HubSpot Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

HubSpot

Don't Miss the Bigger Picture

HubSpot operates in a dynamic SaaS landscape, facing intense rivalry and significant buyer power. Understanding these forces is crucial for any business in this sector.

The complete report reveals the real forces shaping HubSpot’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Limited Supplier Concentration

HubSpot's limited reliance on a concentrated supplier base for its software development tools and services significantly curtails supplier bargaining power. This diversification means that if one supplier were to increase prices or face disruptions, HubSpot has readily available alternatives, reducing its dependence and vulnerability. For instance, the cloud computing market, a key input for many SaaS companies, is highly competitive with major players like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, offering HubSpot considerable negotiating leverage.

Low Switching Costs for HubSpot

HubSpot benefits from relatively low switching costs across its supplier base. This means that if a supplier tries to dictate unfavorable terms or prices, HubSpot can readily shift to another provider without significant disruption or expense. This ease of transition effectively limits the leverage suppliers can wield.

Minimal Threat of Forward Integration

Suppliers to HubSpot, such as those offering cloud infrastructure or specialized software components, generally face a minimal threat of forward integration. The CRM software market demands significant investment in research and development, marketing, and sales, resources most suppliers lack.

For instance, a cloud provider would need to develop a completely new product suite, build a customer base from scratch, and navigate the complex sales cycles typical of enterprise software, a daunting prospect compared to their core business. This lack of capability significantly reduces their leverage over HubSpot.

HubSpot's Importance to Suppliers

HubSpot's position as a customer for its suppliers is varied. While it represents a significant portion of revenue for some niche providers, for the broader market of potential suppliers, HubSpot is generally not a dominant or critical client. This dynamic lessens the suppliers' reliance on HubSpot, reducing their incentive to offer exceptionally favorable terms or to risk jeopardizing the relationship by imposing unfavorable conditions. Suppliers often have diversified customer bases, making them less susceptible to HubSpot's demands.

This situation means suppliers are less likely to wield significant bargaining power over HubSpot. They can afford to maintain standard pricing and terms, as losing HubSpot as a customer, while undesirable, would not cripple their operations. In 2023, HubSpot reported total revenue of $2.20 billion, indicating a substantial but not monopolistic spend across its supply chain. This scale provides some leverage to HubSpot, but the supplier landscape remains competitive.

- Supplier Dependence: For most suppliers, HubSpot is one of many clients, not a make-or-break revenue source.

- Market Diversification: Suppliers typically serve a wider market, reducing their vulnerability to any single customer.

- Risk Mitigation: Suppliers are less inclined to push for aggressive terms that could alienate a significant player like HubSpot.

- Competitive Landscape: The availability of alternative suppliers for many of HubSpot's needs further dilutes individual supplier bargaining power.

Availability of Substitute Inputs

The availability of substitute inputs significantly dilutes supplier bargaining power for companies like HubSpot. For instance, HubSpot relies on cloud infrastructure, and in 2024, the market for these services is highly competitive, with major players like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud offering comparable solutions. This competition means HubSpot can switch providers if one supplier attempts to dictate unfavorable terms.

Furthermore, the software components essential for HubSpot's platform, such as data analytics tools or customer relationship management (CRM) integrations, also have numerous alternatives. In 2024, the SaaS landscape is characterized by a vast array of specialized software providers. This broad selection prevents any single software supplier from wielding excessive influence over HubSpot's operational costs or product development roadmap.

- Cloud Infrastructure Competition: In 2024, the global cloud computing market, valued at over $600 billion, features intense competition among AWS, Azure, and Google Cloud, offering HubSpot flexibility and negotiation leverage.

- Diverse SaaS Ecosystem: The availability of countless SaaS solutions for functions like marketing automation, customer support, and data analysis in 2024 means HubSpot is not dependent on any single vendor.

- Reduced Vendor Lock-in: The ease with which HubSpot can integrate alternative software components in 2024 minimizes the risk of supplier lock-in, further strengthening its negotiating position.

