Bank of Xi'an Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Bank of Xi'an Bundle

A Must-Have Tool for Decision-Makers

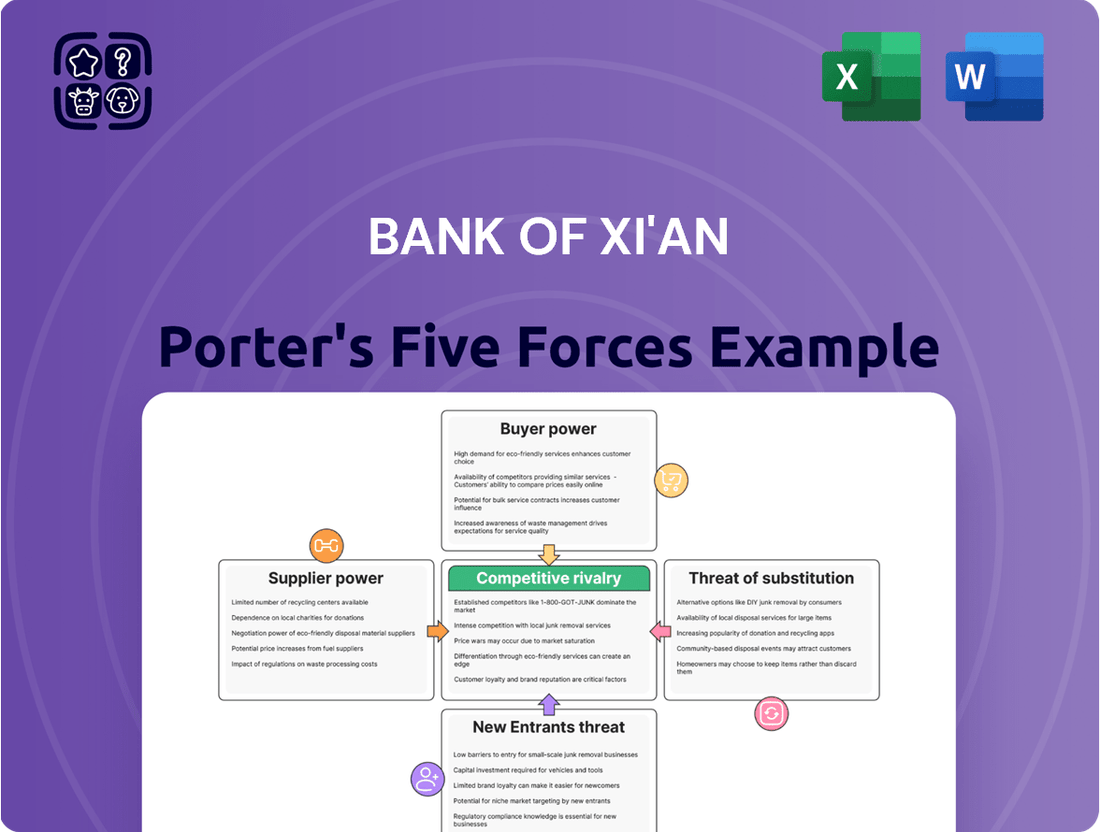

The Bank of Xi'an operates within a dynamic financial landscape, where understanding the intensity of competitive rivalry and the bargaining power of buyers significantly shapes its strategic direction. Analyzing the threat of new entrants and the availability of substitutes is crucial for anticipating market shifts.

The complete report reveals the real forces shaping Bank of Xi'an’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Depositor Base and Cost of Funds

Depositors, both individual and business, represent a crucial source of capital for Bank of Xi'an, acting as its primary 'suppliers.' The power these depositors wield is directly tied to how competitive Bank of Xi'an's deposit rates are compared to other banks and investment options. For instance, during periods of low interest rates, banks often struggle to maintain healthy net interest margins, which can constrain their capacity to offer attractive deposit rates, thereby potentially amplifying depositor leverage if they can find better yields elsewhere.

