Dropbox Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Dropbox

Don't Miss the Bigger Picture

Dropbox operates in a dynamic cloud storage market, facing significant competitive pressures. The threat of new entrants is moderate, as the high initial investment in infrastructure is offset by low switching costs for users. Buyer power is substantial due to the availability of numerous free and low-cost alternatives.

The bargaining power of suppliers is relatively low, as many cloud infrastructure providers exist. However, the threat of substitutes, like integrated collaboration suites, remains a key concern for Dropbox's core offering.

The complete report reveals the real forces shaping Dropbox’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

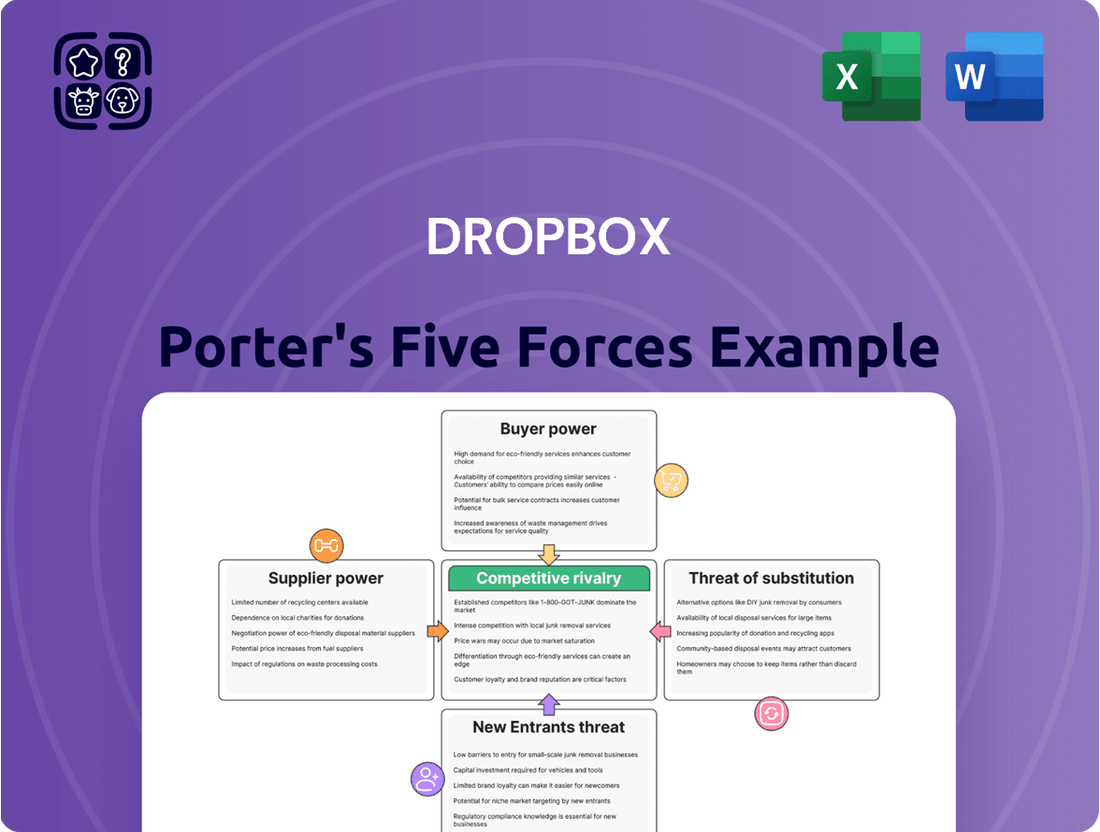

Suppliers Bargaining Power

Limited Differentiation of Core Infrastructure

The bargaining power of suppliers for Dropbox is somewhat limited due to the increasing commoditization of core cloud infrastructure. This means that fundamental components like data centers and network connectivity are offered by numerous providers, making it harder for any single supplier to wield significant influence. For instance, the global cloud infrastructure market, encompassing data centers and related services, was valued at approximately $255 billion in 2023 and is projected to grow, offering ample choice for companies like Dropbox.

