Catapult Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Catapult

A Must-Have Tool for Decision-Makers

Catapult's competitive landscape is shaped by the interplay of five key forces, revealing crucial insights into its market. Understanding the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry is essential for strategic planning. This brief overview highlights the core dynamics at play, but the true depth of Catapult's strategic positioning and potential vulnerabilities lies within a comprehensive analysis.

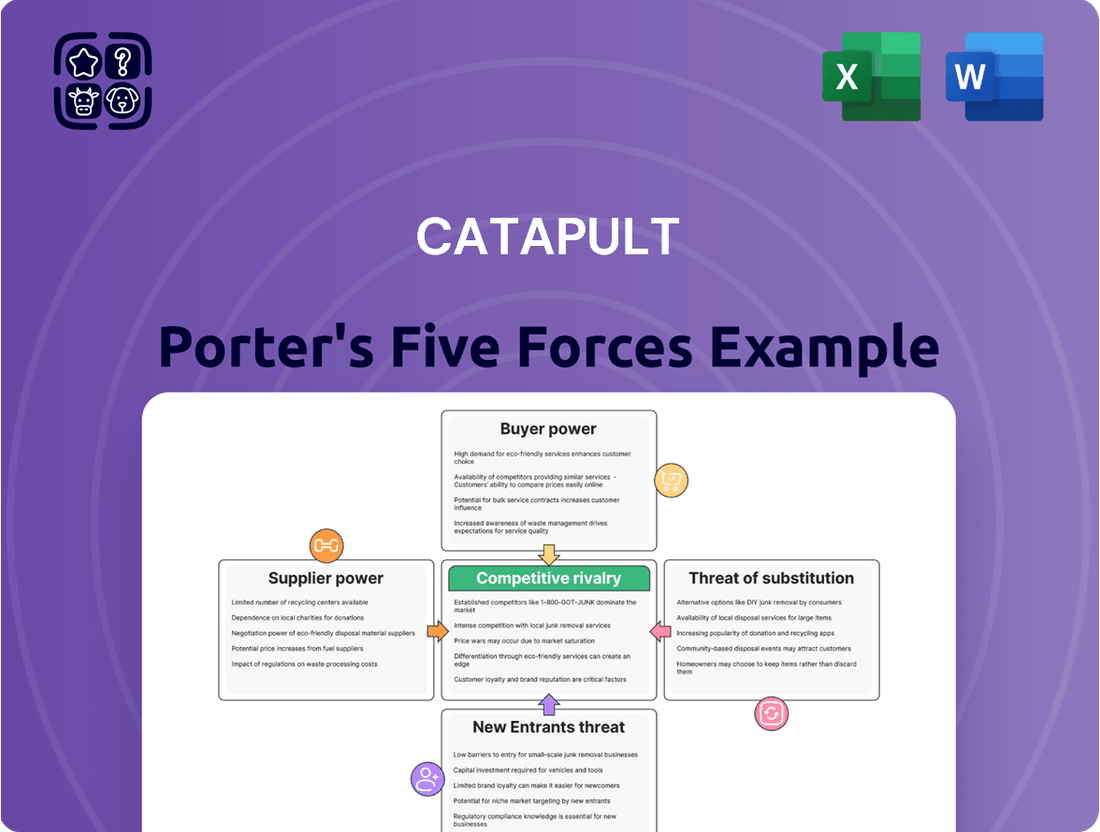

The complete Porter's Five Forces Analysis for Catapult dives deep into each of these forces, offering a data-driven framework to understand its real business risks and market opportunities. Unlock actionable insights to drive smarter decision-making and gain a competitive edge. Get a full strategic breakdown of Catapult’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Specialized Hardware Components

Catapult's reliance on specialized hardware suppliers for its advanced wearable technology, including unique sensors and GPS modules, creates a significant bargaining power dynamic. If these suppliers offer proprietary components that are critical to Catapult's data capture and analysis capabilities, their leverage increases substantially. For instance, a key supplier of a novel biometric sensor, patented and exclusively manufactured, could command higher prices due to limited alternatives.

The potential for this supplier power is amplified if there are only a handful of companies globally capable of producing these highly specialized parts. This scarcity of alternatives directly translates into greater pricing control for the supplier. In 2024, the global market for advanced wearable sensor technology saw significant consolidation, with a few key players emerging as dominant suppliers in niche areas, further concentrating bargaining power.

This dependency poses a risk of increased component costs for Catapult, directly impacting its cost of goods sold and potentially its profit margins. Furthermore, a single critical supplier experiencing production issues or prioritizing other clients could lead to significant supply chain disruptions, affecting Catapult's ability to meet demand for its products.