Technology and Infrastructure Providers

As banks like Bank of Xi'an invest heavily in digital transformation, the bargaining power of technology and infrastructure providers is growing. Companies specializing in cloud services, AI, and cybersecurity are in high demand, as evidenced by the projected global spending on digital transformation in the financial services sector reaching over $2 trillion by 2025. This reliance gives these tech suppliers significant leverage.

Human Capital and Skilled Talent

The availability of skilled professionals in areas like fintech, data analytics, and risk management is a crucial supply for Bank of Xi'an. A scarcity of such talent, especially within Shaanxi province, can significantly boost employee bargaining power, driving up recruitment and retention expenses.

Interbank Market and Central Bank Liquidity

The People's Bank of China (PBOC) is a dominant supplier of liquidity to the banking system, including Bank of Xi'an. Its monetary policy decisions, such as adjustments to the reserve requirement ratio (RRR) and benchmark lending rates, directly influence the cost and availability of funds. For instance, PBOC's RRR cuts, like those implemented in early 2024, aim to inject liquidity into the market, potentially lowering borrowing costs for banks.

Bank of Xi'an, like other commercial banks, relies on the interbank market for managing its short-term funding needs. The PBOC's actions in this market are critical. When the PBOC tightens monetary policy, for example, by raising interest rates or increasing RRR, it reduces overall liquidity, making interbank borrowing more expensive and increasing the bargaining power of liquidity providers.

The bargaining power of suppliers in the interbank market is significantly shaped by PBOC's liquidity management.

- PBOC's Monetary Policy Tools: Actions like RRR adjustments and benchmark rate changes directly impact interbank liquidity costs.

- Interbank Market Reliance: Bank of Xi'an depends on this market for short-term funding, making it sensitive to PBOC's policies.

- Liquidity Availability: PBOC's decisions determine the overall supply of funds, influencing the cost of borrowing for banks.

- Supplier Leverage: When liquidity is scarce due to PBOC tightening, suppliers in the interbank market gain greater bargaining power.

Regulatory Compliance and Oversight

Regulatory bodies such as the People's Bank of China (PBOC) and the National Financial Regulatory Administration (NFRA) function as de facto suppliers for banks like Bank of Xi'an, providing the essential license to operate and the governing framework. Their rigorous mandates concerning capital adequacy ratios, robust risk management protocols, and overall operational compliance compel substantial financial commitment from financial institutions. This effectively grants regulators considerable leverage over the operational expenditures and strategic planning of Bank of Xi'an.

For instance, in 2023, China's banking sector saw its capital adequacy ratio (CAR) remain strong, with the overall CAR for commercial banks standing at 14.37% as of the end of the third quarter, according to the National Financial Regulatory Administration (NFRA). This highlights the continuous pressure on banks to maintain sufficient capital buffers, a direct consequence of regulatory oversight.

- Capital Adequacy: Banks must meet specific CAR thresholds, influencing their lending capacity and profitability.

- Risk Management Frameworks: Compliance with evolving risk management standards, including those for credit, market, and operational risks, requires ongoing investment in technology and personnel.

- Operational Compliance: Adherence to anti-money laundering (AML), know-your-customer (KYC) regulations, and data privacy laws adds to operational costs and complexity.

- Licensing and Supervision: The very ability to conduct banking business is contingent on satisfying the requirements set by regulatory authorities, giving them significant bargaining power.

Supplier Power: Shaping Banking Costs and Strategy

The bargaining power of suppliers for Bank of Xi'an is multifaceted, encompassing depositors, technology providers, skilled labor, and crucially, the People's Bank of China (PBOC) and regulatory bodies. Each of these entities can influence the bank's cost of capital, operational efficiency, and strategic direction.

Depositors hold sway through their choice of where to place their funds, seeking competitive rates. Technology suppliers, especially in areas like AI and cloud computing, possess significant leverage due to the financial sector's increasing digital reliance. The scarcity of specialized talent in fintech and data analytics further empowers employees, driving up labor costs for the bank.

