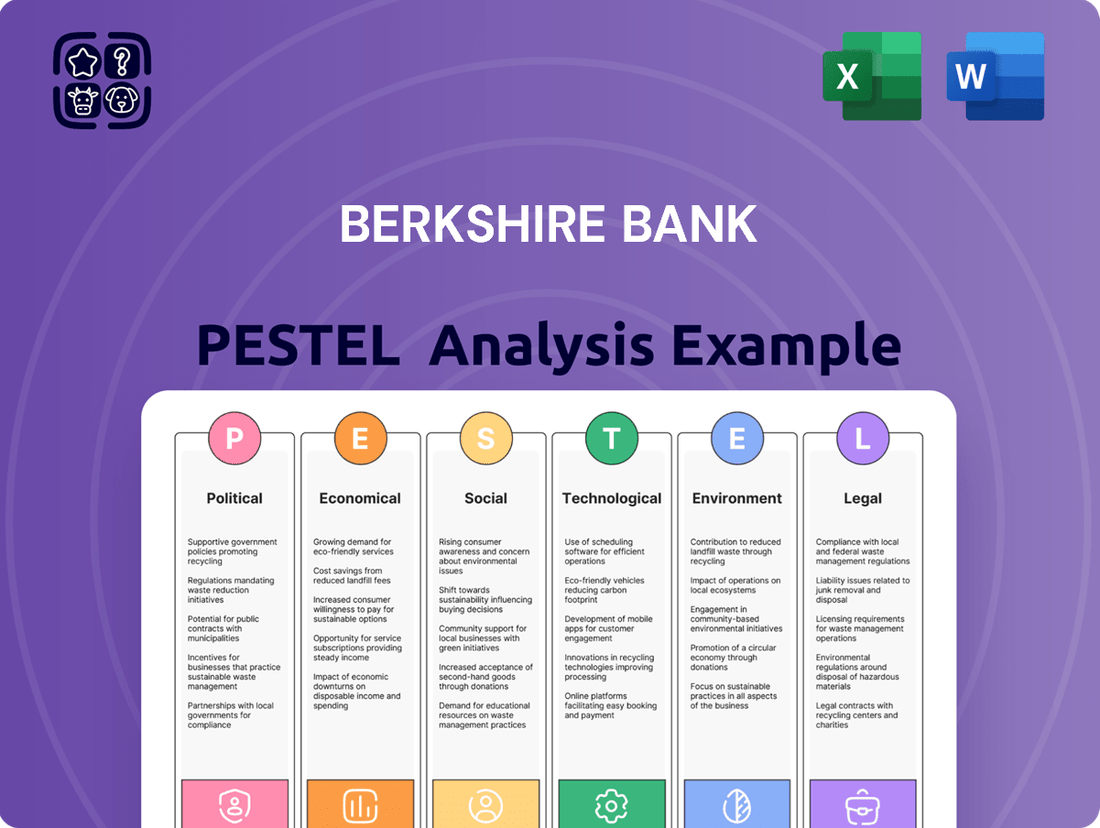

Berkshire Bank PESTLE Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Berkshire Bank

Plan Smarter. Present Sharper. Compete Stronger.

Unlock the critical external factors influencing Berkshire Bank's trajectory with our comprehensive PESTLE analysis. Understand how political shifts, economic volatility, and technological advancements are reshaping the financial landscape. Gain a strategic advantage by leveraging these expert insights to inform your decisions. Download the full PESTLE analysis now for actionable intelligence.

Political factors

Government Policy and Regulation

Berkshire Bank operates within a heavily regulated financial services sector, governed by federal and state banking laws. For instance, the Dodd-Frank Wall Street Reform and Consumer Protection Act, enacted in 2010, continues to shape compliance requirements, impacting capital adequacy and risk management.

Monetary policy shifts by the Federal Reserve, such as interest rate adjustments, directly influence Berkshire Bank's core lending and deposit activities. In 2024, the Federal Reserve maintained its target range for the federal funds rate, impacting borrowing costs and net interest margins for banks nationwide.

New regulatory measures, focused on enhancing financial stability or consumer protection, can impose significant compliance costs and operational adjustments. For example, evolving cybersecurity regulations require continuous investment in technology and protocols to safeguard customer data and maintain operational integrity.

Financial Regulatory Environment

The U.S. banking sector operates under a shifting regulatory framework, reflecting new administrations and evolving oversight priorities. Despite potential moves toward deregulation, a strong emphasis on robust governance, risk management, and compliance remains paramount for institutions like Berkshire Bank.

Anticipated changes to capital and liquidity requirements, alongside a heightened focus on non-financial risks such as cybersecurity and vendor management, will directly influence Berkshire Bank's operational strategies and compliance burdens. For instance, the Federal Reserve's stress tests, which inform capital requirements, are continuously updated, with the 2024 test results indicating varying capital adequacy ratios across the industry.