Dependency on Hyperscale Cloud Providers

Dropbox's reliance on hyperscale cloud providers like AWS, Azure, and Google Cloud, even with its own infrastructure, grants these giants significant bargaining power. These providers control a vast majority of the cloud market, meaning their pricing and service terms can heavily influence Dropbox's operational costs.

In 2024, AWS, Azure, and Google Cloud continue to dominate the global cloud infrastructure market, with AWS alone holding an estimated market share of around 31%. This concentration of power allows them to dictate terms to many businesses, including those like Dropbox that leverage their services for specific needs or to manage fluctuating demand.

High Switching Costs for Core Infrastructure

Migrating substantial data volumes and critical applications between cloud infrastructure providers or data center services presents significant complexity and expense. These elevated switching costs inherently bolster the bargaining power of incumbent suppliers, as Dropbox encounters considerable operational disruption and financial investment when contemplating a change in providers.

This situation effectively creates a degree of dependency for Dropbox on its current infrastructure partners. For example, the estimated cost for enterprises to migrate from one major cloud provider to another can range from hundreds of thousands to millions of dollars, depending on the scale and complexity of services, a factor that directly impacts Dropbox's supplier negotiation leverage.

Availability of Specialized Software and Hardware

The availability of specialized software and hardware can significantly influence the bargaining power of suppliers for a company like Dropbox. When suppliers offer unique or critical components, especially those that enable competitive differentiation, they can command greater leverage. For instance, providers of advanced security software or bespoke data management solutions essential for cloud services can hold considerable sway.

Dropbox's strategic acquisitions, such as Nira for content governance and Promoted.ai for AI-driven search capabilities, highlight a growing reliance on specialized technologies. These moves suggest an increased engagement with specific technology providers whose expertise is crucial for enhancing Dropbox's product offerings and maintaining its competitive edge. This integration of niche technologies can bolster the bargaining power of those suppliers.

- Unique Offerings: Suppliers providing proprietary software for data encryption or AI-powered content analysis can exert significant power if these solutions are not easily replicable.

- Integration Costs: High costs associated with integrating new, specialized hardware or software can make switching suppliers difficult, thereby increasing supplier leverage.

- Essential Capabilities: If a supplier's technology is fundamental to a core Dropbox function, like its sync engine or collaboration tools, their bargaining power is amplified.

- Partnership Dependence: Dropbox's reliance on specific cloud infrastructure providers or AI development partners can create dependencies that suppliers can leverage.

Talent Pool for Cloud Infrastructure Management

The bargaining power of suppliers, particularly concerning the talent pool for cloud infrastructure management, is a significant factor for Dropbox. The scarcity of highly specialized professionals in areas like cloud architecture, cybersecurity, and data center operations grants considerable leverage to the labor market. Dropbox requires these skilled engineers and IT staff to not only maintain its existing cloud infrastructure but also to drive innovation and ensure robust security measures.

This demand for niche expertise can directly impact operational expenses by driving up labor costs. For instance, in 2024, the average salary for a senior cloud engineer in major tech hubs often exceeded $170,000 annually, a figure that can fluctuate based on experience and specific skill sets. The competitive landscape for such talent means that companies like Dropbox must offer attractive compensation and benefits packages to secure and retain these critical employees.

- Talent Scarcity: A shortage of professionals in cloud architecture, cybersecurity, and data center management exists.

- Specialized Needs: Dropbox relies on these skilled individuals for infrastructure maintenance and innovation.

- Increased Labor Costs: High demand for this talent drives up salaries and recruitment expenses.

- Impact on Operations: Rising labor costs directly influence Dropbox's overall operational expenditure.

Supplier Power: Cloud, Tech, and Talent Dynamics

The bargaining power of suppliers for Dropbox is a complex interplay of market dynamics, technological dependence, and talent acquisition. While the commoditization of basic cloud infrastructure limits the power of some suppliers, the concentration of major cloud providers like AWS, Azure, and Google Cloud, along with the increasing reliance on specialized technologies and scarce talent, grants significant leverage to others.

