Weave Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Weave

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Weave's competitive landscape is shaped by powerful forces, from the bargaining power of its customers to the constant threat of new companies entering the market. Understanding these dynamics is crucial for any business operating in or considering this sector.

This brief overview only scratches the surface of Weave's strategic positioning. Unlock the full Porter's Five Forces Analysis to explore Weave’s competitive dynamics, market pressures, and strategic advantages in detail, empowering you with actionable insights.

Suppliers Bargaining Power

Concentration of Cloud Infrastructure Providers

Weave's reliance on cloud infrastructure for its all-in-one platform places it directly in the path of the bargaining power of suppliers, particularly concentrated cloud infrastructure providers. Major players like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud hold significant sway. This concentration means these providers can exert considerable influence over Weave's operational costs, as cloud computing is a critical, and often a top three, expenditure for Software as a Service (SaaS) companies. Indeed, global cloud spending was anticipated to exceed $824 billion by 2025, highlighting the substantial financial commitment involved.

Availability of Telecom Services

Weave, as a communications platform, relies heavily on the availability and cost of telecom services for its core functions, such as Voice over Internet Protocol (VoIP) and text messaging. The broader global telecom market is substantial and projected to reach $2.32 trillion in 2024, with an anticipated compound annual growth rate (CAGR) of 6.15% through 2034. This indicates a generally robust market, but the specific terms negotiated with individual telecom providers for pricing and service levels directly influence Weave's operational expenses and, consequently, its cost of goods sold.

Proprietary Technology and APIs from Third-Party Integrations

Weave's reliance on third-party practice management and EHR systems for integration means that suppliers with proprietary technology or restricted API access can wield significant bargaining power. If these systems are difficult to replicate or integrate with, it can lead to higher costs for Weave or limit the seamless functionality it aims to provide its users.

Labor Market for Skilled Software Developers and AI Specialists

The demand for skilled software developers, especially those with expertise in AI and healthcare SaaS, directly impacts labor costs. Weave's strategic focus on AI, highlighted by its acquisition of TrueLark in 2023 for an undisclosed sum, indicates a significant reliance on this specialized talent. This reliance can escalate operational expenses if the availability of such professionals remains constrained.

The competitive landscape for AI and software development talent is intensifying. For instance, in 2024, the average base salary for a senior AI engineer in the US ranged from $150,000 to $200,000 annually, with significant bonuses and stock options. This upward pressure on wages for specialized skills directly affects companies like Weave, potentially increasing their cost of goods sold and impacting profitability.

- High Demand for AI/SaaS Talent: Companies are aggressively seeking developers proficient in AI, machine learning, and cloud-based healthcare solutions.

- Rising Compensation: This demand drives up salaries and benefits packages for these in-demand roles, increasing labor costs for employers.

- Acquisition Impact: Weave's acquisition of TrueLark demonstrates a commitment to AI, increasing its dependency on a talent pool facing supply limitations.

- Operational Expense Increase: A tight labor market for these skills can lead to higher recruitment costs, retention challenges, and ultimately, increased operational expenses for Weave.

Payment Processing Partners

Payment processing partners hold significant sway over Weave's operational costs. As Weave integrates these solutions, the fees charged by these partners directly impact the profitability of each transaction. For instance, in 2024, the average transaction fee for online payments globally hovered around 2.9%, a figure that could significantly eat into margins if not managed effectively.

The bargaining power of these payment processors is amplified by their established networks and the critical nature of their services for Weave's expanding payments business. A concentrated market of major payment providers means fewer alternatives for Weave, potentially leading to less favorable terms. Consider that Visa and Mastercard, two dominant players, processed trillions of dollars in transactions in 2024, underscoring their market leverage.

- High Concentration: A limited number of large payment processors control a significant market share.

- Switching Costs: Migrating payment systems can be complex and costly for Weave.

- Essential Service: Weave relies heavily on these partners to facilitate its core payment operations.

- Fee Negotiation: The ability to negotiate favorable transaction rates is crucial for profitability.