Political Stability and Trade Relations

While Berkshire Bank's core operations are in the Northeastern U.S., broader political stability and global trade dynamics still matter. For instance, the U.S. experienced a period of heightened geopolitical tensions in late 2023 and early 2024, contributing to market fluctuations that impacted investment portfolios managed by the bank.

Changes in international trade agreements, such as potential renegotiations of existing pacts, could indirectly affect the economic outlook for businesses in the bank's service regions. This, in turn, might influence demand for commercial loans and affect the overall health of the regional economy, a key factor for Berkshire Bank's lending and deposit growth.

Government Spending and Fiscal Policy

Government spending and fiscal policy significantly shape the economic landscape, directly impacting Berkshire Bank's operational environment. For instance, the U.S. federal budget for fiscal year 2024 proposed substantial outlays, with a focus on areas like defense and social programs, which can indirectly boost economic activity and, by extension, demand for banking services. State-level fiscal decisions also play a critical role; a state prioritizing infrastructure development, for example, could see increased business investment and a corresponding rise in commercial lending needs.

Berkshire Bank's performance is closely tied to the government's fiscal stance. A proactive fiscal policy, such as tax cuts or increased transfer payments, can stimulate consumer spending, leading to greater deposit growth and loan demand. Conversely, fiscal tightening, like reduced government spending or tax hikes, could temper economic expansion, potentially slowing loan origination and increasing credit risk. The U.S. national debt, which stood at over $34 trillion as of early 2024, also influences interest rate environments and investor confidence, indirectly affecting the banking sector's profitability and lending capacity.

- Federal Spending Impact: U.S. federal government spending for FY2024 was projected to be in the trillions, influencing overall economic momentum and consumer confidence.

- State Fiscal Strategies: State budgets, such as California's multi-billion dollar budget for FY2024-25, dictate local investment priorities and economic development, affecting regional banking demand.

- Fiscal Policy Tools: Government decisions on taxation and spending directly influence disposable income and business investment, key drivers for loan demand and deposit growth in the banking sector.

- Debt Levels: The substantial U.S. national debt can influence interest rate policies and economic stability, creating both opportunities and risks for banks like Berkshire Bank.

Community Reinvestment Act (CRA) Enforcement

The Community Reinvestment Act (CRA) mandates that banks serve the credit needs of their entire communities, including low- and moderate-income areas. Berkshire Bank, with its community-centric approach, must adhere to these rules, which are adjusted annually based on asset size. For instance, as of early 2024, the CRA asset thresholds were updated, impacting reporting requirements for institutions like Berkshire.

Berkshire Bank's active participation in community development, demonstrated through initiatives such as the 'BEST Community Comeback' program, directly supports CRA goals. These efforts not only fulfill regulatory obligations but also enhance the bank's reputation and foster goodwill within the communities it serves.

The bank's commitment to reinvestment is crucial for maintaining a positive regulatory standing and can influence its ability to obtain approvals for future expansion or mergers. Failing to meet CRA expectations can lead to scrutiny and potential penalties, underscoring the importance of consistent community engagement.

Fiscal Policy Shapes Banking's Economic Landscape

Government fiscal policies, including spending and taxation, directly shape the economic environment Berkshire Bank operates within. For instance, the U.S. federal budget for FY2024, with its significant outlays, influences overall economic activity and demand for banking services. State-level fiscal decisions also play a crucial role, with infrastructure spending potentially boosting regional economic growth and commercial lending needs.

What is included in the product

This PESTLE analysis offers a comprehensive examination of the external macro-environmental factors influencing Berkshire Bank, detailing impacts across Political, Economic, Social, Technological, Environmental, and Legal dimensions.

It provides actionable insights and forward-looking perspectives, enabling strategic decision-making for navigating the evolving landscape.

A concise PESTLE analysis for Berkshire Bank provides a clear roadmap to navigate external challenges, offering stakeholders a readily digestible overview for strategic decision-making.

Economic factors

Interest Rate Environment

The interest rate environment is a critical factor for Berkshire Bank. While the Federal Reserve is anticipated to implement several rate cuts throughout 2025, potentially lowering rates multiple times, the cost of deposits might not decline as quickly. This could lead to continued pressure on Berkshire Bank's net interest margin.

However, a downward trend in interest rates could be a positive catalyst for loan demand, particularly in the mortgage sector. Furthermore, declining rates generally improve the valuation multiples for regional banks like Berkshire Bank.

Economic Growth and Consumer Spending

U.S. GDP growth is anticipated to slow down in 2025, influenced by a moderation in consumer spending and a decline in business investment. This economic deceleration could directly affect Berkshire Bank's loan demand, potentially reducing growth opportunities in both consumer and commercial lending portfolios.

The current high levels of consumer debt present a significant risk. As economic conditions tighten, there's an increased likelihood of consumers struggling to meet their debt obligations, which could translate into higher credit delinquencies and negatively impact the quality of Berkshire Bank's loan assets.

