Deliveroo Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GET THE FULL COMPANY

ANALYSIS BUNDLE FOR

Deliveroo

Go Beyond the Preview—Access the Full Strategic Report

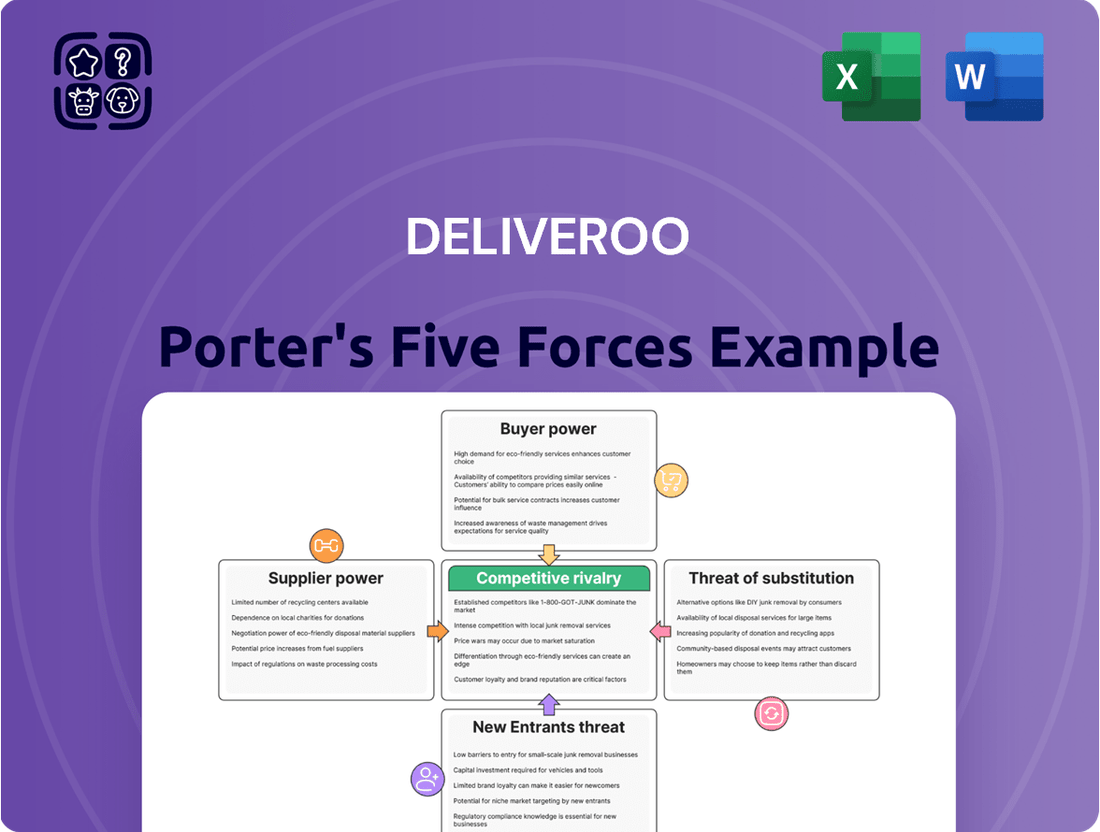

Deliveroo navigates a fiercely competitive food delivery landscape, where the bargaining power of both restaurants and customers can significantly impact profitability. The threat of new entrants looms large, as the low barriers to entry in the gig economy can quickly introduce new players. Intense rivalry among existing platforms, including Uber Eats and Just Eat, further squeezes margins and demands constant innovation.

The availability of substitutes, such as direct restaurant delivery or meal kit services, also exerts pressure on Deliveroo's market share. Furthermore, the power of suppliers – the riders themselves – presents a unique challenge, with potential for labor disputes and wage demands. Understanding these forces is crucial for any stakeholder looking to grasp Deliveroo's strategic position.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Deliveroo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Restaurant Partners

The bargaining power of restaurants with Deliveroo is a significant factor, generally considered moderate to high, especially for well-known or exclusive eateries. Deliveroo's vast network, which includes around 186,000 restaurant, grocery, and retail partners, means that while many are reliant on the platform, the truly popular ones can exert considerable influence.