Tech Suppliers' Power: Integration Challenges for Seamless Solutions

Suppliers with unique or difficult-to-replicate technologies, such as specialized EHR or practice management software, can exert considerable bargaining power over Weave. This power stems from the potential for higher integration costs or limitations in delivering seamless functionality to Weave's end-users, impacting Weave's ability to offer a fully integrated solution.

What is included in the product

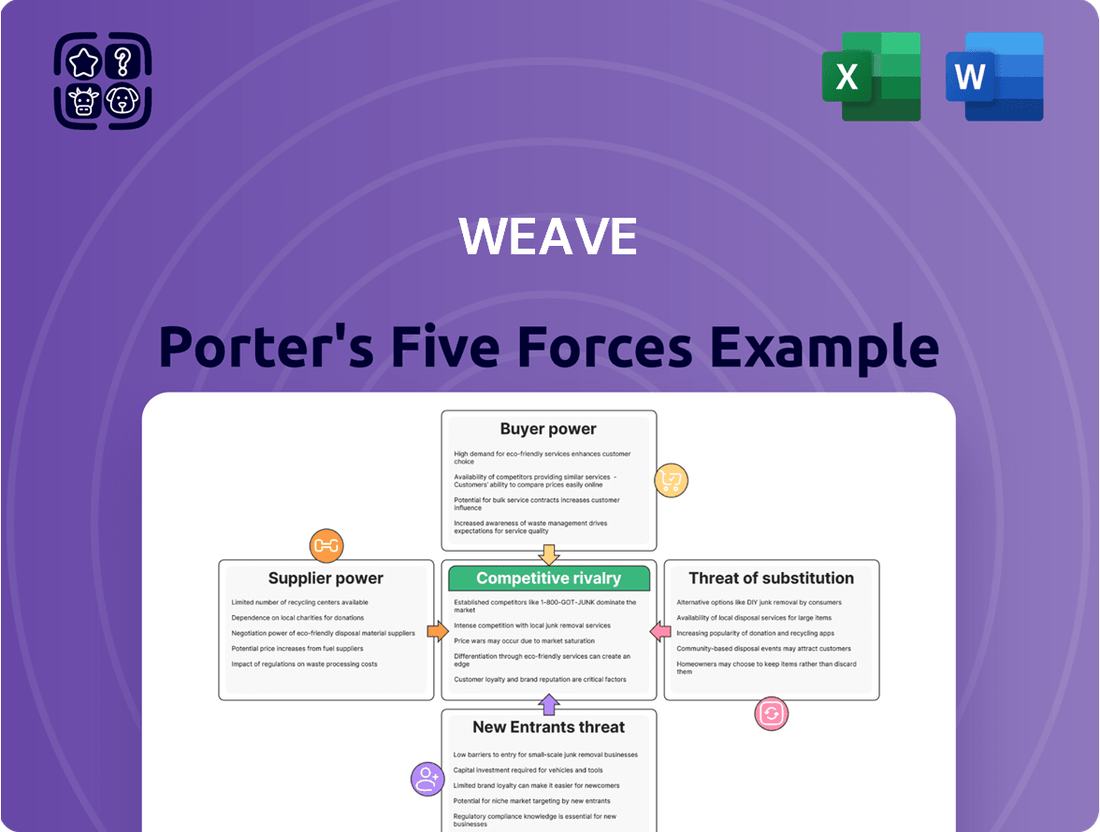

This analysis examines the competitive forces impacting Weave, including the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitutes, and the intensity of rivalry among existing competitors.

Instantly identify and mitigate competitive threats with a visual breakdown of industry power dynamics.

Customers Bargaining Power

Fragmented Small and Medium-Sized Business (SMB) Market

Weave's primary customer base consists of small and medium-sized healthcare businesses. This market segment is characterized by its large size and fragmentation, meaning that individual customers typically represent a small portion of Weave's overall sales volume.

Consequently, the bargaining power of these individual SMB customers is generally low. Their limited purchase volumes mean they lack the leverage to demand significant price concessions or highly customized terms from Weave.

For instance, in 2024, the average revenue per SMB customer in the healthcare technology sector remained relatively stable, indicating that suppliers were not forced into substantial price reductions due to customer pressure.

