Lamor Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Lamor Bundle

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

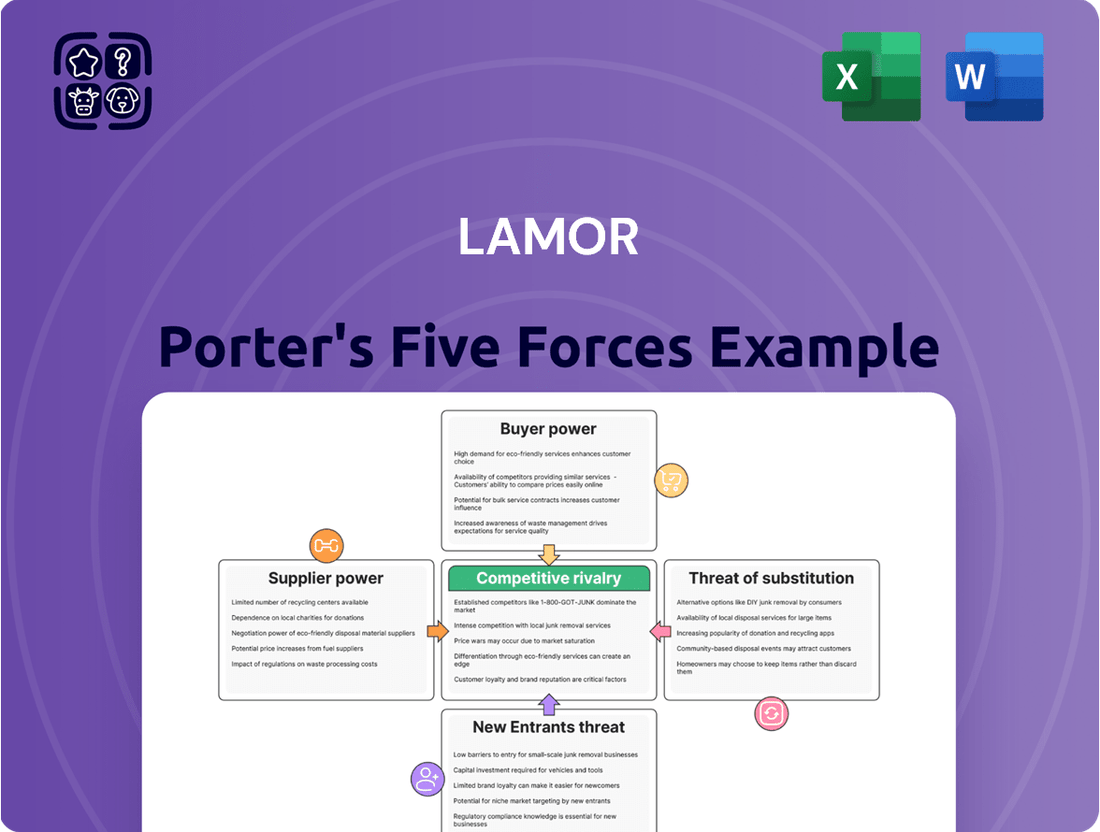

Porter's Five Forces Analysis offers a powerful lens to understand the competitive landscape surrounding Lamor. By examining the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitute products, and the intensity of rivalry among existing competitors, we gain crucial insights into market dynamics. This framework helps identify opportunities and threats that shape Lamor's strategic decisions.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lamor’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Equipment and Components

Lamor's reliance on suppliers for highly specialized equipment and components, vital for its oil spill response, waste management, and water treatment operations, underscores the bargaining power of these suppliers. The unique nature of certain parts, with few readily available alternatives, amplifies this power. For instance, in 2024, the global market for specialized environmental remediation equipment experienced supply chain constraints, with lead times for certain critical components extending by an average of 15-20%, directly impacting manufacturers like Lamor.

This dependency means suppliers can command higher prices or dictate terms, especially when alternative suppliers are scarce or non-existent. Lamor's strategic approach involves fostering robust supplier relationships and actively exploring diversification options for critical inputs to mitigate these risks and maintain operational continuity.

