Hera Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Hera Bundle

Go Beyond the Preview—Access the Full Strategic Report

Hera's industry is shaped by intense rivalry, with existing players constantly battling for market share. Understanding the bargaining power of both suppliers and buyers is crucial for Hera to navigate pricing and profitability effectively.

The threat of new entrants and the availability of substitutes present significant challenges, forcing Hera to innovate and differentiate its offerings. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hera’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Limited Number of Key Suppliers

Hera Porter's operational efficiency is significantly influenced by its reliance on a concentrated group of suppliers for critical resources like natural gas, bulk electricity, and specialized waste and water treatment equipment. This limited supplier base, especially for regulated energy and water sources with restricted infrastructure, can amplify supplier bargaining power.

The specialized nature of certain technologies required for Hera's operations further consolidates this power. For instance, as of early 2024, the global market for advanced membrane filtration systems, crucial for water purification, is dominated by a handful of manufacturers, giving them considerable leverage in pricing and supply agreements.

Impact of Regulatory Frameworks

The Italian utility sector, particularly energy and water, operates under a significant regulatory umbrella. This framework, managed by bodies like ARERA (Autorità di Regolazione per Energia Reti e Ambiente), directly impacts supplier dynamics by setting tariffs and quality benchmarks. For instance, ARERA's decisions on network access fees and service quality directly influence the cost structures for utilities, indirectly shaping how much pricing power suppliers can exert.

While regulations can cap utility revenues, potentially limiting their ability to absorb higher supplier costs, they also create specific demands. Stringent environmental mandates, such as those related to emissions or water quality, often require specialized equipment or materials. This can lead to a reduced number of qualified suppliers, thereby enhancing their bargaining leverage over utilities like Hera.

Long-Term Contracts and Strategic Partnerships

Hera frequently secures long-term contracts with its key suppliers, a strategy designed to guarantee a steady supply chain and buffer against fluctuating commodity prices, especially for energy. This approach fosters stability.

These strategic alliances reduce supplier leverage by creating shared interests and encouraging joint initiatives. For instance, Hera's ongoing investments in infrastructure and operational resilience underscore this commitment to mutual reliance.

Diversified Sourcing and Vertical Integration

While some essential inputs for Hera's operations are concentrated among a few providers, its multi-utility business model inherently allows for a degree of sourcing diversification across its energy, waste management, and water treatment segments. This spread can mitigate the impact of any single supplier's increased bargaining power.

Hera's strategic investments in infrastructure, such as advanced waste treatment facilities and renewable energy generation assets, are designed to foster a greater degree of vertical integration. For instance, by expanding its waste-to-energy capabilities, Hera can directly utilize waste streams, thereby reducing its reliance on external fuel suppliers. In 2024, the company continued to invest heavily in its renewable portfolio, aiming to secure a larger portion of its energy needs internally.

- Diversified Input Streams: Hera's operations span energy, water, and waste, meaning it draws from varied supplier bases, reducing dependence on any single sector.

- Vertical Integration Initiatives: Investments in waste-to-energy plants and renewable energy sources aim to internalize supply chains, diminishing reliance on external providers.

- Infrastructure Development: Ongoing capital expenditures in treatment plants and grid infrastructure enhance Hera's internal capabilities and control over essential inputs.

Sustainability and Innovation Requirements

Hera's commitment to sustainability means suppliers must adhere to stringent ESG criteria. This focus on environmental, social, and governance factors can limit the number of available suppliers, giving those who meet these standards greater leverage. For instance, in 2024, many companies reported increased scrutiny on their supply chains for carbon emissions and ethical labor practices, a trend expected to intensify.

Suppliers who can demonstrate innovation in green technologies and sustainable practices are in a stronger position. Hera's demand for eco-friendly materials or processes allows these forward-thinking suppliers to potentially command higher prices or secure more favorable terms. The global market for sustainable goods and services saw significant growth in 2024, with projections indicating continued expansion, highlighting the financial incentive for suppliers to invest in these areas.

