Commercial Bank of Qatar Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Commercial Bank of Qatar Bundle

From Overview to Strategy Blueprint

The Commercial Bank of Qatar operates within a dynamic financial landscape, influenced by factors like intense rivalry among existing banks and the significant bargaining power of its customers. Understanding these forces is crucial for strategic planning.

The complete report reveals the real forces shaping Commercial Bank of Qatar’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Technology and Infrastructure Providers

The bargaining power of technology and infrastructure providers for Commercial Bank of Qatar is generally considered moderate to high. Banks today are deeply dependent on advanced IT systems, specialized software, and robust cybersecurity measures, often sourced from a select group of vendors.

The significant costs and complexities associated with switching core banking platforms mean these suppliers can wield considerable influence. For instance, in 2023, global IT spending by financial institutions was projected to reach over $600 billion, highlighting the critical nature of these services and the potential leverage of providers in such a market.

Sources of Capital and Funding

The bargaining power of capital suppliers for Commercial Bank of Qatar (CBQ) is generally considered moderate. This includes entities like interbank lenders, large institutional investors, and access to central bank facilities. CBQ, like other banks, relies on a steady flow of funds, but the breadth of global and local financial markets provides multiple avenues for sourcing capital.

However, this power can shift. During periods of tight liquidity or specific economic downturns, the cost of borrowing and the sheer availability of funds can escalate, giving suppliers more leverage. For instance, in early 2024, global interest rate hikes, while beneficial for lending margins, also increased the cost of wholesale funding for many banks, illustrating this dynamic.

Skilled Human Capital

The bargaining power of highly skilled human capital is significant for Commercial Bank of Qatar (CBQ). Talent in areas like digital transformation, cybersecurity, and sophisticated wealth management is in high demand globally and locally, driving up compensation expectations. This intensified competition for specialized expertise means banks must offer attractive packages to secure and retain top performers, directly impacting operational costs and innovation capacity.

Payment Network Operators

Payment network operators, such as Visa and Mastercard, wield considerable bargaining power over commercial banks. Their essential function in processing a vast majority of card transactions makes banks reliant on their infrastructure. This reliance is amplified by the extensive merchant and consumer adoption of these networks, creating a high barrier for banks seeking to switch or negotiate unfavorable terms.

The dominance of these networks means that banks have limited leverage. For instance, in 2023, global digital payment transaction volumes continued their upward trajectory, with card networks being a primary facilitator. This widespread usage underscores the dependency of financial institutions on these operators for their payment processing services, thereby strengthening the suppliers' negotiating position.

- Visa and Mastercard's extensive global reach and established infrastructure are key drivers of their bargaining power.

- Banks are dependent on these networks for the processing of credit and debit card transactions, limiting their ability to dictate terms.

- The widespread consumer and merchant acceptance of major payment networks reduces the viability of alternatives for banks.

Regulatory and Compliance Service Providers

Providers of regulatory and compliance services hold significant bargaining power over commercial banks. The highly regulated nature of the banking sector means that adherence to evolving rules is paramount, making specialized software, advisory, and audit firms essential partners. Failure to comply can result in substantial fines and reputational damage, underscoring the critical role these service providers play.

For instance, in 2024, the global regulatory compliance market was valued at approximately $150 billion, with a projected compound annual growth rate of over 15% through 2030, indicating strong demand and the increasing reliance of financial institutions on these specialized services. This robust market growth reflects the complexity and constant updates in financial regulations worldwide.

- Criticality of Compliance: Banks must navigate a complex web of regulations, making compliance service providers indispensable for operational integrity and avoiding penalties.

- Market Growth: The global regulatory compliance market's expansion, projected to exceed $300 billion by 2030, highlights the increasing reliance and inherent power of these specialized firms.

- Specialized Expertise: The niche knowledge and technical capabilities offered by these providers are difficult for banks to replicate internally, further strengthening their bargaining position.