HubSpot's Strong Supplier Bargaining Power

HubSpot's bargaining power with its suppliers is generally strong due to a diverse and competitive supplier market. The company's ability to switch providers for key inputs like cloud computing services, with major players such as AWS, Azure, and Google Cloud offering comparable solutions in 2024, significantly limits any single supplier's leverage. This competitive landscape, coupled with relatively low switching costs for many of HubSpot's required software components, ensures HubSpot can negotiate favorable terms and avoid supplier-imposed price hikes.

| Input Category | Key Suppliers (Examples) | HubSpot's Leverage Factor | 2024 Market Context |

|---|---|---|---|

| Cloud Infrastructure | AWS, Microsoft Azure, Google Cloud | High (due to intense competition and low switching costs) | Global cloud market exceeding $600 billion, highly competitive |

| SaaS Components (e.g., analytics, integrations) | Numerous specialized SaaS providers | High (due to wide availability of alternatives) | Vast SaaS ecosystem with many interchangeable solutions |

| Software Development Tools | Various software vendors | Moderate to High (depends on specificity of tool) | Broad market with many open-source and commercial options |

What is included in the product

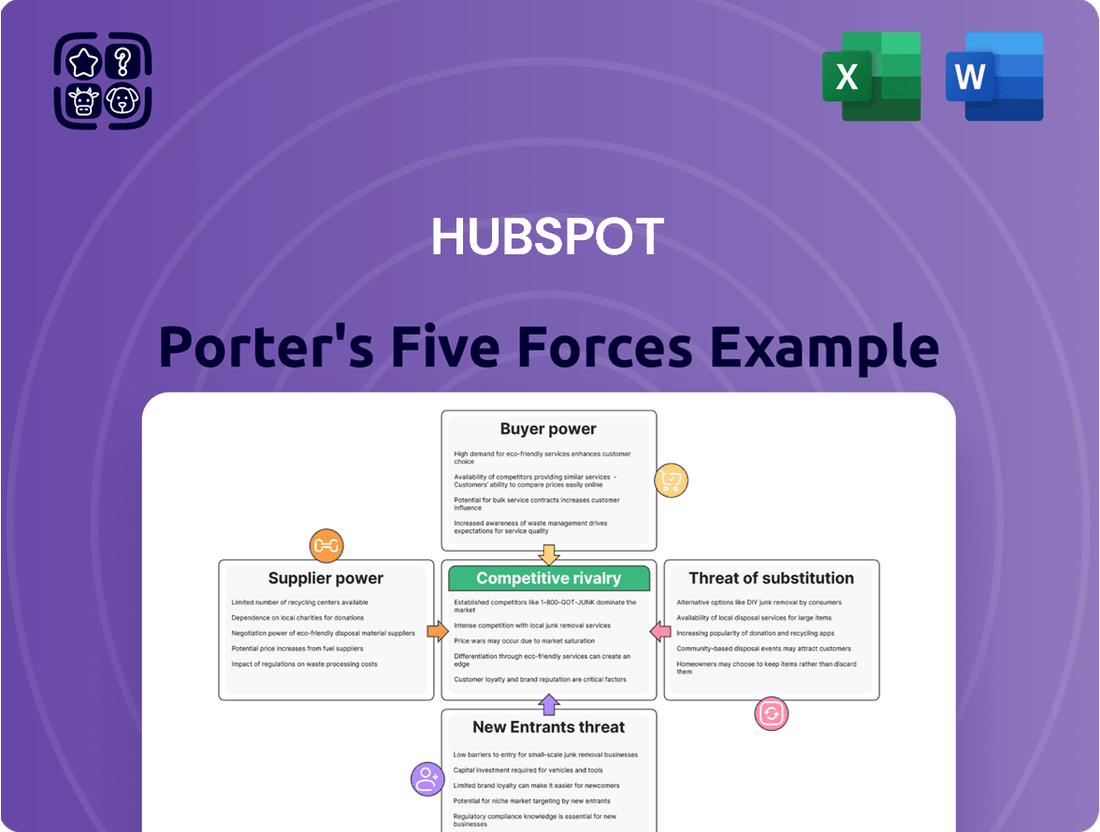

HubSpot's Porter's Five Forces analysis breaks down the competitive landscape for its CRM and marketing software, examining threats from new entrants, the bargaining power of buyers and suppliers, and the intensity of rivalry among existing players.

Instantly identify and address competitive threats with a visual breakdown of industry power dynamics, simplifying complex market analysis.