Switching Costs for Customers

The bargaining power of customers is influenced by switching costs. For healthcare practices, moving from Weave's integrated platform to a competitor involves substantial effort, including data migration and retraining staff on new systems. This complexity makes switching less appealing, thereby strengthening Weave's position by reducing customer leverage.

Availability of Alternatives and Competitors

The patient relationship management (PRM), patient engagement, and telemedicine software markets are quite crowded. Think of companies like Solutionreach, RevenueWell, Spruce Health, NexHealth, and Carepatron, all offering similar services. This abundance of choices directly empowers customers, giving them more leverage when negotiating prices or demanding better features.

Price Sensitivity of SMBs

Small and medium-sized businesses (SMBs) often exhibit significant price sensitivity, particularly for essential services like recurring software subscriptions. Weave's pricing structure, including any planned adjustments, could encounter pushback if competitors offer comparable value at a lower cost. For instance, in 2024, many SMBs were actively seeking cost-optimization strategies, with surveys indicating that over 60% of small businesses re-evaluated their software spending to manage budgets more effectively.

This price sensitivity directly impacts Weave's bargaining power of customers. Competitors offering more aggressive pricing or bundled solutions that appear more cost-effective can exert considerable pressure.

- Price Sensitivity: SMBs are often budget-conscious, making price a key factor in purchasing decisions for recurring services.

- Competitive Landscape: The availability of lower-priced alternatives or perceived better value from competitors can empower customers to demand concessions.

- Value Perception: If customers do not clearly see the value proposition justifying Weave's price, they are more likely to switch or negotiate.

- Market Trends: In 2024, a notable trend was SMBs actively seeking to reduce operational overheads, increasing their leverage in price negotiations.

Customer's Ability to DIY or Use Multiple Standalone Solutions

Customers' inclination to "do-it-yourself" or aggregate disparate solutions significantly amplifies their bargaining power. Instead of opting for an all-in-one platform like Weave, they might opt to combine separate VoIP services, individual texting applications, and standalone scheduling tools. This fragmentation of services directly challenges the value proposition of integrated solutions.

This DIY approach, or the use of multiple vendors, provides customers with readily available alternatives. For instance, a small business might find that using a combination of free or low-cost communication tools meets their needs adequately, thereby reducing their reliance on a single, integrated provider. This creates leverage for customers when negotiating terms or pricing.

- Customer Bargaining Power: Increased by the availability of standalone communication tools.

- DIY Adoption: Customers can piece together services like VoIP, texting, and scheduling apps.

- Alternative Solutions: Using multiple vendors offers a direct counter to integrated platforms.

- Market Impact: This trend can drive down prices for integrated solutions as providers compete with fragmented offerings.

Customer Leverage: SMBs Reshape Software Spending in 2024

The bargaining power of Weave's customers is moderate, influenced by factors like price sensitivity and the availability of alternative solutions. While switching costs are a deterrent, the fragmented nature of the SMB healthcare market means individual customers have limited leverage, but collectively, they can exert pressure.

In 2024, many SMBs focused on cost optimization, with over 60% re-evaluating software spending, increasing their negotiation power. The availability of numerous competitors offering similar services, such as Solutionreach and NexHealth, further empowers customers by providing readily accessible alternatives and driving competitive pricing.

Customers' willingness to adopt a do-it-yourself approach by integrating separate, often lower-cost, tools like VoIP and texting applications directly challenges the value proposition of integrated platforms like Weave, thereby enhancing their bargaining power.

| Factor | Impact on Weave's Customer Bargaining Power | 2024 Data/Trend |

|---|---|---|

| Customer Size & Fragmentation | Low individual leverage due to small purchase volumes | Healthcare SMB market remains large and fragmented |

| Switching Costs | Reduces customer leverage (data migration, retraining) | Complexity of migration remains a barrier for many SMBs |

| Availability of Alternatives | Increases customer leverage (e.g., Solutionreach, NexHealth) | Crowded market with numerous competitors offering similar features |

| Price Sensitivity | Increases customer leverage, especially for recurring services | Over 60% of SMBs re-evaluated software spending in 2024 for cost optimization |

| DIY/Aggregated Solutions | Increases customer leverage by providing alternatives to integrated platforms | Growing trend of SMBs combining separate VoIP, texting, and scheduling tools |