Bank's Supplier Dynamics: Power Play

The bargaining power of suppliers for Commercial Bank of Qatar (CBQ) is a multifaceted issue, with several key groups wielding significant influence. Technology providers, capital sources, skilled labor, payment networks, and regulatory compliance firms all represent areas where CBQ must navigate supplier relationships carefully.

The increasing reliance on sophisticated IT infrastructure and cybersecurity solutions means technology vendors can command strong positions, especially given the high costs and complexity of switching core banking systems. Similarly, the essential role of payment networks like Visa and Mastercard in facilitating transactions grants them considerable leverage due to widespread consumer and merchant adoption.

Capital suppliers, while generally diverse, can exert more power during periods of tight liquidity or economic uncertainty, as seen with the impact of global interest rate hikes on wholesale funding costs in early 2024. The demand for specialized talent in areas like digital banking and cybersecurity also means human capital suppliers can negotiate favorable terms.

| Supplier Category | Bargaining Power Level | Key Factors Influencing Power |

|---|---|---|

| Technology & Infrastructure Providers | Moderate to High | Dependence on advanced IT, high switching costs, limited vendor options. |

| Capital Suppliers (e.g., interbank lenders) | Moderate | Access to diverse global/local markets, but can increase during liquidity crunches. |

| Highly Skilled Human Capital | Significant | High demand for specialized skills (digital, cybersecurity), competitive talent market. |

| Payment Network Operators (Visa, Mastercard) | Considerable | Essential infrastructure, extensive adoption, high barriers to switching. |

| Regulatory & Compliance Service Providers | Significant | Criticality of compliance, specialized expertise, growing market for these services. |