These coveted brands understand their drawing power. They can use this to their advantage, negotiating more favorable commission rates or better operational terms with Deliveroo. This competition among delivery platforms for exclusive partnerships highlights the leverage these popular restaurants possess, directly impacting Deliveroo's profitability and operational costs.

Independent Couriers (Riders)

The bargaining power of Deliveroo's independent couriers, or riders, is best described as moderate. This is primarily because their leverage is directly tied to the demand for delivery services and the availability of competing platforms where they can offer their services.

When demand for food delivery surges, or if there's a scarcity of riders in specific geographic locations or during peak operational hours, these riders gain more influence. Deliveroo, which utilizes a vast network of approximately 135,000 riders worldwide, depends heavily on this workforce to maintain its service quality and ensure prompt deliveries.

Technology Providers

The bargaining power of generic technology providers, like those offering cloud services or mapping APIs, tends to be low for Deliveroo. This is because these services are often commoditized, meaning many companies offer similar solutions, and Deliveroo can easily switch between them. For instance, major cloud providers like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform compete fiercely on price and features, limiting the leverage of any single provider.

However, this dynamic can shift if a technology provider offers highly specialized software or unique data analytics capabilities that are critical to Deliveroo's operations. In such cases, a provider with a proprietary solution or a deep understanding of Deliveroo's specific needs could exert more influence. This is especially true for innovative AI-driven logistics or customer analytics platforms that are not easily replicated.

Payment Processors

The bargaining power of payment processors for Deliveroo is generally considered moderate. These companies are crucial for processing customer payments and ensuring secure, timely transactions, giving them a degree of influence. The reliance on established, scalable, and secure payment infrastructure makes switching to a new provider a complex and potentially costly undertaking, reinforcing the processors' leverage.

Several prominent payment gateways offer services to online platforms like Deliveroo. While competition exists, the specialized nature of the services and the integration required mean that providers can negotiate terms that reflect their value and the ongoing operational necessity for Deliveroo. For instance, in 2024, major payment processors continued to see increased transaction volumes driven by the growth of the digital economy, which can strengthen their negotiating position.

- Dependence on Efficiency: Deliveroo relies heavily on payment processors for seamless customer transactions, a critical component of its service delivery.

- Switching Costs: The technical and operational hurdles involved in changing payment providers can be significant, limiting Deliveroo's ability to switch easily.

- Provider Leverage: Due to the essential nature of their services and integration complexities, payment processors can exert moderate bargaining power in fee structures and terms.

- Market Dynamics: The ongoing growth in online payments in 2024 means processors are in a strong position to negotiate, especially with platforms requiring high transaction volumes and robust security.

Grocery and Retail Partners

Deliveroo's expansion into grocery and non-food retail delivery significantly increases the bargaining power of these partners. Major grocery chains, with their broad product selection and established customer loyalty, can negotiate more advantageous terms, directly impacting Deliveroo's revenue streams from this growing segment.

For instance, in 2023, Deliveroo reported that its grocery and other verticals accounted for 30% of its gross transaction value (GTV), highlighting the increasing reliance on these partnerships. This trend is expected to continue as Deliveroo aims to further diversify its offerings beyond restaurant food.

- Increased Leverage: Large supermarket chains can leverage their significant order volumes and customer reach to demand better commission rates or marketing support from Deliveroo.

- Exclusive Agreements: Retailers offering exclusive product ranges through Deliveroo can use this exclusivity as a bargaining chip for more favorable contract terms.

- Operational Dependence: As Deliveroo becomes more reliant on these partnerships for GTV growth, the suppliers' ability to influence pricing and service level agreements strengthens.

- Market Competition: The competitive landscape for grocery delivery services means that key retail partners have options, further enhancing their bargaining power.