Customers Bargaining Power

Price Sensitivity of SMB Customers

HubSpot's primary customer base, small and medium-sized businesses (SMBs), often operates with tighter budgets. This inherent price sensitivity means they actively seek out the most cost-effective solutions available for their marketing, sales, and service needs. In 2024, many SMBs reported that software costs were a significant consideration, with a substantial portion actively comparing pricing across multiple vendors before making a purchase decision.

Relatively Low Switching Costs

While switching CRM systems can indeed require some effort, the actual costs for customers, especially those on simpler HubSpot plans, are relatively low when compared to the wider software industry. This makes it easier for them to explore and adopt competing platforms if they find better deals or more suitable features. For instance, HubSpot reported a slight dip in average subscription revenue per customer in Q1 2025, suggesting some customers were indeed exploring alternatives.

High Customer Information Availability

Customers in the CRM software market, including those considering HubSpot, are incredibly well-informed today. They have access to vast amounts of information regarding competing products, their pricing, and the features they offer. This ease of access to data significantly amplifies their bargaining power.

Online reviews, dedicated comparison websites, and readily available free trials empower customers to make thoroughly educated purchasing decisions. For instance, a 2024 report indicated that over 85% of B2B software buyers conduct extensive online research before making a purchase. This forces companies like HubSpot to constantly prove their superior value proposition to attract and retain customers.

Unlikely Backward Integration by Customers

The threat of customers backward integrating by developing their own Customer Relationship Management (CRM) or marketing automation software is exceptionally low for companies like HubSpot. This is primarily due to the substantial financial outlay, the need for highly specialized technical talent, and the continuous, resource-intensive maintenance that such in-house development demands.

These high barriers effectively deter most customers from attempting to build their own solutions. Consequently, they remain reliant on external providers. For instance, the global CRM market was valued at approximately $63.9 billion in 2023 and is projected to reach $128.2 billion by 2028, indicating a strong and sustained demand for specialized software from third parties.

- High Development Costs: Building a robust CRM from scratch can cost hundreds of thousands, if not millions, of dollars, making it prohibitive for most businesses.

- Specialized Expertise Required: Companies need skilled software engineers, UI/UX designers, data scientists, and cybersecurity experts, which are often scarce and expensive.

- Ongoing Maintenance & Updates: Software requires constant updates for security patches, new features, and compatibility with evolving technologies, adding significant long-term operational costs.

- Focus on Core Competencies: Most businesses prefer to concentrate their resources and efforts on their primary operations rather than diverting them to complex software development.

Customer Base Growth vs. ARPC Decline

HubSpot's customer base has expanded significantly, reaching over 258,000 customers by the first quarter of 2025, marking a robust 19% year-over-year growth. This expansion highlights the company's ability to attract new users to its platform.

However, this growth is juxtaposed with a 4% decline in average subscription revenue per customer (ARPC) during the same period. This trend suggests that customers may be exercising their bargaining power by selecting more basic subscription tiers or actively seeking ways to reduce their overall spending on HubSpot's services.

- Customer Growth: HubSpot's customer count reached over 258,000 by Q1 2025, a 19% increase year-over-year.

- ARPC Trend: Average subscription revenue per customer (ARPC) saw a 4% decrease in the same timeframe.

- Customer Power Indication: The ARPC decline suggests customers are leveraging their power by opting for lower-priced plans or demanding cost efficiencies.

Bargaining power: Customers reshape value and pricing.

Customers of CRM software, including HubSpot's, possess considerable bargaining power due to the availability of information and relatively low switching costs. This allows them to readily compare offerings and negotiate better terms or opt for more affordable alternatives. The increasing sophistication of buyers, with over 85% conducting extensive research in 2024, further solidifies this power.

While backward integration by customers is unlikely due to high development costs and specialized talent needs, the ability to switch providers or negotiate lower prices remains a significant factor. HubSpot's customer growth to over 258,000 by Q1 2025 is impressive, yet a 4% decrease in average revenue per customer (ARPC) in the same period indicates customers are actively managing their spend, perhaps by choosing less comprehensive plans.

| Metric | Value (Q1 2025) | Trend Implication |

|---|---|---|

| Customer Count | > 258,000 | Market adoption and reach |

| Year-over-Year Customer Growth | 19% | Attracting new users |

| Average Revenue Per Customer (ARPC) | Decreased 4% | Customers exercising price sensitivity or seeking cost efficiencies |

Preview the Actual Deliverable

HubSpot Porter's Five Forces Analysis

This preview showcases the complete, professionally crafted HubSpot Porter's Five Forces Analysis, offering a deep dive into the competitive landscape of the inbound marketing software industry. The document you see here is precisely what you will receive immediately after purchase, ensuring full transparency and immediate utility.

