Bank Of Gansu Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Bank Of Gansu

Don't Miss the Bigger Picture

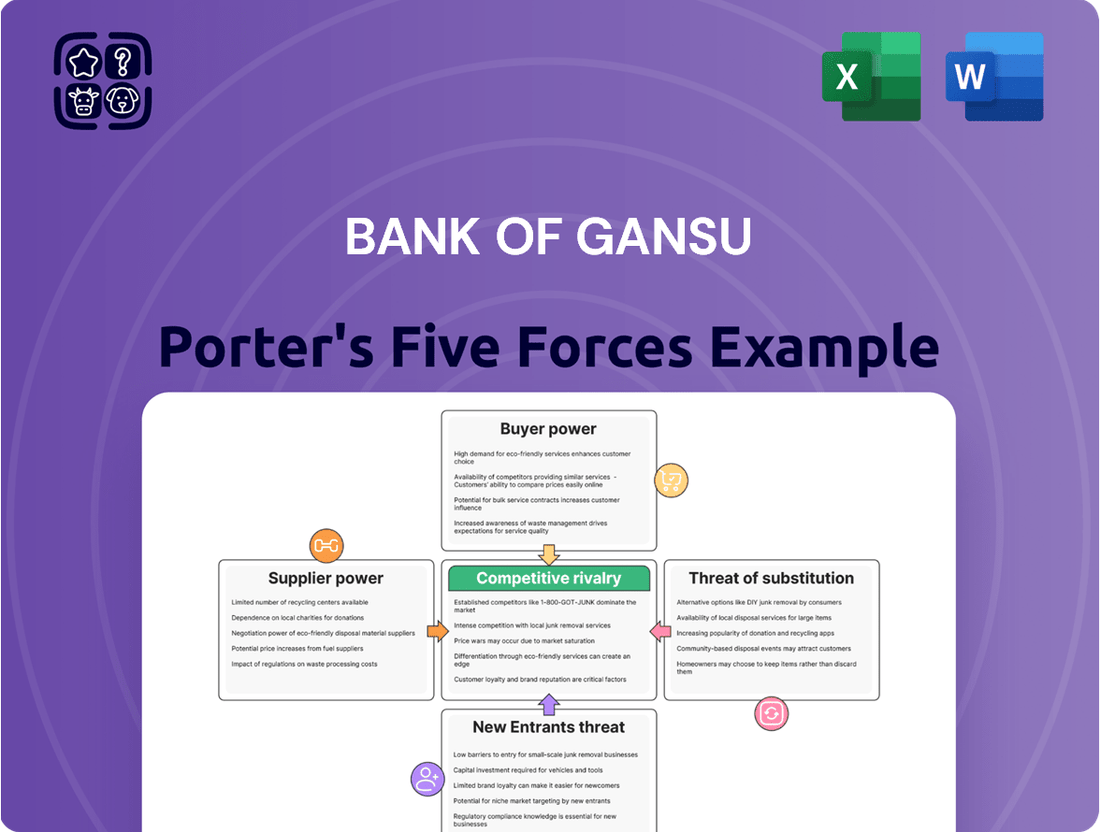

The Bank of Gansu operates within a dynamic financial landscape, where understanding the competitive forces at play is paramount. Our Porter's Five Forces analysis delves into the intense rivalry among existing banks, highlighting how this impacts pricing and profitability.

We examine the bargaining power of buyers, specifically the customers, and how their choices influence the bank's strategies and service offerings.

The threat of new entrants is also a critical factor, as a lower barrier to entry could reshape the competitive intensity within the regional banking sector.

Furthermore, the analysis scrutinizes the bargaining power of suppliers, including technology providers and capital sources, and their leverage over the Bank of Gansu.

Finally, we assess the threat of substitute products or services, considering how alternative financial solutions might erode the bank's market share.

The complete report reveals the real forces shaping Bank Of Gansu’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Funding Source Concentration

The Bank of Gansu's primary suppliers are its funding sources, including retail and corporate depositors and interbank borrowings. A significant concentration of deposits from a few large corporate or government entities directly enhances their bargaining power. As of December 2023, corporate deposits constituted a substantial portion of the bank's total deposits, reflecting this potential vulnerability. Should a few major clients withdraw funds or demand higher interest rates, it could significantly impact the bank's liquidity and cost of funds. This dynamic necessitates a diversified funding base to mitigate supplier power.