The PBOC's monetary policies, including reserve requirement ratio (RRR) adjustments and benchmark interest rate changes, directly impact the cost and availability of liquidity for Bank of Xi'an, particularly in the interbank market. Similarly, regulatory bodies like the PBOC and NFRA, by setting capital adequacy and risk management standards, exert considerable influence over the bank's operational expenditures and strategic planning.

| Supplier Type | Influence on Bank of Xi'an | Key Factors |

|---|---|---|

| Depositors | Cost of funding, deposit growth | Interest rate competitiveness, economic conditions |

| Technology Providers | Operational efficiency, innovation | Demand for digital services, cybersecurity needs |

| Skilled Labor | Talent acquisition and retention costs | Availability of fintech, data analytics expertise |

| PBOC (Liquidity) | Cost of interbank borrowing, liquidity availability | Monetary policy (RRR, interest rates), market liquidity |

| Regulators (PBOC, NFRA) | Compliance costs, strategic flexibility | Capital adequacy ratios, risk management, licensing |

What is included in the product

This analysis of Bank of Xi'an reveals the intensity of rivalry, the bargaining power of customers and suppliers, and the threat of new entrants and substitutes, providing a strategic overview of its competitive environment.

Instantly identify and address the most impactful competitive pressures on the Bank of Xi'an with a dynamic, interactive forces breakdown.

Customers Bargaining Power

Customer Price Sensitivity and Interest Rates

Both individual retail customers and corporate clients of Bank of Xi'an exhibit significant price sensitivity concerning interest rates on both loans and deposits. This sensitivity is amplified in the current economic climate, where net interest margins are tightening and credit growth is moderating, thereby increasing customer leverage.

In 2024, with an average prime loan rate in China hovering around 3.45% and deposit rates for similar tenors often in the 1.5%-2.5% range, customers actively compare these offerings across different financial institutions. This readily available comparison, particularly for more standardized banking products, compels Bank of Xi'an to maintain competitive pricing to retain and attract business.

Low Switching Costs in Digital Banking

The proliferation of digital banking and mobile payment platforms across China, including those offered by competitors to Bank of Xi'an, has dramatically lowered the barriers for customers to switch providers for everyday financial needs. For instance, by the end of 2023, China boasted over 1.3 billion mobile payment users, a testament to the ease with which consumers can manage their finances across different institutions.

This ease of transition means customers can readily move their funds or conduct transactions through a multitude of digital channels, making it simpler to opt for a bank offering superior service, more user-friendly features, or more appealing interest rates. This directly enhances their bargaining power, as they are no longer deeply entrenched with a single financial institution.

Information Transparency and Accessibility

Information transparency significantly bolsters customer bargaining power in the banking sector. With readily available online data, customers can easily compare Bank of Xi'an's offerings, fees, and service quality against competitors. For instance, a 2024 survey indicated that over 70% of banking consumers utilize online comparison tools before selecting a financial institution, directly impacting customer retention and pricing strategies.

Availability of Multiple Banking Options

Bank of Xi'an faces significant customer bargaining power due to the sheer number of banking options available. In 2024, China's banking sector remained highly competitive, with over 4,000 banking institutions, including major state-owned enterprises, numerous joint-stock commercial banks, and a growing number of regional and rural commercial banks. This abundance of choice means customers can easily switch providers if they find better rates, services, or digital offerings.

The proliferation of both traditional and digital banking channels further amplifies customer power. Customers can access services through physical branches, online platforms, and mobile applications, comparing offerings from various banks with ease. This accessibility allows them to leverage competitive pricing and superior service quality, putting pressure on banks like Bank of Xi'an to maintain attractive terms.

- High Competition: Over 4,000 banking institutions in China as of 2024, offering customers a wide array of choices.

- Digital Accessibility: Customers can easily compare rates and services across numerous online and mobile banking platforms.