You're looking at the actual, fully formatted analysis. Once your purchase is complete, you'll gain instant access to this exact document, empowering you with actionable insights into HubSpot's competitive environment without any delay or further modification needed.

Rivalry Among Competitors

Intense and Diverse Competitive Landscape

The CRM and marketing automation software market is incredibly crowded, with a vast number of companies vying for market share. This intense rivalry means businesses have many choices when selecting solutions.

HubSpot faces formidable competition from giants like Salesforce, which held approximately 23.5% of the CRM market share in 2023, and Microsoft Dynamics 365. It also goes head-to-head with specialized marketing automation players such as Marketo and ActiveCampaign, alongside more affordable options like Zoho CRM.

High Market Growth Attracts Competitors

The integrated marketing and sales solution market is experiencing robust expansion, with projections indicating a 19.2% compound annual growth rate (CAGR) and an anticipated market size of $27.3 billion by 2026. This significant growth acts as a powerful magnet, drawing in both established companies looking to broaden their reach and new businesses eager to capture a share of this burgeoning sector. Consequently, the competitive landscape is becoming increasingly dynamic and intense.

Increasing Product Standardization and AI Integration

The CRM and marketing automation landscape is seeing increased product standardization, especially with competitors heavily integrating AI. This makes it harder for companies like HubSpot to stand out solely on features, shifting the battleground to pricing, user experience, and specialized offerings.

For instance, by mid-2024, many CRM providers, including Salesforce and Zoho, have rolled out advanced AI assistants for tasks like lead scoring and customer service, mirroring HubSpot’s own AI investments. This widespread AI adoption means that a unique feature set is less of a differentiator than it once was.

This standardization pressures companies to innovate in areas beyond core functionality. HubSpot’s strategy to counter this involves significant investment in its AI platform, aiming to offer superior predictive analytics and personalized customer journeys, thereby creating new points of differentiation.

Brand Loyalty and Ecosystem Stickiness

HubSpot has built substantial brand loyalty, especially among inbound marketing professionals. Its comprehensive suite of tools, from CRM to marketing automation, means businesses often deeply integrate HubSpot into their daily operations. This integration, a key aspect of its ecosystem, creates significant switching costs. For instance, migrating extensive customer data and established workflows to a competitor can be a complex and costly undertaking.

This ecosystem stickiness directly dampens competitive rivalry. When customers are deeply embedded, the effort and expense required to switch to a rival platform become a major deterrent. This allows HubSpot to maintain a stronger market position, even when facing competitive pricing or feature advancements from other players in the CRM and marketing automation space.

- Brand Loyalty: HubSpot is a recognized leader in the inbound marketing methodology, fostering strong customer allegiance.

- Ecosystem Stickiness: The integrated nature of HubSpot's platform, encompassing CRM, marketing, sales, and service hubs, creates high switching costs for businesses.

- Reduced Rivalry Impact: This stickiness makes it challenging for competitors to lure away established HubSpot customers, thereby mitigating direct competitive pressures.

Strategic Acquisitions and Market Positioning

Major tech players, including Google, have previously expressed interest in acquiring HubSpot. This interest underscores the significant strategic value and competitive positioning of platforms like HubSpot in the unified business solutions market. While the potential Google acquisition did not materialize, these overtures highlight the intense competition and ongoing efforts by large technology companies to consolidate their offerings and capture market share.

These acquisition attempts reflect a broader trend of market consolidation, where established giants seek to integrate best-in-class software solutions to provide comprehensive customer relationship management and marketing automation tools. For instance, Salesforce's acquisition of Slack for $27.7 billion in 2021 demonstrates a similar drive to create integrated ecosystems. Such moves by competitors directly influence the competitive rivalry within the CRM and marketing automation sectors.

- Strategic Importance: Google's past interest in HubSpot signals the platform's high value in the competitive landscape of business solutions.

- Market Dynamics: Failed acquisition talks, like the one with Google, reveal the fluid and dynamic nature of market positioning in the tech industry.