Employee and Labor Market

The Bank of Gansu's employees, particularly those with specialized skills in areas like finance, technology, and risk management, act as crucial suppliers of labor. The competitive landscape of the labor market within Gansu province and the broader Chinese banking sector directly influences their wage demands and potential employee turnover rates. A notable shortage of highly skilled banking professionals, evident as the sector continues to digitalize in 2024, significantly enhances the bargaining power of these employees. This scarcity can lead to increased salary expectations and higher recruitment costs for the bank.

Technology and System Vendors

Bank of Gansu relies heavily on external vendors for core banking systems, digital platforms, and cybersecurity solutions. The market for these specialized technologies, particularly for established enterprise-grade software, often sees consolidation among a few dominant global and domestic providers by 2024. This concentration grants these vendors significant leverage, influencing pricing and the pace of technological upgrades for banks. For instance, the global core banking software market was projected to continue its growth trajectory into 2024, with major players holding substantial market share.

Regulatory and Compliance Services

Bank of Gansu must navigate the complex and evolving regulatory environment set by Chinese financial authorities, including the People's Bank of China and the National Financial Regulatory Administration. Suppliers providing regulatory and compliance services, such as auditing firms and legal counsel, hold significant power due to the mandatory nature of their offerings. These specialized services are critical for the bank to avoid substantial penalties and operational disruptions, reflecting their indispensable role in maintaining market access. For instance, compliance costs for financial institutions globally continue to rise, with many banks allocating over 10% of their operational budget to regulatory adherence in 2024.

- Regulatory compliance expenditures for Chinese banks are projected to increase by over 8% in 2024, driven by new data security and anti-money laundering regulations.

- The number of regulatory updates issued by the NFRA alone exceeded 150 in the first half of 2024, requiring constant adaptation.

- Major auditing firms increased their fees for financial sector clients by an average of 7% in 2024 due to heightened scrutiny and demand for specialized expertise.

- Legal advisory fees related to financial compliance saw an average rise of 5-6% in China during 2024, reflecting the complexity of new regulatory frameworks.

Interbank Lending Market

The Bank of Gansu actively uses the interbank market to manage its short-term liquidity needs. The People's Bank of China's (PBOC) monetary policy significantly shapes the interest rates and terms in this crucial market. In 2024, the PBOC has maintained an accommodative stance, with the 7-day reverse repo rate at 1.80%, influencing overall interbank borrowing costs. However, during periods of tight system-wide liquidity, banks with surplus funds, acting as suppliers, gain substantial bargaining power over borrowers like Bank of Gansu.

- PBOC's 2024 7-day reverse repo rate: 1.80%.

- Interbank market turnover in China exceeded 200 trillion CNY monthly in early 2024.

- Tight liquidity conditions empower lending banks.

Rising Supplier Power Squeezes Bank Costs

Bank of Gansu faces significant supplier power from diverse sources, impacting costs and operations. Large corporate depositors and interbank lenders hold sway, with PBOC’s 7-day reverse repo rate at 1.80% in 2024 influencing borrowing costs. Skilled employees, especially in tech, gain leverage due to market scarcity, leading to higher recruitment expenses.

Moreover, specialized external vendors for core banking systems and critical regulatory compliance service providers, like auditors and legal counsel, exert substantial power. Regulatory compliance expenditures for Chinese banks are projected to increase by over 8% in 2024.

| Supplier Type | Key Power Driver | 2024 Impact |

|---|---|---|

| Funding Sources | Deposit Concentration, Liquidity | PBOC 7-day repo: 1.80% |

| Skilled Labor | Talent Scarcity | Increased wage demands |

| Regulatory Services | Mandatory Compliance | Costs up >8% for banks |

What is included in the product

This Porter's Five Forces analysis delves into the competitive landscape of the Bank of Gansu, examining the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the banking sector.

Understand competitive intensity with a visual breakdown of supplier power, buyer bargaining, threat of substitutes, new entrants, and existing rivalry, all in one place.

Easily identify and address key competitive pressures impacting the Bank of Gansu's profitability and market share.