Inflationary Pressures

While headline inflation has cooled significantly from its 2022 peaks, with the Consumer Price Index (CPI) showing a 3.3% year-over-year increase as of May 2024, the residual effects continue to shape the economic landscape. These lingering pressures can still elevate Berkshire Bank's operating expenses, from technology investments to employee compensation, and notably impact consumer disposable income, potentially slowing loan demand.

The Federal Reserve's monetary policy remains a key consideration, with ongoing discussions about potential interest rate adjustments. Should inflation prove more stubborn than anticipated, the Fed might maintain higher rates for longer, which would positively influence Berkshire Bank's net interest margin on its loan portfolio. Conversely, a swift pivot to rate cuts could compress these margins, necessitating a review of lending strategies.

Effectively navigating these cost dynamics while preserving competitive service pricing is paramount for Berkshire Bank's profitability. For instance, the bank must balance the need to attract and retain talent amidst rising wage expectations with the imperative to offer attractive deposit rates and loan terms to customers, a delicate act in the current economic climate.

Wealth Management Market Trends

The wealth management sector is robust, driven by an expanding pool of high-net-worth individuals and a growing appetite for alternative investments. This upward trajectory is further fueled by an increasing number of individual investors entering the market.

Berkshire Bank, with its wealth management offerings, is well-positioned to capitalize on these dynamics. Key to success will be tailoring services to meet the evolving needs of a diverse client base, including adapting to changing demographic profiles.

- Global wealth is projected to reach $500 trillion by 2025, according to industry reports, creating a larger client base for wealth managers.

- Demand for alternative investments, such as private equity and hedge funds, is surging, with allocations expected to rise significantly in 2024-2025.

- The number of retail investors has seen a notable increase, particularly in the wake of recent market volatility, presenting opportunities for scalable wealth management solutions.

- Investment banking and wealth management revenues are anticipated to be strong performers for financial institutions in the coming year, contingent on stable market conditions.

Mergers and Acquisitions Activity

The U.S. banking sector continues to experience significant consolidation, with projections indicating an acceleration of mergers and acquisitions (M&A) in 2025. This trend is driven by the pursuit of greater scale, efficiency, and competitive advantage in an evolving financial landscape.

Berkshire Bank is actively participating in this consolidation, with its pending merger with Brookline Bancorp, Inc. This strategic move is designed to bolster Berkshire Bank's market position, achieve economies of scale, and ultimately enhance its profitability. Such combinations are pivotal in reshaping the competitive dynamics within the regional banking sector.

The ongoing M&A activity presents a dual nature of opportunities and challenges for regional banks:

- Opportunities: Increased market share, expanded product offerings, and improved operational efficiencies through synergy realization.

- Challenges: Integration complexities, potential regulatory hurdles, and the need to manage cultural differences between merging entities.

- Market Impact: Aggregated data from industry reports suggest that the average deal size for U.S. bank mergers in 2024 reached approximately $1.5 billion, indicating substantial strategic investments being made.

- Strategic Rationale: Banks are increasingly motivated by the need to invest in technology and digital transformation, which is often more feasible with a larger capital base acquired through M&A.

Bank's 2025 Economic Outlook: Navigating Risks, Seizing Opportunities

Economic factors present a mixed outlook for Berkshire Bank. While anticipated interest rate cuts in 2025 could boost loan demand, particularly mortgages, they may also pressure net interest margins if deposit costs remain sticky. Slower U.S. GDP growth in 2025, stemming from moderating consumer spending and business investment, is likely to temper loan growth opportunities.

Persistent high consumer debt levels pose a credit risk, potentially leading to increased delinquencies if economic conditions worsen. Although inflation has eased, its residual effects could still elevate operating expenses and reduce consumer disposable income, further impacting loan demand.

The wealth management sector is a bright spot, with global wealth projected to reach $500 trillion by 2025, driven by high-net-worth individuals and a surge in alternative investments. Berkshire Bank's wealth management division is positioned to benefit from this expansion and the increasing number of retail investors.

The banking sector's consolidation trend, with M&A accelerating in 2025, offers Berkshire Bank strategic opportunities, like its pending merger with Brookline Bancorp, to gain scale and efficiency. However, integration challenges and regulatory considerations are key hurdles to manage.

| Economic Factor | 2024 Projection/Data | 2025 Projection | Impact on Berkshire Bank |

|---|---|---|---|

| Interest Rates | Fed holding steady, potential cuts later in year | Multiple Fed rate cuts anticipated | Potential margin compression, but increased loan demand |

| GDP Growth (U.S.) | Moderate growth | Slowing growth | Reduced loan demand, particularly in commercial lending |

| Inflation (CPI) | 3.3% YoY (May 2024) | Expected to moderate further | Lingering impact on operating costs and consumer spending |

| Consumer Debt | High levels | Continued concern | Increased credit risk and potential delinquencies |

| Wealth Management Growth | Robust | Projected to reach $500 trillion globally by 2025 | Significant opportunity for wealth division |

Preview the Actual Deliverable

Berkshire Bank PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Berkshire Bank PESTLE Analysis provides a comprehensive overview of the Political, Economic, Social, Technological, Legal, and Environmental factors impacting the company.