Advanced Software and Analytics Tools

Suppliers of advanced software and analytics tools, particularly those offering unique algorithms or AI frameworks crucial for video analysis and data processing, wield significant bargaining power over companies like Catapult. This power stems from the specialized nature of their offerings; if Catapult relies on external vendors for these core technologies rather than internal development, the exclusivity and licensing agreements of these tools can directly impact Catapult's operational costs and its ability to differentiate its products in the market.

For instance, a concentrated market of AI and machine learning platform providers can dictate terms, potentially leading to higher licensing fees. In 2024, the global market for AI platforms was estimated to be worth billions, with specialized analytics software commanding premium pricing due to the intricate development and ongoing innovation required. If Catapult's competitive edge relies heavily on a few proprietary software libraries, these suppliers can leverage this dependence to negotiate more favorable terms, thus increasing Catapult's supplier bargaining power.

Manufacturing and Assembly Services

Companies providing manufacturing and assembly services for Catapult's wearable technology hold significant bargaining power. This is particularly true if these suppliers have unique technical capabilities, benefit from substantial economies of scale, or utilize proprietary production methods. These factors can directly influence Catapult's production costs, the quality of its devices, and how quickly it can bring products to market.

The reliance on specialized manufacturers means that disruptions or price increases from these suppliers can directly impact Catapult's operational efficiency and its ability to maintain competitive pricing for its sports performance tracking devices. For instance, a surge in the cost of specialized electronic components sourced by these manufacturers, potentially rising by 5-10% in a given year due to global supply chain pressures, would necessitate a careful review of Catapult's own pricing strategies.

Cloud Infrastructure and Data Storage

The bargaining power of suppliers, particularly for cloud infrastructure and data storage, presents a significant consideration for data-intensive companies like Catapult. The market for these essential services is dominated by a few major players, such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud. This concentration means these providers wield substantial influence over pricing and contract terms.

Catapult's reliance on these providers for scalable infrastructure, data storage, and processing capabilities makes it susceptible to their market power. The ability of these cloud giants to dictate pricing models, service level agreements (SLAs), and even the features available for data security directly impacts Catapult's operational costs and its capacity to deliver reliable services to its own customers. For instance, in 2024, the global cloud computing market was valued at over $600 billion, with the top three providers holding a substantial majority of the market share, underscoring their leverage.

- Dominant Market Players: AWS, Microsoft Azure, and Google Cloud control a significant portion of the cloud infrastructure market, limiting choice for companies like Catapult.

- Pricing Influence: These providers can leverage their market position to influence pricing for essential services, potentially increasing operational expenses for Catapult.

- Contractual Leverage: The terms of service level agreements and data security features offered by major cloud providers can significantly impact Catapult's service delivery and compliance.

- Switching Costs: Migrating large datasets and critical applications between cloud providers can be complex and costly, further strengthening the bargaining power of incumbent suppliers.

Talent Pool for R&D and Specialized Expertise

The availability of highly skilled professionals in fields like engineering, data science, sports science, and product development is absolutely vital for Catapult's ability to innovate and maintain its market position. A limited supply of these specialized individuals can translate into significant bargaining power for the talent themselves, or for the educational bodies and recruitment agencies that source them. This dynamic can directly impact Catapult’s operational costs through increased hiring expenses and potentially slow down the timeline for bringing new products to market.

In 2024, the demand for AI and machine learning specialists, critical for advanced analytics in sports performance, remained exceptionally high. For instance, reports from industry surveys in late 2023 indicated that the average salary for experienced data scientists in technology-focused roles had increased by as much as 15-20% year-over-year, a trend likely continuing into 2024, directly affecting companies like Catapult that rely on such expertise.

- High Demand for Niche Skills: Catapult requires talent with a blend of technical prowess and sports-specific knowledge, a combination that is inherently scarce.

- Talent Acquisition Costs: The competition for these professionals drives up recruitment expenses, impacting the company's R&D budget and overall profitability.

- Impact on Innovation Pipeline: Delays in securing key personnel can hinder the development and launch of next-generation performance tracking and analytics solutions.

- Geographic Talent Concentration: Specialized talent often congregates in specific tech hubs, potentially limiting Catapult's access depending on its operational footprint.