- Competitive Jockeying: Major tech firms constantly vie for dominance by seeking to acquire or partner with key players to offer integrated business solutions.

CRM Market: Intense Rivalry, AI Integration, and Strategic Positioning

The CRM and marketing automation market is intensely competitive, with numerous players offering similar solutions. This high level of rivalry means businesses have abundant choices, often leading to price sensitivity and a focus on user experience and specialized features to differentiate. The market's rapid growth, projected to reach $27.3 billion by 2026 with a 19.2% CAGR, further fuels this competition as new entrants and established firms alike seek to capture market share.

HubSpot faces significant competition from established giants like Salesforce, which commanded roughly 23.5% of the CRM market in 2023, and Microsoft Dynamics 365. The landscape also includes specialized providers such as Marketo and ActiveCampaign, alongside more budget-friendly options like Zoho CRM. This broad competitive set necessitates continuous innovation and strategic positioning.

The increasing integration of AI across CRM platforms, with many competitors like Salesforce and Zoho rolling out similar AI assistants by mid-2024, has led to greater product standardization. This trend shifts the competitive advantage from unique features to factors like pricing, user experience, and the depth of a company's ecosystem. HubSpot's strong brand loyalty and high switching costs, stemming from its integrated platform and the complexity of data migration, serve as key defenses against this intense rivalry.

| Competitor | Approximate CRM Market Share (2023) | Key Offerings |

|---|---|---|

| Salesforce | 23.5% | Comprehensive CRM, Sales Cloud, Marketing Cloud |

| Microsoft Dynamics 365 | N/A (integrated suite) | CRM, ERP, business intelligence |

| Zoho CRM | N/A (part of Zoho suite) | Integrated suite of business applications |

| Marketo (Adobe) | N/A (specialized marketing automation) | Marketing automation, lead management |

| ActiveCampaign | N/A (specialized marketing automation) | Email marketing, marketing automation, CRM |

SSubstitutes Threaten

Availability of Specialized Point Solutions

The availability of specialized point solutions presents a significant threat to all-in-one platforms like HubSpot. Companies can choose from a vast array of single-function software for tasks such as email marketing, SEO, or social media management.

While HubSpot provides integration benefits, some businesses prioritize best-of-breed tools that offer deeper, more tailored functionality in a specific area. This can sometimes come with a lower initial investment. For instance, a company heavily reliant on advanced email automation might find a dedicated email marketing platform more cost-effective and feature-rich than relying solely on HubSpot's built-in capabilities.

Open-Source CRM and Marketing Tools

The rise of open-source CRM and marketing automation tools poses a significant threat of substitutes, especially for businesses prioritizing cost savings or needing highly tailored solutions. These alternatives, while often demanding greater technical skill for setup and upkeep, offer a compelling alternative to established proprietary systems.

Traditional and Manual Business Processes

For very small businesses or startups, traditional manual methods for managing customer relationships and marketing activities, such as spreadsheets, basic email clients, and manual sales tracking, represent a significant substitute. These methods are often perceived as low-cost alternatives, particularly when budget constraints are a primary concern.

While inherently less efficient than integrated software solutions, these manual approaches serve as a functional baseline for businesses not yet ready or able to invest in comprehensive platforms. For instance, a startup might initially rely on Google Sheets for lead tracking and Mailchimp for basic email campaigns, delaying adoption of a CRM like HubSpot until their growth necessitates it.

The availability of these manual substitutes can limit the perceived value of more advanced solutions, especially if the cost-benefit analysis doesn't clearly favor the latter in the early stages. This threat is particularly relevant in 2024 as many new businesses continue to launch with lean operational models.

Custom-Built Internal Solutions

Larger enterprises with substantial IT departments and budgets might opt to develop custom-built internal solutions. This approach offers unparalleled alignment with specific business processes, effectively acting as a substitute for off-the-shelf software like HubSpot.

While the initial development and ongoing maintenance costs can be significant, these custom solutions provide complete control and avoid vendor lock-in. For instance, a global financial institution might invest millions in building proprietary CRM and marketing automation systems, diverting potential spend from SaaS providers.

The threat here is that these bespoke systems, while costly, can offer a superior, integrated experience for large organizations. Consider that in 2024, global IT spending on custom software development was projected to reach hundreds of billions of dollars, indicating a significant market for such alternatives.