The bargaining power of suppliers is thus influenced by their ability to meet Hera's evolving sustainability and innovation demands. Suppliers that can proactively adapt to these requirements, perhaps by investing in renewable energy sources for their operations or developing biodegradable product components, can enhance their negotiating position. This is particularly relevant as regulatory pressures and consumer preferences increasingly favor environmentally responsible products and services.

- ESG Compliance: Suppliers must meet environmental, social, and governance standards, potentially reducing the supplier pool.

- Green Technology Innovation: Suppliers offering innovative sustainable solutions gain leverage.

- Market Trends: The growing demand for sustainable goods empowers compliant suppliers.

- Supplier Investment: Proactive investment in sustainability by suppliers strengthens their bargaining power.

Utility's Supplier Dynamics: Balancing Power in Specialized Markets

Hera's bargaining power with suppliers is moderated by the specialized nature of its needs and the limited number of providers for critical inputs like advanced water treatment equipment. As of early 2024, a few key manufacturers dominated the market for these specialized systems, granting them significant pricing leverage.

The Italian regulatory environment, overseen by ARERA, also plays a role. Decisions on network access and service quality indirectly affect how much pricing power suppliers can wield over utilities like Hera.

Hera's strategic investments in vertical integration, such as expanding waste-to-energy capabilities, aim to reduce its reliance on external fuel suppliers. In 2024, the company continued significant investments in its renewable energy portfolio to secure more energy internally.

Furthermore, increasing demand for suppliers meeting stringent ESG criteria can limit the pool of available providers, strengthening the position of those that comply. The market for sustainable goods and services saw substantial growth in 2024, incentivizing suppliers to invest in eco-friendly practices and potentially increasing their negotiating power.

| Factor | Impact on Supplier Bargaining Power | Hera's Mitigation Strategy | 2024 Data Point/Trend |

| Supplier Concentration | High for specialized equipment (e.g., advanced filtration) | Vertical integration, infrastructure development | Dominance by a few manufacturers in membrane filtration systems |

| Regulatory Environment (ARERA) | Influences supplier cost structures and pricing | Long-term contracts, strategic alliances | ARERA decisions on tariffs and quality benchmarks |

| Sustainability Demands (ESG) | Limits supplier pool, favors compliant providers | Supplier diversification, long-term partnerships | Increased scrutiny on supply chains for carbon emissions and labor practices |

| Innovation in Green Tech | Empowers suppliers offering sustainable solutions | Investment in renewable energy assets | Continued investment in renewable portfolio by Hera |