Supplier Power Shapes Wearable Tech Costs and Vulnerabilities

Suppliers of critical, proprietary hardware components, such as specialized sensors and GPS modules, hold significant bargaining power over Catapult. This leverage is amplified when there are few alternative suppliers capable of producing these niche parts, as seen in the consolidated wearable sensor market of 2024. Such dependency can drive up costs and create supply chain vulnerabilities.

| Supplier Type | Key Components/Services | Bargaining Power Factors | 2024 Market Insight |

|---|---|---|---|

| Hardware Components | Proprietary Sensors, GPS Modules | Scarcity of alternatives, proprietary technology | Consolidation in advanced wearable sensor market |

| Software & Analytics | AI Algorithms, Data Processing Frameworks | Exclusivity of offerings, licensing terms | Billions spent on AI platforms, premium pricing for specialized software |

| Manufacturing & Assembly | Device Production, Technical Capabilities | Economies of scale, proprietary methods | Potential 5-10% component cost increase due to supply chain pressures |

| Cloud Infrastructure | Data Storage, Processing, Scalable Services | Market concentration (AWS, Azure, Google), switching costs | Over $600 billion global cloud market, top 3 providers dominate |

| Specialized Talent | Engineers, Data Scientists, Sports Scientists | High demand for niche skills, talent acquisition costs | 15-20% salary increase for experienced data scientists |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Catapult's unique position in the sports technology market.

Effortlessly identify and address competitive threats with pre-built templates that guide you through each of Porter's Five Forces.

Customers Bargaining Power

Elite Professional Sports Teams and Leagues

The bargaining power of customers in the elite professional sports and leagues sector, a key market for Catapult, is considerable. These organizations, including major football leagues and top-tier athletic teams, are sophisticated buyers making substantial investments in performance technology. Their ability to impact Catapult's revenue stems from their concentrated nature and the critical role technology plays in their success. For instance, a single large league or a collection of major teams represents a significant portion of Catapult's clientele, granting them leverage in negotiations.

Customers' power is amplified by the high stakes involved in performance optimization. Elite sports organizations can demand tailored solutions, competitive pricing, and superior service levels, as any perceived deficiency in technology can translate to a direct competitive disadvantage. While Catapult boasts strong customer retention, often exceeding 90% for its core offerings, this loyalty also implies an expectation of continuous innovation and robust support, further empowering these clients to voice their needs and negotiate favorable terms.

High Switching Costs and Data Integration

When sports organizations deeply integrate Catapult's wearable technology and video analysis into their daily operations, from training to historical data tracking, the cost and disruption of switching to a competitor become substantial. This deep integration means Catapult's solutions become a core part of how teams function, making a transition difficult.

The proprietary nature of the data insights Catapult provides, coupled with its embeddedness within a team's established workflows, creates significant switching costs. This 'lock-in' effect effectively reduces the bargaining power of customers over time, as the effort and expense to move elsewhere increase.

This customer lock-in is a key driver for Catapult's recurring revenue model. For instance, in 2023, Catapult reported a strong recurring revenue base, highlighting the stickiness of their solutions. As of early 2024, the company continues to emphasize this recurring revenue stream as a cornerstone of its financial stability.

Value Proposition of Performance Optimization

Customers, particularly elite sports teams and organizations, are intensely focused on optimizing athlete performance and minimizing injury risks. This critical need, which directly influences competitive outcomes and revenue streams, makes them highly receptive to solutions that deliver tangible benefits. Catapult’s value proposition, centered on real-time performance monitoring and detailed post-session analysis, offers actionable insights that are perceived as essential for gaining a competitive edge.

The demonstrable impact of Catapult's technology on athlete development and injury prevention translates into a high perceived value. This perceived value can significantly lessen customer price sensitivity. For example, in 2024, teams investing in advanced performance analytics often report measurable improvements in player availability and on-field performance, justifying the expenditure as a crucial investment rather than a discretionary cost.

Budget Constraints and ROI Expectations

Professional sports organizations, despite recognizing the value of advanced analytics, are not immune to budget constraints. They demand a demonstrable return on investment (ROI) for any technology expenditure. This means Catapult's solutions will be scrutinized for their cost-effectiveness, directly linking their price to tangible performance improvements and reduced injury rates.

This financial discipline empowers customers, giving them significant leverage during negotiations, especially when considering new technology acquisitions or renewing existing contracts. For example, if a team can achieve similar performance metrics through less expensive means or by optimizing existing resources, they are less likely to agree to premium pricing for Catapult's offerings.

- Budgetary Scrutiny: Teams are increasingly focused on justifying every dollar spent, particularly in areas where direct performance impact is hard to quantify immediately.

- ROI Benchmarking: Customers will compare Catapult's cost against the proven benefits of injury reduction (e.g., fewer lost player days) and performance enhancement (e.g., improved win percentages).

- Negotiating Power: The ability of teams to seek alternative solutions or delay adoption due to budget limitations provides a strong bargaining chip.

Customer Concentration and Market Size

While Catapult serves a broad base of thousands of teams, the market for elite sports performance technology remains a specialized segment. This niche nature means that a concentration of revenue from a few key clients, such as major professional leagues or highly visible teams, could grant those customers significant leverage. For instance, if a single league represents over 10% of Catapult's annual recurring revenue, their ability to negotiate favorable terms increases.