Supplier Power: The Driving Force in Delivery Negotiations

The bargaining power of suppliers, specifically restaurants and grocery partners, is a key consideration for Deliveroo. For restaurants, particularly popular ones, this power is moderate to high, as demonstrated by their ability to negotiate terms due to their drawing power on the platform. This is further amplified by Deliveroo's expansion into grocery and retail, where major chains can leverage their substantial order volumes and customer reach for more favorable contracts.

In 2023, grocery and other verticals represented 30% of Deliveroo's gross transaction value, underscoring the growing importance of these partnerships and the increased leverage these suppliers hold. This reliance means that key retail partners possess options, enhancing their ability to influence pricing and service level agreements.

| Supplier Type | Deliveroo Partner Count (Approx.) | Bargaining Power Level | Key Influencing Factors |

|---|---|---|---|

| Restaurants | 186,000 (total partners) | Moderate to High | Brand recognition, exclusivity, customer demand |

| Grocery & Retail | Significant portion of 186,000 partners | Moderate to High | Order volume, customer loyalty, product selection, competition |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Deliveroo's platform and operational model.

Instantly gauge competitive intensity by visualizing the bargaining power of suppliers and buyers, and the threat of substitutes, streamlining strategic planning.

Customers Bargaining Power

Low Switching Costs

Customers can easily switch between Deliveroo and its competitors, such as Uber Eats and Just Eat, with minimal effort. This low switching cost is a significant factor in their bargaining power.

The ability to compare prices, restaurant options, and delivery speeds across multiple apps empowers consumers. For instance, in 2024, the food delivery market saw intense competition, with platforms frequently offering promotions and discounts to attract and retain users, further highlighting the low switching costs.

This ease of transition means customers can readily shift their business to the platform offering the best value at any given time, putting pressure on Deliveroo to maintain competitive pricing and service quality.

Price Sensitivity

Customers are definitely a key factor for Deliveroo, and their sensitivity to price plays a big role. Many consumers are quite aware of how much they're paying, especially for things like delivery fees and any service charges added on. This means Deliveroo has to be smart about its pricing to stay competitive.

A recent survey from 2025 really highlighted this, showing that a large portion of customers actively look for discounts when picking a food delivery app. This directly impacts Deliveroo's strategy, pushing them to offer more promotions and deals to attract and keep users. It's a clear sign that price is a major driver in customer choice.

Access to Information

Customers today have an unprecedented amount of information at their fingertips. Reviews, ratings, and detailed menu information for countless restaurants are readily available on platforms like Deliveroo itself, Google, and Yelp. This transparency significantly reduces the information gap between the customer and the service provider, allowing diners to easily compare options.

For instance, in the UK, online reviews heavily influence dining choices, with studies showing a substantial percentage of consumers consulting them before ordering. This easy access to comparative pricing and quality assessments directly strengthens their ability to negotiate or simply choose the best value, thereby increasing their bargaining power with food delivery services like Deliveroo.

Availability of Alternatives

Customers possess significant bargaining power due to the sheer availability of alternatives to Deliveroo. They can easily switch to rival food delivery apps like Uber Eats or Just Eat, or opt for direct ordering from restaurants. Even traditional dining out remains a viable and often preferred choice for many.

This abundance of options directly translates into increased leverage for consumers. They can readily compare prices, delivery times, and restaurant selections across different platforms, forcing Deliveroo to remain competitive. In 2024, the food delivery market remains intensely crowded, with numerous players vying for market share, further amplifying customer choice.

- High Availability of Competitors: The presence of multiple food delivery aggregators and direct restaurant ordering channels provides customers with a wide array of choices.

- Price Sensitivity: Customers frequently compare prices and promotions across platforms, influencing their decision-making and pressuring Deliveroo on pricing.

- Convenience vs. Cost Trade-off: While convenience is a driver, customers will readily trade it for cost savings if alternatives offer a better value proposition.