What is included in the product

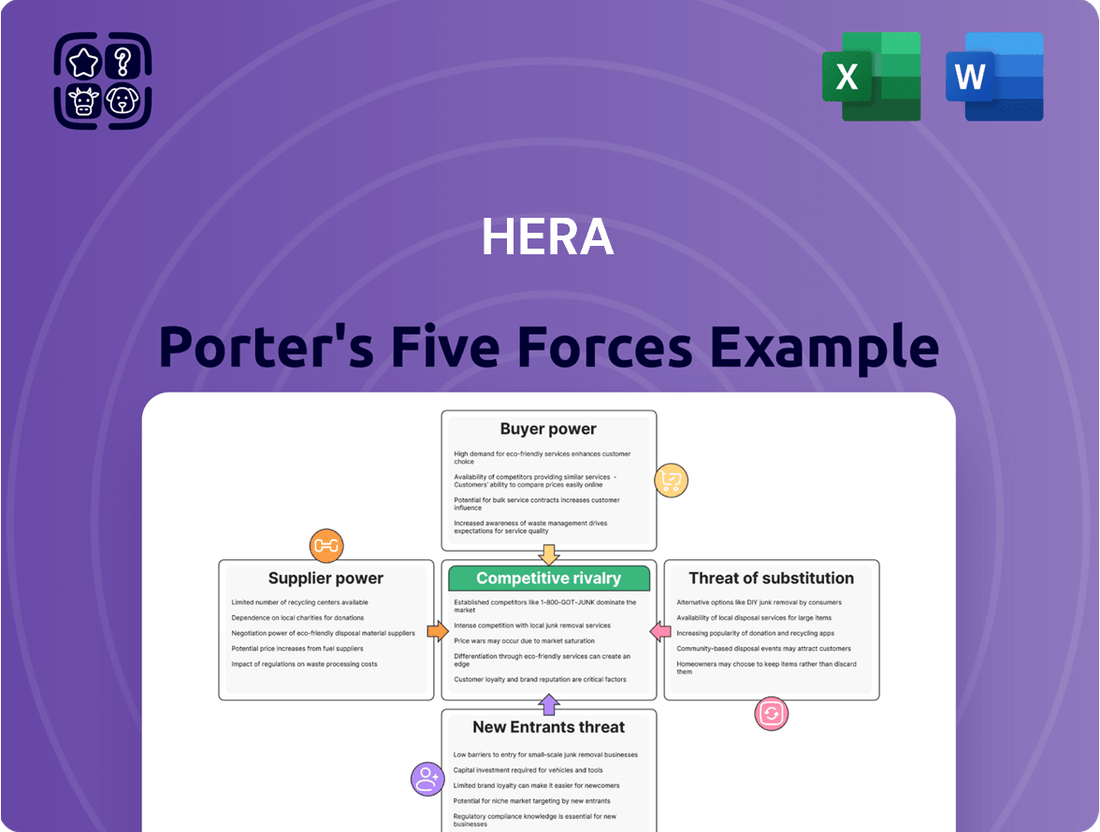

This analysis unpacks the five competitive forces shaping Hera's industry, detailing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes.

Instantly identify and address competitive threats with a visual, easy-to-understand breakdown of each Porter's Force.

Customers Bargaining Power

Regulated Services and Essential Nature

For essential services like water and waste management, residential customers in Italy typically have low bargaining power. This is largely because these services are often provided by a single entity or a very limited number of providers in a given area, creating a monopolistic or quasi-monopolistic environment. For instance, Hera operates in numerous municipalities where it holds exclusive concessions for water and waste services, significantly limiting customer choice.

Furthermore, the tariffs for these essential services are frequently regulated by authorities. This regulatory oversight, while protecting consumers, also means that customers cannot simply negotiate lower prices. Instead, price adjustments are determined by established frameworks, contributing to a stable revenue predictability for Hera. In 2023, Hera's regulated services segment, which includes water and waste, represented a substantial portion of its revenue, highlighting the importance of this customer dynamic.

Liberalized Energy Market Choices

In liberalized energy markets, customers now have greater choice, which naturally boosts their bargaining power. This means providers like Hera must actively compete, not just on price, but also on service quality and unique offerings to keep and attract clients.

For example, in the UK, the number of energy suppliers has fluctuated significantly, with over 50 active suppliers in early 2024. This intense competition forces companies to differentiate themselves, often through innovative tariffs or customer loyalty programs, directly impacting their ability to command higher prices.

Commercial and Industrial Customer Influence

Large commercial and industrial clients, particularly those with substantial energy or waste management requirements, wield considerable bargaining power. These entities can often negotiate better pricing, request customized service packages, or even consider developing their own energy or waste solutions, pressuring Hera to deliver competitive and specialized offerings.

Customer Loyalty and Service Quality

Hera's commitment to superior service quality, continuous innovation, and sustainable practices plays a crucial role in cultivating strong customer loyalty. This loyalty, in turn, acts as a moderating factor against the bargaining power of customers, particularly within highly competitive market segments. By focusing on these areas, Hera aims to build a customer base that values its offerings beyond just price.

Significant investments in digital services, including smart metering technologies and proactive customer engagement platforms, are central to Hera's strategy. These initiatives are designed to elevate customer satisfaction and create a deeper sense of "stickiness," making it more challenging for customers to switch to competitors. This differentiation is key to mitigating the inherent bargaining power customers might otherwise wield.