However, Catapult's strategic diversification across multiple sports disciplines, including soccer, basketball, and American football, along with its global reach into various regional leagues, actively mitigates this risk. This broad customer base dilutes the impact any single customer or small group of customers can have on pricing and contract conditions. By expanding its market penetration, Catapult reduces its reliance on any one dominant buyer, thereby strengthening its own bargaining position.

In 2023, Catapult reported total revenue of approximately AUD 138 million. While specific customer concentration data is proprietary, the company's stated strategy emphasizes broadening its appeal beyond traditional elite sports to include collegiate and even high-performance youth programs. This ongoing expansion aims to further reduce customer concentration and enhance resilience against potential customer power.

- Niche Market: The elite sports performance technology sector is smaller than mass-market wearables, potentially concentrating buyer power.

- Revenue Concentration Risk: High revenue dependence on a few major leagues or teams could empower those customers.

- Diversification Strategy: Catapult's presence in multiple sports (e.g., soccer, basketball) and regions diffuses customer power.

- 2023 Revenue: Catapult's total revenue of approximately AUD 138 million indicates a substantial but specialized market presence.

Elite Sports Buyers: Powering Performance, Shaping Terms

The bargaining power of customers in the elite sports sector, a key market for Catapult, is significant due to the concentrated nature of these sophisticated buyers. Their ability to impact pricing and terms is substantial, especially given the critical role performance technology plays in their competitive success.

Customers' leverage is amplified by the high stakes of performance optimization and the deep integration of Catapult's solutions into their operational workflows, creating high switching costs. While Catapult has strong customer retention, often exceeding 90% for core offerings, this also means clients expect continuous innovation and robust support, enhancing their negotiating position.

Despite the perceived value and demonstrable impact of Catapult's technology, elite sports organizations remain budget-conscious and demand clear ROI. This necessitates Catapult to prove cost-effectiveness, linking its pricing to tangible benefits like reduced injury rates and improved performance metrics. For instance, in 2024, teams investing in advanced analytics seek measurable improvements, justifying expenditure as a critical investment.

Catapult's strategic diversification across multiple sports and global regions effectively dilutes the power of any single customer. While the elite sports technology sector is niche, this broad market penetration reduces reliance on any one dominant buyer, thereby strengthening Catapult's own negotiating stance. In 2023, Catapult reported total revenue of approximately AUD 138 million, with ongoing expansion into collegiate and youth programs further reducing customer concentration risk.

| Factor | Impact on Customer Bargaining Power | Catapult's Mitigation Strategy |

| Customer Concentration | High (few large leagues/teams) | Diversification across sports and regions |

| Switching Costs | High (deep integration, proprietary data) | Recurring revenue model, embedded workflows |

| Price Sensitivity/Budget | Moderate to High (demand for ROI) | Demonstrate tangible performance improvements and cost savings |

| Information Availability | High (benchmarking competitor offerings) | Continuous innovation, superior analytics |

Full Version Awaits

Catapult Porter's Five Forces Analysis

This preview showcases the complete Catapult Porter's Five Forces Analysis you will receive immediately after purchase. It meticulously details the competitive landscape, examining the threat of new entrants, the bargaining power of buyers, the bargaining power of suppliers, the threat of substitute products or services, and the intensity of rivalry among existing competitors within the industry. This in-depth analysis is professionally formatted and ready for your immediate use, providing actionable insights to inform your strategic decisions without any surprises or placeholders.

Rivalry Among Competitors

Established Competitors with Diverse Offerings

The sports technology landscape is intensely competitive, featuring established rivals such as Hudl Sportscode, Kitman Labs, STATSports, and Kinduct. These companies offer a range of specialized solutions, from video analysis to comprehensive athlete management and performance tracking.

Catapult distinguishes itself within this crowded market by providing an integrated platform that seamlessly combines wearable data with advanced video analysis capabilities. This dual approach allows Catapult to cater to both the performance enhancement and injury prevention needs of athletes, alongside tactical development and coaching strategies.

In 2024, the global sports technology market continued its robust growth, with estimates suggesting it could reach over $40 billion, underscoring the significant investment and competition in areas like athlete performance monitoring and data analytics.

Catapult’s strategy to compete effectively relies on its ability to deliver a unified ecosystem for sports teams, offering a more holistic view of athlete well-being and on-field performance than many specialized competitors.

Rapid Technological Innovation

The sports technology sector is defined by swift technological evolution, with artificial intelligence, machine learning, and sophisticated sensor technology at the forefront. This ceaseless innovation fuels fierce competition as businesses race to deliver the most precise, insightful, and intuitive solutions.

