BlackRock Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

BlackRock Bundle

A Must-Have Tool for Decision-Makers

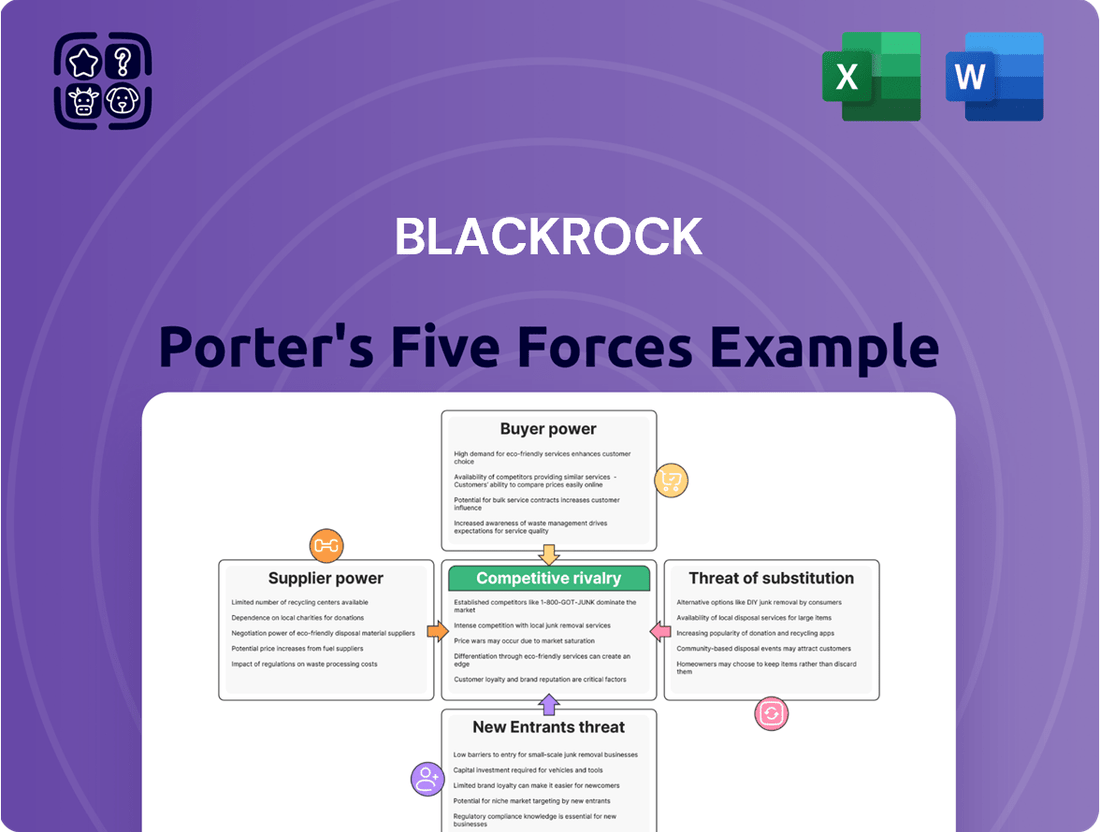

BlackRock, a titan in asset management, faces a complex competitive landscape shaped by five key forces. Understanding the intensity of rivalry among existing competitors, the bargaining power of buyers and suppliers, and the threats of new entrants and substitutes is crucial for navigating this dynamic market.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore BlackRock’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Power 1

BlackRock's reliance on critical data providers like Bloomberg Terminal, which commands a substantial 78% market share in financial data services, indicates a considerable bargaining power for these suppliers. The sheer volume of BlackRock's annual expenditure on these essential services underscores their importance to the firm's operational efficiency and market intelligence gathering.

Supplier Power 2

BlackRock's reliance on cloud computing services, particularly from dominant providers like Amazon Web Services (AWS), significantly amplifies supplier power. AWS alone accounts for an impressive 62% of BlackRock's cloud infrastructure, underscoring a substantial dependency. These multi-year agreements and the sheer scale of BlackRock's cloud expenditures mean these few technology providers wield considerable influence.