The high switching costs associated with cloud infrastructure migrations, often running into millions of dollars, solidify the position of incumbent providers. Furthermore, Dropbox's strategic acquisitions of companies with unique AI and governance technologies underscore a growing dependence on specialized suppliers whose expertise is critical for product differentiation.

This dependence, coupled with the scarcity of highly skilled cloud professionals, drives up operational costs. For instance, senior cloud engineers in 2024 could command salaries exceeding $170,000 annually, directly impacting Dropbox's expenditure on talent acquisition and retention.

| Supplier Type | Leverage Factors | Impact on Dropbox |

|---|---|---|

| Hyperscale Cloud Providers (AWS, Azure, Google Cloud) | Market dominance (AWS ~31% market share in 2024), high switching costs (millions of dollars) | Significant influence on pricing and service terms, operational dependence |

| Specialized Technology Providers (AI, Security, Data Management) | Proprietary/unique offerings, essential for competitive differentiation | Potential for higher pricing, increased reliance for product enhancement |

| Talent Pool (Cloud Architects, Cybersecurity Experts) | Scarcity of specialized skills, high demand | Increased labor costs (avg. senior cloud engineer >$170k in 2024), recruitment challenges |

What is included in the product

This analysis dissects the competitive forces impacting Dropbox, revealing the intensity of rivalry, the power of buyers and suppliers, the threat of new entrants and substitutes, and ultimately, Dropbox's strategic positioning.

Instantly visualize competitive pressures with a dynamic, interactive Porter's Five Forces model for Dropbox, enabling faster strategic adjustments.

Customers Bargaining Power

Low Switching Costs for Freemium Users

Dropbox's freemium strategy means that users can switch between services with minimal financial outlay. This low barrier to entry for free users directly amplifies their bargaining power. For instance, if a user finds a competitor offering similar storage for free, the cost of moving their files is negligible.

The seamless migration of data to alternatives like Google Drive or Microsoft OneDrive, both of which offer substantial free storage tiers, further empowers consumers. This ease of switching compels Dropbox to constantly enhance its offerings to retain users and encourage upgrades to paid plans, as evidenced by the competitive landscape in cloud storage where user acquisition is often driven by free service tiers.

Abundance of Alternatives

The cloud storage market is incredibly crowded, meaning Dropbox customers have loads of other options. Think of giants like Google Drive and Microsoft OneDrive, which often come bundled with their other services, giving users a readily available alternative. There are also many smaller, specialized cloud storage providers catering to specific needs.

This abundance of choices significantly shifts power to the customer. They can easily compare features, pricing, and storage capacities across various platforms. For instance, in 2024, the global cloud storage market size was estimated to be around $100 billion, highlighting the sheer number of providers vying for market share and the competitive pressure this creates.

Customers can readily switch providers if they find a better deal or service elsewhere. This ease of switching, coupled with the widespread availability of similar functionalities, means customers don't feel locked into any single provider. They can demand better terms or simply move to a competitor if Dropbox's offerings aren't meeting their expectations.

Price Sensitivity, Especially for Basic Storage

Customers seeking basic cloud storage are highly sensitive to price. This is particularly true given the prevalence of free storage tiers offered by numerous competitors. Dropbox's pricing power for these fundamental services is therefore limited by this price-conscious market segment.

The competitive environment further pressures Dropbox on pricing. Rivals often package storage with broader productivity suites or offer more substantial free storage options. This makes it challenging for Dropbox to command premium prices for its standalone basic storage. For instance, in 2024, the average cost per gigabyte of cloud storage continued to decline across the industry, reflecting this intense price competition.

Value Proposition for Paid Users

While individual Dropbox users might be quite sensitive to price, particularly for basic storage needs, the company's strategic shift towards business and enterprise clients significantly alters this dynamic. These larger customers often place a higher premium on robust features such as advanced collaboration tools, stringent security protocols, compliance certifications, and seamless integration with existing business software. For instance, as of early 2024, many businesses are looking for cloud solutions that can streamline workflows and enhance team productivity, making these features more critical than marginal cost differences.