What is included in the product

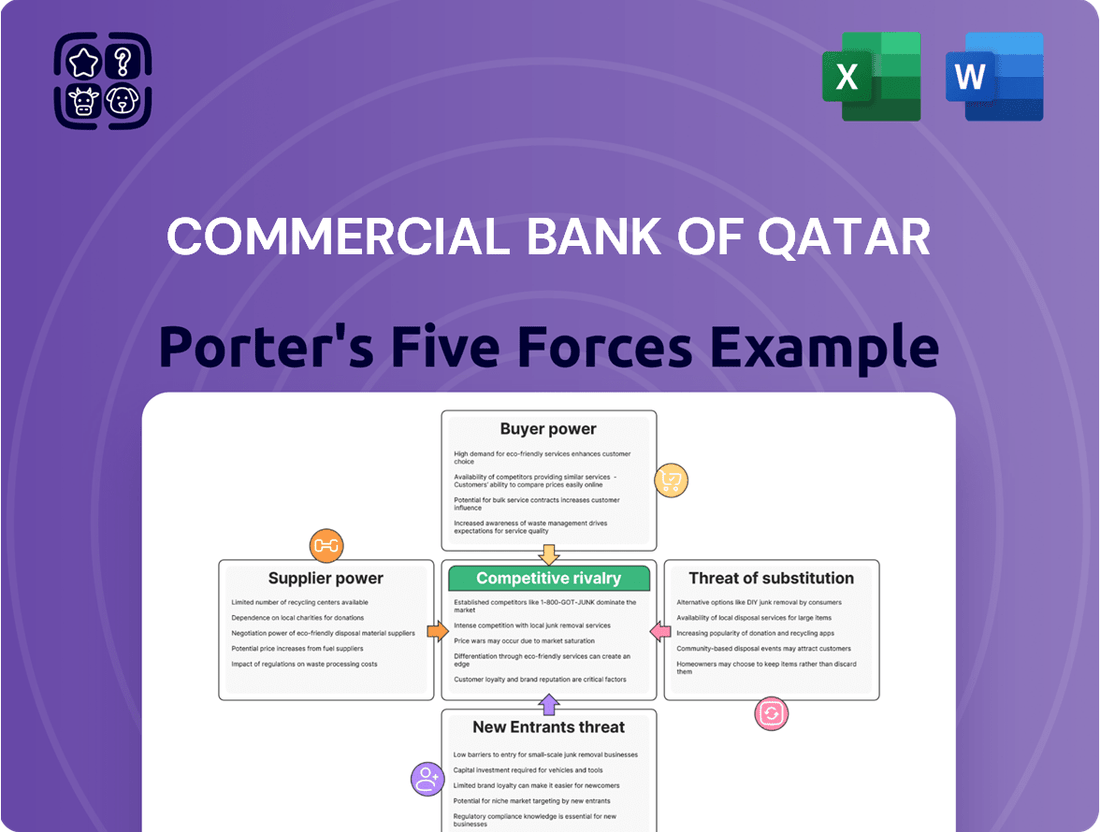

Tailored exclusively for Commercial Bank of Qatar, analyzing its position within its competitive landscape by examining the intensity of rivalry, bargaining power of buyers and suppliers, threat of new entrants, and the impact of substitutes.

Easily identify and mitigate competitive threats by visualizing the intensity of each of Porter's Five Forces impacting the Commercial Bank of Qatar.

Customers Bargaining Power

Retail Banking Customers

For retail banking customers in Qatar, the bargaining power typically remains low. This is largely due to the significant switching costs involved in changing banks, which include updating direct debits, loan agreements, and the hassle of transferring credit history. While digital banking and competitive product offerings are starting to give customers a bit more leverage, especially for straightforward accounts, the overall impact on their bargaining power is still relatively contained.

Corporate and Institutional Clients

Corporate and institutional clients, particularly major corporations and government bodies, wield considerable bargaining power in the banking sector. Their substantial transaction volumes and intricate financial requirements allow them to negotiate highly customized terms and pricing, giving them significant leverage. For instance, in 2024, large corporate clients often command lower fees and better interest rates due to the sheer scale of their business, a trend that intensifies competition among banks vying for their patronage.

Availability of Information and Digital Tools

Customers in Qatar's banking sector now wield significant power due to readily accessible information online. They can easily compare product features, interest rates, and service quality across different commercial banks, a stark contrast to previous eras. This transparency empowers them to make more informed decisions, directly influencing bank pricing and service strategies.

The proliferation of digital tools and financial aggregators further amplifies customer bargaining power. Platforms allow individuals and businesses to quickly identify the most competitive offerings, forcing banks like Commercial Bank of Qatar to constantly innovate and maintain attractive terms. For instance, in 2024, the average personal loan interest rate in Qatar hovered around 5-7%, with digital platforms enabling customers to pinpoint the banks offering rates at the lower end of this spectrum.

Low Switching Costs for Certain Products

While changing banks entirely can be a complex process, the bargaining power of customers is amplified when considering specific, easily transferable products. For instance, customers can readily shift simple savings accounts or certain unsecured loans to a competitor offering more attractive interest rates or superior digital services. This ease of movement is particularly pronounced in today's increasingly connected financial landscape.

The ability for customers to switch certain products with minimal friction directly impacts commercial banks like those in Qatar. In 2024, the fintech sector continued to grow, offering streamlined digital onboarding and account management, further reducing switching costs for basic banking needs. For example, some neobanks in the region reported customer acquisition rates that were significantly driven by competitive rates on savings products, indicating a clear customer sensitivity to better offers.

- Low Switching Costs for Simple Products: Customers can easily move savings accounts or unsecured loans to competitors offering better rates or services.

- Digitalization Amplifies Mobility: The rise of digital banking and fintech solutions makes it simpler than ever for customers to compare and switch providers for specific financial products.

- Impact on Deposit Rates: Banks face pressure to offer competitive rates on easily switchable deposits to retain customer funds, as evidenced by market trends in the Middle East.

- Competitive Pressure on Loan Products: Similarly, for unsecured lending, banks must remain competitive on pricing and terms to prevent customers from seeking alternatives.