- Custom solutions offer tailored functionality, eliminating the need for workarounds often associated with SaaS platforms.

- The avoidance of vendor lock-in provides long-term strategic flexibility and cost control.

- Significant upfront investment and ongoing maintenance are key considerations for businesses evaluating this substitute.

- Large enterprises with dedicated IT resources are the primary segment considering and implementing these internal builds.

Impact of AI on DIY Capabilities

The rise of accessible AI tools presents a significant threat of substitutes for integrated marketing and sales platforms. Basic marketing tasks, from content generation to lead qualification, can now be partially automated by a growing array of standalone AI applications. For example, AI-powered writing assistants can produce blog posts or social media updates, diminishing the exclusive value proposition of a platform's content creation suite.

This trend is particularly concerning as AI capabilities become more sophisticated and user-friendly. Many small to medium-sized businesses might opt for a patchwork of specialized AI tools rather than a comprehensive, all-in-one solution. By 2024, the market for AI in marketing was projected to reach substantial figures, indicating a growing adoption of these alternative solutions.

- AI-powered content creation tools can replicate some functionalities of a marketing platform's content hub.

- Generic AI platforms offer basic automation for marketing and sales, reducing reliance on integrated systems.

- The increasing accessibility and affordability of AI tools empower users to perform tasks previously requiring specialized software.

- Businesses may choose to assemble a suite of AI tools instead of investing in a single, comprehensive platform.

Beyond All-in-One: The Rise of Marketing Platform Substitutes in 2024

The threat of substitutes for platforms like HubSpot comes from various sources, including specialized point solutions, open-source alternatives, manual processes, custom-built enterprise systems, and increasingly, accessible AI tools. These substitutes often appeal to specific business needs, cost sensitivities, or desires for greater control and customization.

In 2024, the market for marketing automation software, which includes platforms like HubSpot and their substitutes, was projected to continue its robust growth, with some estimates placing it in the tens of billions of dollars globally. This indicates a significant demand for solutions, but also highlights the competitive landscape where substitutes can capture market share by offering specialized value propositions.

For instance, the proliferation of AI writing assistants in 2024, with many offering free or low-cost tiers, directly competes with the content creation features of comprehensive platforms. Similarly, the ongoing development in the open-source CRM space provides viable, cost-effective alternatives for businesses prioritizing flexibility and avoiding vendor lock-in, a trend that gained further momentum throughout 2024.

| Substitute Category | Key Appeal | Example Scenario | 2024 Market Context |

|---|---|---|---|

| Specialized Point Solutions | Deeper functionality, best-of-breed | A company using a dedicated email marketing tool for advanced segmentation. | Continued growth in niche SaaS markets. |

| Open-Source Alternatives | Cost savings, customization | A startup leveraging an open-source CRM for a highly tailored sales process. | Increasing developer communities and feature sets. |

| Manual Processes | Low initial cost, simplicity | A very small business using spreadsheets for lead tracking. | Persistent for early-stage startups with tight budgets. |

| Custom-Built Solutions | Unparalleled integration, control | A large enterprise developing an in-house marketing automation system. | Significant IT spending on bespoke software development. |

| Accessible AI Tools | Task automation, affordability | A small business using AI writing tools for social media content. | Rapid adoption and increasing sophistication of AI applications. |

Entrants Threaten

High Initial Capital Requirements

Entering the comprehensive CRM and marketing automation software market, where HubSpot is a major player, demands significant upfront investment. This includes hefty costs for research and development, building robust IT infrastructure, and executing extensive marketing campaigns to gain traction.

These substantial financial barriers effectively discourage many potential new competitors from entering and challenging established companies. For instance, building a competitive SaaS platform often requires millions in initial funding, making it difficult for smaller startups to compete on scale and feature set.

Complexity of Technological Infrastructure

The sheer technological complexity of building a comprehensive platform like HubSpot presents a substantial barrier to entry. Developing a robust, scalable, and integrated software solution that effectively manages marketing, sales, customer service, and operations requires immense technical expertise and investment. Newcomers must contend with the challenge of creating a sophisticated and stable infrastructure capable of rivaling established players.

Strong Brand Loyalty and Switching Costs

HubSpot benefits from substantial brand loyalty, especially among small and medium-sized businesses (SMBs). This strong recognition makes it harder for new players to gain traction.