Supplier Power 3

BlackRock's reliance on specialized research technology vendors, despite significant in-house software development, grants these suppliers a degree of bargaining power. While BlackRock invested $672 million in in-house software development in 2023, reducing external dependency by 34%, the unique nature of certain data and analytics means these external providers can exert influence.

Supplier Power 4

The bargaining power of suppliers for BlackRock is significantly influenced by the demand for specialized human capital, particularly in areas like investment management and fintech. Highly skilled financial professionals and technology experts are crucial, and their scarcity can grant them considerable leverage. Recruitment firms specializing in these niche areas can also exert influence.

BlackRock's substantial investments in technology and talent underscore the importance of these suppliers. For instance, in 2023, the company continued to invest heavily in its Aladdin platform, a key technological asset, and actively sought to attract and retain top-tier talent to drive innovation and manage complex portfolios. This focus indicates an awareness of the competitive landscape for skilled personnel.

- Human Capital as a Critical Supplier: BlackRock relies heavily on the expertise of financial professionals and technology specialists, making them key suppliers.

- Talent Scarcity Drives Power: High demand for niche skills in investment management and fintech empowers individuals and specialized recruitment firms.

- Investment Reflects Supplier Importance: BlackRock's significant spending on technology and talent acquisition highlights the strategic value of these suppliers.

- Competitive Talent Market: The ongoing competition for top talent means suppliers can negotiate favorable terms, impacting BlackRock's operational costs and innovation capacity.

Supplier Power 5

BlackRock's bargaining power with suppliers is influenced by its scale and strategic acquisitions. Recent moves, like the acquisition of Global Infrastructure Partners (GIP) for $12.5 billion and the planned acquisition of HPS Investment Partners and Preqin, are designed to bolster its private markets and data analytics capabilities. These investments aim to internalize functions previously reliant on external providers, thereby strengthening BlackRock's negotiating leverage by reducing dependency.

By bringing more expertise and data in-house, BlackRock can potentially negotiate more favorable terms with remaining external suppliers. This strategic shift not only enhances operational efficiency but also positions BlackRock to exert greater control over its cost structures and service providers.

- Acquisitions Enhance Internal Capabilities: GIP, HPS, and Preqin acquisitions aim to reduce reliance on external data and investment service providers.

- Strengthened Negotiating Position: Internalizing functions allows BlackRock to negotiate better terms with remaining suppliers.

- Reduced Dependency: The strategic moves signal a move towards greater self-sufficiency, diminishing supplier leverage.

BlackRock's Tech Reliance: Supplier Power Dynamics

BlackRock's dependence on key technology providers, like those offering essential cloud infrastructure, presents a significant avenue for supplier bargaining power. With providers such as Amazon Web Services (AWS) holding a substantial portion of BlackRock's cloud needs, these suppliers can leverage their market position. This reliance is further amplified by the long-term nature of these contracts and the sheer volume of services BlackRock consumes.

| Supplier Category | Key Providers | BlackRock Dependency Indicator | Impact on Supplier Power |

|---|---|---|---|

| Data Services | Bloomberg Terminal | 78% Market Share | High |

| Cloud Infrastructure | AWS | 62% of Cloud Infrastructure | High |

| Specialized Tech | Niche Research Platforms | Essential for unique analytics | Moderate |

| Human Capital | Top Financial & Tech Talent | High demand, scarcity | High |

What is included in the product

This analysis evaluates the competitive intensity and attractiveness of the asset management industry for BlackRock, detailing the impact of rivals, buyer power, supplier leverage, new entrants, and substitutes.

Quickly identify and mitigate competitive threats with a visual breakdown of industry power dynamics.

Customers Bargaining Power

Customer Power 1

BlackRock's customer base is incredibly varied, encompassing both massive institutional investors and individual retail clients. As of 2024, institutional investors represented a substantial 76% of BlackRock's total Assets Under Management (AUM). This significant concentration of assets under management by large entities gives these customers considerable sway.