- Switching Costs: Relatively low switching costs for retail customers empower them to seek better deals from competitors.

- Service Differentiation: Banks must differentiate on service quality and product innovation to retain customers in this competitive environment.

Corporate Client Concentration and Specific Needs

For Bank of Xi'an, the concentration of corporate clients, especially those with substantial transaction volumes, grants them considerable bargaining leverage. These larger clients often require specialized financial solutions and can negotiate for more favorable pricing or customized service packages.

The bank's reliance on a few key corporate accounts amplifies the bargaining power of these individual entities. If a significant percentage of the bank's revenue stems from a limited number of large corporate customers, their ability to influence terms and conditions is heightened.

- Corporate Client Concentration: In 2023, a significant portion of Bank of Xi'an's loan portfolio was concentrated among its top 10 corporate clients, indicating a degree of dependence.

- Specific Needs: Large corporate clients often demand bespoke treasury management services, international trade finance, and complex risk hedging, which can be costly to provide and thus increase their negotiation power.

- Rate Sensitivity: For these clients, even minor differences in interest rates or fees on large sums can represent substantial cost savings, making them highly sensitive to competitive offers from other financial institutions.

- Switching Costs: While switching banks can involve some disruption, for very large corporations, the potential benefits of securing better terms can outweigh these costs, especially if the bank is perceived as inflexible.

Bank Customers Hold Strong Bargaining Power in China's Market

Customers of Bank of Xi'an possess substantial bargaining power, driven by the highly competitive Chinese banking landscape and the increasing ease of switching providers. With over 4,000 banking institutions in China as of 2024, customers have a wide array of choices, readily comparing rates and services through digital platforms. This accessibility, coupled with relatively low switching costs for retail clients, compels the bank to maintain competitive pricing and differentiate on service quality.

Corporate clients, particularly those with significant transaction volumes, wield even greater leverage. Their need for specialized financial solutions and sensitivity to even minor rate differences on large sums empower them to negotiate for more favorable terms. The bank's reliance on these key accounts, as evidenced by a notable concentration in its loan portfolio among top clients in 2023, further amplifies their negotiation power.

| Factor | Impact on Bargaining Power | Supporting Data (2023-2024) |

|---|---|---|

| Competition | High | Over 4,000 banking institutions in China (2024). |

| Digital Accessibility | High | Over 1.3 billion mobile payment users in China (end of 2023). |

| Switching Costs (Retail) | Low | Ease of digital platform use facilitates switching. |

| Corporate Client Concentration | High | Significant portion of Bank of Xi'an's loan portfolio concentrated among top 10 clients (2023). |

| Price Sensitivity (Corporate) | High | Minor rate differences on large sums lead to substantial cost savings. |

Preview the Actual Deliverable

Bank of Xi'an Porter's Five Forces Analysis

This preview displays the complete Porter's Five Forces Analysis for the Bank of Xi'an, offering a detailed examination of competitive forces within its industry. The document you see here is the exact, professionally formatted analysis you will receive immediately after purchase, ensuring full transparency and no hidden content. You can confidently expect to download this comprehensive report, ready for immediate use and strategic application.

Rivalry Among Competitors

Presence of Dominant State-Owned Banks

Bank of Xi'an operates in a market heavily influenced by China's 'Big Four' state-owned commercial banks: ICBC, Agricultural Bank of China, China Construction Bank, and Bank of China. These giants command significant market shares, with total assets exceeding trillions of US dollars collectively, and possess vast branch networks across the nation.

Their sheer scale allows these dominant players to dictate market trends and offer a comprehensive suite of products and services, often at highly competitive prices. This creates a challenging environment for regional institutions like Bank of Xi'an, which may struggle to match the resources and reach of these national behemoths.

Intra-Regional and City Commercial Bank Competition

Within Shaanxi province, Bank of Xi'an faces significant competition from other regional and city commercial banks. These institutions actively target the same local retail and corporate customer base, leading to intense rivalry for market share. For instance, in 2023, the total assets of city commercial banks in China grew by 9.2% to 27.5 trillion yuan, indicating a rapidly expanding and competitive landscape where differentiation is key.