Customers Bargaining Power

Customer Price Sensitivity

Customers of Bank of Gansu, both individual and corporate, can readily compare interest rates and service fees across various financial institutions, especially with digital banking platforms enhancing transparency. This heightened price sensitivity empowers them to demand competitive loan and deposit rates, directly impacting the bank's profitability. For instance, in 2024, the banking sector continues to see intense competition for deposits, with many customers actively seeking the best rates available. This pressure can narrow the bank's net interest margins, compelling it to innovate services beyond just pricing.

Low Switching Costs

For Bank of Gansu, the ease with which customers can switch providers significantly impacts their bargaining power. Many basic banking services, like deposit accounts and personal loans, are highly commoditized, meaning customers perceive little difference between offerings. In 2024, the widespread availability of digital account opening processes has further reduced the time and effort required to move funds or services. This low switching cost means customers can readily seek out competitors offering better interest rates or lower fees, as evidenced by general banking trends showing increased digital migration. Therefore, Bank of Gansu faces pressure to remain competitive on pricing and service quality to retain its customer base.

Access to Information

The rise of financial technology and widespread internet access has significantly empowered banking customers with more information. Customers can now easily compare Bank of Gansu’s loan rates or deposit yields against those offered by national giants like Industrial and Commercial Bank of China or regional competitors. This transparency, fueled by platforms showing real-time product comparisons, enhances their bargaining position, as seen with over 85% of Chinese adults using mobile payments as of early 2024, reflecting high digital engagement in financial services.

Large Corporate and Government Clients

Large corporate clients and government entities exert significant bargaining power over Bank of Gansu, primarily due to their substantial transaction volumes and deposit bases. These key clients frequently negotiate for more favorable loan rates, reduced service fees, and bespoke financial products tailored to their specific needs. Losing such large accounts could notably impact the bank's profitability and overall financial stability, underscoring the importance of retention strategies.

- Major corporate and government deposits represented a significant portion of Bank of Gansu's total deposits in 2024.

- These clients often secure loan interest rates below average market rates due to their negotiation leverage.

- Customized financial solutions are a common demand, requiring dedicated bank resources and specialized offerings.

- A single large corporate or government withdrawal can visibly affect the bank's liquidity ratios and earnings.

Availability of Alternative Banking Channels

The proliferation of online and mobile banking platforms significantly empowers customers against the Bank of Gansu. No longer geographically tied, customers benefit from a wide array of choices for financial activities offered by numerous competitors. This availability of alternatives, with China's mobile banking user base projected to exceed 1.1 billion in 2024, compels the Bank of Gansu to continuously enhance its service quality and digital offerings to retain its customer base.

- Digital banking penetration in China reached approximately 90% in 2024.

- Over 80% of banking transactions in China are now conducted through digital channels.

- Major banks in China invested billions in digital transformation during 2023-2024.

- Fintech platforms offer competitive services, capturing a significant market share.

Customer Power Reshapes Bank of Gansu's Profitability

Customers wield significant bargaining power over Bank of Gansu due to high price sensitivity and low switching costs, driven by easily accessible digital comparisons of rates and services. In 2024, the widespread adoption of mobile banking, exceeding 1.1 billion users in China, further amplifies customer choice and reduces loyalty. Large corporate and government clients also exert substantial influence, often negotiating preferential terms for their significant deposits and transaction volumes, directly impacting the bank's profitability.

| Customer Power Factor | 2024 Data Point | Impact on Bank of Gansu |

|---|---|---|

| Mobile Banking Users (China) | >1.1 Billion | Increased competition, lower loyalty |

| Digital Banking Penetration | ~90% | Demands superior digital services |

| Corporate Client Deposit Share | Significant % (Negotiated) | Pressure for bespoke terms & lower rates |

Preview Before You Purchase

Bank Of Gansu Porter's Five Forces Analysis

You're previewing the final version—precisely the same document that will be available to you instantly after buying. This comprehensive Porter's Five Forces analysis delves into the competitive landscape of the Bank of Gansu, evaluating the intensity of rivalry among existing competitors, the bargaining power of buyers, the threat of new entrants, the bargaining power of suppliers, and the threat of substitute products or services. Understanding these forces is crucial for strategic decision-making and identifying opportunities for competitive advantage. This detailed report provides actionable insights to navigate the complexities of the banking sector.

