efficiency; market share consolidation amplifies strength. |

| Hospitals/Post-Acute Facilities | Patient volume, referral source importance | ~1.5 million Medicare beneficiaries received home health annually; crucial for post-hospitalization care. |

What You See Is What You Get

Enhabit Home Health & Hospice Porter's Five Forces Analysis

You're previewing the final version of Enhabit Home Health & Hospice's Porter's Five Forces Analysis—precisely the same document that will be available to you instantly after buying. This comprehensive analysis details the competitive landscape, including the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the industry. You'll gain actionable insights into the strategic positioning of Enhabit Home Health & Hospice based on these key market forces.

Rivalry Among Competitors

Fragmented yet Consolidating Market Landscape

The U.S. home health and hospice sector is characterized by its fragmented nature, featuring a vast number of local and regional players. However, this landscape is actively evolving, with a clear trend towards consolidation driven by mergers and acquisitions. This means that while many small providers exist, larger entities are increasingly absorbing them, reshaping the competitive arena.

Enhabit, as a prominent national provider, faces intense competition from other major national companies such as Amedisys and LHC Group, which are also actively participating in this consolidation. This dynamic creates a challenging environment where maintaining market share necessitates constant strategic adjustments and a keen awareness of competitor activities.

Intense Competition for Clinical Talent

The healthcare industry, particularly in home health and hospice, faces a fierce battle for qualified clinical professionals. This intense competition for nurses, therapists, and aides is a major driver of operational costs for companies like Enhabit. The shortage means providers must offer more than just good patient care; they need to be employers of choice, which translates to competitive compensation and benefits packages.

In 2024, the demand for home health aides and registered nurses continued to outpace supply, exacerbating this rivalry. For instance, the U.S. Bureau of Labor Statistics projected a 22% growth for home health and personal care aides from 2022 to 2032, much faster than the average for all occupations. This creates a significant challenge for Enhabit to staff its operations effectively and maintain service levels, directly impacting its ability to scale and its profit margins.

Reimbursement Pressures and Policy Shifts

The home health and hospice sector, including companies like Enhabit, is constantly dealing with pressure on how much they get paid by government programs like Medicare and Medicaid, as well as by private insurance companies. For example, proposals for Medicare payment cuts, even if not fully implemented, create uncertainty and force companies to be more efficient. This makes it harder to compete solely on service quality when cost control becomes paramount.

These reimbursement challenges directly impact profitability and intensify competition, pushing companies to focus heavily on managing their revenue cycles effectively. Enhabit, like its peers, must streamline billing and collection processes to maintain financial health amidst these pressures. The ongoing need to adapt to evolving payment structures, such as shifts away from volume-based to value-based care models, requires significant operational adjustments.

Policy shifts, such as the implementation and subsequent adjustments to the Patient-Driven Groupings Model (PDGM) for Medicare home health, are critical. PDGM, introduced in 2020 and continuing to be refined, changed how home health agencies are reimbursed by classifying patients into payment groups based on clinical characteristics and expected resource use. This model rewards agencies that can provide high-quality care within these defined payment parameters, making adaptability a key competitive advantage.

Differentiation Through Specialized Services and Technology

Competitive rivalry in home health and hospice is intensifying as providers differentiate through specialized services and technology adoption. Enhabit is focusing on personalized care plans and investing in technologies like AI and remote patient monitoring to stand out. This strategic differentiation is crucial in a market where continuous innovation is key to improving patient outcomes and operational efficiency.

The healthcare sector, especially home-based care, is seeing a significant push towards advanced technological integration. For instance, by the end of 2024, many home health agencies are expected to have implemented or be piloting AI-driven tools for tasks such as patient risk stratification and appointment scheduling. Remote monitoring devices are also becoming more common, allowing for continuous patient data collection and early intervention, which directly impacts competitive positioning.

- Specialized Services: Providers are moving beyond general care to offer niche services like advanced wound care, palliative care integration, and high-acuity support at home, attracting specific patient populations.

- Technology Adoption: Investments in AI for operational efficiency and predictive analytics, alongside remote patient monitoring (RPM) solutions, are becoming standard for competitive differentiation.

- Patient Outcomes: The focus on technology and specialization directly aims to improve patient outcomes, reduce hospital readmissions, and enhance the overall patient experience, which are key metrics for success.

- Market Trends: By mid-2024, reports indicated a growing trend of home health agencies acquiring or partnering with technology firms to bolster their service offerings and competitive edge.