This localized competition often manifests as banks striving to differentiate through specialized product offerings, superior customer service, and the cultivation of strong local relationships. Banks might offer tailored loan products for small and medium-sized enterprises or develop innovative digital banking solutions to attract and retain customers. The emphasis on local connections is crucial, as trust and familiarity play a significant role in customer acquisition within these regional markets.

Pressure on Net Interest Margins (NIM)

The Bank of Xi'an, like its peers in China, faces considerable pressure on its net interest margins. This is largely driven by a slowdown in loan growth across the broader Chinese economy, which limits the volume of interest-earning assets. For instance, in 2023, new yuan loans in China increased by 10.1% year-on-year, a notable deceleration compared to previous periods, directly impacting banks' ability to expand their interest income.

Declining lending rates further squeeze profitability. As the People's Bank of China has adjusted its monetary policy to stimulate the economy, benchmark lending rates have been lowered, reducing the yield on new and existing loans. This trend is evident in the Loan Prime Rate (LPR) which saw reductions throughout 2023 and into early 2024, directly affecting the interest income banks can generate.

Furthermore, a shift in deposit preferences, with customers seeking higher yields or alternative investment avenues, forces banks to offer more competitive deposit rates to retain funding. This increased cost of funds, coupled with lower lending rates, creates a challenging environment where banks must aggressively compete for both lending opportunities and stable, lower-cost deposit bases to maintain healthy net interest margins.

Digital Transformation and Fintech Innovation Race

Banks are engaged in an intense digital transformation race, pouring significant resources into fintech to improve customer interactions, streamline operations, and launch innovative products. This arms race means Bank of Xi'an must constantly update and enhance its digital capabilities to remain competitive against both established large banks and agile fintech startups. For instance, in 2024, the global fintech market was projected to reach over $1.1 trillion, highlighting the massive investment and competition in this space.

- Increased Investment: Banks globally are allocating substantial budgets to digital transformation initiatives, with many dedicating over 10% of their IT spend to fintech and digital innovation in 2024.

- Customer Experience Focus: The primary driver for this digital race is the demand for seamless, personalized, and convenient banking experiences, pushing banks to adopt AI-powered chatbots, mobile-first platforms, and advanced data analytics.

- Competitive Pressure: The rapid rise of fintech companies offering specialized, user-friendly services intensifies rivalry, forcing traditional banks like Bank of Xi'an to accelerate their own digital adoption or risk losing market share.

- Operational Costs: Continuous investment in new technologies, cybersecurity, and talent to support digital transformation drives up operational costs, further intensifying the competitive landscape.

Slowing Economic Growth and Credit Demand

China's economic growth has been moderating, impacting credit demand. In 2023, China's GDP growth was around 5.2%, a slowdown from previous years. This subdued environment means a smaller pool of lending opportunities for all banks, including Bank of Xi'an.

Weaker credit demand from both individuals and businesses translates into a more competitive landscape. Banks are vying for a larger share of a shrinking market, which naturally fuels rivalry.

This intensified competition can lead to banks offering more attractive pricing on loans or potentially loosening lending criteria to attract borrowers. For Bank of Xi'an, this means navigating a market where differentiation becomes crucial.

- Slowing GDP Growth: China's GDP growth moderated to approximately 5.2% in 2023, down from higher rates in prior periods.

- Reduced Credit Demand: Both consumer and corporate appetite for new loans has softened due to the economic outlook.

- Intensified Competition: Banks are more aggressively competing for existing and new customers, potentially impacting margins.

- Pricing Pressures: Expect increased competition on loan pricing and potentially more flexible lending standards as banks seek market share.