Catapult faces this dynamic environment, necessitating sustained investment in research and development to preserve its market leadership. For instance, the company's commitment to R&D is evident in its development of AI-powered analytics and real-time video analysis capabilities, crucial for staying ahead.

In 2024, the global sports technology market was valued at approximately $20.9 billion, with a projected compound annual growth rate (CAGR) of over 15% through 2030, underscoring the significant impact of rapid innovation on market expansion and competitive pressures.

Market Growth and Attractiveness

The global sports technology market is booming, with projections showing strong future growth. For instance, the market for sports wearables alone was valued at approximately $13.6 billion in 2023 and is expected to climb significantly. This rapid expansion acts as a magnet, drawing in both established companies looking to broaden their reach and fresh startups eager to carve out a niche.

This robust growth fuels intense competitive rivalry. As the market becomes more attractive, existing companies are motivated to innovate and increase their market share, while the prospect of high returns encourages new players to enter, often with disruptive technologies or business models. This dynamic creates a challenging environment where companies must constantly adapt to stay ahead.

The increasing demand for sophisticated performance tracking, athlete monitoring, and fan engagement solutions further intensifies this competition. Companies are investing heavily in research and development to offer cutting-edge products and services, leading to a continuous cycle of innovation and market pressure.

Brand Reputation and Customer Relationships

In the competitive landscape of elite sports technology, a strong brand reputation and deep customer relationships are paramount. Catapult has cultivated this by delivering proven results, evidenced by its extensive global client base of over 4,600 teams. This strong foundation contributes to high Annual Contract Value (ACV) retention rates, a key indicator of client satisfaction and loyalty.

However, the sector is dynamic, with rivals actively seeking to erode Catapult's standing. Competitors are investing in building similar levels of trust and offering attractive alternatives designed to capture market share. For instance, companies like STATSports and Hudl are increasingly investing in R&D and customer success initiatives to challenge established players.

- Catapult serves over 4,600 teams globally.

- High ACV retention rates underscore strong customer relationships.

- Competitors are actively working to build trust and offer alternatives.

- The sector demands continuous innovation to maintain brand loyalty.

Product Differentiation and Ecosystem Integration

Competitive rivalry in the sports technology sector, including for companies like Catapult, heavily relies on product differentiation and the seamless integration of these products into existing team workflows and the broader sports ecosystem. Catapult's strategy of combining advanced hardware, such as wearable devices, with sophisticated software and analytics platforms creates a unified and comprehensive solution for athlete performance monitoring and management.

This integrated approach sets Catapult apart from competitors who might focus on just one aspect, like hardware or software, or offer more fragmented solutions. For instance, while some competitors might offer standalone wearable devices or a separate software analytics platform, Catapult’s strength lies in knitting these elements together to provide a holistic view of athlete data and performance insights.

The competitive landscape features a variety of strategies; some rivals might concentrate on a niche market segment, offering highly specialized hardware or software, while others aim for broader athlete management systems that encompass more than just performance analytics. This diversity in competitive approaches means rivalry is not just about features but also about how well a solution fits into the complex operational needs of sports organizations.

In 2024, the emphasis on data-driven decision-making in sports continues to intensify, pushing companies to innovate in both hardware accuracy and software usability. Companies are investing heavily in AI and machine learning to extract deeper insights from athlete data, further fueling the differentiation race. For example, advancements in sensor technology and the development of predictive analytics for injury prevention are key battlegrounds.

- Product Integration: Catapult's advantage stems from its ability to link wearable data with video analysis and tactical software, offering a more complete picture than single-function competitors.

- Ecosystem Play: Successful players are those who can integrate their solutions with existing club infrastructure, such as electronic medical records or team communication platforms.

- Data Analytics Sophistication: The depth and actionability of insights derived from data are critical differentiators, with AI-powered analytics becoming increasingly important.

- Specialization vs. Breadth: Rivals differentiate by either offering best-in-class niche products or comprehensive, all-encompassing athlete management platforms.

Sports Tech's $20.9 billion Battle: Innovation and AI Drive Growth

The competitive rivalry within sports technology is fierce, driven by rapid innovation and a growing market. Companies like Hudl, Kitman Labs, and STATSports are major players, offering specialized solutions that range from video analysis to athlete management. Catapult differentiates itself by providing an integrated platform that combines wearable data with advanced video analysis, creating a comprehensive solution for performance and injury prevention.

In 2024, the global sports technology market was estimated to be around $20.9 billion, with projections indicating a compound annual growth rate exceeding 15% through 2030. This substantial growth attracts both established companies and new entrants, intensifying competition as businesses vie for market share through technological advancements and superior product offerings.