Geographic Reach and Referral Network Strength

Companies that can reach more patients and have strong connections with those who refer them, like hospitals, have a significant edge. Enhabit's presence in 34 states allows it to serve a wider patient base and tap into more referral sources compared to smaller, local competitors. This broad geographic reach, combined with dedicated efforts to cultivate relationships with key referrers such as hospital discharge planners, is crucial for sustained growth and market share.

- Nationwide Presence: Enhabit operates in 34 states, offering a broad geographic footprint.

- Referral Network: The company actively builds and maintains relationships with referral sources, particularly hospital discharge planners.

- Competitive Advantage: This extensive network and reach differentiate Enhabit from smaller, localized competitors.

- Growth Driver: Optimizing high-value referral streams is identified as a key factor for Enhabit's expansion.

Rivalry Heats Up: Home Health & Hospice Battle for Talent and Tech

Competitive rivalry within the home health and hospice sector is intense, driven by a fragmented market undergoing consolidation. Enhabit faces direct competition from other national players like Amedisys and LHC Group, who are also actively engaged in mergers and acquisitions. This dynamic necessitates continuous strategic adaptation and a sharp focus on market positioning.

The battle for qualified clinical staff, particularly nurses and aides, significantly fuels this rivalry. In 2024, the demand for these professionals continued to outstrip supply, with the U.S. Bureau of Labor Statistics projecting a 22% growth for home health and personal care aides between 2022 and 2032. This scarcity forces providers like Enhabit to invest heavily in competitive compensation and benefits to attract and retain talent, directly impacting operational costs and service delivery capabilities.

Companies are also differentiating through specialized service offerings and technology adoption. Enhabit is investing in AI and remote patient monitoring to enhance personalized care plans and operational efficiency. By mid-2024, many agencies were integrating AI tools for risk stratification and piloting remote monitoring, aiming to improve patient outcomes and reduce readmissions, thereby gaining a competitive edge.

| Competitor | 2024 Market Share (Est.) | Key Differentiators | Recent Activity |

|---|---|---|---|

| Enhabit Home Health & Hospice | ~5-7% | National presence, specialized care focus | Investment in technology, strategic partnerships |

| Amedisys | ~8-10% | Broad service offerings, strong referral networks | Acquisition by UnitedHealth Group (Optum) completed in 2023, impacting 2024 landscape |

| LHC Group | ~7-9% | Integrated care models, geographic diversification | Acquisition by Optum completed in 2023, similar impact to Amedisys |

| Other Regional/Local Providers | ~70-80% (collectively) | Community-specific services, personalized patient relationships | Continued consolidation through smaller acquisitions |

SSubstitutes Threaten

Hospital and Skilled Nursing Facility (SNF) Care

While the healthcare landscape increasingly favors home-based care, hospitals and skilled nursing facilities (SNFs) continue to serve as significant substitutes for patients needing acute or intensive post-acute care that home settings cannot safely accommodate. For instance, in 2024, the average length of stay in a U.S. hospital remained around 5-6 days, with SNFs providing an average post-hospital stay of 20-30 days for rehabilitation.

These institutional settings offer a higher degree of continuous medical supervision and access to specialized equipment, making them essential for managing complex medical conditions or severe injuries. This reality necessitates that providers like Enhabit must clearly articulate and prove the efficacy and safety of their in-home services for suitable patient demographics to remain competitive.

Informal Caregivers and Family Support

The threat of informal caregiving is a significant factor for Enhabit Home Health & Hospice. Many families rely on unpaid assistance from relatives or friends for daily tasks, transportation, and personal care. This can directly reduce the demand for professional home health services, especially for non-clinical support.

In 2023, an estimated 61 million Americans provided care to a family member or friend with a chronic illness, disability, or aging issue, according to the AARP. This vast pool of informal caregivers represents a substantial substitute for paid home health services, particularly when the care needs are less medically intensive.

Outpatient Clinics and Rehabilitation Centers

Outpatient clinics and rehabilitation centers present a significant threat of substitution for Enhabit Home Health & Hospice. For individuals requiring physical, occupational, or speech therapy, these facilities offer an alternative to in-home services. If a patient is mobile and values a structured, clinical setting, they might opt for an outpatient clinic rather than receiving therapy at home.

This substitution is particularly relevant when patients can easily travel to a clinic. For instance, the Centers for Medicare & Medicaid Services (CMS) data indicates a substantial number of Medicare beneficiaries utilize outpatient therapy services. In 2023, Medicare Part B spending on outpatient physical therapy alone was in the billions of dollars, demonstrating the scale of these alternative care settings.