- Restaurant Independence: Restaurants can choose to partner with multiple platforms or focus on their own direct delivery, reducing reliance on any single aggregator like Deliveroo.

Subscription Models

Subscription models, such as Deliveroo Plus, are designed to foster customer loyalty by offering perks like free delivery. However, customers retain significant bargaining power because their decision to subscribe hinges entirely on the perceived value and savings compared to per-order fees. This creates a dynamic where Deliveroo seeks to secure predictable revenue streams while customers weigh the subscription cost against their expected usage and the tangible benefits provided.

- Customer Choice: Despite subscription benefits, customers can opt out if they find the service no longer offers sufficient value, directly impacting Deliveroo's recurring revenue.

- Price Sensitivity: The willingness of customers to subscribe is directly tied to their perception of cost savings and the overall convenience offered by the subscription versus paying for each delivery.

- Competitive Offers: Customers can switch to rival platforms or services if they perceive better value, thereby limiting the pricing power of Deliveroo's subscription programs.

Customers Drive Food Delivery Competition

Customers wield considerable power in the food delivery market, largely due to the ease with which they can switch between providers. This low switching cost means Deliveroo must constantly compete on price, service, and restaurant selection to retain its user base.

In 2024, the food delivery landscape remained highly competitive, with platforms frequently employing promotions and discounts to attract and keep customers. This environment directly amplifies customer bargaining power, as consumers can readily shift to whichever service offers the most appealing deal at any given moment.

The extensive availability of information, including restaurant reviews and price comparisons across multiple apps, further empowers customers. This transparency allows them to make informed decisions, often prioritizing cost-effectiveness and value, which puts pressure on Deliveroo to maintain competitive pricing and service standards.

| Factor | Impact on Deliveroo | Customer Action |

|---|---|---|

| Low Switching Costs | Reduces customer loyalty, increases price sensitivity | Easily move between Deliveroo, Uber Eats, Just Eat |

| Price Sensitivity | Limits Deliveroo's pricing power, necessitates promotions | Actively seek discounts and compare prices |

| Information Availability | Empowers customers to compare offerings | Utilize reviews and ratings to choose best value |

Preview the Actual Deliverable

Deliveroo Porter's Five Forces Analysis

This preview showcases the complete Deliveroo Porter's Five Forces Analysis, offering a thorough examination of competitive forces within the food delivery market. The document you see here is precisely what you will receive immediately after purchase, ensuring no discrepancies or missing information. It delves into the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitutes, and the intensity of rivalry among existing competitors. This professionally formatted analysis is ready for your immediate use, providing actionable insights into Deliveroo's strategic landscape.

Rivalry Among Competitors

Intense Competition from Major Players

The online food delivery landscape is fiercely competitive, with giants like Uber Eats, Just Eat Takeaway.com, and DoorDash constantly battling for dominance. These well-funded companies engage in aggressive marketing campaigns and price wars to win over customers and restaurants. For instance, in 2023, DoorDash's revenue reached $8.3 billion, showcasing the scale of investment in this sector.

Low Product Differentiation

The fundamental service of food delivery is inherently similar across various platforms, making it difficult for companies like Deliveroo to truly differentiate themselves. This limited product differentiation means competition often boils down to factors like the breadth of restaurant choices available, how quickly food arrives, and the cost to the consumer.

This lack of distinctiveness intensifies the rivalry among food delivery services. For instance, in 2024, the market continues to see intense price wars and promotions as companies attempt to attract and retain customers in a highly competitive landscape. Deliveroo, along with its rivals, must constantly innovate on secondary features or operational efficiencies to carve out a unique selling proposition.

Aggressive Pricing and Promotions

Competitors in the food delivery market, like Just Eat Takeaway and Uber Eats, often engage in aggressive pricing strategies. This includes frequent discounts, free delivery offers, and attractive loyalty programs designed to capture market share and retain customers. For instance, many platforms in 2024 continued to heavily subsidize delivery fees, impacting overall profitability across the sector.