Customer Segmentation and Value

The bargaining power of customers in Qatar's banking sector is heavily influenced by how they are segmented and the overall value they represent to institutions like Commercial Bank of Qatar. High-net-worth individuals and large corporate clients, due to their substantial deposits, borrowing needs, and potential for cross-selling, wield considerable influence. For instance, in 2024, large corporate clients were estimated to account for a significant portion of the loan portfolios of major Qatari banks, giving them leverage in negotiating terms and pricing.

Conversely, the bargaining power of the average retail customer is generally lower. Banks strategically segment their customer base to offer differentiated services and pricing structures that acknowledge these power differences. This segmentation allows banks to optimize their offerings, from personalized wealth management for high-value clients to standardized digital services for the broader retail market, reflecting the varying levels of customer influence.

- Customer Value Drives Bargaining Power: High-net-worth individuals and large corporations possess greater negotiation leverage due to their significant financial contributions.

- Segmentation Reflects Power: Banks segment customers to tailor services and pricing, acknowledging the varying power dynamics between different customer groups.

- Corporate Clients' Influence: Large corporate clients in Qatar, representing substantial portions of bank loan books, can negotiate more favorable terms.

Customer Power: Shifting Dynamics in Banking

The bargaining power of customers for Commercial Bank of Qatar is a mixed bag, largely depending on the customer segment. While retail customers have limited individual power, corporate clients can negotiate significant terms due to their transaction volumes.

Digitalization and increased transparency empower all customers to compare offerings, forcing banks to remain competitive. This means even smaller customers can exert pressure by easily switching to better deals, especially for straightforward products.

In 2024, the growth of fintech and readily available online comparisons meant that customers could more easily identify and move to banks offering superior rates or services, particularly for savings and unsecured loans.

| Customer Segment | Bargaining Power | Key Drivers |

|---|---|---|

| Retail Customers | Low to Moderate | Switching costs, digital comparison tools, ease of moving simple products |

| Corporate Clients | High | Transaction volume, customized needs, potential for large deposits and loans |

| High-Net-Worth Individuals | Moderate to High | Significant assets under management, demand for personalized services |

What You See Is What You Get

Commercial Bank of Qatar Porter's Five Forces Analysis

This preview showcases the exact Porter's Five Forces analysis for the Commercial Bank of Qatar you will receive. It meticulously details the competitive landscape, including the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the Qatari banking sector. You're looking at the actual document; once you complete your purchase, you’ll get instant access to this exact file, ready for your strategic planning.

Rivalry Among Competitors

Number and Size of Competitors

The Qatari banking landscape features a moderate number of significant local institutions, such as Qatar National Bank (QNB), Doha Bank, and Masraf Al Rayan, all competing directly with Commercial Bank of Qatar. These well-established, diversified banks actively vie for market share across various banking services.

This concentration of strong players fuels a competitive environment where differentiation through superior service, advanced digital platforms, and innovative product development is crucial for success. For instance, QNB, as of early 2024, maintained a dominant market position with total assets exceeding QAR 1.1 trillion, highlighting the scale of competition.

Market Growth Rate

The Qatari banking sector's growth is closely tied to the nation's economic diversification and substantial government investment. This generally creates a favorable environment for expansion. However, when certain banking segments mature or if the overall economy experiences a slowdown, competition among banks can become much fiercer. This heightened rivalry often manifests as price competition and aggressive marketing campaigns as institutions fight for market share.

Product and Service Differentiation

While core banking products often face commoditization, Qatari banks are increasingly differentiating through advanced digital banking solutions and personalized wealth management. For instance, Qatar National Bank (QNB) has heavily invested in its digital channels, aiming to provide a seamless customer experience that goes beyond basic transactional services.

Specialized offerings, such as Sharia-compliant financial products, also serve as a key differentiator in the market, catering to a significant segment of the population. This focus on unique value propositions helps banks like Commercial Bank of Qatar to mitigate intense price competition and foster stronger customer relationships.