Catapult's strategy to maintain its competitive edge involves continuous investment in research and development, focusing on areas like AI-powered analytics and real-time video analysis. This commitment is crucial for staying ahead in a sector where swift technological evolution is the norm, and companies must constantly innovate to meet the increasing demand for sophisticated performance tracking and data insights.

The emphasis on data-driven decision-making in sports in 2024 has intensified the need for accurate hardware and user-friendly software. Companies are heavily investing in AI and machine learning to extract deeper athlete data insights, with advancements in sensor technology and predictive analytics for injury prevention being key areas of competition.

| Key Competitors | Primary Offerings | Catapult's Differentiator | Market Context (2024) |

|---|---|---|---|

| Hudl | Video analysis, performance management | Integrated hardware and software platform | Global sports technology market valued at approx. $20.9 billion |

| Kitman Labs | Athlete management systems, injury prevention | Holistic view of athlete data | Projected CAGR of over 15% through 2030 |

| STATSports | Wearable tracking devices, data analytics | Seamless combination of wearable and video data | High demand for AI/ML in sports analytics |

SSubstitutes Threaten

Traditional Coaching Methods and Manual Data Collection

Traditional coaching methods, relying on observation and manual data gathering, still serve as a substitute. This approach, while less advanced, can be attractive for teams with tighter budgets or those hesitant to invest in new technology.

These traditional methods bypass the upfront costs and learning curves associated with sophisticated sports technology. For instance, a smaller amateur league might opt for manual player assessments rather than investing in wearable sensors, saving thousands in initial outlay.

However, the efficacy of these substitutes is limited when compared to modern solutions. They often lack the granular detail and objective analysis that data-driven platforms offer, hindering the ability to fine-tune athlete performance at an elite level.

While 2024 saw continued growth in sports analytics adoption, a significant portion of the amateur and semi-professional market still utilizes these lower-tech alternatives, demonstrating their persistence as a viable, albeit less powerful, substitute.

Generic Consumer Wearables and Fitness Trackers

The threat of substitutes for Catapult's advanced athlete monitoring solutions comes primarily from generic consumer wearables and fitness trackers. These devices, readily available at lower price points, offer basic health and activity metrics like step counts and heart rate. For instance, popular consumer smartwatches from brands like Apple and Samsung, which saw significant sales growth in 2024, provide some of these functions.

While these consumer-grade devices can serve as a partial substitute for teams or athletes with very tight budgets, their capabilities are fundamentally limited. They typically lack the specialized sensors, data granularity, and sophisticated analytics that Catapult provides. This means they cannot offer the same level of performance insights, injury prevention data, or tactical analysis crucial for elite sports performance.

Basic Video Analysis Software and Free Tools

Simpler video analysis software and free tools present a threat by offering basic functionality for reviewing game footage. While these options can provide some visual feedback, they often lack the sophisticated capabilities found in platforms like Catapult. For instance, many free tools do not offer AI-powered insights or the ability to integrate data from wearable devices, which are crucial for elite performance optimization.

These less advanced alternatives can fulfill some of the needs of lower-tier teams or individual athletes who may not have the budget for premium solutions. However, their limitations become apparent when high-level tactical analysis and detailed performance metrics are required. The gap in data-driven insights means these substitutes fall short in providing the comprehensive understanding necessary for professional sports organizations aiming to gain a competitive edge.

Internal Data Analytics Departments of Sports Organizations

The threat of substitutes for Catapult's services comes from the potential for large, well-funded sports organizations to build their own internal data analytics departments. This could reduce their need for external vendors. For instance, the NFL's investment in player tracking data and analytics infrastructure demonstrates this trend.

However, establishing and maintaining these advanced internal systems is a substantial undertaking. It demands significant capital expenditure, access to specialized data scientists and engineers, and continuous investment in research and development. These barriers mean that only a select few organizations can realistically implement such a substitute.

The ongoing costs associated with internal solutions, including software development, hardware upgrades, and personnel, can be considerable. In 2024, the average salary for a sports data scientist ranged from $90,000 to $150,000 annually, highlighting the talent acquisition costs.

- High upfront investment: Building proprietary analytics platforms requires substantial capital.

- Specialized talent needs: Expertise in data science, software engineering, and sports performance is crucial.

- Ongoing R&D: Continuous innovation is necessary to stay competitive, adding to operational costs.

- Limited feasibility: Only the largest and most financially robust organizations can realistically pursue this path.

Alternative Performance Enhancement Methodologies

Beyond direct technological substitutes, alternative methodologies like advanced sports psychology, nutrition science, or highly specialized physical therapy represent indirect threats. These focus on different aspects of performance enhancement, offering different pathways for athletes and teams to improve. For instance, a team heavily investing in advanced biomechanics tracking might allocate less budget to a cutting-edge sports psychology program, creating a trade-off.