These price wars directly pressure Deliveroo's profit margins. Despite the company's focus on operational efficiencies and premium service offerings, the need to remain competitive in pricing can erode profitability. The constant battle for customer acquisition through promotional pricing makes it challenging for Deliveroo to maintain healthy margins, especially as operational costs remain significant.

Market Share Dynamics

Competitive rivalry is intense in the food delivery sector, directly impacting Deliveroo's market share. While Deliveroo maintains a strong presence in its key markets, its share is not static. It is constantly influenced by the strategies of rivals and shifts in what customers want.

In 2024, Deliveroo's market share in the crucial UK market stood at 16.2%. This places it behind major competitors like Uber Eats and other delivery platforms that operate their own fleets. This dynamic suggests a highly competitive landscape where gaining and retaining market share requires continuous innovation and strategic maneuvering.

- UK Market Share (2024): Deliveroo at 16.2%.

- Key Competitors: Uber Eats, company-owned delivery platforms.

- Market Dynamics: Fluctuations driven by competitor actions and consumer preferences.

- Implication: High rivalry necessitates constant strategic adaptation.

Expansion into New Verticals

Competitive rivalry in the food delivery sector is intensifying as companies like Deliveroo broaden their horizons beyond traditional restaurant meals. They are actively expanding into grocery and other retail deliveries, a move that significantly escalates competition. This diversification means that once distinct market segments are now overlapping, forcing established players to contend with rivals entering their newly defined territories.

Deliveroo's own strategic push into grocery delivery exemplifies this trend. By offering supermarket items, Deliveroo directly competes with dedicated grocery delivery platforms and even traditional supermarkets that might develop their own rapid delivery services. This strategic expansion blurs industry lines, creating a more crowded and dynamic competitive landscape where companies are constantly seeking new avenues for growth and market share.

- Diversification into Grocery: Deliveroo's expansion into grocery delivery, mirroring moves by competitors like Uber Eats and DoorDash, intensifies rivalry by entering a new, lucrative market segment.

- Increased Overlap: As delivery platforms diversify, the overlap in services increases, meaning companies are no longer just competing on restaurant delivery but also on convenience for groceries and other retail items.

- Heightened Competition: This multi-vertical competition forces all players to innovate and optimize across a broader range of services, potentially leading to price wars and a greater focus on customer retention.

Online Food Delivery: Intense Rivalry Heats Up

The competitive rivalry within the online food delivery sector is exceptionally high, with major players like Uber Eats and Just Eat Takeaway.com consistently vying for market share. This intense competition manifests through aggressive pricing, extensive marketing, and a continuous drive for operational efficiency. Deliveroo, operating within this dynamic environment, faces constant pressure to innovate and maintain its customer base amidst these powerful rivals.

| Competitor | 2023 Revenue (USD Billion) | 2024 UK Market Share (%) |

|---|---|---|

| Deliveroo | N/A (Reported in Euros) | 16.2% |

| Uber Eats | N/A (Part of Uber's broader reporting) | Significantly higher than Deliveroo |

| Just Eat Takeaway.com | €5.5 Billion (2023) | Significant market presence |

SSubstitutes Threaten

Traditional Restaurant Dining

Traditional restaurant dining remains a significant substitute for online food delivery services like Deliveroo. This in-person experience offers a unique social and sensory value that delivery simply cannot replicate, from the ambiance to immediate service. Following pandemic-related restrictions, a notable segment of consumers has returned to dining out, reinforcing its presence as a competitive alternative. For instance, in the UK, while food delivery surged, restaurant dine-in revenue in 2023 continued to represent a substantial portion of the overall hospitality market, demonstrating enduring consumer preference for the traditional model.

Cooking at Home

The threat of substitutes for Deliveroo's services is significant, with preparing meals at home posing a direct and often more cost-effective alternative. This option is particularly appealing to consumers who are highly price-sensitive or those who have specific health requirements and dietary preferences that are easier to manage when cooking their own food. In 2024, the rising cost of living globally has likely amplified this trend, with many households actively seeking ways to reduce discretionary spending.