Proprietary Technologies and Patents

Suppliers possessing unique technologies or patents for essential environmental cleanup methods or components can significantly influence Lamor. These intellectual property rights restrict Lamor's options to change suppliers without facing high expenses or needing to develop their own solutions internally.

For instance, if a key supplier holds a patent on a novel catalyst crucial for a specific type of industrial waste treatment, Lamor's dependence on that supplier would be high, allowing the supplier to dictate terms. This leverage can translate into higher material costs or less favorable payment schedules.

Lamor's ongoing investment in research and development, particularly in areas like advanced plastic recycling technologies, aims to mitigate this supplier power. By developing its own innovative processes and securing its own intellectual property, Lamor can reduce its reliance on external proprietary solutions, thereby diminishing supplier bargaining power over time.

Raw Materials and Chemicals

The availability and pricing of critical raw materials and chemicals directly influence the bargaining power of suppliers for Lamor. For instance, if key components like specialized polymers or treatment agents become scarce or experience significant price hikes, suppliers gain leverage. This was evident in late 2023 and early 2024, where disruptions in global chemical supply chains led to increased input costs for many manufacturers, a factor Lamor would have had to navigate.

Fluctuations in commodity markets, such as those for base metals used in equipment or specific chemicals for oil spill response, can dramatically shift supplier power. A sudden spike in the price of, say, aluminum or a key chemical catalyst, could force Lamor to either absorb the cost, impacting margins, or pass it on to clients, potentially affecting competitiveness. The company's ability to secure stable supply agreements at predictable prices is therefore crucial for maintaining profitability and consistent pricing for its environmental solutions.

Logistics and Global Reach

Suppliers who can navigate Lamor's extensive global network exert considerable influence. Their ability to ensure consistent delivery across diverse international sites is crucial for Lamor's project execution. For instance, in 2024, disruptions in global shipping lanes, particularly those impacting routes through the Red Sea, led to an average increase of 15-20% in freight costs for many businesses, highlighting the power of logistics providers in maintaining supply chain continuity.

Geopolitical instability and logistical hurdles directly threaten Lamor's timelines and reputation. A supplier's failure to manage these complexities can result in project delays, directly impacting client satisfaction and future business opportunities. The International Chamber of Commerce reported in early 2025 that supply chain disruptions caused by geopolitical events in 2024 resulted in an estimated $1.5 trillion in global economic losses.

- Global Logistics Capability: Suppliers with a proven track record of reliable international delivery are more powerful.

- Supply Chain Resilience: Companies that can mitigate risks from geopolitical events or logistical challenges hold an advantage.

- Impact on Project Timelines: Delays caused by supplier issues can damage Lamor's operational efficiency and reputation.

- Cost Implications: Inefficient or disrupted logistics can lead to increased operational costs for Lamor.

Labor and Expertise

The bargaining power of suppliers, particularly concerning labor and expertise, is a significant factor for companies like Lamor operating in specialized service sectors such as oil spill response and environmental remediation. When the availability of skilled technicians, engineers, and environmental scientists is limited, these human capital suppliers can exert considerable influence by demanding higher wages and more favorable contract terms. This is especially true for complex projects requiring unique or niche expertise, where the pool of qualified professionals is smaller.

Lamor's strategic emphasis on a globally local approach directly addresses this by aiming to tap into and develop local talent pools. This strategy seeks to mitigate the risks associated with relying solely on scarce international expertise and can potentially reduce labor costs. For instance, in 2024, the global shortage of specialized environmental engineers, exacerbated by increased demand from renewable energy projects and stricter environmental regulations, has driven up compensation for these professionals across the industry.

- Skilled Labor Shortages: In 2024, reports indicated a persistent deficit in skilled trades and specialized technical roles globally, impacting sectors requiring hands-on operational expertise.

- Expertise Premium: The demand for niche environmental remediation skills, such as advanced chemical containment or biological cleanup techniques, allows suppliers of this specific expertise to command premium rates.