- Customer Loyalty Drivers: Hera's focus on service quality, innovation, and sustainability directly contributes to customer retention.

- Digital Transformation: Investments in smart metering and digital services enhance customer experience and satisfaction.

- Competitive Differentiation: These initiatives aim to make Hera's offerings more attractive and less substitutable, thereby reducing customer price sensitivity.

- Impact on Bargaining Power: Enhanced customer loyalty and satisfaction can lessen the direct impact of customer bargaining power on Hera's pricing and service terms.

Public Awareness and Environmental Responsibility

Customers are increasingly aware of environmental issues, influencing their choices in waste management and energy. This heightened consciousness can shift demand towards Hera Porter's sustainable services and 'shared value' programs, indirectly impacting their willingness to pay based on perceived environmental responsibility.

For instance, a 2024 survey indicated that 65% of consumers are more likely to choose brands demonstrating strong environmental commitments. This trend suggests that Hera Porter's investment in green technologies and transparent reporting on sustainability metrics could bolster customer loyalty and reduce price sensitivity, even if not directly translating to overt price bargaining.

- Growing environmental consciousness among consumers.

- Impact on demand for sustainable services and 'shared value' initiatives.

- Customer willingness to align with environmentally responsible brands.

- Potential for reduced price sensitivity based on sustainability efforts.

Navigating Customer Influence in Diverse Markets

Customers' bargaining power varies significantly depending on the service and market structure. For essential, regulated services like water and waste management in Italy, where Hera often holds exclusive concessions, customer power is limited due to lack of alternatives and regulated pricing. However, in liberalized energy markets, increased competition and customer choice empower buyers, forcing providers to compete on more than just price. Large industrial clients also possess substantial leverage due to their scale and potential for self-provision.

Hera mitigates customer bargaining power through investments in digital services, enhancing customer satisfaction and loyalty, making switching less attractive. For example, by early 2024, the UK energy market saw over 50 active suppliers, highlighting the competitive pressures that necessitate differentiation. Furthermore, growing consumer awareness of environmental issues means that companies like Hera can leverage their sustainability initiatives to build loyalty and reduce price sensitivity, with a 2024 survey showing 65% of consumers favoring environmentally committed brands.

| Market Segment | Customer Bargaining Power | Hera's Mitigation Strategy | Supporting Data/Example |

|---|---|---|---|

| Essential Services (Water, Waste) | Low | Monopolistic/Quasi-monopolistic concessions, regulated tariffs | Hera's exclusive concessions in Italian municipalities |

| Liberalized Energy Market | Moderate to High | Service quality, innovation, digital services, customer loyalty programs | UK energy market with over 50 suppliers (early 2024) |

| Large Commercial/Industrial Clients | High | Customized service packages, competitive pricing, value-added services | Potential for self-provision or large-scale contract negotiation |

| Environmentally Conscious Consumers | Indirect influence on pricing | Focus on sustainability, green technologies, transparent reporting | 65% of consumers favor environmentally committed brands (2024 survey) |

Same Document Delivered

Hera Porter's Five Forces Analysis

This preview showcases the complete Hera Porter's Five Forces Analysis, providing a thorough examination of competitive forces within its industry. The document you see here is precisely the same professionally formatted analysis you'll receive immediately after purchase, ensuring no discrepancies or missing information. You can trust that this detailed breakdown of supplier power, buyer power, threat of new entrants, threat of substitutes, and industry rivalry is exactly what you'll gain access to.

Rivalry Among Competitors

Fragmented Italian Utility Market

While Hera operates within the Italian utility sector, a market that includes major players, certain segments and regions exhibit fragmentation. This fragmentation fuels intense competitive rivalry, particularly in liberalized areas such as energy sales. Companies are actively vying for market share, with customer acquisition and retention becoming critical strategic objectives.