The bargaining power of BlackRock's customers is notably influenced by the size of their investments. For instance, the top 10 institutional clients alone contribute around 22% of BlackRock's total revenue. This substantial financial contribution means these major players can negotiate for better terms, lower fees, or more customized services, directly impacting BlackRock's profitability.

Customer Power 2

BlackRock faces significant bargaining power from its customers, largely due to the sheer number of alternative asset managers available. Giants like Vanguard, State Street, and Fidelity offer comparable services, giving clients a robust selection. This competitive landscape means customers can readily switch if they feel they are not receiving optimal value or terms, amplifying their leverage.

Customer Power 3

BlackRock's formidable brand recognition and its vast array of investment products, from ETFs to alternative investments, serve as significant deterrents against customer power. The company's integrated technology platform, Aladdin, further solidifies client relationships by offering sophisticated, all-encompassing solutions that are difficult to replicate elsewhere.

Clients with complex investment needs are less likely to switch providers when BlackRock's comprehensive suite of services effectively addresses their requirements. This loyalty, fostered by unique value propositions and integrated platforms, naturally diminishes the bargaining leverage of individual or institutional customers.

In 2023, BlackRock reported total assets under management (AUM) of $9.08 trillion, showcasing the immense scale and client commitment that underpins its ability to manage customer power. This sheer size and the breadth of services offered make switching costly and complex for many clients.

Customer Power 4

Customers wield significant power, particularly evident in the ongoing fee compression across the asset management industry. This pressure is especially pronounced in the exchange-traded fund (ETF) market, where both retail and institutional investors are highly attuned to costs. BlackRock has responded by strategically lowering fees in rapidly expanding segments, betting on increased volume to compensate for reduced per-unit revenue. For instance, in 2023, BlackRock saw continued inflows into its lower-cost iShares ETFs, underscoring client demand for fee-sensitive products.

This customer power translates into a constant need for BlackRock to innovate and justify its value proposition beyond just price. The ability of investors to easily switch between providers, especially with the proliferation of low-cost passive investment options, means BlackRock must continually demonstrate superior performance, exceptional service, or unique product offerings to retain and attract assets.

- Fee Compression: Retail and institutional investors are increasingly prioritizing lower fees, impacting profitability in areas like ETFs.

- Price Sensitivity: BlackRock's strategy involves targeted price reductions in high-growth, price-sensitive categories.

- Volume Offset: The aim is to compensate for lower fees through a significant increase in assets under management and trading volume.

- Competitive Landscape: The ease with which clients can move assets necessitates continuous value demonstration by BlackRock.

Customer Power 5

The bargaining power of customers in the asset management industry, particularly for a firm like BlackRock, is influenced by the increasing demand for sophisticated investment vehicles. Clients are actively seeking out private markets and systematic strategies, as BlackRock's Q1 and Q2 2025 earnings reports indicate a strong inflow into these areas, demonstrating a clear client preference for diversification and potentially higher returns. This shift means clients have more options and can exert pressure on providers to deliver specialized products and competitive fees.

BlackRock's capacity to meet these evolving client needs, including its exploration and integration of digital assets, directly impacts customer stickiness. By offering a comprehensive suite of products that align with current market trends, BlackRock can mitigate the inherent power customers hold. For instance, if clients perceive a lack of innovation or tailored solutions, they are more likely to explore alternative asset managers, thereby increasing their bargaining leverage.

- Client Diversification: Investors are increasingly looking beyond traditional equities and bonds, driving demand for private equity, private credit, and real estate, areas where BlackRock has been actively expanding its offerings.

- Fee Sensitivity: While seeking alpha, clients remain cost-conscious, especially in a competitive landscape where lower-cost passive strategies are readily available.

- Information Asymmetry Reduction: Greater access to market data and research empowers clients to make more informed decisions and negotiate more effectively.