Dropbox actively works to reduce the bargaining power of its customers by enhancing the perceived value of its paid offerings. Features like Dropbox Paper, designed for collaborative document creation, and HelloSign, an e-signature solution, aim to increase customer reliance and reduce churn. This focus on integrated business solutions makes it more costly and disruptive for enterprises to switch to a competitor, thereby diminishing their leverage.

- Enterprise Focus: Dropbox's investment in enterprise-grade features directly addresses the needs of business customers, making them less likely to switch based on price alone.

- Value-Added Services: Tools like Dropbox Paper and HelloSign increase customer stickiness by providing essential business functionalities beyond basic file storage.

- Integration Benefits: Seamless integration with other business applications (e.g., Microsoft Office, Salesforce) further embeds Dropbox into customer workflows, reducing the incentive to seek alternatives.

Data Portability and Interoperability

The increasing emphasis on data portability and interoperability significantly bolsters customer bargaining power within the cloud storage market. This trend allows users to migrate their data seamlessly between providers, diminishing the impact of vendor lock-in. For instance, by 2024, a significant portion of cloud users expressed a desire for easier data transfer capabilities, with surveys indicating over 60% prioritizing this feature when choosing a provider.

Open APIs and standardized data formats are key drivers of this shift. These technologies enable customers to integrate cloud storage services with a multitude of other applications, further reducing dependency on any single platform. This enhanced flexibility means customers can readily switch if a competitor offers better pricing or features, directly pressuring existing providers.

- Data Portability Trend: Customer demand for easy data migration between cloud services is a growing concern for providers.

- Open APIs Impact: Integration with diverse applications via open APIs reduces customer reliance on a single vendor.

- Reduced Vendor Lock-in: Customers are less committed to a provider when data transfer is straightforward, increasing their leverage.

- Competitive Pressure: The ease of switching providers due to portability forces Dropbox to remain competitive on pricing and service.

Cloud Storage Customers Hold the Power Amidst Fierce Competition

The bargaining power of Dropbox's customers is notably high, especially for individuals and small businesses. This is largely due to the abundance of competing cloud storage solutions, many of which offer comparable free tiers. For instance, in 2024, services like Google Drive and Microsoft OneDrive, often bundled with their respective productivity suites, provided substantial free storage, making it easy for users to switch without incurring costs.

This ease of switching is further amplified by increasing data portability and interoperability standards. Customers can readily move their files, meaning they are not locked into any single provider and can demand better terms or simply migrate if unsatisfied. The sheer volume of choices available in the roughly $100 billion global cloud storage market in 2024 means customers hold significant leverage.

| Factor | Impact on Dropbox | Supporting Data (2024 Estimates) |

|---|---|---|

| Availability of Substitutes | High | Cloud storage market valued at ~$100 billion globally. Numerous competitors (Google Drive, OneDrive, iCloud) offer free tiers. |

| Switching Costs (for basic users) | Low | Minimal financial outlay for free users; data migration is generally straightforward. |

| Price Sensitivity (for basic users) | High | Prevalence of free storage tiers by competitors limits Dropbox's pricing power for basic services. |

| Customer Importance | Varies (High for Enterprise) | Individual users are price-sensitive; enterprise clients value features (security, collaboration) over minor price differences. |

Preview Before You Purchase

Dropbox Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces analysis of Dropbox, detailing industry rivalry, the threat of new entrants, the bargaining power of buyers and suppliers, and the threat of substitutes. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy. You'll gain insights into how these forces shape Dropbox's competitive landscape and strategic positioning. This analysis is crucial for understanding the sustainability of Dropbox's business model and identifying potential opportunities and threats within the cloud storage market.

Rivalry Among Competitors

High Number of Strong Competitors

The cloud storage landscape is fiercely competitive, with numerous strong players vying for market share. Dropbox directly contends with tech titans such as Google, Microsoft, and Apple. These giants leverage their vast ecosystems, often integrating storage solutions like Google Drive, OneDrive, and iCloud with their productivity suites and operating systems.

This integration creates substantial pressure on Dropbox regarding pricing and the need for continuous feature innovation. For instance, Microsoft 365 subscribers receive 1TB of OneDrive storage, making it a compelling value proposition. Similarly, Google bundles significant storage with its Workspace offerings. Apple's iCloud is deeply embedded within its hardware ecosystem, making it a natural choice for iPhone and Mac users.