The content and structure shown in the preview is the same document you’ll download after payment. It delves into key insights and strategic considerations for Berkshire Bank, offering valuable market intelligence.

What you’re previewing here is the actual file—fully formatted and professionally structured. This detailed PESTLE analysis is designed to equip you with the knowledge needed to understand Berkshire Bank's operating landscape.

Sociological factors

Demographic Shifts and Customer Behavior

Demographic shifts significantly impact banking needs. As the U.S. population ages, there's a growing demand for retirement planning and wealth management services. Conversely, younger generations, like Gen Z, prioritize digital banking solutions and mobile-first experiences. For example, a 2024 report indicated that over 70% of Gen Z prefer using mobile apps for banking transactions.

Berkshire Bank must tailor its services to these evolving preferences. This means investing in user-friendly digital platforms and offering personalized financial advice accessible through various channels. Catering to the digital expectations of younger customers, who often seek instant access to their financial information and quick transaction capabilities, is crucial for future growth and customer retention.

Financial Literacy and Inclusion

Berkshire Bank's commitment to financial literacy and inclusion is a significant sociological driver. By investing in community programs, the bank aims to uplift economic well-being, fostering a more stable customer base. For instance, their 'BEST Community Comeback' initiative, launched in 2023, has already provided financial education to over 5,000 individuals across its service areas, directly impacting social mobility.

Changing Work Patterns and Remote Work

The enduring trend of remote and hybrid work arrangements significantly reshapes demand for commercial real estate, potentially affecting Berkshire Bank's lending portfolios tied to office spaces. As of early 2024, reports indicate a sustained preference for flexible work, with many companies maintaining hybrid models, leading to questions about the long-term viability of traditional office occupancy rates.

Berkshire Bank's extensive physical branch network faces strategic challenges due to this shift. Customer preferences are increasingly leaning towards digital banking solutions, a trend amplified by remote work. For instance, a 2024 survey by the American Bankers Association found that over 70% of consumers now utilize mobile banking for most transactions, suggesting a reduced reliance on physical branches.

This evolving customer behavior necessitates a re-evaluation of Berkshire Bank's branch footprint and a greater investment in digital infrastructure. Adapting to these changing work patterns also impacts the bank's internal operations, influencing employee engagement strategies and the need for digital tools that support a dispersed workforce.

Community Engagement and Corporate Responsibility

Berkshire Bank demonstrates a strong commitment to its communities through its foundation, which channels investments into local nonprofits and development projects. For instance, in 2023, Berkshire Bank's foundation contributed $2.5 million to various community initiatives, reflecting a tangible dedication to social well-being.

This active engagement, bolstered by employee volunteer programs that logged over 15,000 hours in 2023, significantly enhances Berkshire Bank's social license to operate. Such initiatives are crucial for fostering positive stakeholder relationships and building trust, which are vital for a bank's reputation and enduring success.

- Community Investment: Berkshire Bank's foundation allocated $2.5 million in 2023 to support local nonprofits and community development.

- Employee Volunteerism: Bank employees contributed over 15,000 volunteer hours in 2023, strengthening community ties.

- Social License: Active corporate responsibility efforts bolster the bank's public image and its permission to operate within communities.

- Stakeholder Relations: These initiatives are key to building and maintaining positive relationships with customers, employees, and the broader public.

Consumer Trust and Confidence

Maintaining consumer trust and confidence is absolutely critical for Berkshire Bank, especially in the current financial climate. Recent reports indicate that consumer confidence in the banking sector can fluctuate significantly; for instance, the American Consumer Confidence Index saw a dip in early 2024 before showing signs of recovery, highlighting the sensitivity of public perception to economic events and institutional actions.

Factors like data breaches, which unfortunately remain a concern across the financial industry, or instances of perceived lack of transparency can quickly erode the trust Berkshire Bank has worked hard to build. A 2024 survey by a leading financial research firm found that over 60% of consumers consider data security a top priority when choosing a bank, and a significant portion would switch providers after a single data breach incident.

Berkshire Bank's commitment to responsible banking, ethical practices, and prioritizing customer satisfaction is therefore not just good business, but a strategic imperative. This focus is vital for retaining its existing client base and attracting new customers in a highly competitive market. For example, banks that consistently score high on customer service and transparency metrics, like Berkshire Bank aims to, often see lower customer attrition rates, typically in the single digits annually, compared to industry averages that can reach double digits.

- Data Security Concerns: Over 60% of consumers prioritize data security when selecting a bank (2024 survey data).

- Impact of Breaches: A significant percentage of customers would switch banks following a data breach.

- Trust as a Differentiator: Banks with strong transparency and ethical practices experience lower customer attrition.

- Consumer Confidence Trends: Public trust in financial institutions can be volatile, influenced by economic conditions and institutional behavior.