- Technological Integration: BlackRock's ability to leverage technology for client reporting, portfolio management, and access to new asset classes like digital assets can enhance client loyalty and reduce their inclination to switch providers.

Client Power Shapes Asset Management

Customers hold substantial power over BlackRock, primarily driven by the availability of numerous alternative asset managers and the industry-wide trend of fee compression, especially in the ETF market. As of 2024, institutional investors, representing 76% of BlackRock's AUM, can leverage their significant investment size, with the top 10 clients alone contributing around 22% of revenue, to negotiate better terms. BlackRock's ability to retain clients and mitigate this power hinges on its broad product offering, technological integration like Aladdin, and responsiveness to evolving client demands for sophisticated and cost-effective investment solutions.

| Factor | Description | Impact on BlackRock |

|---|---|---|

| Customer Concentration | Large institutional investors manage a significant portion of BlackRock's AUM. | Increases their bargaining power, allowing for fee negotiation and demand for customized services. |

| Availability of Alternatives | Numerous competitors offer similar asset management services. | Facilitates client switching, forcing BlackRock to remain competitive on fees and service quality. |

| Fee Sensitivity | Clients, particularly in the ETF market, are highly focused on minimizing costs. | Drives fee reductions by BlackRock to maintain market share, impacting profit margins. |

| Demand for Sophistication | Clients seek specialized products like private markets and digital assets. | Requires BlackRock to innovate and expand its offerings to retain clients and prevent them from seeking specialized providers. |

Preview Before You Purchase

BlackRock Porter's Five Forces Analysis

This preview showcases the comprehensive BlackRock Porter's Five Forces Analysis you will receive immediately upon purchase, ensuring you get the exact, professionally formatted document. It delves into the competitive landscape, examining the threat of new entrants, the bargaining power of buyers and suppliers, the intensity of rivalry among existing competitors, and the threat of substitute products or services. Understand BlackRock's strategic positioning within the asset management industry through this detailed analysis, which is ready for immediate use without any alterations. What you see is precisely what you get—a complete and actionable business strategy tool.

Rivalry Among Competitors

Competitive Rivalry 1

The investment management landscape is intensely competitive, with BlackRock contending against formidable players like Vanguard, State Street Global Advisors, Fidelity Investments, Charles Schwab, and Morgan Stanley. These giants offer a broad spectrum of comparable investment products, including exchange-traded funds (ETFs), mutual funds, and comprehensive institutional portfolio management services. As of early 2024, the total assets under management (AUM) in the global ETF market alone surpassed $11 trillion, highlighting the sheer scale of this competitive arena.

Competitive Rivalry 2

The exchange-traded fund (ETF) market, a cornerstone of BlackRock's iShares business, is a battlefield of intense competition. Fee wars are a constant feature, with providers aggressively lowering expense ratios to attract assets. For instance, by early 2024, many broad-market ETFs had expense ratios at or below 0.03%.

New entrants and established players alike are relentlessly innovating, introducing novel ETF structures and thematic products to capture investor interest. This constant stream of new offerings fuels fierce competition for market share, forcing BlackRock to continuously adapt its product development and pricing strategies to remain a leader.

Competitive Rivalry 3

BlackRock's Aladdin, a powerful risk management platform, encounters significant competition from a growing number of financial technology firms. These competitors are actively developing and offering alternative solutions that aim to provide similar, or even superior, capabilities in areas like portfolio management, trading, and risk analysis. The competitive landscape is dynamic, with new entrants and established players constantly innovating to capture market share.

Maintaining Aladdin's leadership position hinges on BlackRock's commitment to ongoing technological advancement and feature enhancement. Failing to innovate could lead to client attrition as users seek more cutting-edge or cost-effective alternatives. For instance, as of early 2024, the fintech sector continues to see substantial investment, with many firms focusing on AI-driven insights and cloud-based scalability, directly challenging existing platforms.