Product Differentiation is Key but Challenging

While basic cloud storage feels like a commodity, companies like Dropbox work hard to offer unique advantages. They differentiate through advanced features, seamless collaboration tools, robust security, and a smooth user experience. Dropbox, for instance, emphasizes its intuitive design, reliable synchronization, and deep integrations with popular platforms like Adobe Creative Cloud, Zoom, and Slack, aiming to capture user loyalty.

However, this differentiation is a constant battle. Competitors aren't standing still; they are also continuously investing in innovation to offer comparable or superior features. This dynamic means that while differentiation is crucial for survival and growth in the cloud storage market, it's also incredibly challenging to maintain a significant, lasting edge.

Aggressive Pricing Strategies

The competitive landscape for cloud storage is intensely shaped by aggressive pricing, with major rivals like Google Drive and Microsoft OneDrive offering substantial free storage tiers. This forces Dropbox to constantly reassess its pricing for paid plans to remain competitive. For instance, as of mid-2024, Google One offers plans starting at 100GB for $1.99/month, while Microsoft OneDrive provides 100GB for $1.99/month, directly challenging Dropbox's own tiered offerings.

Competitors often leverage their broader ecosystems to bundle storage at attractive price points, putting pressure on Dropbox's margins. Microsoft 365 subscriptions, for example, include 1TB of OneDrive storage, making it a difficult value proposition to beat for users already invested in the Microsoft ecosystem. This widespread availability of competitively priced or bundled storage makes it challenging for Dropbox to solely rely on storage capacity as its primary differentiator.

Industry Growth Attracts and Sustains Rivalry

The cloud storage market's robust expansion is a magnet for fierce competition. This booming sector is expected to grow from $124.57 billion in 2025 to a substantial $273.05 billion by 2029, demonstrating a compound annual growth rate of 21.7%. Such impressive growth naturally attracts numerous players, all eager to capture a piece of this expanding pie.

This high growth environment intensifies rivalry as companies pour resources into innovation. To stand out and secure market share, businesses are heavily investing in cutting-edge technologies, particularly artificial intelligence (AI) and machine learning (ML). These advancements are crucial for developing differentiated services and enhancing user experience.

- Market Growth Fuels Competition: The cloud storage market's projected growth to $273.05 billion by 2029 attracts many competitors.

- Investment in Technology: Companies are investing heavily in AI and ML to gain a competitive edge.

- Vying for Market Share: Rapid expansion means intense competition for customer acquisition and retention.

- Innovation as a Differentiator: New technologies are key to distinguishing services in a crowded market.

Strategic Partnerships and Ecosystem Lock-in

Competitors frequently leverage their established ecosystems, like Microsoft 365 and Google Workspace, to deeply integrate cloud storage. This seamless integration fosters significant customer lock-in, making it challenging for users to switch providers. For instance, Microsoft's OneDrive is a core component of Windows and Office, providing a deeply embedded user experience.

Dropbox actively combats this by forging strategic partnerships and broadening its service portfolio. By introducing features such as document automation and advanced AI-powered search capabilities, Dropbox aims to create a more comprehensive and indispensable ecosystem for its users, thereby reducing the incentive to leave.

- Ecosystem Integration: Competitors like Microsoft and Google benefit from deeply integrated cloud storage within their broader software suites.

- Customer Lock-in: This integration creates strong switching costs for users invested in these ecosystems.

- Dropbox's Strategy: Dropbox counters by building its own ecosystem through strategic alliances and expanded feature sets.

- Value Enhancement: New offerings like document automation and AI search aim to increase Dropbox's utility and user stickiness.

Cloud Storage Wars: Differentiating Amidst Giants

The competitive rivalry within cloud storage is intense, primarily driven by tech giants like Google, Microsoft, and Apple. These companies leverage their extensive ecosystems, bundling cloud storage with operating systems and productivity suites, creating significant pricing pressure and demanding continuous innovation from Dropbox.