While Catapult's solutions often integrate with these other disciplines, the existence of strong alternatives means that investment in one area can sometimes divert resources from another. This is particularly relevant as the sports science landscape broadens. In 2024, the global sports nutrition market alone was valued at over $50 billion, demonstrating a significant investment in non-technological performance aids.

- Sports Psychology: Focuses on mental skills, performance under pressure, and team cohesion.

- Nutrition Science: Optimizes athlete fueling, recovery, and overall health through diet.

- Physical Therapy & Rehabilitation: Specializes in injury prevention, recovery, and restoring optimal physical function.

- Advanced Training Methodologies: Includes novel strength and conditioning techniques or skill-specific drills.

Athlete Performance: Diverse Substitutes Challenge Advanced Systems

The threat of substitutes for Catapult's advanced athlete monitoring systems is multifaceted, encompassing lower-tech alternatives and broader performance enhancement strategies. Generic consumer wearables, while offering basic metrics, lack the specialized data crucial for elite performance. Similarly, simpler video analysis tools provide limited insights compared to integrated platforms.

While 2024 saw continued adoption of advanced analytics, a substantial amateur market still relies on traditional observation and manual data gathering, presenting a cost-effective substitute. These methods bypass the investment and learning curves of sophisticated technology, making them accessible for smaller organizations.

The emergence of robust in-house analytics departments within large sports organizations also poses a threat, though the high costs and specialized talent required limit this substitute's feasibility to only the most financially sound entities. In 2024, the average sports data scientist salary underscored these personnel costs.

Furthermore, indirect substitutes like sports psychology, advanced nutrition science, and specialized physical therapy compete for investment. The global sports nutrition market, exceeding $50 billion in 2024, exemplifies the significant resources allocated to these non-technological performance aids, highlighting a potential trade-off in budget allocation.

Entrants Threaten

High Capital Investment for Hardware and R&D

The threat of new entrants in the elite sports wearable technology market, particularly for companies like Catapult, is significantly mitigated by the immense capital required for research and development. Developing cutting-edge, reliable wearable devices for professional athletes demands massive investment in R&D, intricate prototyping, and establishing sophisticated manufacturing facilities. For instance, companies in this space often spend millions annually on sensor advancements and data analytics capabilities to stay competitive.

New players must be prepared to absorb these substantial upfront expenditures to even begin challenging established firms. This barrier extends to the continuous need for innovation in sensor technology and the expertise in data science, areas where incumbents like Catapult have already built significant advantages and intellectual property. The sheer scale of investment needed to match existing technological sophistication and market presence acts as a powerful deterrent to potential new entrants.

Intellectual Property and Patents

Established companies like Catapult hold a substantial portfolio of patents and proprietary algorithms. These innovations cover critical areas such as athlete tracking, biomechanics, and advanced video analysis, creating a strong technological moat.

New entrants would struggle to replicate this technological depth without infringing on existing intellectual property. Developing genuinely unique technologies requires significant R&D investment, presenting a formidable hurdle.

Alternatively, licensing Catapult's patented technology would necessitate substantial financial outlay. In 2024, licensing fees for advanced sports analytics technology can range from tens of thousands to millions of dollars annually, depending on the scope and exclusivity.

This financial burden and the legal risk associated with IP infringement act as significant deterrents, effectively raising the barrier to entry for potential competitors in the sports performance analytics market.

Difficulty in Building Trust and Relationships with Elite Sports Organizations

Professional sports organizations are inherently cautious about integrating novel technologies that directly influence athlete performance and well-being. This risk aversion translates into a significant hurdle for new entrants seeking to establish a foothold in this specialized market.

Cultivating the essential trust, proving consistent reliability, and forging enduring partnerships with these elite entities is a protracted and demanding endeavor. For instance, Catapult, a leader in this space, has spent over a decade nurturing these crucial relationships, highlighting the substantial time investment required.

New companies face the daunting task of not only developing superior technology but also overcoming the established trust and proven track record that incumbents like Catapult have meticulously built over many years. This deeply entrenched loyalty and confidence among top-tier sports organizations acts as a powerful deterrent to new market participants.

Scalability Challenges for Data Processing and Analytics

The threat of new entrants in the sports analytics sector, particularly concerning scalability challenges for data processing, is substantial. New players must contend with the immense task of handling, processing, and analyzing real-time performance data from vast numbers of athletes and video feeds. This necessitates significant investment in robust, scalable cloud infrastructure and advanced analytics capabilities.