The practical difficulties and expenses involved in migrating from HubSpot's integrated platform to a competitor's system present a significant hurdle for potential new entrants. For instance, in 2024, businesses often rely on HubSpot for CRM, marketing automation, and sales tools, making a complete data migration and retraining process time-consuming and costly.

Difficulty in Establishing Distribution Channels

New companies face a significant hurdle in building the extensive distribution networks that established players like HubSpot already possess. This includes direct sales teams, robust partner ecosystems, and a seamless online customer journey, all of which are costly and time-consuming to replicate.

For instance, in the SaaS market, where HubSpot operates, the cost of customer acquisition can be substantial. In 2023, the average customer acquisition cost (CAC) for SaaS companies ranged from $1,000 to $5,000, highlighting the investment needed to build a customer base, which is intrinsically linked to distribution reach.

- Difficulty in replicating HubSpot's established partner network.

- High cost and time investment required to build a comparable online presence and direct sales force.

- New entrants must overcome the inertia of existing customer relationships with established providers.

- The need to invest heavily in marketing and sales infrastructure to even begin competing on distribution.

Regulatory and Data Privacy Hurdles

While the CRM software sector doesn't typically face high capital investment barriers, new entrants must contend with increasingly stringent data privacy regulations like GDPR and CCPA. Navigating these complex legal frameworks and ensuring robust compliance adds significant cost and technical overhead, creating a substantial hurdle for those looking to enter the market. For instance, in 2024, companies investing in data privacy compliance saw an average increase of 15% in their operational budgets specifically for legal and IT security teams.

Building a CRM platform that not only functions effectively but also adheres to these evolving data privacy standards requires specialized expertise and ongoing investment. This complexity can deter potential competitors who may lack the resources or knowledge to meet these requirements from the outset.

- Regulatory Compliance Costs: New CRM entrants in 2024 faced an average of $50,000-$150,000 in initial legal and compliance setup costs.

- Data Privacy Expertise: A shortage of skilled data privacy professionals in 2024 meant higher salaries and recruitment challenges for new firms.

- Evolving Standards: The constant updates to data privacy laws necessitate continuous adaptation, adding to the long-term threat of new entrants.

High Barriers Protect CRM Market from New Entrants

The threat of new entrants into the CRM and marketing automation space, where HubSpot is a significant player, is generally considered moderate to low. High upfront investments in research and development, coupled with the need for robust IT infrastructure and extensive marketing, create substantial financial barriers. For example, developing a competitive SaaS platform can easily require millions in initial funding, making it challenging for smaller startups to enter the market and compete effectively.

The technological complexity of creating an integrated platform like HubSpot, which spans marketing, sales, and customer service, demands immense technical expertise and ongoing investment. Newcomers must also contend with established brand loyalty and the practical difficulties and costs associated with data migration for businesses already using HubSpot. In 2024, businesses often found switching CRM providers a time-consuming and costly endeavor.

Furthermore, building comparable distribution networks, including direct sales teams and partner ecosystems, is both expensive and time-consuming. The average customer acquisition cost in the SaaS market in 2023 ranged from $1,000 to $5,000, underscoring the significant investment required to build a customer base.

| Barrier | Description | 2024 Data/Impact |

|---|---|---|

| Capital Requirements | High costs for R&D, IT infrastructure, and marketing. | Developing competitive SaaS platforms can cost millions. |

| Technological Complexity | Need for sophisticated, scalable, and integrated software. | Requires immense technical expertise and investment to rival established players. |

| Brand Loyalty & Switching Costs | Established customer relationships and migration difficulties. | Data migration and retraining are time-consuming and costly for businesses. |

| Distribution Channels | Building sales teams and partner networks. | Customer acquisition costs in SaaS averaged $1,000-$5,000 in 2023. |

| Regulatory Compliance | Adhering to data privacy laws like GDPR and CCPA. | Initial legal and compliance setup costs for new CRM entrants averaged $50,000-$150,000. |

Porter's Five Forces Analysis Data Sources

Our HubSpot Porter's Five Forces analysis leverages a robust combination of publicly available company filings, industry-specific market research reports, and proprietary HubSpot usage data. This blend ensures a comprehensive understanding of competitive pressures, customer behavior, and market dynamics.