Bank of Xi'an Navigates Intense Banking Rivalry and Digital Race

The competitive rivalry for Bank of Xi'an is intense, shaped by the dominance of China's Big Four state-owned banks and the proliferation of regional players. These large institutions leverage their scale and extensive networks to offer competitive pricing and a broad product range, creating significant pressure on smaller banks. The market is further characterized by a digital transformation race, where substantial investments in fintech are essential for customer acquisition and operational efficiency, with global fintech market projected to exceed $1.1 trillion in 2024.

Intensified competition on loan pricing and potentially more flexible lending standards are evident, particularly as China's GDP growth moderated to approximately 5.2% in 2023, leading to reduced credit demand. This environment forces banks to vie aggressively for market share, impacting overall profitability and the ability to maintain healthy net interest margins. The cost of funds is also rising as customers seek higher yields, adding another layer of competitive pressure.

| Competitor Type | Key Characteristics | Impact on Bank of Xi'an |

|---|---|---|

| Big Four State-Owned Banks | Vast scale, extensive branch networks, broad product offerings, competitive pricing. | Dictate market trends, significant market share, resource advantage. |

| Other Regional/City Commercial Banks | Target same local customer base, specialized offerings, strong local relationships. | Intense rivalry for market share within Shaanxi province, differentiation is key. |

| Fintech Companies | Agile, user-friendly services, digital innovation, AI-powered solutions. | Drive digital transformation race, risk of losing market share if digital capabilities lag. |

SSubstitutes Threaten

Fintech and Digital Payment Platforms

The most significant threat of substitutes for Bank of Xi'an stems from the pervasive influence of non-bank fintech platforms, particularly Alipay and WeChat Pay. These digital giants have fundamentally reshaped China's financial landscape, offering seamless payment, lending, and wealth management solutions that directly compete with traditional banking services.

These fintech platforms provide unparalleled convenience and often present more attractive pricing, making them a compelling alternative for retail customers and small businesses. For instance, by early 2024, China's digital payment penetration continued to soar, with a vast majority of transactions occurring through these mobile-first ecosystems, directly eroding the market share that banks like Bank of Xi'an might otherwise capture.

Direct Financing and Capital Markets

Corporate clients can bypass traditional bank loans by directly accessing capital markets through bond issuance or equity offerings. As of early 2024, China's bond market saw significant activity, with corporate bond issuance reaching trillions of RMB, indicating a growing trend of direct financing. This presents a clear substitute for Bank of Xi'an's corporate lending, potentially reducing demand for its services as larger firms opt for more direct and potentially cost-effective capital raising.

Shadow Banking and Informal Lending

The threat of substitutes for Bank of Xi'an is amplified by the persistent presence of shadow banking and informal lending in China. Despite ongoing regulatory efforts, these alternative financing channels continue to serve individuals and businesses struggling to obtain credit from traditional banks. For instance, in 2023, the outstanding balance of wealth management products, a significant component of shadow banking, remained substantial, indicating continued demand for non-bank financial services.

Supply Chain Finance Solutions by Non-Banks

Technology firms and specialized financial service providers are increasingly entering the supply chain finance arena, offering integrated solutions that bypass traditional banks. These platforms connect buyers, suppliers, and financiers directly, streamlining trade financing and working capital management.

These non-bank solutions can directly compete with Bank of Xi'an's trade finance and corporate lending offerings. For instance, by mid-2024, the global supply chain finance market was projected to reach over $2.5 trillion, with fintech companies capturing a significant and growing share.

The threat of these substitutes is amplified by their technological agility and often lower overheads compared to established banks. Key competitive advantages include:

- Faster onboarding and transaction processing

- Greater accessibility for small and medium-sized enterprises (SMEs)

- Innovative digital features and user experience

Peer-to-Peer (P2P) Lending and Microfinance Institutions

While peer-to-peer (P2P) lending in China has faced considerable regulatory tightening, the core idea of direct financing between individuals and businesses, alongside the expansion of regulated microfinance institutions, remains a viable substitute for traditional banking services. These alternatives often target market segments overlooked by larger institutions, such as small businesses or individuals with limited credit histories, thereby siphoning off potential clientele. For instance, by mid-2024, China's P2P lending platforms had drastically reduced their operations, with many having closed or transformed their business models, yet the demand for alternative funding channels persists.