Dropbox must differentiate itself through features like seamless collaboration and robust security to counter the value offered by integrated solutions. For example, Microsoft 365 subscribers get 1TB of OneDrive storage, a compelling offer that challenges Dropbox's standalone plans.

The market's rapid growth, projected to reach $273.05 billion by 2029, fuels this competition, leading to heavy investment in AI and ML for service enhancement. This dynamic necessitates constant adaptation and a strong value proposition to retain users against deeply integrated competitors.

| Competitor | Key Offering | Pricing Example (Monthly) |

|---|---|---|

| Microsoft OneDrive | Integrated with Microsoft 365, 1TB storage | $6.99 (Microsoft 365 Personal) |

| Google Drive | Part of Google Workspace, 2TB storage | $9.99 (Google One Premium) |

| Apple iCloud | Integrated with Apple devices, 200GB storage | $2.99 (iCloud+) |

| Dropbox | Focus on collaboration and sync, 2TB storage | $11.99 (Dropbox Plus) |

SSubstitutes Threaten

Traditional On-Premises Storage

Traditional on-premises storage, while declining in individual use, remains a significant substitute for businesses, particularly those with stringent regulatory or security needs. These systems offer unparalleled data control, a key differentiator for many organizations, despite their higher initial investment and ongoing maintenance costs.

For instance, in 2024, many enterprises continued to invest in on-premises infrastructure to meet data sovereignty laws or safeguard highly sensitive intellectual property, often citing greater physical security and direct management capabilities as primary drivers. This preference, however, comes with a substantial price tag, as the total cost of ownership for on-premises solutions typically outpaces cloud-based alternatives.

Physical Storage Devices

For individual users, physical storage devices like external hard drives and USB flash drives continue to serve as substitutes for cloud storage. These options are particularly appealing for local backups or when internet access is unreliable, offering a tangible alternative to digital cloud services.

While cloud storage boasts superior collaboration and remote access, some individuals still prefer physical media for highly sensitive data, viewing it as a more secure option. This perception of enhanced security, coupled with the absence of internet dependency, keeps these physical alternatives relevant in the market.

The market for external hard drives and SSDs remains robust, with global sales of external SSDs projected to grow significantly. For instance, the external SSD market was valued at over $15 billion in 2023 and is expected to see a compound annual growth rate of around 15% through 2030, indicating continued consumer demand for these physical storage solutions.

Email Attachments and Direct File Transfer

Email attachments and direct file transfer, like peer-to-peer sharing or secure FTP, present a substitute threat for cloud storage services. These methods can be sufficient for very basic needs, such as sending a single document to one person.

However, their utility diminishes rapidly when dealing with larger files or collaborative projects. For instance, email attachment size limits, often around 25MB, are a significant constraint compared to the gigabytes or terabytes offered by cloud solutions.

Furthermore, these simpler methods lack crucial features such as robust version control, which is vital for tracking changes in collaborative documents, and centralized management for multiple users and files.

This makes them poor substitutes for businesses or individuals requiring organized, scalable, and collaborative file sharing, especially as cloud storage adoption continues to grow; by 2024, the global cloud storage market size was valued at over $100 billion.

Specialized Collaboration and Project Management Tools

The threat of substitutes for Dropbox is significant, particularly from integrated collaboration and project management tools. Many platforms like Microsoft Teams, Slack, and even specialized tools such as Asana and Trello now offer robust file-sharing and storage capabilities directly within their workflows.

This integration means users can manage documents, share updates, and collaborate on projects all within a single application, diminishing the perceived need for a standalone cloud storage solution. For instance, Microsoft 365's deep integration of OneDrive with Teams allows for seamless file management directly in chat and channel conversations.

This trend is further amplified by the increasing demand for streamlined digital workspaces. By consolidating functionalities, these alternative platforms reduce friction and improve efficiency for teams, making them attractive substitutes.

- Integrated File Management: Collaboration platforms offer built-in file storage and sharing, reducing reliance on separate cloud services.

- Workflow Consolidation: Tools like Microsoft Teams and Slack allow users to manage documents within their existing communication and project management workflows.

- Reduced Perceived Need: As these features become standard, the unique value proposition of dedicated cloud storage providers can be diluted.