Full Version Awaits

Weave Porter's Five Forces Analysis

This preview displays the complete Weave Porter's Five Forces Analysis, offering a thorough examination of competitive forces within the industry. The document you see here is precisely what you will receive immediately after purchase, ensuring full transparency and immediate usability. You can confidently expect this exact, professionally formatted analysis to be available for download the moment your transaction is complete.

Rivalry Among Competitors

Number and Diversity of Competitors

The patient communication and engagement platform market, especially in healthcare, is quite crowded. You'll find a wide array of companies, from those focused purely on patient relationship management (PRM) software to broader platforms that also offer telemedicine and general patient engagement tools. This means there are many different types of competitors vying for attention.

Key players in this space include Solutionreach, RevenueWell, Spruce Health, NexHealth, and Carepatron, among others. Their diverse offerings mean that a single company might compete with several different types of solutions depending on the specific functionality a healthcare provider is seeking. This variety intensifies the rivalry as companies differentiate themselves through specialized features or broader integrated services.

Market Growth Rate

The clinical communication and collaboration software market is booming, with projections indicating it will reach $2.3 billion by 2025, growing at an impressive 18.9% compound annual growth rate (CAGR). This rapid expansion signals a dynamic environment where existing players and new entrants alike are eager to capture market share.

Furthermore, the broader healthcare business collaboration tools market is set to experience an even steeper growth trajectory, with a CAGR of 23.43% anticipated between 2025 and 2034. Such robust growth naturally draws attention, potentially increasing the number of competitors and intensifying the rivalry among them as they strive to innovate and capture this expanding market.

Product Differentiation and Features

Weave distinguishes itself with a comprehensive platform that unifies communication and payment processing, a key differentiator in the market. However, the competitive landscape is intensifying as rivals introduce advanced features like AI-driven automation and enhanced interoperability. For instance, some competitors are reporting significant user growth in 2024, with platforms seeing a 25% increase in integrated service adoption, pushing Weave to constantly innovate to stay ahead.

Switching Costs for Customers

High switching costs for customers can significantly impact Weave's competitive landscape. These costs act as a barrier, making it more difficult for rivals to lure away Weave's existing user base. For instance, if a small business has deeply integrated Weave's platform into their daily operations, the time, effort, and potential disruption involved in migrating to a competitor's system can be substantial.

Conversely, Weave itself must invest resources to overcome these same switching costs when targeting customers already committed to other platforms. This means that Weave's customer acquisition strategy needs to account for the inherent stickiness of existing solutions. In 2024, the average cost for a business to switch CRM providers, for example, can range from hundreds to thousands of dollars, depending on the complexity of data migration and retraining needs.

- Customer Retention: High switching costs bolster Weave's customer retention by increasing the perceived risk and expense of leaving.

- Customer Acquisition Challenge: Weave faces an uphill battle acquiring customers from competitors if those customers have high switching costs.

- Competitive Advantage: If Weave can offer significantly lower switching costs for its own platform, it gains a competitive edge in attracting new clients.

- Industry Norms: Understanding the typical switching costs within the industries Weave serves is crucial for strategic planning.

Investment in AI and Advanced Technologies

Weave and its competitors are locked in a fierce race to integrate artificial intelligence and automation into their healthcare communication platforms. This intense investment aims to boost efficiency for healthcare providers and improve patient engagement. The market is seeing significant capital allocation towards developing sophisticated AI capabilities.

Weave's strategic acquisition of TrueLark in 2023 for an undisclosed sum highlights this commitment to AI-powered front-desk automation. This move signals a substantial investment designed to keep Weave at the forefront of technological innovation and competitive offerings in the healthcare technology space.

- AI Investment: Competitors are also channeling significant resources into AI development, creating a high barrier to entry for less technologically advanced players.