Rivalry Among Competitors

Large National and State-Owned Banks

Bank of Gansu faces intense competitive pressure from large, state-owned commercial banks like Bank of China and China Construction Bank. These national giants, with extensive branch networks and strong brand recognition, dominate the financial landscape, including Gansu province. For instance, as of early 2024, China Construction Bank reported total assets exceeding CNY 38 trillion, showcasing their immense financial power. Such major players command significant resources and often benefit from implicit government support, making them formidable rivals for regional banks. This competitive rivalry necessitates constant innovation and niche focus from Bank of Gansu to retain its market position.

Other Regional and City Commercial Banks

The Chinese banking market is highly fragmented, with numerous regional and city commercial banks directly competing with Bank of Gansu. These local institutions, numbering over 130 city commercial banks and around 2,500 rural commercial banks as of late 2023, possess deep understanding of local economies and strong relationships. This leads to intense competition for the same customer segments, especially small and medium-sized enterprises (SMEs) and individual depositors within Gansu province. Their localized approach often gives them an edge in securing local business.

Digital Transformation and Innovation

Competitive rivalry intensifies as digital capabilities become paramount for banks. Financial institutions are heavily investing in FinTech to enhance customer experiences, streamline operations, and roll out innovative products. Bank of Gansu must accelerate its digital transformation to match rivals in a market where mobile and online banking users exceeded 900 million in China by early 2024. Staying ahead is crucial as digital services drive customer acquisition and retention.

Focus on Green and Inclusive Finance

Competitive rivalry intensifies in specialized areas like green and inclusive finance, particularly for micro and small enterprises. Bank of Gansu's growth in green loans, reaching RMB 10.5 billion by year-end 2023 and projected to exceed RMB 12 billion in 2024, reflects a broader industry trend. This means the bank faces rivals actively pursuing these government-supported initiatives, increasing pressure.

- Green loans at Bank of Gansu reached RMB 10.5 billion by end-2023.

- Industry-wide, competition in green and inclusive finance is escalating significantly in 2024.

- Rivals are also heavily investing in these government-backed sectors.

Price and Non-Price Competition

Competition for Bank of Gansu involves both pricing strategies, like interest rates on loans and deposits, and non-price elements such as service quality, digital innovation, and brand reputation. The broader Chinese banking sector faces significant pressure on net interest margins, indicating fierce price competition. For instance, the average net interest margin for Chinese commercial banks continued its downward trend in early 2024, reflecting this intensity. Banks are also actively launching new financial products and enhancing digital services to attract and retain customers, moving beyond just rates.

- Chinese commercial banks' average Net Interest Margin (NIM) was approximately 1.74% by Q1 2024, down from 1.91% in 2023.

- Digital banking adoption in China reached 89% in 2024, highlighting the importance of non-price digital features.

- Loan Prime Rates (LPR) reductions in 2024 further intensify interest rate competition among banks.

- Banks are investing heavily in AI-driven customer service and personalized financial solutions.

Chinese Regional Bank: Digital Battle, Fierce Rivals, Slim Margins

Bank of Gansu faces intense competitive rivalry from dominant state-owned banks and a fragmented market of over 130 city commercial banks. Digitalization is a key battleground, with Chinese mobile banking users exceeding 900 million by early 2024, forcing rapid FinTech adoption. Competition also intensifies in niche segments like green finance, while industry-wide net interest margins fell to 1.74% by Q1 2024, underscoring severe pricing pressure.

| Competitive Factor | 2024 Market Data | Impact on Bank of Gansu |

|---|---|---|

| State-owned Banks' Assets | CCB assets > CNY 38T (early 2024) | Dominance requires niche focus. |

| Mobile Banking Users | >900M users (early 2024) | Accelerated digital transformation needed. |

| Net Interest Margin (NIM) | ~1.74% (Q1 2024) | Pressure on profitability and pricing. |

| Green Loans Growth | Bank of Gansu: RMB 12B (proj. 2024) | High competition in specialized areas. |

| Digital Banking Adoption | 89% (2024) | Essential for customer acquisition/retention. |

SSubstitutes Threaten

Fintech Companies and Digital Wallets

A significant substitute threat for Bank of Gansu stems from dominant fintech players like Ant Group's Alipay and Tencent's WeChat Pay. These platforms collectively hold over 90% of China's mobile payment market as of early 2024. They offer convenient solutions for daily payments and transfers, often bypassing traditional banking channels. The digital payments market in China is projected to reach a transaction value exceeding USD 4.5 trillion by 2025, highlighting the scale of this substitution. This shift reduces reliance on conventional bank accounts for many consumers and businesses.