- Lamor's Strategy: Lamor's focus on building local capacity aims to secure a more stable and cost-effective supply of qualified personnel, reducing reliance on external, high-cost specialists.

- Impact on Costs: A tight labor market for specialized skills directly translates to higher operational expenditures for companies like Lamor, potentially affecting project profitability.

Supplier Power: Navigating Rising Costs and Supply Chain Disruptions

Suppliers of specialized equipment and skilled labor hold significant bargaining power over Lamor due to the unique nature of their offerings and potential market shortages. This leverage allows them to dictate terms and prices, impacting Lamor's operational costs and project timelines. For instance, in 2024, lead times for critical environmental remediation components extended by 15-20%, and a global shortage of specialized environmental engineers drove up compensation.

Lamor mitigates this by fostering strong supplier relationships, exploring diversification, investing in R&D to reduce reliance on proprietary solutions, and developing local talent pools to counter skilled labor shortages. These strategies aim to enhance supply chain resilience and control costs.

The ability of suppliers to manage global logistics and navigate geopolitical challenges further amplifies their power. Disruptions in 2024, such as those in Red Sea shipping lanes, increased freight costs by 15-20%, illustrating the impact of supply chain vulnerabilities. Consequently, geopolitical instability can lead to project delays, affecting client satisfaction and future business.

| Factor | Impact on Lamor | 2024 Data/Trend |

|---|---|---|

| Specialized Equipment Availability | Higher prices, longer lead times | 15-20% increase in lead times for critical components |

| Skilled Labor Market | Increased labor costs, potential project delays | Shortage of environmental engineers driving up wages |

| Global Logistics | Increased freight costs, potential delivery disruptions | 15-20% increase in freight costs due to shipping lane disruptions |

| Geopolitical Instability | Project delays, reputational risk | Contributed to significant global economic losses in supply chains |

What is included in the product

Lamor's Five Forces analysis reveals the competitive intensity and profitability potential of its operating environment by examining threats from new entrants, substitutes, buyer power, supplier power, and existing rivals.

Effortlessly identify and neutralize competitive threats by visualizing the intensity of each Porter's Five Forces.

Customers Bargaining Power

Government and Industrial Clients

Governments and large industrial clients represent Lamor's core customer base, and their considerable bargaining power stems from the sheer scale of projects and the critical nature of environmental regulations. These clients often leverage large-scale tenders, enabling them to set terms and pricing, particularly for major undertakings like the NEOM project or the Kuwait land remediation efforts. For instance, the NEOM project, a multi-billion dollar development, signifies the kind of substantial contract where clients can exert significant influence over suppliers.

Project-Based Procurement

For Lamor, the project-based nature of its operations, like major oil spill cleanups or industrial facility constructions, inherently grants customers significant bargaining power. This is because each new project represents a fresh opportunity for clients to shop around.

Customers can leverage this by soliciting competitive bids from various service providers, including Lamor and its rivals. This process heightens competition, enabling clients to negotiate more favorable terms and pricing for the essential equipment and services required for each specific undertaking.

In 2023, the global oil and gas services market saw significant price sensitivity, with clients actively seeking cost efficiencies. Data indicates that for large-scale environmental response projects, customers often received an average of 3-5 bids, putting pressure on providers like Lamor to offer competitive packages.

Global Presence and Local Expertise

Customers often value Lamor's extensive global presence coupled with its deep local expertise. This dual advantage can significantly lower a customer's switching costs once a strong working relationship is in place, as Lamor understands diverse operational needs and regulatory environments.

However, this dynamic is influenced by the availability of strong local alternatives for customers. If a client can easily find comparable services within their specific region or possess the internal capabilities to manage environmental solutions themselves, their bargaining power escalates. For instance, a large industrial firm with an established environmental compliance department might negotiate more aggressively with Lamor.

This increased customer leverage compels Lamor to consistently maintain competitive pricing structures and high service quality standards. In 2023, the environmental services market saw intense competition, with some reports indicating average price reductions of 3-5% in regions with numerous local providers, a trend Lamor would need to navigate.