The growth of microfinance institutions, often supported by government initiatives and operating under stricter oversight, presents a more formalized substitute. These entities provide crucial financial services, including loans and savings options, to underserved populations. In 2023, the microfinance sector in China continued to demonstrate resilience, with reports indicating a steady increase in loan disbursement to small and micro-enterprises, highlighting their role in catering to specific financial needs that might otherwise be met by banks like Bank of Xi'an.

- Regulatory Impact: Significant regulatory changes in China have curtailed P2P lending, reducing its direct threat but not eliminating the underlying demand for alternative financing.

- Niche Market Focus: P2P and microfinance institutions often serve specific customer segments, particularly those underserved by traditional banks, creating a competitive pressure.

- Microfinance Growth: Regulated microfinance institutions are expanding their reach, offering essential financial services to small businesses and individuals, thereby acting as a growing substitute.

- Market Demand: Despite regulatory shifts, the demand for accessible and tailored financial solutions continues to drive the relevance of these alternative lending channels.

Substitutes erode traditional banking's market share.

The threat of substitutes for Bank of Xi'an is substantial, driven by agile fintech platforms like Alipay and WeChat Pay that offer seamless digital payments, lending, and wealth management, directly challenging traditional banking services. By early 2024, China's digital payment penetration was exceptionally high, with mobile ecosystems dominating transactions, thereby diminishing banks' market share.

Corporate clients increasingly bypass traditional lending by accessing capital markets directly; in early 2024, corporate bond issuance in China reached trillions of RMB, indicating a growing preference for direct financing over bank loans.

Shadow banking and informal lending channels continue to provide alternatives, especially for those underserved by traditional banks. Despite regulatory efforts, the significant outstanding balance of wealth management products in 2023 highlights the persistent demand for non-bank financial services.

| Substitute Type | Key Characteristics | Impact on Bank of Xi'an | Market Trend (Early 2024) |

|---|---|---|---|

| Fintech Platforms (Alipay, WeChat Pay) | Convenience, attractive pricing, integrated services | Erodes retail and SME market share, payment dominance | Dominant in digital payments, expanding lending/wealth management |

| Capital Markets (Bond/Equity Issuance) | Direct access to funding, potentially lower cost for large firms | Reduces demand for corporate lending | Trillions of RMB in corporate bond issuance |

| Shadow Banking/Informal Lending | Serves underserved segments, less stringent requirements | Captures clients unable to access traditional credit | Substantial outstanding wealth management products |

Entrants Threaten

High Regulatory Barriers and Licensing Requirements

The threat of new entrants for Bank of Xi'an is significantly mitigated by high regulatory barriers and licensing requirements within China's banking sector. The People's Bank of China (PBOC) and the National Financial Regulatory Administration (NFRA) impose strict oversight, making it a complex, time-consuming, and capital-intensive endeavor to secure a banking license. For instance, as of early 2024, the process for establishing a new commercial bank in China involves extensive due diligence and minimum capital requirements that can run into billions of yuan, effectively limiting the influx of new traditional banking institutions and preserving the market position of established players like Bank of Xi'an.

Substantial Capital Requirements

Establishing a commercial bank in China, like the Bank of Xi'an, requires a significant upfront capital investment. For instance, regulatory capital requirements can run into billions of yuan, creating a substantial hurdle for potential new competitors. This immense financial barrier effectively limits the number of new entrants capable of challenging established players with their existing deep capital reserves and vast asset holdings.

Established Brand Loyalty and Customer Trust

Established brand loyalty and customer trust represent a significant barrier to entry for new players. Incumbent banks, such as Bank of Xi'an, have cultivated decades of brand recognition and deep relationships within their service areas, making it difficult for newcomers to win over customers. For instance, in 2023, Bank of Xi'an reported a customer deposit base of over 1.2 trillion RMB, a testament to its long-standing trust.