Peer-to-Peer (P2P) Lending and Online Lenders

Online lending platforms, though facing increased regulatory scrutiny, continue to pose a significant substitute for traditional bank loans, particularly for small businesses and individual borrowers. These platforms often leverage advanced big data and AI for credit scoring, enabling notably faster loan approvals compared to conventional banks. In 2024, the global digital lending market continues its expansion, with online lenders offering rapid access to capital, appealing to those seeking efficiency and convenience. This digital shift compels traditional banks like Bank of Gansu to innovate their loan processes to remain competitive.

Wealth Management and Investment Platforms

Fintech platforms and specialized wealth management firms present a significant substitute threat to Bank Of Gansu's investment services. These digital-first providers offer access to diverse investment products, often with lower fees and more intuitive interfaces than traditional banks. For instance, global fintech investment in wealth tech reached approximately $12 billion in 2024, indicating robust platform growth. This shift attracts a growing share of retail investment funds, challenging conventional banking models.

Digital Currencies

The development of China's central bank digital currency, the e-CNY, presents a significant long-term substitute for Bank of Gansu's traditional payment systems. As of early 2024, e-CNY pilot programs expanded, with transactions reaching 1.8 trillion yuan by June 2024, indicating growing adoption. This shift could alter fund flows within the financial system, potentially reducing reliance on commercial banks like Bank of Gansu for payment settlement and even deposits. The People's Bank of China continues to broaden e-CNY usage scenarios, impacting the competitive landscape for regional banks.

- e-CNY transactions reached approximately 1.8 trillion yuan by June 2024.

- Pilot programs expanded to various provinces, including Gansu, increasing accessibility.

- Direct digital currency holdings could reduce demand for traditional bank deposits.

- Payment settlement bypasses commercial banks, impacting fee income.

Insurance and Trust Companies

Other financial institutions, like insurance and trust companies, present a notable threat as substitutes for some of Bank of Gansu's services. Certain insurance products now incorporate significant savings or investment components, directly competing with traditional bank deposits and wealth management offerings. Similarly, trust companies provide robust financing and asset management solutions, often rivaling corporate banking services and investment avenues. This diversification of non-bank financial institutions intensifies competition for customer funds and financial service provision.

- In 2024, the total assets under management by Chinese trust companies continue to grow, indicating their increasing capacity to compete for corporate and high-net-worth individual clients.

- China's insurance sector saw continued premium growth into 2024, with a focus on investment-linked products that directly attract savings.

- The competitive landscape is further intensified by the digital transformation of these substitute providers, enhancing accessibility and product diversification.

- Customers increasingly seek integrated financial solutions, blurring the lines between traditional banking, insurance, and trust services.

Digital Rivals Challenge Traditional Banking Dominance

Bank of Gansu faces significant substitute threats from dominant fintech platforms like Alipay and WeChat Pay, which control over 90% of China's mobile payment market as of early 2024. Online lending and wealth management platforms offer faster, more accessible alternatives for loans and investments, attracting significant capital. The e-CNY, with 1.8 trillion yuan in transactions by June 2024, could further diminish reliance on traditional bank payment systems and deposits. Additionally, insurance and trust companies increasingly compete for deposits and corporate financing.

| Substitute Type | Key Impact | 2024 Data Point |

|---|---|---|

| Fintech Payments | Bypass traditional channels | 90%+ China mobile payment share |

| E-CNY | Reduces reliance on bank deposits | 1.8 trillion yuan transactions (June 2024) |

| Wealth Tech | Alternative investment access | $12 billion global investment |

Entrants Threaten

High Capital Requirements

The banking industry requires significant capital, making it tough for new players to enter. New banks must meet stringent regulatory capital adequacy ratios, with the People's Bank of China and the National Financial Regulatory Administration (NFRA) setting strict benchmarks. For instance, commercial banks in China generally need a core Tier 1 capital adequacy ratio above 8.5% as of 2024. This high capital hurdle acts as a major barrier, effectively limiting the threat of new entrants for established institutions like Bank of Gansu.