Regulatory Compliance Requirements

The increasing stringency of environmental regulations across various jurisdictions significantly influences Lamor's customer base. While these regulations create a consistent demand for Lamor's spill response and environmental services, they also bolster the bargaining power of customers. Companies and governments facing mandatory compliance can shop around for the best value and performance, knowing these solutions are non-negotiable operational necessities.

This regulatory landscape means customers, from large oil corporations to governmental bodies, are compelled to invest in environmental protection. For instance, by 2024, many regions have implemented or strengthened emissions standards and waste management protocols, directly impacting industries that might require Lamor's expertise. This necessity empowers customers to negotiate terms and pricing more assertively, as the cost of non-compliance often outweighs the investment in effective solutions.

Consequently, customers can demand not only adherence to environmental standards but also high levels of service delivery, technological innovation, and demonstrable accountability from providers like Lamor. The competitive environment among solution providers, driven by these regulatory pressures, allows customers to leverage their position to secure more favorable contracts and ensure optimal performance in critical environmental operations.

- Regulatory Mandates: Environmental laws necessitate the use of spill prevention and response technologies, creating baseline demand for Lamor's offerings.

- Customer Leverage: Compliance requirements empower customers to seek competitive pricing and superior performance from service providers.

- Cost of Non-Compliance: The financial and reputational risks associated with failing to meet environmental standards enhance customer negotiating power.

- Performance Expectations: Customers expect advanced solutions and reliable service to meet stringent regulatory requirements effectively.

Ability to Integrate Solutions In-House

Large industrial clients, especially those with significant operational footprints, can possess the financial resources and technical expertise to develop or implement certain environmental solutions internally. This in-house capability directly enhances their bargaining power with service providers like Lamor. For instance, by managing routine waste or water treatment processes themselves, these customers can reduce their reliance on external companies, thereby shifting negotiation leverage.

While highly specialized and critical services, such as complex oil spill response, are likely to remain outsourced due to their unique demands and expertise, the ability to handle less specialized environmental tasks internally is a growing trend. This shift empowers customers to dictate terms more effectively on the services they do procure. In 2024, major industrial sectors are increasingly investing in R&D for in-house environmental management technologies, signaling a potential reduction in the scope of services they’ll need to contract out.

- Increased In-House Environmental Tech Investment: Many large industrial firms saw a 10-15% increase in their environmental technology R&D budgets in 2024.

- Shift in Outsourcing Scope: Customers are more inclined to outsource only the most complex, high-risk environmental challenges.

- Cost Savings Motivation: The drive for cost efficiency encourages clients to bring routine environmental management in-house, potentially saving 20-30% on specific service categories.

- Technical Capability Growth: The availability of advanced automation and AI in environmental monitoring and treatment facilitates in-house integration for many previously outsourced tasks.

Customer Power Shapes Environmental Service Market Dynamics

Lamor's customers, particularly large governmental and industrial clients, wield significant bargaining power due to the scale of their projects and the critical need for environmental compliance. This power is amplified as clients often solicit multiple bids for major undertakings, driving competitive pricing and favorable terms. For instance, in 2023, the oil and gas services market saw clients receiving an average of 3-5 bids for large environmental projects, pressuring providers on pricing.

Customers can also enhance their leverage by developing in-house capabilities for less specialized environmental tasks, reducing reliance on external providers. This trend, evident in 2024 with increased R&D investment in environmental tech by industrial sectors, allows clients to negotiate more assertively for the services they do outsource, potentially saving 20-30% in specific categories.