Competitive Rivalry 4

Competitive rivalry in the asset management sector is heating up, particularly with the growing emphasis on Environmental, Social, and Governance (ESG) investing. Firms are increasingly allocating significant capital to sustainable finance strategies. For instance, by the end of 2023, BlackRock reported that its iShares ESG ETFs had seen substantial inflows, reflecting this trend. This shift means that companies are not just competing on traditional financial returns but also on their commitment and demonstrable progress in ESG metrics.

Investor expectations are evolving, demanding a dual focus on strong financial performance underpinned by robust data analytics and clear ESG-driven results. This necessitates a sophisticated approach to data integration and reporting. Many leading asset managers, including BlackRock, are investing heavily in AI and advanced analytics to identify ESG opportunities and manage risks effectively. The ability to demonstrate tangible positive impact alongside financial gains is becoming a key differentiator.

- ESG Integration: Asset managers are embedding ESG factors into their investment processes, leading to increased competition for ESG-focused talent and proprietary data.

- Data Analytics: Firms leveraging advanced data analytics to identify ESG alpha and manage portfolio risk are gaining a competitive edge.

- Investor Demand: A significant portion of new investment capital is flowing into ESG-aligned funds, pressuring all market participants to adapt.

- Resource Allocation: Major players like BlackRock and Invesco are visibly increasing their budgets and strategic focus on sustainable investment products and research.

Competitive Rivalry 5

BlackRock actively manages competitive rivalry by differentiating its offerings. By integrating public and private markets and expanding into digital assets, the firm aims to capture new client demands and stay ahead of competitors. This strategic expansion, exemplified by acquisitions like GIP and HPS, strengthens its market position.

The competitive landscape for BlackRock is intensified by players offering similar asset management services. However, its strategic moves, such as the acquisition of Global Infrastructure Partners (GIP) for approximately $12.5 billion in early 2024, underscore a commitment to broadening its capabilities and capturing a larger share of the growing private markets, a segment experiencing significant client interest.

- BlackRock's integration of public and private markets aims to offer a more comprehensive investment solution.

- Expansion into digital assets signals a proactive approach to evolving market trends and client needs.

- The acquisition of Global Infrastructure Partners (GIP) for roughly $12.5 billion in 2024 highlights strategic growth in alternative investments.

- Acquiring HPS Investment Partners further bolsters BlackRock's private credit capabilities, a key growth area in the current financial climate.

BlackRock's Triple Threat: ETF Fees, Fintech, ESG Competition

BlackRock faces intense rivalry from major asset managers like Vanguard and State Street, particularly in the rapidly growing ETF market where fees are a constant battleground, with many broad-market ETFs hovering around 0.03% expense ratios by early 2024. The firm also competes fiercely with fintech companies offering advanced risk management platforms, forcing continuous innovation in its Aladdin offering, especially as the fintech sector attracts substantial investment in AI and cloud solutions. Furthermore, the increasing demand for ESG investing means BlackRock must differentiate not only on financial returns but also on its sustainability credentials, a trend evidenced by significant inflows into its iShares ESG ETFs by late 2023.

SSubstitutes Threaten

1

Robo-advisors represent a substantial threat of substitutes, especially for individual retail investors. These platforms leverage automation and algorithms to deliver investment advice and manage portfolios, often at a fraction of the cost of traditional human advisors. The convenience and accessibility they offer appeal to a growing segment of the market, challenging established players.

The growth trajectory for robo-advisors is impressive. Projections indicate that assets under management by these automated services could reach a staggering $2.4 trillion by 2025. This rapid expansion underscores their increasing appeal and the potential for them to capture significant market share from traditional wealth management services.

2

The threat of substitutes for BlackRock, particularly from direct investing platforms, is significant. These platforms, like Robinhood or Charles Schwab’s self-directed accounts, empower individuals to manage their own investments, bypassing traditional asset managers. In 2024, the number of retail investors utilizing these platforms continued to grow, with many seeking lower fees and greater control over their portfolios.