In the UK, for instance, consumer spending on takeaway and delivery services, while substantial, faces increasing scrutiny as households manage budgets. Data from early 2024 indicated a continued interest in home cooking, driven by both economic pressures and a desire for greater control over ingredients and nutrition. This inclination directly diverts potential revenue away from food delivery platforms like Deliveroo.

Direct Restaurant Takeaway/Pickup

Customers have a strong alternative in directly ordering takeaway or pickup from restaurants, bypassing delivery platforms like Deliveroo altogether. This direct channel eliminates delivery fees for consumers and allows restaurants to keep more of their revenue, making it a compelling substitute. For instance, many quick-service restaurants (QSRs) have robust online ordering systems for pickup, directly competing for customer loyalty without incurring third-party commissions.

Meal Kit Delivery Services

Meal kit delivery services represent a significant threat of substitutes for Deliveroo, offering a different approach to convenient meal solutions. Companies like HelloFresh provide pre-portioned ingredients and recipes, catering to consumers who want to cook at home but prefer to skip the planning and shopping stages. This segment of the food industry is experiencing robust growth, with the global meal kit delivery service market expected to reach approximately $20 billion by 2027, indicating a strong and expanding alternative for consumers.

- Convenience Factor: Meal kits offer a curated cooking experience, reducing decision fatigue and preparation time for busy individuals.

- Market Growth: The meal kit industry is expanding, with significant projected growth signaling increasing consumer adoption of this substitute.

- Target Audience Overlap: Both meal kit services and Deliveroo appeal to consumers seeking convenient meal options, creating direct competition for disposable income and mealtime occasions.

- Cost-Effectiveness Perception: While initial costs can seem high, some consumers perceive meal kits as cost-effective due to reduced food waste and the elimination of impulse grocery purchases.

Grocery Delivery Services

The threat of substitutes for Deliveroo's core food delivery business is significant, primarily stemming from the increasing availability and popularity of grocery delivery services. These platforms allow consumers to order ingredients directly for home cooking, bypassing the need for restaurant meals. This presents an indirect but powerful substitute, fulfilling the fundamental need for food consumption at home with growing convenience.

The landscape of grocery delivery has evolved dramatically. Many traditional supermarkets now offer their own dedicated online ordering and delivery options, directly competing with third-party platforms. Furthermore, specialized online grocery retailers and even meal kit services cater to consumers looking for at-home food solutions. For instance, in the UK, online grocery sales saw substantial growth, with major players like Tesco and Sainsbury's investing heavily in their delivery infrastructure. By 2024, the online grocery market in the UK was projected to reach over £20 billion, highlighting the scale of this substitute threat.

- Supermarket Own Delivery: Major grocers like Ocado (which partners with Marks & Spencer in the UK) and Amazon Fresh offer rapid grocery delivery, directly competing for at-home meal occasions.

- Meal Kit Services: Companies such as HelloFresh and Gousto provide pre-portioned ingredients and recipes, simplifying home cooking and offering an alternative to restaurant delivery.

- Convenience Stores with Delivery: Some convenience chains are also expanding delivery options, serving immediate needs that might otherwise be met by quick-service restaurant delivery.

- Increased Home Cooking Trend: Post-pandemic, there has been a sustained interest in home cooking, further bolstering the appeal of grocery delivery as a substitute for restaurant takeout.

Rising Alternatives: Home Cooking & Direct Pickup Threaten Delivery

The threat of substitutes for Deliveroo is considerable, with direct restaurant takeaway and home cooking representing strong alternatives. Consumers increasingly opt for pickup to avoid delivery fees, and the rising cost of living in 2024 encourages more home preparation.

Meal kit services also present a significant substitute, offering convenience for home cooking. For example, the global meal kit market is projected to reach around $20 billion by 2027, indicating robust consumer adoption of this alternative.