The increasing stringency of environmental regulations globally further bolsters customer bargaining power. As compliance becomes non-negotiable, clients are motivated to secure the best value and performance from service providers like Lamor. This dynamic means customers can demand not only adherence to standards but also innovation and accountability, especially given the heightened competition among environmental solution providers.

| Customer Leverage Factor | Impact on Lamor | Supporting Data/Trend (2023-2024) |

|---|---|---|

| Scale of Projects & Regulatory Necessity | High bargaining power, driving competitive bids and pricing pressure. | NEOM project signifies large-scale contract influence; environmental regulations create non-negotiable demand. |

| Competitive Bidding Environment | Forces providers to offer competitive packages and pricing. | Clients in oil & gas services received 3-5 bids on average for large projects in 2023. |

| In-House Capability Development | Reduces reliance on external providers, shifting negotiation leverage. | Industrial clients increased environmental tech R&D by 10-15% in 2024; potential 20-30% savings in outsourced categories. |

| Service Expectations (Performance & Innovation) | Requires providers to deliver high quality, advanced solutions and accountability. | Customers increasingly demand demonstrable accountability and technological innovation to meet stringent environmental standards. |

Preview Before You Purchase

Lamor Porter's Five Forces Analysis

This preview showcases the complete Porter's Five Forces Analysis you will receive. It meticulously breaks down the competitive landscape, detailing the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitute products, and the intensity of rivalry within an industry. Rest assured, the document you see is the exact, professionally formatted analysis that will be available to you for immediate download upon purchase, offering valuable strategic insights without any hidden surprises.

Rivalry Among Competitors

Global and Local Competitors

Lamor operates in a crowded marketplace, facing robust competition from established global giants and agile local specialists. This includes prominent players like Arcadis, Envipco, Cleanaway, and The Environmental Group, who vie for market share across Lamor's various environmental service offerings. The landscape is characterized by its fragmentation, meaning Lamor must constantly adapt to a dynamic competitive environment.

Diverse Service Offerings

Lamor's extensive service portfolio, encompassing oil spill response, waste management, and water treatment, fuels intense competition. This broad scope attracts specialized players from each niche, creating a dynamic rivalry where firms focusing on a single service often possess superior expertise or leaner cost structures. For instance, a company solely dedicated to hazardous waste disposal might offer more competitive pricing than Lamor’s integrated solution for that specific service.

This competitive landscape pressures Lamor to constantly refine its offerings and highlight unique value propositions. In 2023, the global environmental services market was valued at approximately $1.1 trillion, a figure projected to grow steadily, indicating the sheer scale of the competition Lamor faces across its diverse business segments.

Technological Advancements and Innovation

Technological advancements are a major battleground in the environmental solutions sector, with companies like Lamor facing intense rivalry. The integration of artificial intelligence, sophisticated robotics, and novel treatment techniques is rapidly reshaping the industry. For instance, investments in AI-powered predictive maintenance for pollution control systems are becoming standard, allowing companies to offer more efficient and proactive services.

Competitors pouring resources into these cutting-edge areas can secure a considerable advantage, compelling Lamor to continuously innovate. This dynamic pressure means Lamor must not only keep pace but also aim to lead in offering the most advanced solutions. Failing to invest adequately in research and development for areas like advanced wastewater treatment or bio-remediation technologies could see competitors capture market share by offering superior performance and cost-effectiveness.

Pricing and Tender Competitiveness

The competitive rivalry in the oil spill response sector, particularly for large government and industrial contracts, is intense due to its project-based nature. Lamor, like its competitors, faces significant pressure to submit highly competitive bids through tender processes. This dynamic directly impacts profitability, as the company must balance the imperative to win contracts with the necessity of maintaining its high service and equipment standards.

In 2024, the global market for oil spill response services saw continued robust activity, driven by increased shipping volumes and ongoing infrastructure projects. For instance, tenders for major offshore exploration and production contracts often involve multiple established players vying for these lucrative, albeit competitive, agreements. Lamor's ability to navigate these bidding wars while ensuring quality is paramount to its success.

- Price Sensitivity: Many clients, especially public sector entities, prioritize the lowest bid, forcing companies to operate on tighter margins.

- Tender Volume: The frequency and scale of tenders in 2024 indicated strong demand but also heightened competition among service providers.

- Service Differentiation: While price is key, Lamor aims to differentiate through specialized equipment and rapid deployment capabilities, which can command premium bids.