This trend is fueled by increased financial literacy and a desire for cost-efficiency. For instance, the average expense ratio for actively managed ETFs in the U.S. was around 0.46% in early 2024, while many direct investing platforms offer commission-free trading for many securities, making them an attractive alternative for cost-conscious investors. This accessibility can divert potential clients, especially those who are confident in their ability to research and select investments independently.

3

The threat of substitutes for BlackRock's core offerings, primarily traditional public market investments, is significant and growing. Alternative investment vehicles like private equity, venture capital, and direct real estate investments offer diversification and potentially higher returns, attracting investors seeking options beyond stocks and bonds. For instance, global private equity assets under management reached an estimated $13.9 trillion by the end of 2023, demonstrating a substantial and growing market.

BlackRock itself recognizes this shift, actively expanding its presence in private markets to counter this threat. By developing and offering products in areas such as infrastructure, private credit, and real estate, BlackRock aims to retain investor capital that might otherwise flow to specialized alternative investment firms. This strategic move acknowledges that investors are increasingly looking for a broader spectrum of investment opportunities beyond public exchanges.

4

Cryptocurrency and other digital assets are emerging as potential substitutes for traditional investment vehicles. While still in their early stages, these assets could divert investment capital from conventional products as the market matures. For instance, the total market capitalization of cryptocurrencies, which stood around $1.6 trillion in early 2024, demonstrates a growing investor interest in alternative assets.

As digital assets gain broader acceptance and regulatory clarity, their appeal as substitutes for traditional investments like stocks and bonds may increase. This trend could challenge established financial products by offering different risk-return profiles and diversification benefits. The increasing institutional adoption, with some major financial institutions offering crypto-related services, signals a growing legitimacy for these digital assets.

The threat of substitutes is further amplified by the evolving nature of financial technology and investor preferences.

- Digital Assets as Substitutes: Cryptocurrencies and other digital assets present a growing alternative to traditional investments, offering a new avenue for capital allocation.

- Market Maturation and Acceptance: As the digital asset market matures and gains wider acceptance, it has the potential to attract significant capital away from conventional investment products.

- Investor Interest and Market Cap: The total market capitalization of cryptocurrencies, exceeding $1.6 trillion in early 2024, highlights a substantial and growing investor base for these alternative assets.

- Institutional Adoption: Increased involvement from major financial institutions in offering digital asset services further legitimizes these assets and enhances their substitutive potential.

5

The threat of substitutes for BlackRock's services is intensifying as investor preferences evolve. A notable trend, particularly evident in 2024, is the increasing demand for personalized financial advice and greater control over investment portfolios. This shift encourages clients to explore hybrid advisory models that blend human expertise with digital platforms, or entirely new financial planning methodologies, potentially bypassing traditional, large-scale asset management firms.

This evolving landscape means clients might seek out robo-advisors, direct indexing solutions, or even decentralized finance (DeFi) platforms as alternatives. For instance, the global robo-advisory market was projected to reach hundreds of billions of dollars by 2024, showcasing a significant appetite for tech-driven, lower-cost investment solutions that offer a high degree of customization and user control. This presents a direct challenge to the conventional asset management model.

- Growing demand for personalized advice: Investors increasingly want tailored strategies, not one-size-fits-all solutions.

- Rise of hybrid and digital platforms: Many prefer combining human interaction with technology for investment management.

- Emergence of alternative investment solutions: Robo-advisors and direct indexing offer competitive alternatives to traditional asset managers.

- Investor desire for control: Clients want more direct say and transparency in how their money is managed.