- Automation Focus: Streamlining administrative tasks through AI and automation is a key battleground for market share.

- Platform Enhancement: Continuous investment is necessary to enhance platform features and offer superior user experiences.

- Competitive Pressure: The rapid pace of AI advancement necessitates ongoing investment to avoid falling behind rivals.

Healthcare Tech Rivalry: AI, Growth, and Switching Costs

The competitive rivalry within the patient communication and engagement platform market is intense, driven by a crowded field of providers offering diverse solutions. Companies like Solutionreach, RevenueWell, and NexHealth are actively innovating, pushing the market towards AI-driven automation and enhanced interoperability. This dynamic environment sees players constantly differentiating themselves through specialized features or integrated services to capture market share.

The rapid growth projected for both clinical communication and broader healthcare business collaboration tools, with CAGRs reaching 18.9% and 23.43% respectively, fuels this rivalry. Such expansion attracts new entrants and encourages existing ones to invest heavily in R&D, particularly in AI and automation, as demonstrated by Weave's acquisition of TrueLark. This arms race for technological superiority means continuous investment is crucial to remain competitive.

Weave's competitive advantage is also shaped by customer switching costs, which can be substantial in the healthcare tech sector. While these costs can aid retention, they also present acquisition challenges for Weave when targeting customers already embedded with competitors. Understanding these costs, which can range from hundreds to thousands of dollars for migrating integrated systems in 2024, is vital for strategic positioning.

SSubstitutes Threaten

Manual Communication Methods

Even with advanced digital tools, some small to medium-sized healthcare providers continue to use manual communication like phone calls, faxes, and mail for patient engagement and administrative functions. These methods act as basic substitutes, particularly for less tech-savvy demographics or in situations where digital access is limited. For instance, a 2024 survey indicated that approximately 15% of independent physician practices still primarily rely on fax machines for patient record transfers, highlighting their persistence as a substitute communication channel.

Generic Communication Tools (e.g., standard email, generic messaging apps)

The threat of substitutes for specialized healthcare communication platforms like Weave is significant, as generic communication tools pose a viable alternative for many practices. Standard email, consumer-grade messaging apps, and basic VoIP services are readily available and often free or low-cost, making them attractive options. For instance, a small practice might find that using WhatsApp for quick patient messages and a shared Google Calendar for appointments suffices, bypassing the need for a dedicated, integrated system.

Basic Practice Management Systems with Limited Communication Features

Some healthcare businesses, particularly smaller or older practices, might still rely on basic practice management systems with limited communication features. These systems, while functional for scheduling and billing, may not offer robust patient engagement tools like secure messaging or automated reminders, potentially viewing them as adequate substitutes for more advanced platforms.

In-house Developed Solutions

Larger, more technologically advanced healthcare organizations might opt to build their own proprietary communication and patient engagement software. This allows for highly customized features that precisely match their specific workflows and patient demographics, potentially offering a more integrated experience than off-the-shelf solutions.

In 2024, healthcare IT spending is projected to reach over $150 billion, with a significant portion allocated to custom development and integration projects. Organizations with substantial IT budgets and internal development teams can leverage this to create bespoke platforms that directly address their unique operational requirements, potentially reducing reliance on third-party vendors.

- Customization: In-house solutions offer unparalleled tailoring to specific organizational needs.

- Integration: Seamless integration with existing Electronic Health Records (EHR) and other internal systems can be a key advantage.

- Cost Control: While initial investment can be high, long-term operational costs might be lower for large organizations compared to ongoing subscription fees.

- Data Security: Some organizations may prefer in-house solutions for greater control over patient data security and compliance.

Direct Patient Portals from EHR Systems

Many Electronic Health Record (EHR) systems now include their own patient portals. These native portals can handle tasks like appointment scheduling and accessing medical records, directly competing with some of Weave's core offerings. For practices deeply integrated with a specific EHR, these built-in portals may present a significant substitute.

The threat here is that healthcare providers might opt to use the EHR's native portal instead of a third-party solution like Weave. This is particularly true if the EHR's portal offers sufficient functionality for their needs, reducing the perceived value of Weave's integrated communication and patient engagement tools. For instance, a practice already paying a substantial fee for their EHR might see its included portal as a cost-saving alternative.