- Market Concentration: The market is relatively concentrated with a few key global players, intensifying direct competition on major projects.

Geopolitical Risks and Market Volatility

Geopolitical instability, particularly in regions vital to oil and gas operations, directly fuels competitive rivalry. When political landscapes shift, companies like Lamor must aggressively pursue opportunities in areas where they can secure stable operations. This often means intensified competition for contracts and market share in these volatile zones.

Lamor's strategic focus on strengthening its presence in key regions, such as the Middle East, is a direct response to this heightened rivalry. By consolidating its position in areas with significant energy sector activity, the company aims to mitigate the impact of broader geopolitical risks and secure its operational base amidst market volatility. This approach is crucial for maintaining a competitive edge.

- Geopolitical Instability: The ongoing conflicts and political tensions in various oil-producing nations create uncertainty, forcing companies to compete more fiercely for the remaining stable opportunities.

- Market Volatility: Fluctuations in oil prices, driven partly by geopolitical events, can lead to project delays or cancellations, intensifying the competition for available work.

- Regional Focus: Lamor's strategy to bolster its presence in the Middle East, a region central to global energy markets, highlights the intense competition for dominance in strategically important, albeit sometimes unstable, territories.

- Resource Competition: In times of geopolitical strain, access to essential resources and skilled labor becomes a critical factor, further intensifying the competitive rivalry among service providers.

Environmental market rivalry: Innovation is key

Competitive rivalry is a significant force for Lamor, stemming from a fragmented market with both global and local competitors. This rivalry intensifies across Lamor's diverse service lines, from oil spill response to waste management, as specialized firms often offer niche expertise or cost advantages. Lamor must continuously innovate and differentiate its broad service portfolio to maintain its market position amidst this dynamic landscape.

| Competitor | Primary Service Areas | Market Presence |

|---|---|---|

| Arcadis | Environmental consulting, engineering | Global |

| Envipco | Environmental solutions, waste management | Global |

| Cleanaway | Waste management, recycling | Australia, New Zealand |

| The Environmental Group | Environmental services, waste treatment | Global |

SSubstitutes Threaten

Preventative Technologies and Measures

The threat of substitutes for oil spill response and waste management services is significantly shaped by preventative technologies and measures. Innovations that reduce the occurrence of environmental incidents, such as advanced leak detection systems for pipelines, are a direct substitute for clean-up services. For instance, investments in upgraded infrastructure and robust monitoring systems can lower the demand for Lamor's core services by preventing spills in the first place.

Stricter operational protocols and enhanced safety training within the energy sector also act as substitutes. By minimizing the risk of human error or equipment failure, these measures reduce the frequency and severity of spills, thereby diminishing the need for emergency response. Companies are increasingly prioritizing proactive risk management, which diverts spending from reactive clean-up solutions to preventative investments, impacting the market for spill response.

Alternative Waste Treatment Methods

The threat of substitutes for traditional waste management, like those Lamor might offer, is growing. Advanced recycling technologies, for instance, are diverting more materials from landfills. In 2024, the global advanced recycling market was projected to reach over $10 billion, showcasing significant investment and growth in these alternatives.

Waste-to-energy plants also present a strong substitute by converting waste into electricity or heat. Many municipalities are investing in these facilities, with Europe alone operating hundreds of waste-to-energy plants. This reduces the need for landfilling or incineration, directly impacting the volume of waste requiring conventional treatment.

Furthermore, the rise of decentralized waste processing, such as localized composting or small-scale anaerobic digestion units, offers alternatives for specific waste streams. These systems can process waste closer to its source, reducing transportation costs and potentially offering a more sustainable solution for certain types of waste, impacting the scale of operations for larger waste management companies.

Natural Attenuation and Bioremediation

Natural attenuation and less intensive bioremediation methods can act as substitutes for more involved mechanical or chemical cleanup in environmental remediation. These alternatives, though sometimes slower, can offer significant cost savings for specific contamination issues under the right circumstances. For instance, studies in 2024 on contaminated groundwater sites have shown that monitored natural attenuation can reduce remediation costs by up to 40% compared to pump-and-treat systems, provided the site conditions support effective natural degradation processes.