Market Evolution: The Rise of Investment Substitutes

The threat of substitutes for BlackRock's core business is multifaceted, encompassing technological advancements, evolving investor preferences, and the emergence of new asset classes. Robo-advisors and direct investing platforms offer lower-cost, more accessible alternatives for retail investors. Furthermore, alternative investments like private equity and digital assets are capturing investor capital, challenging traditional public market vehicles. The increasing demand for personalized advice and greater control over portfolios further fuels this trend.

| Substitute Category | Key Characteristics | Impact on BlackRock | Supporting Data (2024/2025 Projections) |

|---|---|---|---|

| Robo-Advisors | Automated, algorithm-driven advice; lower fees; high accessibility. | Diverts retail investor assets; pressure on traditional advisory fees. | Projected to manage $2.4 trillion by 2025. |

| Direct Investing Platforms | Self-directed trading; commission-free options; greater investor control. | Reduces reliance on intermediaries; appeals to cost-conscious and empowered investors. | Continued growth in retail investor participation, with many seeking lower fees. |

| Alternative Investments (Private Equity, VC, Real Estate) | Diversification; potentially higher returns; less correlation to public markets. | Attracts capital that might otherwise go to traditional assets; requires BlackRock to expand offerings. | Global private equity AUM estimated at $13.9 trillion by end of 2023. |

| Digital Assets (Cryptocurrencies) | New asset class; potential for diversification and high returns; evolving regulatory landscape. | Could divert investment capital; requires adaptation and potential integration into offerings. | Total crypto market cap exceeded $1.6 trillion in early 2024. |

Entrants Threaten

1

The threat of new entrants in the investment management sector, including BlackRock, is relatively low. Significant capital is needed to establish operations, manage diverse investment portfolios, and meet client demands. For instance, setting up a robust technological infrastructure and compliance framework alone can cost millions.

Furthermore, the industry is heavily regulated, with stringent licensing and compliance requirements varying by jurisdiction. Navigating these regulatory landscapes requires specialized expertise and substantial investment, acting as a considerable deterrent for newcomers. BlackRock, as a global leader, operates within this complex web, and new players must demonstrate a similar level of compliance from the outset.

Building established distribution networks and brand recognition is another major hurdle. BlackRock benefits from its extensive global reach and long-standing relationships with institutional investors and financial advisors. A new entrant would struggle to replicate this scale and trust quickly, making it difficult to attract significant assets under management (AUM) and compete effectively. As of Q1 2024, BlackRock managed over $10.5 trillion in AUM, a testament to its established position.

2

The threat of new entrants for BlackRock is relatively low, primarily due to the significant barriers to entry in the asset management industry. Building the brand recognition and trust that BlackRock, a firm with decades of history, commands is a formidable challenge for newcomers. For instance, as of the first quarter of 2024, BlackRock managed an impressive $10.5 trillion in assets, a testament to the deep-seated client relationships and proven track record it has cultivated.

New players find it incredibly difficult to attract significant assets and market share when competing against such established incumbents. The sheer scale and operational complexity required to manage vast portfolios, coupled with the need for robust regulatory compliance, also pose substantial hurdles. This means that while niche players might emerge, those capable of challenging BlackRock's position on a large scale are few and far between.

3

The threat of new entrants in the asset management industry, particularly for a firm like BlackRock, is somewhat mitigated by the significant capital and technological infrastructure required to compete effectively. Developing and maintaining sophisticated proprietary technology platforms, such as BlackRock's Aladdin, presents a substantial hurdle. This platform, which is central to BlackRock's operations and client offerings, represents years of development and billions in investment, making it incredibly difficult for newcomers to replicate.

The sheer scale of investment needed for a comparable risk management and investment technology platform is immense, encompassing not only software development but also the ongoing costs of data acquisition, cybersecurity, and specialized talent. For instance, in 2023, BlackRock reported approximately $10 billion in technology and transition risk spending, highlighting the ongoing commitment to maintaining its technological edge. This high cost of entry, coupled with the need for deep expertise in both finance and technology, significantly dampens the threat of new, well-funded competitors emerging to challenge established players like BlackRock.