Building or acquiring this complex infrastructure, coupled with the requisite expertise in managing big data, presents a formidable operational and technical barrier. For instance, a company aiming to compete with established leaders in athlete performance tracking would need to invest in petabyte-scale data storage and distributed computing frameworks, a cost that can easily run into tens of millions of dollars upfront. The ongoing costs for cloud services and specialized talent further amplify this challenge.

- Infrastructure Investment: New entrants require substantial capital for scalable cloud computing (e.g., AWS, Azure, GCP) capable of handling terabytes of daily data.

- Data Processing Expertise: Acquiring or developing skilled data scientists and engineers proficient in big data technologies like Spark and Hadoop is critical.

- Real-time Analytics: The ability to process and deliver insights from live data streams, a core requirement in sports, demands sophisticated low-latency architectures.

- Cost of Development: The initial outlay for building such a comprehensive data processing and analytics platform can exceed $20 million, deterring many potential new entrants.

Regulatory Hurdles and Data Privacy Concerns

The threat of new entrants in the sports technology sector, particularly those dealing with athlete data, is significantly shaped by evolving regulatory landscapes. For example, the General Data Protection Regulation (GDPR) in Europe, which came into full effect in 2018, imposes strict rules on how personal data, including sensitive health and performance metrics, can be collected, processed, and stored. New companies must invest heavily in robust compliance infrastructure and secure data management systems to avoid substantial penalties, which can reach up to 4% of global annual revenue or €20 million, whichever is higher. Similarly, regions are implementing or strengthening HIPAA-like regulations to protect health information, adding further layers of complexity and cost for any aspiring market participant.

These compliance requirements create a substantial barrier to entry. Newcomers must not only develop innovative technology but also demonstrate a deep understanding and adherence to a patchwork of international and national data protection laws. This necessitates significant upfront investment in legal counsel, compliance officers, and secure IT architecture. Established companies, having already invested in and refined their compliance frameworks, possess a distinct advantage, making it harder for new players to compete on a level playing field from the outset.

Consider the increasing focus on data privacy in 2024 and beyond. Reports indicate a growing consumer demand for data control, pushing regulators to enact even more stringent measures. For instance, several US states have introduced or passed comprehensive data privacy laws, mirroring some aspects of GDPR, which could impact sports tech companies operating within those states. This trend suggests that navigating the regulatory environment will only become more challenging and costly for new entrants.

- Increased Compliance Costs: New entrants face significant expenses in legal, technical, and operational aspects to meet data protection standards like GDPR and HIPAA.

- Data Security Investment: Building and maintaining secure systems to protect sensitive athlete performance and health data is a prerequisite, demanding substantial capital.

- Regulatory Complexity: Navigating a complex and evolving web of global and regional data privacy laws presents a considerable challenge for startups.

- Advantage for Incumbents: Established players benefit from pre-existing compliance frameworks, reducing their relative risk and cost of entry compared to new firms.

High Barriers Block New Entrants in Elite Sports Tech

The threat of new entrants into the elite sports wearable technology market, where Catapult operates, is significantly lowered by high capital requirements for research and development. Developing advanced, reliable devices for professional athletes demands substantial investment in R&D, complex prototyping, and sophisticated manufacturing. For example, companies in this sector often allocate millions annually to sensor advancements and data analytics to maintain a competitive edge.

New competitors must be ready to absorb these considerable upfront costs. This barrier also includes the perpetual need for innovation in sensor technology and data science expertise, areas where incumbents like Catapult have already established strong advantages and intellectual property. The sheer scale of investment needed to match existing technological sophistication and market presence serves as a powerful deterrent.

Established players like Catapult possess extensive patent portfolios and proprietary algorithms covering critical areas such as athlete tracking and biomechanics, creating a robust technological moat. New entrants would find it challenging to replicate this depth without infringing on existing intellectual property, and developing genuinely unique technologies requires significant R&D investment, posing a formidable hurdle.

The sports analytics sector faces substantial barriers for new entrants, particularly concerning data processing scalability. New players must manage the immense task of processing real-time performance data from numerous athletes and video feeds, necessitating significant investment in scalable cloud infrastructure and advanced analytics. Building this complex infrastructure, alongside the required big data expertise, presents a formidable operational and technical challenge.

The regulatory landscape also poses a significant threat to new entrants in sports technology, especially concerning athlete data. Regulations like GDPR impose strict rules on data collection and processing, requiring substantial investment in compliance infrastructure and secure data management systems to avoid hefty penalties. Navigating this complex web of global and regional data protection laws is a considerable challenge for startups.

Porter's Five Forces Analysis Data Sources

Our Catapult Porter's Five Forces analysis leverages a robust blend of primary and secondary data, including proprietary market research, company filings, and industry expert interviews, to provide a comprehensive view of competitive dynamics.