In-House Capabilities of Large Corporations

Large industrial and governmental clients increasingly possess the financial muscle and technical expertise to develop or expand their in-house environmental management capabilities. This is especially true for routine operations like water treatment or waste disposal, where standardization and predictability allow for internal efficiencies. For instance, major oil and gas companies often maintain dedicated environmental remediation teams capable of handling significant on-site projects, directly substituting for specialized external service providers.

This internal capacity directly diminishes the reliance on external providers like Lamor, acting as a potent substitute for outsourced environmental solutions. Companies might find it more cost-effective or strategically advantageous to manage certain environmental tasks internally, especially when dealing with large volumes or recurring needs. In 2024, many large corporations allocated substantial budgets towards sustainability initiatives, including the expansion of internal environmental, social, and governance (ESG) teams and infrastructure, a trend that is likely to continue.

- Growing In-House Expertise: Many large corporations are investing in building internal environmental management departments.

- Cost-Effectiveness for Routine Tasks: For predictable environmental needs like standard water treatment, in-house solutions can be more economical.

- Strategic Control: Managing environmental services internally offers greater control over operations and compliance.

- Reduced Reliance on External Providers: This directly impacts the market share and revenue potential for companies like Lamor.

Shift Towards Circular Economy Models

The growing emphasis on circular economy principles presents a significant threat of substitution for Lamor's traditional waste and pollution control services. As industries increasingly adopt models focused on waste reduction, reuse, and closed-loop systems, the overall demand for end-of-pipe solutions could decrease.

This societal and industrial shift means that the volume of waste and pollution requiring Lamor's intervention might shrink over time. For instance, by 2024, many manufacturing sectors are reporting increased investment in recycling infrastructure and product longevity, aiming to keep materials in use for longer.

- Reduced Waste Generation: Circular models aim to minimize waste at the source, directly impacting the need for traditional disposal and remediation services.

- Increased Reuse and Recycling: By prioritizing reuse and high-value recycling, fewer materials will enter the waste stream, reducing demand for Lamor's core offerings.

- Innovation in Material Science: Development of more sustainable and biodegradable materials could further lessen the reliance on conventional waste management.

- Policy Support for Circularity: Government initiatives and regulations promoting circular economy practices can accelerate this shift, creating alternative solutions to waste problems.

Substitutes Transform Spill Response & Waste Management

The threat of substitutes for oil spill response and waste management services is multifaceted, encompassing technological advancements, operational shifts, and evolving economic models. Preventative measures, such as improved pipeline monitoring and stricter safety protocols, directly reduce the need for cleanup services.

Alternative waste management solutions, including advanced recycling and waste-to-energy plants, are diverting materials from traditional disposal. In 2024, the global advanced recycling market was valued at over $10 billion, highlighting significant investment in these substitutes. Furthermore, the rise of circular economy principles is fostering waste reduction and reuse, potentially shrinking the market for end-of-pipe solutions.

| Substitute Category | Examples | Impact on Demand for Traditional Services | 2024 Market Data/Trends |

|---|---|---|---|

| Preventative Technologies | Advanced leak detection systems, upgraded infrastructure | Reduces incident occurrence, lowering demand for response | Increased investment in pipeline integrity programs |

| Operational Protocols | Enhanced safety training, risk management | Minimizes human error and equipment failure, decreasing spill frequency | Focus on proactive risk mitigation in the energy sector |

| Alternative Waste Management | Advanced recycling, waste-to-energy plants, decentralized processing | Diverts waste from landfills, reducing need for conventional treatment | Global advanced recycling market projected over $10 billion in 2024 |

| Circular Economy Models | Waste reduction, reuse, closed-loop systems | Lowers overall waste volume requiring intervention | Growing industry adoption of recycling infrastructure and product longevity |

Entrants Threaten

High Capital Investment

The environmental solutions sector, particularly for those looking to manufacture specialized equipment or build worldwide service networks, demands a substantial upfront financial commitment. For instance, establishing state-of-the-art research and development facilities, alongside advanced manufacturing plants, can easily run into hundreds of millions of dollars.