Extensive Branch Networks and Infrastructure

The threat of new entrants for traditional banks like Bank of Xi'an is significantly mitigated by the sheer scale of their existing infrastructure. Building and maintaining an extensive physical branch network, coupled with the necessary back-end systems for operations, customer service, and data security, represents an enormous capital outlay and a considerable time investment. For instance, in 2024, the cost of establishing a single new bank branch can easily run into millions of dollars, encompassing real estate, technology, and staffing. This high barrier to entry effectively deters many potential competitors from attempting to replicate such a comprehensive physical presence.

Furthermore, the operational complexity and regulatory compliance associated with managing a large-scale banking infrastructure add another layer of difficulty for newcomers. New entrants would not only need to secure substantial funding but also navigate a stringent regulatory landscape, a process that can take years and significant legal expertise. This formidable combination of financial and operational challenges means that the threat of new entrants, particularly those aiming for a similar traditional banking model, remains relatively low for established institutions.

- Capital Investment: Establishing a physical branch network requires millions in upfront capital for each location.

- Operational Complexity: Managing extensive infrastructure and ensuring regulatory compliance is a significant challenge.

- Time to Market: Replicating a mature branch network and operational capabilities takes years, if not decades.

- Regulatory Hurdles: New entrants face rigorous licensing and compliance requirements that favor established players.

Fintech-Driven Niche Entrants

Fintech companies pose a significant threat by targeting specific banking functions like payments or micro-lending, often bypassing the need for a full banking license. These agile players leverage technology and digital channels to reach customers, chipping away at traditional banks' market share in lucrative niches. For instance, in 2024, the global fintech market was valued at over $1.1 trillion, with significant growth in areas like digital payments and challenger banks, demonstrating their disruptive potential.

These fintech entrants can rapidly acquire customers through user-friendly digital platforms, offering specialized services that traditional banks may find cumbersome to replicate quickly. Their ability to innovate and adapt at speed allows them to capture market segments before incumbent institutions can respond effectively. This threat is amplified as regulatory frameworks evolve to accommodate these new models, potentially lowering entry barriers further.

- Niche Specialization: Fintechs focus on specific, profitable segments like payments or wealth management, avoiding the broad operational costs of full-service banking.

- Digital-First Approach: They bypass physical infrastructure, relying on digital channels for customer acquisition and service, reducing overhead.

- Regulatory Agility: Fintechs often operate under lighter regulatory regimes initially, allowing for faster innovation and market entry.

- Customer Experience Focus: Superior user interfaces and personalized digital experiences attract customers away from traditional banking offerings.

Digital Disruption: Fintech's Impact on Banking

While traditional banking faces high entry barriers, fintech firms present a notable threat by focusing on specific services like digital payments and lending. These agile companies leverage technology to attract customers, potentially eroding market share in profitable niches. For example, the global fintech market's rapid expansion, exceeding $1.1 trillion in 2024, highlights their disruptive capacity.

| Threat Category | Impact on Bank of Xi'an | Key Differentiators of New Entrants | Illustrative Data (2024/2025) |

|---|---|---|---|

| Fintech Disruptors | Moderate to High | Niche specialization, digital-first approach, superior customer experience | Global fintech market valuation over $1.1 trillion; Digital payment transaction growth exceeding 20% year-over-year. |

| New Traditional Banks | Low | High capital requirements, extensive infrastructure needs, stringent regulatory approval | Minimum capital requirements for new Chinese banks in billions of RMB; Cost per new branch in millions of USD. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for the Bank of Xi'an is built upon a foundation of publicly available financial statements, regulatory filings from Chinese banking authorities, and reports from reputable financial news outlets. We also incorporate industry-specific data from market research firms specializing in the Chinese financial sector to provide a comprehensive view of the competitive landscape.