Demographics & Trust: The New Banking Imperative

Sociological factors significantly shape banking preferences and trust. Demographic shifts, like the aging population and the rise of digital natives, necessitate tailored services, with younger generations prioritizing mobile-first experiences, as evidenced by over 70% of Gen Z preferring app-based banking in 2024.

Berkshire Bank's community engagement, including a $2.5 million foundation investment in 2023 and over 15,000 employee volunteer hours, builds social license and strengthens stakeholder relations.

Consumer trust is paramount, with 2024 data showing over 60% of consumers prioritizing data security, making ethical practices and transparency crucial for customer retention and acquisition.

Technological factors

Digital Transformation and Online Banking

Berkshire Bank must navigate the accelerating digital transformation in banking, with a growing customer preference for mobile and online services. This shift necessitates ongoing investment to maintain and enhance its digital platforms, ensuring a seamless customer experience.

The expansion of Berkshire Bank's digital presence, while beneficial for customer engagement, also heightens its exposure to cyber threats. In 2024, the financial services sector experienced a significant rise in sophisticated cyberattacks, underscoring the critical need for robust cybersecurity measures.

A proactive and comprehensive cybersecurity strategy is paramount for Berkshire Bank's digital operations. This includes investing in advanced threat detection, data encryption, and employee training to safeguard customer information and maintain trust in an increasingly digital financial landscape.

Cybersecurity Threats and Data Protection

Financial institutions like Berkshire Bank are increasingly vulnerable to advanced cyber threats, including ransomware and AI-powered phishing attacks. The global cost of cybercrime is projected to reach $10.5 trillion annually by 2025, highlighting the immense financial risk. Banks must continually invest in robust security measures, such as advanced encryption and multi-factor authentication, to safeguard sensitive customer data and maintain operational integrity.

Adoption of AI and Automation

Berkshire Bank's technological landscape is heavily influenced by the accelerating adoption of AI and automation. These technologies are revolutionizing core banking functions, from bolstering threat detection and response mechanisms to streamlining client servicing and proactively anticipating wealth management needs.

For instance, AI's capacity to analyze vast datasets is crucial for identifying and mitigating sophisticated cyber threats. However, this same power is being leveraged by malicious actors. Reports from 2024 indicate a significant rise in AI-powered phishing and malware attacks, underscoring the dual-edged nature of this technology.

To counter this, Berkshire Bank must strategically deploy AI to fortify its digital defenses. Simultaneously, substantial investment in employee training is paramount. By equipping staff with the skills to recognize and respond to AI-driven threats, the bank can build a more resilient operational framework and maintain client trust in an increasingly complex digital environment.

Fintech Innovation and Competition

Fintech innovation is rapidly reshaping the financial services landscape, introducing formidable competition for traditional institutions like Berkshire Bank. Companies offering digital-first banking, investment platforms, and specialized financial tools are attracting customers with convenience and often lower fees. For example, the global fintech market was valued at over $2.4 trillion in 2023 and is projected to grow significantly.

Berkshire Bank needs to embrace this technological shift to remain competitive. This involves developing hybrid service models that blend digital accessibility with personalized human interaction. Exploring the integration of robo-advisory services, which leverage algorithms for investment management, could help reduce operational costs associated with traditional fund management.

Furthermore, investing in robust big data analytics capabilities is crucial for understanding customer behavior, personalizing offerings, and improving client acquisition and retention strategies. By analyzing vast datasets, Berkshire Bank can identify emerging trends and tailor its services to meet evolving customer needs more effectively.

Strategic partnerships and collaborations with agile fintech firms present another avenue for growth and innovation. These alliances can allow Berkshire Bank to quickly adopt new technologies, expand its service portfolio, and reach new customer segments without the extensive in-house development time and cost.

- Fintech Market Growth: The global fintech market's projected continued expansion underscores the urgency for traditional banks to adapt.

- Hybrid Service Models: Offering a blend of digital and in-person services caters to diverse customer preferences.

- Robo-Advisory Potential: Utilizing robo-advisors can streamline investment management and potentially lower costs.

- Data-Driven Strategies: Leveraging big data enhances customer insights for improved acquisition and retention.

- Fintech Collaborations: Partnerships offer a strategic pathway to integrate new technologies and expand services.

Cloud Computing and Infrastructure

The banking sector's increasing reliance on cloud computing presents Berkshire Bank with significant opportunities for enhanced scalability and operational efficiency. By migrating services to the cloud, the bank can more readily adjust its IT resources to meet fluctuating customer demand, a key advantage in today's dynamic financial landscape. For instance, global cloud spending by financial services firms is projected to reach over $100 billion in 2024, highlighting the industry's commitment to this technology.

However, this digital transformation necessitates a robust approach to security. Berkshire Bank must implement advanced cloud security measures, such as end-to-end encryption and continuous security audits, to safeguard sensitive customer data and ensure uninterrupted service delivery. The potential for data breaches remains a critical concern, with the financial services industry experiencing a significant number of cyberattacks annually.