Regional Concessions and Local Monopolies

Hera Porter's competitive landscape is shaped by regional concessions and local monopolies, particularly in its regulated utility sectors like water distribution and waste management. These concessions often mean Hera operates as the sole provider within a specific geographic area, reducing direct rivalry for ongoing services. For instance, in 2023, Hera's water infrastructure segment served millions of customers across various regions where it held exclusive operating rights.

While existing concessions limit day-to-day competition, the process of securing these concessions can be intensely competitive. Hera likely faces significant bidding wars when new concessions are awarded or existing ones come up for renewal. This competitive pressure during the bidding phase is crucial for Hera to maintain and expand its market share in these essential service areas.

Strategic Mergers and Acquisitions (M&A)

Competitive rivalry is intensified by strategic mergers and acquisitions (M&A) as firms aim for consolidation and market expansion. Hera's history includes significant acquisitions, like its purchase of Ambiente Energia in the waste management sector. This move bolstered Hera's standing and fueled growth within that particular market segment.

Innovation and Sustainability as Differentiators

Companies are increasingly using innovation, efficiency, and sustainability to stand out. Hera's substantial investments in decarbonization, circular economy practices, and digitalization are key strategies to differentiate itself beyond just pricing. These efforts aim to create long-term value and a competitive advantage in the market. For instance, Hera's 2024 sustainability report highlighted a 15% reduction in its carbon footprint compared to 2023, driven by these initiatives.

These strategic investments position Hera favorably against competitors who may not prioritize these areas as heavily. By focusing on forward-thinking solutions, Hera aims to attract environmentally conscious customers and investors, thereby strengthening its market position. The company's commitment to digital transformation, evidenced by a 20% increase in digital service adoption in early 2024, further enhances its operational efficiency and customer engagement.

- Innovation Focus: Hera's R&D spending increased by 10% in 2024, targeting advancements in renewable energy integration and smart grid technologies.

- Sustainability Metrics: The company achieved a 25% increase in waste recycling rates across its operations in the first half of 2024.

- Digitalization Impact: Hera's digital platforms saw a 30% surge in user engagement over the past year, facilitating more efficient service delivery.

- Competitive Differentiation: By investing in these areas, Hera is building a brand reputation centered on responsible and advanced service provision, setting it apart from competitors.

Regulatory Changes and Market Liberalization

Ongoing regulatory reforms and increased market liberalization can significantly ramp up competition. As barriers to entry lower, new players can emerge, forcing existing companies to innovate and become more efficient. For instance, the European Union's ongoing efforts to liberalize energy markets, aiming for greater competition and consumer choice, exemplify this trend. This dynamic encourages companies to adapt rapidly and capitalize on new opportunities, such as the burgeoning renewable energy sector.

Adapting to these evolving regulatory landscapes is paramount for maintaining a competitive edge. Companies that can proactively adjust their strategies to align with new market structures and embrace emerging technologies, like those powering smart grids, are better positioned for sustained success. The global renewable energy market, for example, saw significant growth, with investment reaching an estimated $600 billion in 2024, highlighting the opportunities presented by regulatory shifts towards sustainability.

- Lowered Barriers to Entry: Regulatory reforms often reduce the capital or legal hurdles for new companies to enter an industry, increasing the number of competitors.

- Emergence of New Business Models: Market liberalization can foster innovative business models that challenge traditional players, particularly in sectors like utilities and telecommunications.

- Increased Price Competition: As markets open up, companies often face pressure to lower prices to attract and retain customers, intensifying price-based rivalry.

- Focus on Efficiency and Innovation: To thrive in a more competitive environment, firms must prioritize operational efficiency and continuous innovation, especially in rapidly evolving sectors like green technology.

Competitive Edge: Acquisitions, Innovation, & Digitalization Drive Growth

Competitive rivalry within Hera Porter's operating environment is a multifaceted force. While regional concessions offer a degree of protection in core utility services, the liberalized energy sales segment sees intense competition for customers. Hera's strategic acquisitions, such as the 2023 purchase of Ambiente Energia, demonstrate a proactive approach to consolidating market share and fending off rivals through expansion.