Exit Barriers

Exit barriers for commercial banks in Qatar, including Commercial Bank of Qatar, are substantial. These are driven by immense capital requirements, stringent regulatory oversight from the Qatar Central Bank, and the systemic risk associated with any bank's failure, which could destabilize the broader economy. This means that even in challenging market conditions, banks are often compelled to remain operational rather than exit.

Consequently, these high exit barriers contribute to intensified competition. Banks that might otherwise scale back operations or leave the market are incentivized to stay and continue competing, even if it means accepting lower profit margins. This persistence among existing players naturally fuels a more aggressive competitive landscape.

- High Capital Investment: Establishing and maintaining a bank requires significant capital, often in the billions of dollars, making it difficult to recoup investments upon exit.

- Regulatory Hurdles: Obtaining regulatory approval for operations, mergers, or even liquidations is a complex and lengthy process, acting as a significant deterrent to easy exit.

- Systemic Risk: The failure of a bank can have cascading effects on the financial system and the wider economy, prompting regulators to actively prevent exits that could trigger instability.

Strategic Objectives of Competitors

The strategic objectives of competing banks heavily shape the competitive landscape for Commercial Bank of Qatar (CBQ). Banks prioritizing aggressive growth and market share expansion, for instance, are likely to engage in more competitive pricing and innovative product launches. This forces CBQ to continually adapt its strategies to retain its standing in the market.

For example, many regional banks in the GCC, including those operating in Qatar, have outlined ambitious digital transformation goals. By mid-2024, several Qatari banks reported significant investments in AI-driven customer service and enhanced mobile banking platforms, aiming to capture a larger share of the digitally-savvy customer base. This focus on digital leadership intensifies the rivalry, compelling CBQ to invest in similar technologies and service enhancements to remain competitive.

- Aggressive Growth Strategies: Some competitors aim for rapid expansion, potentially through mergers, acquisitions, or aggressive lending practices, directly challenging CBQ's market position.

- Digital Transformation Focus: A key objective for many rivals is achieving digital leadership, evidenced by increased spending on fintech partnerships and advanced mobile banking solutions.

- Profitability Targets: While growth is important, many banks also maintain strong profitability objectives, leading to a balance between competitive pricing and margin protection.

- Customer Acquisition Drives: Competitors often launch targeted campaigns to attract new customers, employing attractive interest rates and loyalty programs that necessitate a strategic response from CBQ.

Qatar's Banking Battle: Digital Dominance and Market Share

The competitive rivalry within Qatar's banking sector is intense, characterized by a few dominant local players like Qatar National Bank (QNB), Doha Bank, and Masraf Al Rayan, all vying for market share against Commercial Bank of Qatar (CBQ). This rivalry is further fueled by ongoing digital transformation initiatives, with banks heavily investing in advanced platforms and AI-driven services to attract and retain customers.

The market's growth, tied to Qatar's economic diversification, generally supports expansion, but can lead to fiercer competition, especially during economic slowdowns, manifesting as aggressive pricing and marketing. Differentiation through specialized offerings like Sharia-compliant products and superior digital experiences is key. For instance, QNB's asset base exceeding QAR 1.1 trillion as of early 2024 underscores the scale of competition.

High exit barriers, including substantial capital requirements and strict regulatory oversight, compel banks to remain competitive rather than exit, intensifying the rivalry. Competitors' strategic objectives, such as aggressive growth and digital leadership, necessitate continuous adaptation from CBQ, as seen in mid-2024 reports of significant investments in AI and mobile banking by Qatari banks.

| Competitor | Approximate Asset Size (Early 2024, QAR Trillions) | Key Competitive Strategy |

|---|---|---|

| Qatar National Bank (QNB) | 1.1+ | Market dominance, digital leadership, diversified services |

| Doha Bank | ~0.10 | Customer service, digital offerings, regional expansion |

| Masraf Al Rayan | ~0.09 | Sharia-compliant finance, wealth management, digital integration |

SSubstitutes Threaten

Fintech and Digital Payment Solutions

Fintech companies pose a significant threat by offering digital payment solutions, peer-to-peer lending, and mobile wallets. These alternatives are often more convenient and cost-effective than traditional banking services, especially for everyday transactions and smaller credit needs.