Furthermore, managing the risks associated with third-party cloud service providers is paramount. Berkshire Bank needs to establish stringent vendor risk management protocols, including thorough due diligence and clear contractual obligations, to mitigate potential vulnerabilities introduced through external partnerships. As of early 2025, regulatory bodies are increasingly scrutinizing third-party risk management within financial institutions, making this a crucial area of focus.

- Scalability and Efficiency: Cloud adoption allows for dynamic resource allocation, improving responsiveness to market changes and customer needs.

- Enhanced Security Measures: Implementing strong encryption, access controls, and regular audits are vital to protect financial data in cloud environments.

- Third-Party Risk Management: Rigorous vetting and ongoing monitoring of cloud service providers are essential to prevent breaches and maintain compliance.

- Industry Trend: Financial services cloud spending is anticipated to exceed $100 billion globally in 2024, underscoring its strategic importance.

Banking's Digital Leap: AI, Fintech, Cloud Reshape Operations

Berkshire Bank must embrace AI and automation to streamline operations, from enhancing fraud detection to personalizing client wealth management. Reports from 2024 indicate a sharp rise in AI-powered cyber threats, underscoring the need for sophisticated defenses and employee training to counter these evolving risks.

Fintech innovation is a major technological factor, with the global market valued over $2.4 trillion in 2023 and expected to grow. Berkshire Bank must integrate digital solutions, potentially through robo-advisory services and data analytics, to remain competitive and improve customer engagement.

Cloud computing offers Berkshire Bank scalability and efficiency, with financial services cloud spending projected to exceed $100 billion in 2024. However, robust security measures and stringent third-party risk management are critical to protect sensitive data against increasing cyber threats.

| Technological Factor | Description | Key Data/Trend (2024/2025) | Implication for Berkshire Bank |

| AI & Automation | Integration of AI for operational efficiency and client services. | AI-powered cyberattacks on the rise; AI adoption critical for threat mitigation. | Invest in AI defenses and employee training; leverage AI for personalized services. |

| Fintech Disruption | Rise of digital-first financial services. | Global fintech market >$2.4 trillion (2023), with continued growth. | Develop hybrid models, explore robo-advisory, utilize data analytics, partner with fintechs. |

| Cloud Computing | Migration of services to cloud for scalability and efficiency. | Financial services cloud spending >$100 billion (2024). | Enhance cloud security, implement strong third-party risk management. |

Legal factors

Banking Regulations and Compliance

Berkshire Bank navigates a dense regulatory landscape, encompassing federal rules like those from the Federal Reserve and state-specific banking laws. These regulations dictate everything from initial licensing and the scope of services offered to crucial safety and soundness metrics. For instance, in 2024, the banking sector continued to see scrutiny on capital adequacy ratios, with many institutions maintaining buffers well above the minimum requirements to ensure stability.

Staying compliant requires constant vigilance, as regulations are not static; they evolve with economic conditions and policy shifts. Failure to adapt can lead to significant penalties, operational disruptions, and even the revocation of a banking license. The cost of compliance, including technology investments and personnel, remains a substantial operational expense for banks like Berkshire.

Consumer Protection Laws

Consumer protection laws, such as the Fair Credit Reporting Act and the Gramm-Leach-Bliley Act, dictate how Berkshire Bank handles customer data and offers financial products. These regulations, continually updated to address evolving digital threats and financial practices, are crucial for maintaining customer confidence. For instance, in 2024, the Consumer Financial Protection Bureau (CFPB) continued its focus on enforcing fair lending practices, impacting how banks like Berkshire Bank assess creditworthiness and market their services.

Anti-Money Laundering (AML) and Sanctions

Berkshire Bank, like all financial institutions, operates under rigorous anti-money laundering (AML) and sanctions regulations. These rules are designed to prevent illicit financial activities, and compliance is non-negotiable.

To meet these requirements, Berkshire Bank must invest heavily in sophisticated internal controls and reporting systems. These systems are crucial for identifying and flagging suspicious transactions, ensuring the bank doesn't inadvertently facilitate criminal enterprises. For instance, the Financial Crimes Enforcement Network (FinCEN) in the US reported over $5.8 trillion in suspicious activity reports (SARs) filed in 2023 alone, highlighting the sheer volume of activity financial institutions must monitor.

This commitment to compliance necessitates continuous investment in technology and specialized staff training. Keeping up with evolving regulatory landscapes and sophisticated money laundering techniques requires ongoing adaptation and resource allocation, a significant operational cost for banks.

Data Privacy Regulations

Data privacy regulations are paramount for Berkshire Bank, especially given the sensitive customer information it handles. Adhering to laws like GDPR and CCPA, which govern Personally Identifiable Information (PII), is essential for safeguarding customer data from breaches and misuse. Failure to comply can lead to significant fines; for instance, GDPR violations can result in penalties up to 4% of global annual revenue or €20 million, whichever is higher.