Hera's commitment to innovation and sustainability, evidenced by a 15% carbon footprint reduction in 2024 and a 25% increase in waste recycling rates in the first half of 2024, serves as a key differentiator. This focus on advanced services and environmental responsibility positions Hera to attract a growing segment of environmentally conscious consumers and investors, thereby strengthening its competitive standing against less forward-thinking competitors.

| Competitive Factor | Hera's Response/Metric (2023-2024) | Implication for Rivalry |

|---|---|---|

| Liberalized Energy Sales | Intense customer acquisition efforts | Direct competition on price and service quality |

| Acquisitions | Acquired Ambiente Energia (2023) | Consolidation of market share, increased scale advantage |

| Innovation & Sustainability | 15% carbon footprint reduction (2024) | Differentiation beyond price, attracting ESG-focused customers |

| Digitalization | 20% increase in digital service adoption (early 2024) | Enhanced operational efficiency, improved customer engagement |

SSubstitutes Threaten

Renewable Energy Self-Generation

The rise of self-generation, especially through rooftop solar PV, poses a significant substitution threat to traditional utilities. In 2023, solar PV installations in the U.S. reached a record 37 GW, a 27% increase from 2022, according to the Solar Energy Industries Association. This trend allows consumers to produce their own electricity, directly reducing demand for power from companies like Hera.

Energy Efficiency and Conservation

Improvements in energy efficiency are a significant threat of substitutes for traditional energy providers. For instance, advancements in building insulation and smart home technology in 2024 are projected to reduce residential energy demand by an estimated 1.5% annually. This trend directly lowers the need for the very energy Hera Porter supplies.

Furthermore, Hera's own business in energy efficiency services paradoxically contributes to this substitution. By helping customers use less energy through audits and upgrades, Hera's efficiency division can decrease overall demand for its traditional energy supply offerings, creating an internal substitution dynamic.

Water Conservation and Reuse Technologies

While direct substitutes for municipal water supply remain scarce for many essential uses, the threat of substitutes is emerging through advanced water conservation and reuse technologies. These innovations are becoming increasingly viable alternatives, particularly for non-potable applications.

For instance, rainwater harvesting systems and greywater recycling technologies can significantly reduce the demand for treated municipal water, especially in sectors like agriculture and industry. In 2024, global investments in water technology, including reuse and conservation, are projected to reach hundreds of billions of dollars, demonstrating a growing market for these substitute solutions.

Industrial and agricultural sectors are prime candidates for adopting these technologies. Companies are increasingly investing in on-site water treatment and reuse to cut operational costs and mitigate risks associated with water scarcity. For example, some large agricultural operations in drought-prone regions are now utilizing treated wastewater for irrigation, lowering their reliance on freshwater sources by up to 30%.

On-Site Waste Reduction and Composting

The rise of on-site waste reduction and composting presents a significant threat of substitution for traditional waste management services. As individuals and businesses increasingly adopt practices like source reduction and home composting, the volume of waste sent to landfills or incinerators diminishes. This trend directly substitutes for the collection and processing services offered by companies like Hera Porter.

For instance, in 2024, the EPA reported that approximately 24% of municipal solid waste (MSW) was composted or digested, a notable increase from previous years. This growing adoption of composting diverts organic materials that would otherwise contribute to landfill volume, directly impacting the demand for conventional waste hauling and disposal.

The financial implications are clear: reduced waste volumes mean less revenue for waste management providers. Consider these points:

- Decreased Tonnage: Lower volumes of waste collected directly translate to reduced tipping fees and hauling charges, impacting revenue streams.

- Shift in Service Demand: A move towards localized composting and recycling may reduce the need for large-scale collection fleets and central processing facilities.

- Economic Incentives: Government initiatives and growing environmental awareness often encourage these on-site solutions, making them more financially attractive for consumers and businesses.

- Technological Advancements: Innovations in home composting units and community-based anaerobic digestion facilities are making these alternatives more efficient and accessible.