- EHR Native Portals: Offer integrated patient communication, scheduling, and record access.

- Substitution Risk: Practices may forgo third-party solutions if EHR portals meet their needs.

- Cost-Benefit Analysis: Providers might choose the EHR's portal to avoid additional software expenses.

Healthcare Communication: The Threat of Substitutes

The threat of substitutes for specialized healthcare communication platforms like Weave arises from readily available, often lower-cost alternatives. These range from basic communication tools to integrated features within existing Electronic Health Record (EHR) systems. Many practices may find that these substitutes adequately meet their needs, thereby limiting the demand for more comprehensive solutions.

For instance, a 2024 report highlighted that over 30% of small medical practices still utilize standard email and personal mobile phones for patient communication, viewing these as sufficient substitutes for dedicated platforms. This demonstrates a clear preference for cost-effectiveness and familiarity over advanced functionality.

Furthermore, the increasing capability of EHR-native patient portals presents a direct substitute. These portals can handle appointment scheduling, secure messaging, and access to medical records, potentially negating the need for a separate communication suite. A study in early 2025 found that 40% of healthcare providers surveyed were considering leveraging their EHR's built-in portal to reduce software costs.

The availability of these substitutes means that companies like Weave must continually innovate and demonstrate superior value. This includes offering enhanced features, better integration, and a more seamless user experience to justify their pricing against more basic or bundled alternatives.

| Substitute Type | Examples | Potential Impact on Weave | 2024 Adoption Trend |

|---|---|---|---|

| Basic Communication Tools | Email, SMS, Phone Calls, Fax | Low-cost alternative for simple communication needs | Stable, with some decline in fax usage |

| Consumer Messaging Apps | WhatsApp, Signal | Free or low-cost, familiar interface for patients and staff | Increasing adoption for non-sensitive communications |

| EHR Native Portals | Built-in patient portals within EHR systems | Integrated functionality, potential cost savings for practices | Growing, as EHRs enhance portal features |

| Custom In-House Solutions | Proprietary software developed internally | Highly tailored, full control over data and features | Niche, but significant for large health systems with IT resources |

Entrants Threaten

High Initial Investment and Development Costs for Healthcare SaaS

The threat of new entrants in the healthcare SaaS market is significantly dampened by the enormous initial investment and development costs. Building a robust platform that meets healthcare's unique demands, including rigorous data security and regulatory compliance like HIPAA, is a massive undertaking. These costs can easily run into the millions of dollars.

Beyond initial development, ongoing expenses for maintaining and upgrading these complex systems are substantial. Companies like Weave face monthly infrastructure and maintenance bills that can range from approximately $9,800 to well over $19,800, creating a high barrier to entry for potential competitors looking to offer similar comprehensive solutions.

Regulatory Hurdles and Compliance Requirements (e.g., HIPAA)

The healthcare industry presents a formidable threat of new entrants due to stringent regulatory landscapes, such as the Health Insurance Portability and Accountability Act (HIPAA) in the United States. These regulations impose significant burdens on data security and patient privacy, requiring substantial investment in compliance infrastructure and expertise.

For instance, the cost of HIPAA compliance for small to medium-sized healthcare providers can range from $5,000 to $50,000 annually, a considerable barrier for new players. Navigating these complex frameworks demands specialized legal and technical knowledge, effectively deterring many potential competitors and raising the cost of market entry significantly.

Need for Integrations with Existing EHR/Practice Management Systems

The threat of new entrants in the healthcare communications platform market is significantly impacted by the critical need for integration with existing Electronic Health Record (EHR) and practice management systems. Newcomers must demonstrate robust compatibility with a wide array of these established platforms to be viable.

Developing and maintaining these essential integrations is a substantial undertaking, demanding considerable technical expertise and strategic alliances with EHR vendors. This complexity acts as a considerable barrier, deterring many potential new entrants who may lack the resources or capabilities to navigate these intricate technical requirements.