Assisted Living Facilities and Residential Care Homes

Assisted living facilities and residential care homes present a significant threat of substitution for Enhabit's home health and hospice services. These options cater to individuals needing continuous supervision and assistance with daily activities, especially when 'aging in place' becomes unfeasible or family support is insufficient. This directly impacts Enhabit's long-term care customer segment.

The demand for assisted living and residential care is growing. For example, in 2024, the U.S. assisted living market size was estimated to be around $60 billion, reflecting a strong preference for comprehensive care solutions. This growth indicates that a substantial portion of Enhabit's potential customer base might opt for these more integrated care settings rather than solely relying on in-home services.

- Market Growth: The U.S. assisted living market is projected to continue its expansion, driven by an aging population and increasing acceptance of such facilities.

- Comprehensive Care: These facilities offer a bundled approach to care, including housing, meals, and personal assistance, which can be more appealing than fragmented in-home services for some individuals.

- Cost Considerations: While costs vary, the all-inclusive nature of assisted living can sometimes be perceived as more predictable or manageable than the variable costs associated with ongoing home health care.

Standalone Telehealth or Remote Monitoring Services

While Enhabit Home Health & Hospice leverages technology, the growing accessibility of standalone telehealth platforms and remote patient monitoring devices presents a threat. These services can act as partial substitutes for traditional in-home care, particularly for routine check-ups, medication management, or ongoing chronic condition oversight where direct physical intervention isn't critical.

For instance, the U.S. telehealth market was valued at over $40 billion in 2023 and is projected to continue its strong growth trajectory. Patients may find these digital solutions more convenient and cost-effective for specific needs, potentially reducing demand for some of Enhabit's in-person services.

- Standalone telehealth platforms offer convenient alternatives for routine consultations.

- Remote patient monitoring devices can manage chronic conditions without frequent in-person visits.

- The increasing adoption of these technologies by consumers poses a direct substitution risk.

- Enhabit must highlight the unique value of its integrated, hands-on care model.

Key Substitutes Shaping the Home Healthcare Market

Hospitals and skilled nursing facilities remain significant substitutes, especially for acute care needs. In 2024, hospital stays averaged 5-6 days, with SNFs providing around 20-30 days of post-acute care, offering higher medical supervision and specialized equipment.

Informal caregiving is a substantial substitute, with 61 million Americans providing unpaid care in 2023. This reliance on family and friends reduces demand for professional services, particularly for non-clinical support.

Outpatient clinics and rehabilitation centers offer alternatives for therapy services. The billions spent by Medicare Part B on outpatient physical therapy in 2023 highlight the scale of these clinical alternatives.

Assisted living facilities, valued at $60 billion in 2024, provide comprehensive care and supervision, appealing to those for whom aging in place is not feasible.

| Substitute Type | Key Characteristics | 2023/2024 Data Point | Impact on Enhabit |

| Hospitals/SNFs | Acute/intensive care, higher supervision | Avg. 5-6 day hospital stay; 20-30 day SNF stay | Direct substitute for complex cases |

| Informal Caregiving | Unpaid assistance with daily tasks | 61 million informal caregivers (2023) | Reduces demand for non-clinical services |

| Outpatient Clinics | Structured therapy setting | Billions in Medicare Part B outpatient PT spending (2023) | Alternative for rehabilitation needs |

| Assisted Living | Bundled housing, meals, personal care | $60 billion U.S. assisted living market (2024) | Alternative for long-term care segment |

Entrants Threaten

High Regulatory and Licensing Barriers

The home health and hospice sector faces significant barriers to entry due to stringent regulatory requirements. New companies must navigate a complex web of federal and state licensing, certifications, and ongoing compliance with laws like the Medicare Conditions of Participation. For instance, the Centers for Medicare & Medicaid Services (CMS) imposes detailed quality reporting measures and anti-fraud protocols that demand substantial investment in infrastructure and expertise.

Substantial Capital Investment Requirements

The home health and hospice industry demands substantial capital investment, posing a significant barrier to new entrants. Establishing a national presence, akin to Enhabit's extensive network of hundreds of locations across numerous states, necessitates considerable upfront funding for facility acquisition, advanced medical equipment, and robust IT infrastructure. These high start-up costs can effectively deter smaller, less-resourced competitors from entering the market.

Challenges in Workforce Recruitment and Retention

The severe nationwide shortage of skilled healthcare professionals, particularly nurses and therapists, presents a significant barrier to entry for new home health and hospice providers. This scarcity means new companies face immense difficulty in attracting and retaining the qualified staff necessary to operate effectively.