- Market Trends: The push for unified digital workspaces makes solutions that bundle storage with collaboration highly appealing.

Hybrid Cloud and Edge Computing Solutions

The increasing popularity of hybrid cloud setups, which blend private data centers with public cloud services, presents a significant substitute for purely cloud-based storage solutions. This approach allows businesses to keep sensitive data on-premises while leveraging the cloud for other workloads, potentially lessening dependence on a single public cloud provider. For instance, by Q3 2024, a significant portion of enterprises were actively implementing hybrid cloud strategies to optimize cost and performance.

Edge computing is also emerging as a notable substitute, especially for applications requiring low latency and real-time data processing. By processing data closer to where it's generated, edge solutions can reduce the need for constant data transfer to a central cloud, offering an alternative for certain data handling requirements. This trend is driven by the proliferation of IoT devices, with the global edge computing market projected to reach hundreds of billions of dollars by the end of the decade.

- Hybrid Cloud Adoption: Businesses increasingly adopt hybrid models to balance on-premises security with cloud scalability.

- Edge Computing Growth: Edge solutions process data locally, reducing reliance on centralized cloud storage for specific use cases.

- Reduced Cloud Dependence: These technologies offer alternative data storage and processing strategies, potentially fragmenting market share for dominant cloud providers.

- Performance and Latency Benefits: Edge computing, in particular, addresses needs where proximity to data sources is critical, offering a distinct advantage over traditional cloud models for certain applications.

Storage Alternatives: A Multifaceted Challenge

The threat of substitutes for Dropbox is multifaceted, encompassing traditional storage, integrated collaboration tools, and emerging technologies. While cloud storage offers convenience, alternatives address specific needs like security, cost, or workflow integration. The market continues to evolve, with new solutions constantly challenging the status quo for cloud-based file sharing and storage.

Integrated collaboration platforms like Microsoft Teams and Slack have become significant substitutes by embedding file storage and sharing directly into communication workflows. This consolidation reduces the need for a separate cloud storage service. For example, Microsoft 365's deep integration of OneDrive with Teams allows users to manage files seamlessly within chat and channel conversations, a key driver for efficiency in 2024.

Emerging technologies such as hybrid cloud and edge computing also present substitute threats. Hybrid cloud strategies allow businesses to maintain sensitive data on-premises while leveraging public cloud for other functions, potentially reducing reliance on a single provider. Edge computing, by processing data closer to its source, offers an alternative for applications demanding low latency, thereby lessening the need for constant cloud data transfer.

| Substitute Category | Key Features | Impact on Dropbox | 2024 Market Context |

| On-Premises Storage | High security, data control | Relevant for specific enterprise needs | Continued investment by businesses for regulatory compliance |

| Collaboration Platforms (e.g., Teams, Slack) | Integrated file sharing, workflow consolidation | Reduces need for standalone cloud storage | Deep integration of OneDrive with Teams is a prime example |

| Physical Storage (e.g., External HDDs) | Tangible, offline access | Niche appeal for backups, offline use | External SSD market expected strong growth |

| Hybrid/Edge Computing | Data proximity, flexibility | Offers alternative data handling strategies | Growing enterprise adoption of hybrid cloud models |

Entrants Threaten

High Capital Investment for Infrastructure

Building a cloud storage service from scratch demands immense upfront capital. Think about the cost of constructing and outfitting data centers, purchasing vast quantities of servers, and ensuring top-notch networking capabilities. This isn't pocket change; it's a multi-billion dollar undertaking.

For instance, major cloud providers like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform have invested tens of billions of dollars annually in their infrastructure. In 2023 alone, these companies continued their aggressive expansion, with capital expenditures on data centers and related hardware running into the tens of billions, creating a formidable barrier for any newcomer aiming to compete at a similar scale.

This sheer scale of investment, particularly for hyperscale operations, effectively deters most potential competitors. It's a significant hurdle that requires not just deep pockets but also a long-term strategic commitment, making it incredibly difficult for new, smaller players to establish a meaningful presence in the market.