4

The threat of new entrants for BlackRock, while present, is somewhat mitigated by the significant capital and regulatory hurdles required to replicate its scale and breadth of services. While robo-advisors have indeed lowered the initial cost for providing basic digital investment advice, building a platform that can effectively serve institutional clients, manage complex alternative asset classes, and navigate global regulatory landscapes demands substantial resources and expertise. For instance, the sheer operational complexity of managing trillions in assets under management (AUM), as BlackRock does, presents a formidable barrier that new, smaller players struggle to overcome. Many established financial institutions are also bolstering their own digital capabilities, further consolidating the market rather than creating openings for entirely new, disruptive entities at BlackRock's level.

Consider these points regarding new entrants:

- Capital Intensity: Launching a global asset management firm with BlackRock's product diversity and infrastructure requires billions in upfront capital, far beyond typical fintech startups.

- Regulatory Compliance: Navigating the intricate and evolving regulatory frameworks across multiple jurisdictions is a significant ongoing cost and expertise requirement that new entrants often lack.

- Brand Trust and Reputation: BlackRock benefits from decades of building trust, particularly with large institutional investors who prioritize stability and proven track records.

- Economies of Scale: BlackRock's vast scale allows for significant cost efficiencies in technology, operations, and distribution, which are difficult for smaller competitors to match.

5

The threat of new entrants for BlackRock is moderate. While the asset management industry has historically been accessible, significant capital requirements for technology, compliance, and talent act as a deterrent. For instance, establishing a robust compliance framework alone can cost millions, deterring smaller players.

Regulatory shifts can, however, create opportunities. Changes in disclosure rules for active Exchange Traded Funds (ETFs), for example, might lower barriers for specialized niche providers. Yet, the overall burden of adhering to global financial regulations, including those implemented in 2024 concerning ESG reporting and data privacy, remains a substantial hurdle, demanding significant investment and expertise that new entrants often lack.

- High Capital Investment: Launching a competitive asset management firm requires substantial upfront capital for technology infrastructure, marketing, and regulatory compliance.

- Regulatory Complexity: Navigating the intricate web of global financial regulations, including evolving rules on digital assets and sustainable investing, poses a significant barrier to entry.

- Brand Recognition and Trust: Established players like BlackRock benefit from decades of building trust and brand loyalty, which new entrants struggle to replicate quickly.

- Economies of Scale: BlackRock's massive scale allows for lower operating costs per dollar managed, creating a cost advantage that new, smaller firms find difficult to match.

Asset Management: High Barriers Protect Incumbents

The threat of new entrants into BlackRock’s market remains relatively low, primarily due to the substantial barriers inherent in the asset management industry. Significant capital is essential for building the necessary technology infrastructure, compliance frameworks, and distribution networks, making it difficult for newcomers to compete effectively. For example, BlackRock’s proprietary Aladdin platform represents billions in investment and years of development, a cost prohibitive for most aspiring firms.

Furthermore, the industry is heavily regulated, and compliance with global financial regulations, which continue to evolve with new mandates in areas like ESG reporting and data privacy, requires specialized expertise and significant ongoing investment. This stringent regulatory environment, coupled with the challenge of building brand trust and achieving economies of scale comparable to BlackRock’s $10.5 trillion in AUM as of Q1 2024, deters most potential new entrants from challenging established players on a large scale.

| Barrier to Entry | Impact on New Entrants | BlackRock's Advantage |

| Capital Intensity | Extremely High; requires billions for technology, operations, and talent. | Established infrastructure and ability to fund continuous innovation. |

| Regulatory Compliance | Complex and costly; requires deep expertise across multiple jurisdictions. | Extensive legal and compliance teams with proven track record. |

| Brand Trust & Reputation | Difficult to build; institutional investors prioritize stability and track record. | Decades of proven performance and deep client relationships. |

| Economies of Scale | Challenging to achieve; impacts cost efficiency in operations and distribution. | Lower operating costs per AUM, enabling competitive pricing and wider reach. |

Porter's Five Forces Analysis Data Sources

Our BlackRock Porter's Five Forces analysis is built upon a robust foundation of data, including BlackRock's own financial statements, SEC filings, and investor presentations. We also leverage industry reports from leading research firms and macroeconomic data to provide a comprehensive view of the competitive landscape.