For instance, the global digital payments market was valued at approximately $2.4 trillion in 2023 and is projected to grow substantially, indicating a clear shift in consumer preference towards these digital channels. This trend pressures commercial banks like CBQ to enhance their own digital capabilities to remain competitive and retain customers.

Direct Capital Markets Access

For large corporations, the ability to access capital markets directly presents a substantial alternative to traditional commercial bank loans. Companies can issue bonds or shares to raise funds, sidestepping banks for specific financial requirements, thereby diminishing the need for corporate lending services.

Non-Bank Lenders and Credit Providers

The rise of non-bank lenders, such as specialized finance companies and online platforms, presents a significant threat, particularly in the consumer and SME loan segments. These alternative providers often distinguish themselves by offering more adaptable terms and quicker approval times, appealing to borrowers who find traditional banking procedures lengthy.

For instance, in 2024, the global fintech lending market continued its robust expansion, with digital platforms facilitating billions in loans, often bypassing traditional banking infrastructure. This trend directly challenges commercial banks like Commercial Bank of Qatar (CBQ) by siphoning off market share and putting pressure on interest margins.

To counter this, CBQ must focus on enhancing the agility and efficiency of its own lending processes. Streamlining application procedures and offering more personalized, faster loan solutions are crucial steps to retain customers and remain competitive against these agile, often digitally-native, non-bank competitors.

Cryptocurrencies and Blockchain Technology

Cryptocurrencies and blockchain technology present a nascent but growing threat of substitution for traditional banking services. While not yet a mainstream alternative for daily transactions, these digital assets and their underlying technology offer potential for decentralized remittances and asset management, areas where commercial banks like CBQ operate. As regulatory clarity improves, these alternatives could siphon off market share.

The global cryptocurrency market capitalization reached approximately $2.5 trillion in early 2024, indicating significant, albeit volatile, growth. This suggests a tangible shift in how some individuals and entities view and utilize financial assets, potentially bypassing traditional banking channels for certain activities.

- Decentralized Finance (DeFi): DeFi platforms built on blockchain offer lending, borrowing, and trading services outside traditional financial institutions, potentially reducing reliance on commercial banks.

- Remittances: Blockchain-based remittance services can offer lower fees and faster transaction times compared to traditional methods, posing a threat to established players.

- Digital Assets as Stores of Value: Cryptocurrencies like Bitcoin are increasingly perceived by some as a store of value, competing with traditional savings and investment products offered by banks.

Wealth Management and Investment Platforms

Online investment platforms, robo-advisors, and independent wealth management firms present a significant threat of substitutes to Commercial Bank of Qatar's (CBQ) wealth management services. These alternatives frequently boast lower fee structures and enhanced accessibility, drawing in investors who might otherwise engage with CBQ's private banking or asset management divisions. For instance, the global robo-advisory market was projected to reach over $2.6 trillion in assets under management by 2024, indicating a strong shift towards digital and cost-effective investment solutions.

CBQ needs to actively strengthen its value proposition in wealth management to counter this trend. This involves not only competitive pricing but also emphasizing personalized advice, exclusive market insights, and superior client service that digital-only platforms may struggle to replicate. The increasing adoption of digital financial tools by younger demographics, who are often more price-sensitive, further underscores the urgency for CBQ to innovate.

- Lower Fees: Digital platforms often charge significantly less than traditional wealth managers, with some robo-advisors operating on fees as low as 0.25% of assets under management.

- Greater Accessibility: Online platforms allow for easy account opening and management from anywhere, often with lower minimum investment requirements than traditional private banking.

- Technological Advancement: Robo-advisors leverage algorithms for portfolio management, offering sophisticated yet automated investment strategies.

- Investor Preference: A growing segment of investors, particularly millennials and Gen Z, prefer digital interactions and are comfortable with technology-driven financial advice.