Strict Regulatory and Licensing Hurdles

Entering the Chinese banking market presents significant hurdles due to strict regulatory and licensing requirements. Obtaining a banking license from authorities like the China Banking and Insurance Regulatory Commission (CBIRC), now part of the National Financial Regulatory Administration (NFRA) as of 2023, is a complex and lengthy process. The government maintains tight control over the financial sector to ensure stability, making it exceptionally difficult for new players, especially foreign entities, to gain entry. This robust oversight, characteristic of China's financial system in 2024, effectively limits competition and reinforces the position of established local banks like Bank of Gansu.

Established Brand Identity and Customer Trust

Established banks, including Bank of Gansu, benefit from deep-rooted brand recognition and customer loyalty built over decades. New entrants face substantial hurdles in replicating this trust, which is paramount in the financial sector. Building a credible reputation often necessitates significant marketing investments and a proven track record, a process that can take years. For instance, as of early 2024, customer acquisition costs in the banking industry remain high, reflecting the difficulty of dislodging incumbent relationships. This ingrained trust acts as a formidable barrier, protecting Bank of Gansu's market share against potential new competitors.

Access to Distribution Channels

New banks face a significant hurdle in establishing distribution channels, as incumbent institutions like Bank of Gansu boast extensive physical branch networks and sophisticated digital platforms. Building a comparable physical presence is prohibitively costly, with branch setup expenses in China potentially reaching millions of CNY per location. Digitally, new entrants must contend with established banks' robust online services and mobile banking apps, which saw over 90% penetration among urban Chinese users by early 2024. This makes customer acquisition challenging without massive investment in infrastructure or innovative digital solutions.

- Physical branch expansion costs are substantial, limiting new entrants' ability to match incumbents' reach.

- Incumbent banks have deeply entrenched digital ecosystems, including mobile apps and online banking platforms.

- Customer acquisition is difficult without significant investment in new, competitive distribution channels.

- Over 90% of urban Chinese users adopted mobile banking by early 2024, highlighting digital dominance.

Government Policy and Support for Local Banks

Chinese government policies often favor local and state-owned banks, like Bank of Gansu, to ensure financial stability and support regional economic development. This creates an uneven playing field, making it difficult for new, independent, or foreign-owned banks to compete effectively against incumbents that receive implicit or explicit government support. New bank licenses remain scarce, reflecting these high barriers to entry. For instance, the National Financial Regulatory Administration (NFRA) maintains tight control over new financial institution approvals.

- State-owned commercial banks held over 40% of total banking assets in China as of late 2023, highlighting their dominant position.

- Strict regulatory requirements mean only a handful of new banking licenses are granted annually, significantly limiting new entrants.

- Implicit government guarantees for established local banks deter potential competitors, who lack similar backing.

- Foreign bank assets in China were less than 2% of the total banking system by early 2024, indicating high market entry barriers.

Banking Entry: High Hurdles, Steep Costs

The banking sector's high capital requirements, like the 8.5% core Tier 1 capital ratio for Chinese commercial banks in 2024, significantly deter new players. Additionally, stringent regulatory hurdles and scarce new banking licenses make entry exceptionally difficult. Established banks benefit from deep customer loyalty and extensive distribution networks, including over 90% mobile banking penetration in urban China by early 2024, making customer acquisition costly for new market participants.

| Barrier to Entry | Key Metric (2024 Data) | Impact on New Entrants |

|---|---|---|

| Capital Requirements | Core Tier 1 Capital Ratio: 8.5% | High financial burden |

| Regulatory Hurdles | New Licenses Granted: Very few annually | Limited market access |

| Distribution & Brand | Mobile Banking Penetration: >90% (urban) | High customer acquisition costs |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Bank of Gansu is built upon comprehensive data from the bank's annual reports, official regulatory filings with the China Banking and Insurance Regulatory Commission (CBIRC), and industry-specific market research reports focusing on the Chinese banking sector.

We also incorporate macroeconomic data from reputable sources like the National Bureau of Statistics of China and financial market data from platforms such as Bloomberg and Wind Information to provide a robust understanding of the competitive landscape and external influences.