In 2024, the demand for registered nurses, a critical role in home health, continued to outstrip supply, with projections indicating a persistent deficit for years to come. This competitive labor market makes it exceptionally challenging for new entrants to build a stable and experienced clinical team, a fundamental requirement for delivering quality patient care and establishing a market presence.

Difficulty in Establishing Referral Networks and Payer Contracts

New entrants into the home health and hospice sector, like those looking to compete with established providers such as Enhabit, face a substantial hurdle in developing robust referral networks. Existing players have cultivated deep relationships with hospitals, physicians, and other healthcare providers over many years, creating a steady stream of patient referrals. For instance, as of 2024, the home healthcare industry is heavily reliant on physician orders and hospital discharge planners, making these established connections invaluable.

Furthermore, securing favorable contracts with payers, including government programs like Medicare and Medicaid, as well as a multitude of private insurance companies, is a critical barrier. These contracts dictate reimbursement rates and are essential for a new company's financial sustainability and ability to attract patients. In 2024, Medicare remains the largest payer for home health services, underscoring the importance of successfully navigating its reimbursement structures.

- Established Referral Networks: Existing providers like Enhabit benefit from long-standing relationships with hospitals and physician groups, which are vital for patient volume.

- Payer Contract Negotiation: New entrants must negotiate complex and often lengthy contracts with numerous payers, including Medicare, Medicaid, and private insurers, which is a time-consuming and resource-intensive process.

- Reimbursement Challenges: Securing competitive reimbursement rates from payers is crucial for financial viability, and new companies often lack the leverage of established providers.

- Market Access: The difficulty in building these foundational relationships and contracts significantly limits a new entrant's ability to gain market access and compete effectively.

Brand Reputation and Trust Building

In the home health and hospice sector, patient trust and brand reputation are absolutely critical. Established players like Enhabit have cultivated this trust over many years through consistent, high-quality care. This makes it difficult for new companies to break in.

New entrants face a significant hurdle in building a reputable brand. They need substantial investment in marketing and rigorous quality control to earn patient confidence. This is a lengthy and demanding process, especially in a field as sensitive as healthcare.

For instance, a 2023 report indicated that over 70% of patients choose home health providers based on recommendations and established reputations. This statistic underscores the challenge new entrants face in displacing trusted, long-standing organizations.

- Brand Reputation: Crucial for patient choice in home health.

- Trust Building: Requires significant time and investment for new entrants.

- Market Entry Barrier: Established providers benefit from years of credibility.

- Quality Assurance: Essential for new providers to gain patient confidence.

Home Health & Hospice: High Barriers to Entry

The threat of new entrants in the home health and hospice sector is generally considered low, largely due to substantial barriers. These include high capital requirements for infrastructure and technology, alongside the necessity of navigating complex and evolving regulatory landscapes. Securing necessary licenses and certifications, such as those mandated by the Centers for Medicare & Medicaid Services (CMS), demands significant expertise and investment.

The industry's reliance on a skilled workforce, particularly nurses and therapists, further limits new entrants. In 2024, the persistent shortage of these professionals, with demand significantly outpacing supply, makes it incredibly difficult for new companies to recruit and retain the necessary clinical staff. This labor scarcity is a critical deterrent.

Building established referral networks with hospitals and physicians, a process that takes years, is another major hurdle. New companies must also negotiate complex reimbursement contracts with a multitude of payers, including Medicare, which remains the largest payer for home health services as of 2024. These established relationships and payer contracts provide a significant competitive advantage to existing providers.

| Barrier | Description | Impact on New Entrants |

|---|---|---|

| Regulatory Compliance | Stringent federal and state licensing, certifications, and ongoing adherence to CMS Conditions of Participation. | High cost and complexity, requiring specialized knowledge. |

| Capital Investment | Significant upfront costs for facilities, medical equipment, and IT infrastructure. | Deters smaller, less-resourced competitors. |

| Skilled Workforce Shortage | Nationwide scarcity of nurses and therapists. | Makes recruitment and retention of qualified staff extremely challenging. |

| Referral Networks | Established relationships with hospitals and physicians. | New entrants struggle to gain consistent patient referrals. |

| Payer Contracts | Negotiating reimbursement rates with Medicare, Medicaid, and private insurers. | New companies lack the leverage of established providers. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Enhabit Home Health & Hospice is built upon a comprehensive review of industry-specific market research reports, company financial filings (10-K, 10-Q), and reputable healthcare industry publications to capture competitive dynamics.