Maintaining strict adherence is not just about avoiding penalties but also about preserving customer trust, a cornerstone of banking. In 2023, data breaches affected millions of individuals globally, highlighting the increasing risk and the importance of robust data protection measures. Berkshire Bank's commitment to these regulations directly impacts its reputation and its ability to retain and attract customers.

- GDPR Fines: Up to 4% of global annual revenue or €20 million.

- CCPA Impact: Increased consumer rights regarding personal data collection and sale.

- Customer Trust: Data protection is a key driver of customer loyalty in the financial sector.

- 2023 Breach Statistics: Millions of individuals impacted by data compromises worldwide.

Merger and Acquisition Legal Framework

Berkshire Bank's pending merger with Brookline Bancorp, Inc. necessitates careful navigation of the intricate legal landscape governing financial institution consolidations. This involves securing necessary approvals from key regulatory bodies such as the Federal Reserve, the Office of the Comptroller of the Currency (OCC), and relevant state banking departments. For instance, the Bank Merger Act of 1960, as amended, outlines the approval process, requiring demonstration that the merger will not unduly concentrate banking power or pose a risk to financial stability.

Compliance with antitrust statutes, including the Clayton Act, is paramount to ensure the merger does not substantially lessen competition in the relevant markets. Shareholder approval is also a critical legal hurdle, requiring adherence to proxy solicitation rules and corporate governance standards. The Federal Trade Commission (FTC) and the Department of Justice (DOJ) scrutinize mergers for potential anti-competitive effects, and their review is a significant part of the legal framework.

- Regulatory Approvals: Obtaining consent from the Federal Reserve and state banking authorities is a prerequisite for finalizing the merger.

- Antitrust Compliance: Ensuring the transaction does not violate antitrust laws, preventing undue market concentration.

- Shareholder Vote: Securing approval from both Berkshire Bank and Brookline Bancorp shareholders is a mandatory legal step.

Navigating Banking's Regulatory & Merger Compliance

Berkshire Bank faces stringent legal frameworks governing its operations, from capital requirements set by the Federal Reserve to consumer protection laws like the Fair Credit Reporting Act. In 2024, the banking sector saw continued emphasis on robust capital adequacy, with institutions maintaining significant buffers above minimums to ensure stability and compliance. These evolving regulations necessitate ongoing investment in technology and specialized personnel to mitigate risks and avoid penalties.

The bank must also adhere to strict anti-money laundering (AML) and data privacy regulations, such as GDPR and CCPA, to prevent illicit financial activities and protect sensitive customer information. Failure to comply can result in substantial fines; for example, GDPR violations can incur penalties up to 4% of global annual revenue. In 2023, millions of individuals were impacted by data breaches globally, underscoring the critical importance of data protection for customer trust and regulatory adherence.

Berkshire Bank’s proposed merger with Brookline Bancorp requires navigating complex legal approvals from entities like the Federal Reserve and the OCC, alongside antitrust reviews by the FTC and DOJ. Ensuring compliance with the Bank Merger Act and antitrust statutes is crucial for the transaction's success, alongside obtaining necessary shareholder approvals. This legal diligence is paramount for a smooth consolidation and continued operational integrity.

| Regulatory Area | Key Legislation/Body | 2023/2024 Focus/Data | Impact on Berkshire Bank |

|---|---|---|---|

| Capital Adequacy | Federal Reserve | Continued scrutiny on capital buffers above minimums | Requires maintaining strong financial health |

| Consumer Protection | CFPB, FCRA | Enforcement of fair lending practices | Influences credit assessment and marketing |

| AML/Sanctions | FinCEN | Over $5.8 trillion in SARs filed in 2023 | Mandates robust internal controls and reporting |

| Data Privacy | GDPR, CCPA | Millions impacted by data breaches in 2023 | Necessitates strict data protection for trust and compliance |

| Merger Approvals | Federal Reserve, OCC, FTC, DOJ | Antitrust and financial stability reviews | Requires extensive legal and regulatory diligence |

Environmental factors

Climate Change Risk and Disclosure

The escalating frequency and severity of extreme weather events, a direct consequence of climate change, present tangible physical risks to financial institutions like Berkshire Bank. These risks can manifest as increased defaults on loans tied to vulnerable properties or businesses, thereby impacting asset quality and overall portfolio performance. For instance, the National Oceanic and Atmospheric Administration (NOAA) reported 28 separate billion-dollar weather and climate disasters in the U.S. during 2023, a record-breaking year.

While regulatory approaches to climate risk disclosure are still evolving in the U.S., with varying stances among different financial oversight bodies, Berkshire Bank has proactively acknowledged environmental sustainability. Its sustainability reports highlight a commitment to supporting low-carbon initiatives and actively assessing potential climate-related financial risks. This forward-looking approach is crucial for building resilience in the face of a changing climate and for aligning with investor expectations for environmental, social, and governance (ESG) performance.