Furthermore, grocery delivery services are gaining traction, enabling consumers to prepare meals at home more easily. In the UK, online grocery sales exceeded £20 billion in 2024, underscoring the growing appeal of at-home food solutions over restaurant delivery.

| Substitute Category | Key Features | Impact on Deliveroo |

|---|---|---|

| Restaurant Dine-In | Social experience, ambiance, immediate service | Directly competes for dining occasions, especially post-pandemic recovery. |

| Home Cooking | Cost-effectiveness, health control, ingredient customization | Amplified by economic pressures in 2024, reducing discretionary spending on delivery. |

| Direct Restaurant Takeaway/Pickup | No delivery fees for consumers, higher margins for restaurants | Bypasses third-party platforms, diverting revenue and customer loyalty. |

| Meal Kit Delivery Services | Convenience, reduced food waste, simplified planning | Growing market ($20 billion by 2027 projection) appeals to similar convenience-seeking consumers. |

| Grocery Delivery Services | Enables home cooking, wider selection of ingredients | Significant growth (UK market >£20 billion in 2024) offers a fundamental food solution at home. |

Entrants Threaten

High Capital Requirements

New companies looking to break into the food delivery market face substantial financial hurdles. They need to invest heavily in creating sophisticated technology platforms, which are crucial for managing orders, logistics, and customer experience. For instance, developing a user-friendly app and a reliable backend system requires millions in upfront investment.

Building a reliable network of delivery riders is another significant cost. This involves recruiting, onboarding, and potentially providing equipment or insurance for couriers, all of which adds to the initial capital outlay. Companies like Deliveroo have already established large, efficient networks, making it challenging for newcomers to match their reach and speed without considerable funding.

Furthermore, aggressive marketing and customer acquisition campaigns are essential to gain market share. New entrants must spend heavily on advertising, promotions, and discounts to attract both customers and restaurants. In 2024, the cost of acquiring a new customer in the online food delivery sector often exceeded $50, a figure that can quickly escalate for businesses without deep pockets.

These high capital requirements act as a strong deterrent, effectively limiting the number of viable new competitors that can challenge established players like Deliveroo. The sheer scale of investment needed to build a comparable service makes it a difficult market for startups to enter and succeed.

Strong Brand Recognition and Network Effects

Deliveroo, like many in the food delivery sector, benefits from strong brand recognition. In 2024, customer trust remains paramount, making it challenging for newcomers to gain traction. This is compounded by powerful network effects: a larger restaurant selection draws more customers, and a larger customer base attracts more delivery riders, creating a virtuous cycle that new entrants find difficult to break into without significant investment and time.

Regulatory and Legal Complexities

The food delivery sector is grappling with increasingly complex regulations, especially concerning the classification of gig economy workers and the acquisition of local operating permits. For instance, in 2024, several European countries continued to debate and implement new rules impacting worker status, which can significantly alter operational costs and business models for any new entrant.

These evolving legal frameworks act as a substantial hurdle for nascent companies aiming to enter the market. Understanding and complying with varying national and regional laws, from labor rights to food safety standards, requires considerable legal expertise and financial investment, effectively raising the barrier to entry.

Operational Complexity and Logistics

The operational complexity of building and managing an efficient logistics network presents a significant barrier for new entrants. This includes developing sophisticated systems for real-time tracking, advanced route optimization algorithms, and the substantial undertaking of managing a large, dynamic fleet of couriers. For instance, companies like Deliveroo invest heavily in technology to ensure swift and reliable deliveries, a costly endeavor for startups.

New entrants must therefore overcome substantial logistical hurdles to even approach competitive service levels. The intricate coordination required to manage fluctuating demand, courier availability, and delivery times necessitates significant technological investment and operational expertise. Without this, a new player would struggle to offer the speed and reliability customers expect.

- High Capital Investment in Technology: Significant upfront costs are required for sophisticated logistics software, tracking systems, and data analytics platforms.