Economies of Scale and Cost Advantages of Incumbents

Dropbox, like many established tech companies, benefits from substantial economies of scale. This means that as their user base grows, their cost per user actually decreases. For instance, in 2023, Dropbox reported a substantial portion of its revenue was derived from its large existing customer base, enabling them to invest heavily in infrastructure and development without drastically increasing per-unit costs.

New entrants would face a steep challenge in replicating these cost advantages. Building a comparable infrastructure and marketing to attract a critical mass of users to achieve similar economies of scale would require immense capital investment. Without this scale, a new service would likely have higher operational costs per user, making it difficult to compete on price with a mature player like Dropbox.

Brand Recognition and User Trust

New entrants face a significant hurdle due to Dropbox's strong brand recognition and over 700 million registered users as of late 2023. Establishing a comparable level of trust and loyalty in the cloud storage market, where data security is paramount, is a formidable barrier for emerging companies.

Technological Complexity and Expertise

The development and ongoing maintenance of a robust cloud storage platform demand considerable technological sophistication. This includes building and managing secure, scalable, and highly reliable infrastructure, which requires deep expertise in areas like distributed systems, data encryption, and network engineering.

New competitors entering the market face a steep learning curve and substantial investment in acquiring the necessary technical capabilities. This technological barrier means that simply having capital isn't enough; a strong foundation in advanced IT is crucial.

The talent pool for these specialized skills is also a significant factor. Companies like Dropbox invest heavily in attracting and retaining top-tier engineers and cybersecurity professionals. In 2024, the demand for cloud computing and cybersecurity talent remained exceptionally high, with average salaries for senior cloud engineers often exceeding $150,000 annually in major tech hubs.

New entrants must therefore not only develop cutting-edge technology but also successfully recruit and retain a team with the requisite expertise to compete effectively. This talent acquisition challenge is a substantial deterrent.

- High Capital Investment: Significant upfront costs for infrastructure, R&D, and talent acquisition.

- Specialized Skill Requirements: Need for expertise in cloud architecture, cybersecurity, and data management.

- Talent Scarcity: Competition for skilled engineers and IT professionals drives up labor costs.

- Rapid Technological Evolution: Continuous investment is needed to keep pace with advancements in cloud technology.

Regulatory and Compliance Hurdles

The cloud storage sector faces a significant threat from new entrants due to stringent regulatory and compliance hurdles, particularly concerning data privacy. Companies like Dropbox must continuously adapt to evolving regulations such as GDPR, which mandates strict data handling protocols. New players entering this market must invest heavily in understanding and adhering to these complex legal frameworks across multiple regions, creating a substantial barrier to entry. For instance, achieving compliance with HIPAA for healthcare data storage adds another layer of complexity and cost.

Navigating these requirements translates into considerable operational overhead and inherent risk for any new company, especially those targeting enterprise clients who demand robust data protection and compliance assurances. The ongoing need to update systems and policies to meet new legislation, such as potential future data localization mandates or evolving cybersecurity standards, further amplifies this challenge. These compliance costs can represent a significant portion of a new entrant's initial capital expenditure, potentially deterring smaller or less-resourced competitors.

- Data Privacy Regulations: Evolving global standards like GDPR and CCPA significantly increase compliance burdens.

- Jurisdictional Complexity: Operating across multiple countries requires adherence to diverse and often conflicting legal requirements.

- Operational Overhead: New entrants must allocate substantial resources to legal, IT, and security infrastructure for compliance.

- Enterprise Focus Risk: Businesses targeting enterprise clients face higher scrutiny and demand for certified compliance, amplifying entry barriers.

Why New Cloud Storage Players Face Uphill Battle

The threat of new entrants in cloud storage remains moderate, primarily due to the substantial capital required for infrastructure and the need for specialized technical expertise. While the market is attractive, the high barriers to entry, including data center construction and talent acquisition, limit the number of genuinely disruptive new players. Established brands also possess significant customer loyalty and brand recognition that new competitors must overcome.

Porter's Five Forces Analysis Data Sources

Our Dropbox Porter's Five Forces analysis is built on a foundation of public company filings, industry analyst reports, and market research data. We also leverage news archives and competitor announcements to capture real-time market dynamics and strategic moves.