Digital Disruptors Challenge Traditional Banking Dominance

The threat of substitutes for Commercial Bank of Qatar (CBQ) is substantial, driven by evolving financial technologies and alternative service providers. Fintech companies, for example, offer digital payment solutions and peer-to-peer lending, often at lower costs and with greater convenience than traditional banking. The global digital payments market's valuation, projected to grow significantly from its 2023 figure of approximately $2.4 trillion, highlights this shift in consumer preference.

Furthermore, corporations increasingly access capital markets directly by issuing bonds or shares, bypassing commercial bank loans for fundraising. This trend is mirrored in the non-bank lending sector, where specialized finance companies and online platforms provide faster, more flexible loan options, particularly for consumers and SMEs. The global fintech lending market's robust expansion in 2024, facilitating billions in loans, directly challenges traditional banks by capturing market share and pressuring interest margins.

Digital investment platforms and robo-advisors also present a significant substitute threat to CBQ's wealth management services, offering lower fees and enhanced accessibility. The global robo-advisory market's projected growth to over $2.6 trillion in assets under management by 2024 underscores the increasing investor preference for these digital, cost-effective solutions. Even nascent technologies like cryptocurrencies and blockchain offer potential for decentralized remittances and asset management, areas where banks traditionally operate.

| Substitute Category | Key Offerings | Impact on CBQ | Market Trend (2024 Data/Projections) |

|---|---|---|---|

| Fintech Companies | Digital Payments, P2P Lending, Mobile Wallets | Reduced transaction fees, customer attrition for basic services | Global digital payments market valued at ~$2.4T (2023), strong growth projected |

| Capital Markets | Bond Issuance, Equity Offerings | Decreased demand for corporate lending | Continued robust activity in global debt and equity markets |

| Non-Bank Lenders | Consumer Loans, SME Financing | Loss of market share in lending segments, pressure on interest rates | Global fintech lending market facilitated billions in loans, continued expansion |

| Digital Investment Platforms | Robo-Advisors, Online Wealth Management | Competition for wealth management clients, fee compression | Robo-advisory market projected to exceed $2.6T AUM (2024) |

| Cryptocurrencies/Blockchain | Decentralized Finance (DeFi), Remittances, Digital Assets | Potential disruption of payment and asset management services | Global crypto market cap ~ $2.5T (early 2024), increasing adoption |

Entrants Threaten

Regulatory Hurdles and Capital Requirements

The threat of new entrants into Qatar's banking sector is significantly dampened by formidable regulatory barriers and substantial capital prerequisites. The Qatar Central Bank (QCB) mandates a rigorous licensing process, demanding considerable financial investment and unwavering adherence to compliance protocols, effectively discouraging potential new players.

Economies of Scale and Brand Loyalty

Existing banks, including Commercial Bank of Qatar, enjoy substantial economies of scale. This means they can spread their operational, technological, and customer acquisition costs over a larger base, making it difficult for newcomers to match their cost efficiency. For instance, in 2023, major Qatari banks reported significant asset growth, allowing for greater operational leverage.

Furthermore, decades of operation have fostered strong brand loyalty and trust among customers for established players like Commercial Bank of Qatar. This deep-rooted customer relationship and the perception of stability act as significant hurdles for new entrants attempting to capture market share and build a comparable level of credibility.

Distribution Channels and Network Effects

Incumbent banks in Qatar, like Commercial Bank of Qatar, benefit from deeply entrenched distribution channels. As of early 2024, Commercial Bank of Qatar operates a significant network of branches and ATMs across the country, facilitating widespread customer access and transaction capabilities. This physical presence, combined with their advanced digital banking platforms, creates a formidable barrier for any new entrant looking to establish a comparable reach.

Replicating this extensive infrastructure would necessitate considerable capital investment for new players. Beyond physical assets, established banks leverage network effects, particularly in payment systems. For instance, a larger customer base using Commercial Bank of Qatar’s payment solutions makes those solutions more valuable for every user, a benefit that is difficult for newcomers to quickly achieve.