- Complex Fleet Management: Effectively managing a large, dispersed fleet of independent contractors or employees, including onboarding, training, and performance monitoring, is a major challenge.

- Route Optimization Expertise: Developing and maintaining efficient routing systems that adapt to real-time traffic and order volume requires specialized data science and engineering capabilities.

Established Restaurant Partnerships

Deliveroo and its competitors have built strong, often exclusive, ties with a vast number of restaurants. These established partnerships make it difficult for new food delivery services to quickly assemble an attractive and comprehensive restaurant selection, a crucial element for drawing in customers.

New entrants face a significant hurdle in replicating the extensive network of restaurants that incumbent players like Deliveroo have cultivated. For instance, in 2024, over 80% of major restaurant chains in key European markets had existing agreements with at least one major delivery platform.

Securing a comparable range of popular eateries is essential for a new service to gain traction. Without a robust and appealing restaurant offering, attracting a critical mass of users becomes an uphill battle.

- Established Restaurant Relationships: Deliveroo's deep integration with a wide variety of restaurants, including exclusive deals, presents a high barrier for newcomers.

- Limited Restaurant Selection for Entrants: New platforms struggle to onboard enough desirable restaurants to compete effectively, impacting customer acquisition.

- Customer Acquisition Challenge: A weak restaurant portfolio directly hinders a new entrant's ability to attract and retain a significant user base in 2024.

- Competitive Advantage: Incumbents leverage their existing restaurant networks as a key differentiator, making it harder for new players to gain market share.

Food Delivery Market: A Fortress for New Entrants

The threat of new entrants into the food delivery market, like the one Deliveroo operates in, remains moderate but significant. While the initial capital investment for technology platforms and building a rider network is substantial, the established players have already overcome these hurdles. For instance, in 2024, the cost of developing a robust delivery app and logistics system could easily run into the millions of dollars, creating a significant barrier for startups. Furthermore, the need for aggressive marketing to acquire both customers and restaurants adds another layer of financial strain. Reports from 2024 indicated that the customer acquisition cost in this sector could exceed $50 per user, a figure that demands deep pockets.

Established brands also hold considerable sway, making it hard for newcomers to gain trust. Network effects, where more restaurants attract more customers and vice versa, create a powerful advantage for incumbents like Deliveroo. In 2024, this cycle made it particularly difficult for new entrants to gain traction without substantial funding and time. Moreover, the increasing regulatory landscape, especially concerning gig economy workers and permits, adds complexity and cost, further deterring new players from entering the competitive food delivery arena.

The challenge for new entrants is amplified by the strong, often exclusive, relationships Deliveroo and its competitors have with restaurants. In 2024, over 80% of major restaurant chains in key European markets had existing agreements with major delivery platforms, making it difficult for newcomers to secure a competitive restaurant selection. This limited portfolio directly hinders a new entrant's ability to attract and retain a significant user base, a critical factor for success in the fast-paced food delivery market.

| Barrier Type | Description | 2024 Impact/Example |

|---|---|---|

| Capital Requirements | High upfront investment in technology and logistics. | Developing a sophisticated app and backend system can cost millions. |

| Brand Loyalty & Network Effects | Customer trust and the virtuous cycle of more restaurants/customers. | Difficult for new players to break into established user bases and restaurant partnerships. |

| Restaurant Partnerships | Exclusive deals and extensive restaurant networks of incumbents. | Over 80% of major restaurant chains had existing agreements in key European markets in 2024. |

| Regulatory Hurdles | Evolving laws on gig workers and operating permits. | New rules in several European countries in 2024 increased compliance costs for delivery platforms. |

Porter's Five Forces Analysis Data Sources

Our Deliveroo Porter's Five Forces analysis is built upon a foundation of comprehensive data, including company financial reports, investor presentations, and market research from reputable firms. We also leverage industry news, competitor analyses, and regulatory filings to provide a nuanced understanding of the competitive landscape.