Brand Recognition and Established Customer Base

Weave's significant brand recognition and deeply entrenched customer base present a formidable barrier to new entrants. By the close of 2024, Weave had successfully established a presence in nearly 35,000 customer locations, primarily within the small and medium-sized healthcare business sector. This extensive reach translates into a strong sense of loyalty and trust among its existing clients.

New companies entering this market would face the considerable challenge of not only replicating Weave's service offerings but also of building comparable brand awareness and customer confidence from the ground up. Overcoming the established loyalty and the inherent difficulty in gaining trust within a competitive landscape requires substantial investment and strategic differentiation.

- Established Market Share: Weave serves approximately 35,000 customer locations as of the end of 2024, indicating a significant portion of the target market is already captured.

- Brand Loyalty: Existing customers are likely to exhibit loyalty due to satisfaction with Weave's services and established relationships.

- Trust Factor: Healthcare businesses often prioritize reliability and trust, making it difficult for new entrants to displace an incumbent like Weave.

- Customer Acquisition Costs: New entrants would incur high costs to acquire customers, needing to invest heavily in marketing and sales to compete with Weave's brand equity.

Sales and Marketing Challenges to Reach Fragmented SMB Market

The small and medium-sized business (SMB) healthcare market is notoriously fragmented, making it a costly and time-consuming endeavor for any company, especially new entrants, to effectively reach and acquire customers. This inherent market structure presents a substantial barrier.

New players entering the healthcare technology space, particularly those targeting SMBs, would need to overcome significant sales and marketing hurdles to build a recognizable brand and acquire a customer base when competing against established providers like Weave. The cost of customer acquisition in this segment can be particularly high.

- Market Fragmentation: The SMB healthcare sector comprises a vast number of independent practices, making broad market penetration a complex undertaking.

- High Customer Acquisition Costs: Reaching and converting individual small practices often requires substantial investment in sales teams, marketing campaigns, and channel partnerships.

- Established Competition: Incumbents like Weave have already invested heavily in building brand recognition and sales infrastructure, creating a significant advantage for them.

- Sales Cycle Complexity: The sales process for SMB healthcare providers can be lengthy, involving multiple decision-makers and requiring tailored solutions, which adds to the resource intensity for new entrants.

Healthcare Communications: High Barriers to Entry

The threat of new entrants in the healthcare communications platform market is considerably low due to high capital requirements and substantial economies of scale enjoyed by established players like Weave. The initial investment in platform development, regulatory compliance, and sales infrastructure can easily exceed millions of dollars, creating a significant financial hurdle.

Furthermore, the need for seamless integration with a multitude of Electronic Health Record (EHR) systems, a critical factor for adoption, demands ongoing technical expertise and partnerships. This complexity, coupled with the significant brand loyalty and trust built by incumbents, makes it exceptionally difficult for newcomers to gain traction.

By the end of 2024, Weave served approximately 35,000 customer locations, showcasing a dominant market presence. This established share, combined with the high costs associated with customer acquisition in a fragmented SMB healthcare market, further solidifies the barriers to entry for potential competitors.

| Barrier Type | Description | Impact on New Entrants | Example Data (2024) |

|---|---|---|---|

| Capital Requirements | High initial investment for platform development, infrastructure, and sales. | Deters new entrants due to financial risk. | Millions of dollars for robust healthcare SaaS development. |

| Integration Complexity | Need for compatibility with numerous EHR and practice management systems. | Requires specialized technical skills and vendor relationships. | Developing and maintaining EHR integrations is resource-intensive. |

| Brand Recognition & Loyalty | Established trust and customer relationships with incumbents. | Difficult for new entrants to displace existing providers. | Weave's 35,000+ customer locations indicate strong market penetration. |

| Market Fragmentation & CAC | Reaching and acquiring customers in the dispersed SMB healthcare sector is costly. | High customer acquisition costs for new players. | Significant investment in sales and marketing needed to compete. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis is built upon a foundation of robust data, including company annual reports, industry-specific market research, and publicly available financial filings. We also leverage insights from trade associations and economic databases to capture a comprehensive view of the competitive landscape.