Sustainability and ESG Initiatives

Berkshire Bank's dedication to sustainability is evident in its ESG reports, showcasing a commitment to environmental responsibility. The bank achieved 100% renewable electricity for its operations, a significant step in reducing its carbon footprint.

Furthermore, Berkshire Bank has actively worked on reducing its overall emissions, aligning with global efforts to combat climate change. These proactive environmental measures not only enhance its brand reputation but also appeal to a growing segment of investors prioritizing ESG principles.

By mitigating long-term environmental risks and demonstrating corporate citizenship, Berkshire Bank positions itself favorably in a market increasingly focused on sustainable business practices. This focus can lead to stronger investor relations and a more resilient business model.

Green Lending and Sustainable Finance

The financial sector is experiencing a significant shift towards green lending and sustainable finance, driven by increasing investor and consumer demand for environmentally responsible products. Berkshire Bank's strategic focus on environmental sustainability and its support for low-carbon initiatives through its 'BEST Community Comeback' program directly aligns with this growing market trend.

By offering tailored financial solutions for businesses and individuals prioritizing environmental consciousness, Berkshire Bank is well-positioned to tap into new revenue streams and enhance its market share in this expanding segment. For instance, as of early 2024, sustainable finance assets globally were projected to reach over $50 trillion, highlighting the substantial opportunity.

Resource Management and Operational Footprint

Berkshire Bank, like many financial institutions, actively manages its operational environmental footprint. This includes monitoring and aiming to reduce energy consumption, waste generation, and water usage across its branches and corporate offices.

The bank's commitment to sustainability is demonstrated through initiatives focused on lowering emissions and increasing the use of renewable electricity. For example, in 2023, Berkshire Bank reported a 15% reduction in its overall energy consumption compared to its 2020 baseline, partly through upgrades to energy-efficient lighting and HVAC systems.

These efforts not only align with environmental goals but also present opportunities for cost savings. By optimizing resource use, Berkshire Bank can lower utility expenses, a tangible benefit that supports its financial performance.

- Energy Consumption: Berkshire Bank is investing in energy-efficient technologies, aiming for a 20% reduction in energy use by 2025.

- Waste Reduction: The bank has implemented enhanced recycling programs, targeting a 25% decrease in landfill waste by the end of 2024.

- Water Usage: Water conservation measures in facilities have led to a 10% decrease in water consumption in 2023 compared to the previous year.

- Renewable Energy: Berkshire Bank is working towards sourcing 50% of its electricity from renewable sources by 2026.

Regulatory and Public Pressure for Environmental Responsibility

Despite some U.S. financial regulators easing climate risk disclosure requirements, a strong current of public and international demand persists for financial institutions to showcase their environmental commitment. Berkshire Bank's commitment to Environmental, Social, and Governance (ESG) reporting, with a particular emphasis on environmental sustainability, positions it well to satisfy stakeholder expectations.

This proactive stance is crucial for maintaining a favorable reputation in a landscape where 73% of investors consider ESG factors when making investment decisions, according to a 2024 survey by Morgan Stanley. Berkshire Bank's efforts in areas like reducing its operational carbon footprint, which saw a 5% decrease in Scope 1 and 2 emissions in 2023, directly address this pressure.

- Stakeholder Expectations: Meeting the growing demand from customers, employees, and investors for demonstrable environmental stewardship.

- Reputation Management: Proactively addressing environmental concerns enhances brand image and trust.

- International Standards: Aligning with global trends in climate-related financial disclosures, even if domestic regulations fluctuate.

- Competitive Advantage: Differentiating Berkshire Bank as a responsible financial partner in an increasingly eco-conscious market.

Bank's Green Push: Cutting Waste & Emissions

Berkshire Bank is actively addressing environmental factors, including a commitment to reducing its operational footprint. The bank aims for a 20% reduction in energy use by 2025 and has implemented enhanced recycling programs to decrease landfill waste by 25% by the end of 2024. These initiatives are crucial as 73% of investors consider ESG factors in their decisions, a trend Berkshire Bank's 5% reduction in Scope 1 and 2 emissions in 2023 directly addresses.

| Environmental Initiative | Target/Status | Year | Impact |

|---|---|---|---|

| Energy Consumption Reduction | 20% reduction | 2025 | Lower operational costs, reduced carbon footprint |

| Waste Reduction | 25% decrease in landfill waste | 2024 | Improved resource management, reduced environmental impact |

| Scope 1 & 2 Emissions Reduction | 5% reduction | 2023 | Demonstrates commitment to climate action |

| Renewable Electricity Sourcing | 50% | 2026 | Further reduces reliance on fossil fuels |

PESTLE Analysis Data Sources

Our PESTLE Analysis for Berkshire Bank is constructed using a blend of publicly available data from financial regulatory bodies, economic indicators, and industry-specific reports. This ensures a comprehensive understanding of the political, economic, social, technological, legal, and environmental factors influencing the bank's operating landscape.