Access to Funding and Liquidity

New entrants into Qatar's banking sector might struggle to secure robust funding and maintain sufficient liquidity, particularly during their formative years. Established institutions, like Commercial Bank of Qatar, benefit from deep-rooted relationships with depositors and access to interbank markets, often at more favorable rates.

In 2024, the Qatari banking sector saw a slight increase in its aggregate loan-to-deposit ratio, indicating a tightening liquidity environment for some. For instance, while Commercial Bank of Qatar maintained a healthy liquidity coverage ratio, newcomers would need substantial capital to compete for deposits and meet regulatory liquidity requirements.

- Funding Challenges: New banks must build trust to attract deposits, a process that takes time and significant marketing investment.

- Liquidity Management: Meeting stringent liquidity coverage ratios requires substantial holdings of high-quality liquid assets, which can be costly for new entrants.

- Interbank Market Access: Existing banks have established credit lines and reputations in the interbank market, facilitating easier and cheaper access to short-term funding.

- Cost of Funds: New entrants often face higher borrowing costs compared to established banks with long-standing customer bases and diversified funding streams.

Incumbent Reaction and Competitive Response

The threat of new entrants into Qatar's banking sector is significantly influenced by the potential for aggressive retaliation from established players like the Commercial Bank of Qatar (CBQ). These incumbents are likely to deploy robust strategies, including competitive pricing, intensified marketing efforts, and accelerated product development, to protect their existing market share and deter newcomers.

This strong defensive posture makes the entry landscape particularly challenging. For instance, in 2024, major Qatari banks, including CBQ, continued to focus on digital transformation and customer acquisition, signaling a commitment to maintaining their competitive edge. Any new entrant would need substantial capital and a well-defined strategy to overcome the barriers erected by these proactive responses.

- Aggressive Pricing: Incumbents may lower interest rates on loans or offer higher rates on deposits to squeeze profit margins for new entrants.

- Enhanced Marketing: Increased advertising spend and targeted campaigns can build brand loyalty and make it harder for new banks to gain traction.

- Product Innovation: Launching new digital services or specialized financial products can further solidify the position of existing banks.

- Regulatory Hurdles: Navigating Qatar's financial regulations can also serve as a significant barrier, requiring substantial investment and expertise.

Qatar's Banking Fortress: Entry Barriers Keep New Players Out

The threat of new entrants in Qatar's banking sector, including for Commercial Bank of Qatar, is low due to high capital requirements and stringent licensing by the Qatar Central Bank. Established banks benefit from economies of scale, brand loyalty, and extensive distribution networks, making it difficult for newcomers to compete on cost and reach.

New entrants face significant challenges in securing funding and maintaining liquidity, as established players like Commercial Bank of Qatar have deep depositor relationships and better access to interbank markets. In 2024, the Qatari banking sector's aggregate loan-to-deposit ratio indicated a tightening liquidity environment, further challenging new players needing substantial capital to meet regulatory liquidity coverage ratios.

| Factor | Impact on New Entrants | Example (Commercial Bank of Qatar) |

|---|---|---|

| Regulatory Barriers | High | Rigorous licensing, substantial capital needs |

| Economies of Scale | Challenging | Lower cost per transaction due to large customer base |

| Brand Loyalty | Significant hurdle | Decades of trust and established customer relationships |

| Distribution Channels | Formidable barrier | Extensive branch/ATM network and advanced digital platforms |

| Funding & Liquidity | Difficult to secure | Established depositor base and interbank market access |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for the Commercial Bank of Qatar is built upon a robust foundation of data, including the bank's annual reports, disclosures to regulatory bodies like the Qatar Central Bank, and comprehensive industry research from financial data providers such as S&P Capital IQ and Bloomberg. We also incorporate insights from reputable market research firms specializing in the MENA banking sector to ensure a thorough understanding of the competitive landscape.