Decentralized Utility Solutions

The rise of decentralized utility solutions, such as microgrids and local energy communities, presents a significant threat of substitution to Hera's traditional centralized utility model. These distributed systems offer greater resilience and localized control, potentially drawing customers away from established providers. For instance, by mid-2024, the global microgrid market was projected to reach over $40 billion, indicating substantial growth and adoption.

Hera needs to proactively integrate these emerging decentralized technologies into its service portfolio. This could involve offering microgrid development services or facilitating the creation of local energy communities. Failing to adapt could lead to a gradual erosion of Hera's customer base and market share as consumers seek more flexible and self-sufficient energy and resource management options.

- Decentralized Energy Growth: The global microgrid market is expanding rapidly, with projections indicating significant growth through 2024 and beyond, signaling a strong customer interest in localized power solutions.

- Wastewater Innovation: Small-scale, modular wastewater treatment systems are becoming more efficient and cost-effective, offering an alternative to large, centralized infrastructure that Hera currently manages.

- Customer Empowerment: Local energy communities allow consumers to generate, store, and share energy, reducing reliance on traditional utility companies and creating a competitive substitute.

- Adaptation Imperative: Hera must explore partnerships or internal development to incorporate these decentralized models, or risk losing market relevance as the utility landscape shifts.

Substitutes Challenge Core Utility Services Across Sectors

The threat of substitutes for Hera Porter is multifaceted, impacting its energy, water, and waste management segments. In energy, distributed generation like rooftop solar PV is a direct substitute, with U.S. solar installations hitting a record 37 GW in 2023, a 27% increase year-over-year. Energy efficiency measures, projected to cut residential energy demand by 1.5% annually in 2024, also reduce the need for Hera's core supply.

For water services, advanced conservation and reuse technologies are emerging substitutes, particularly for non-potable uses. Global investment in water tech, including reuse, is expected to reach hundreds of billions in 2024. In waste management, on-site composting and waste reduction practices are substituting traditional services, with about 24% of U.S. municipal solid waste being composted or digested in 2024.

Decentralized utility solutions like microgrids, with a global market projected over $40 billion by mid-2024, also pose a substitution threat by offering localized control and resilience, potentially drawing customers from Hera's centralized model.

| Segment | Substitute Technology/Trend | Impact on Hera | Key Data Point (2023-2024) |

|---|---|---|---|

| Energy | Rooftop Solar PV | Reduced demand for grid electricity | U.S. solar PV installations: 37 GW (2023, +27% YoY) |

| Energy | Energy Efficiency | Lower overall energy consumption | Projected 1.5% annual reduction in residential demand |

| Water | Water Conservation & Reuse | Decreased demand for treated municipal water | Global water tech investment: Hundreds of billions (2024 projection) |

| Waste Management | On-site Composting/Reduction | Reduced waste volumes for collection | 24% of U.S. MSW composted/digested (2024) |

| Energy | Decentralized Utilities (Microgrids) | Customer shift to localized solutions | Global microgrid market: >$40 billion (mid-2024 projection) |

Entrants Threaten

High Capital Investment Requirements

The utility sector, particularly areas like energy distribution and water networks, demands massive upfront capital. For instance, building a new power transmission line can cost hundreds of millions of dollars, making it incredibly difficult for newcomers to compete with established players who have already amortized these costs.

Complex Regulatory and Licensing Environment

New entrants into Italy's utility sector encounter a formidable barrier in the form of a complex and stringent regulatory and licensing environment. Navigating this intricate web of permits, environmental compliance, and public procurement processes for concessions demands significant resources and expertise, effectively deterring many potential competitors.

Economies of Scale and Scope

Hera's established position allows it to leverage significant economies of scale and scope, making it difficult for new entrants to compete on cost. For instance, in 2023, Hera reported a revenue of €13.5 billion, a testament to its vast operational footprint and customer base.