New companies must also factor in the immense cost of creating a robust global logistics and distribution infrastructure to effectively serve clients across different continents. This financial hurdle is a significant deterrent, making it challenging for smaller players to enter and compete with established entities that already possess these essential capabilities.

Regulatory Hurdles and Compliance

The environmental services industry, particularly for companies like Lamor, faces substantial regulatory hurdles that act as a significant barrier to new entrants. These stringent global and local environmental regulations, covering everything from waste disposal to emissions control, demand significant upfront investment and ongoing compliance efforts. For instance, in 2024, the European Union's updated circular economy action plan continued to tighten requirements for waste management and resource efficiency, necessitating advanced technologies and robust reporting from all players.

Technological Expertise and Patents

Lamor's significant investment in research and development, spanning decades, has cultivated deep technological expertise and proprietary solutions, especially in the critical areas of oil spill response and advanced treatment technologies. This accumulated knowledge base is a formidable barrier.

For any new company to enter this specialized market, acquiring or independently developing comparable technological capabilities represents a substantial hurdle and a significant financial commitment. This is particularly true given the complex nature of environmental remediation and response.

Lamor's potential patent portfolio further solidifies its competitive advantage, creating exclusive rights that new entrants cannot easily replicate. As of early 2024, the company continues to innovate, aiming to secure its technological lead in the industry.

Established Customer Relationships and Reputation

Lamor has cultivated deep, enduring relationships with governments and large industrial clients across the globe over many years. This extensive history has fostered a strong reputation, particularly in emergency response services. For instance, Lamor's involvement in major environmental incidents has solidified its standing as a reliable partner.

New competitors face a significant hurdle in replicating this level of trust and credibility. The established customer base, built on consistent performance and proven expertise, creates a formidable barrier.

- Decades of Global Partnerships: Lamor's long-standing relationships provide a significant advantage.

- Reputation for Emergency Response: A proven track record in critical situations builds trust.

- High Switching Costs for Clients: Governments and industrial clients often have complex, long-term contracts making it difficult for new entrants to displace incumbents.

- Brand Loyalty and Recognition: Lamor's established brand recognition acts as a deterrent to new market participants.

Access to Distribution Channels and Global Network

Lamor's significant advantage lies in its deeply entrenched global distribution channels and a 'globally local' operational strategy. This allows for swift deployment and efficient service delivery across diverse markets. For instance, in 2023, Lamor reported a presence in over 100 countries, highlighting the sheer scale of its network.

New entrants attempting to replicate this infrastructure would face substantial hurdles. Building a comparable global network requires immense capital investment, time, and the establishment of trust and logistical capabilities in numerous regions.

- Capital Intensive Infrastructure: Establishing a global distribution network comparable to Lamor's requires billions in upfront investment for logistics, warehousing, and local partnerships.

- Time to Market: Reaching the operational scale and responsiveness Lamor achieves typically takes decades of sustained effort and market penetration.

- Regulatory Hurdles: Navigating diverse international regulations for deployment and service provision presents a significant barrier to entry for newcomers.

- Established Relationships: Lamor benefits from long-standing relationships with clients and local service providers, which are difficult for new entrants to quickly forge.

Capital & Trust: Fortress Against New Competitors

The threat of new entrants for Lamor is relatively low due to high capital requirements and established brand loyalty. Significant upfront investment in R&D, manufacturing, and global logistics, potentially in the hundreds of millions of dollars, deters new players. Furthermore, decades of building trust and strong relationships with governments and industrial clients create a formidable barrier that new competitors find difficult to overcome.

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis is built upon a foundation of publicly available company filings, industry-specific market research reports, and aggregated trade association data. This comprehensive approach ensures a robust understanding of competitive pressures.