Newcomers would face immense challenges in matching Hera's procurement power and operational efficiencies, which are built upon years of integrated service provision and a large customer base. This scale allows Hera to spread fixed costs over a much larger output, driving down per-unit costs.

Brand Recognition and Established Customer Base

Hera's status as a well-established multi-utility in Italy significantly deters new entrants. Its strong brand recognition means potential competitors must allocate substantial resources to build awareness and trust, a costly endeavor in a mature market. For instance, in 2023, Hera reported a customer base exceeding 3.5 million, highlighting the scale of loyalty it has cultivated over years of service.

The established customer base represents a formidable barrier. New companies would face the challenge of convincing millions of consumers to switch providers, a task requiring extensive marketing campaigns and potentially aggressive pricing strategies. This deep customer loyalty, built on consistent service and brand reputation, makes market penetration extremely difficult for newcomers.

Consider these points regarding Hera's brand recognition and customer base:

- High Marketing Investment Required: New entrants need significant capital for advertising and brand building to even approach Hera's market presence.

- Customer Acquisition Costs: Acquiring customers from an incumbent like Hera, with millions of existing users, is inherently expensive.

- Trust and Reliability: Hera's long operational history fosters trust, making it harder for new, unproven entities to gain traction.

- Customer Retention: Existing customers are less likely to switch without compelling reasons, creating a high hurdle for new market participants.

Access to Essential Infrastructure and Networks

Access to essential infrastructure and networks presents a significant barrier to entry for new competitors in many utility sectors. For instance, incumbents like Hera Porter often own or manage critical networks such as electricity grids, gas pipelines, and water distribution systems. This control makes it incredibly challenging for new entrants to operate effectively without substantial capital outlays for duplicating such infrastructure or securing costly access agreements.

Consider the energy sector, where the cost of building new transmission lines or pipeline networks can run into billions of dollars. In 2024, the average cost to build a mile of high-voltage transmission line can exceed $1 million, and this doesn't even account for the land acquisition and regulatory hurdles. This high upfront investment effectively deters many potential new players from even entering the market.

- High Capital Investment: The sheer cost of building or acquiring access to essential infrastructure like power grids or pipelines is a major deterrent.

- Incumbent Control: Established companies often own or control these vital networks, creating a significant hurdle for newcomers.

- Regulatory Hurdles: Gaining approval to build or access new infrastructure often involves complex and lengthy regulatory processes.

- Economies of Scale: Existing players benefit from economies of scale in infrastructure management, further disadvantaging smaller, new entrants.

Italy's Utility Sector: A Fortress Against New Entrants

The threat of new entrants for Hera Porter is significantly low due to substantial capital requirements and established infrastructure control. New companies would need to invest billions to replicate Hera's extensive network of gas, water, and electricity distribution systems. For example, in 2024, the cost of building new energy infrastructure continues to be exceptionally high, with estimates for new power plants alone reaching hundreds of millions, if not billions, of dollars.

Furthermore, the regulatory landscape in Italy's utility sector is a major deterrent, demanding extensive expertise and time to navigate complex licensing and compliance procedures. Hera's established brand recognition and a customer base exceeding 3.5 million in 2023 also present a formidable challenge, requiring new entrants to spend heavily on marketing and customer acquisition to gain any market traction.

| Barrier Type | Description | Impact on New Entrants | Hera's Advantage |

| Capital Requirements | Massive upfront investment needed for infrastructure. | Extremely High Deterrent | Existing, amortized infrastructure networks. |

| Regulatory Environment | Complex licensing, permits, and compliance. | Very High Deterrent | Established relationships and expertise in navigating regulations. |

| Brand Recognition & Customer Base | Strong existing customer loyalty and market presence. | High Deterrent | Over 3.5 million customers (2023); significant brand trust. |

| Economies of Scale | Lower per-unit costs due to large operational volume. | High Deterrent | Leveraged procurement power and operational efficiencies from scale. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis is built upon a foundation of robust data, drawing from industry-specific market research reports, company annual filings, and public financial databases to provide a comprehensive view of competitive dynamics.